Sample Category Title

Market Update – Asian Session: China Caixin PMI Assures Markets Of Growth

Headlines/Economic Data

General Trend: Asian equity markets trade mixed after earlier declines in the US

China Feb Caixin PMI Manufacturing index rises to 6-month high, despite decline seen in the official index

Aluminum Corp of China (CHALCO) said there was no ‘major’ information to be disclosed following its share price declines

Chinese aluminum and steel names under pressure as markets expect President Trump to announce 20 and 25% tariffs respectively

President Trump said to plan emergency meeting with steel and aluminum execs on Thursday

Meanwhile, China President Xi’s top economic adviser is expected to meet on Thursday with top Trump Administration officials, including Treasury Sec Mnuchin

BoJ dovish dissenter Kataoka reiterates more easing is needed

US dollar (USD) in focus ahead of Fed Chair Powell’s second day of testimony

Japan

Nikkei 225 opened -0.8%; closed -1.6%

TOPIX Iron & Steel Index -1.8%, Electric Appliances -1.6%

Japan mega-banks trade broadly lower, track earlier declines in the US financial sector

Automakers decline after Wednesday’s gain in the Yen

(JP) JAPAN Q4 CAPITAL SPENDING EX SOFTWARE: 4.7% V 2.7%E; CAPITAL SPENDING Y/Y: 4.3% V 3.0%E; Company Profits: 0.9% v 5.5% prior; Company Sales: 5.9% v 4.8% prior

Kawasaki Heavy,[-5.5%], 7012.JP Confirms quality problem with N700-Series Shinkansen car undercarriages

(JP) Japan final Feb PMI Manufacturing: 54.1 v 54.0 prelim

(JP) BoJ Gov Kuroda: Reiterates BOJ's easing has contributed to growth – parliament

(JP) BoJ Kataoka: Still 'quite distant' from mulling shift from easy policy, must ease more to achieve price goal quickly ; 2019 GDP likely to fall to 0.5-1.0%

(JP) Japan PM Abe: BOJ Gov Kuroda's policies have not been wrong to date, want him to keep working towards 2% target - parliament

(JP) Nikkei looks at how BOJ Gov Kuroda may not serve a full term after being reappointed

(JP) Japan MoF sells ¥2.3T v ¥2.3T indicated in 0.1% (prior 0.1%) 10-yr JGB; avg yield 0.062% v 0.088% prior; bid to cover 4.53x v 4.58x prior

Looking Ahead: Japan Jan Unemployment rate due for release on Friday, along with the Tokyo Feb CPI data

Fast Retailing [9983.JP] is scheduled to report Feb sales on Friday (prior figures came after the market close)

Korea

Kospi closed for holiday

SK Telecom, 017670.KR CEO Jung-ho: Working on wearable technology called “The Sleeve” that will be enabled by the fifth-generation telecom network with Nokia Bell Labs - Korean press

(KR) South Korea has submitted a document rebutting US trade group representing its pharmaceutical industry that Korea’s drug pricing policies favor its domestic industry - Korean press

(KR) South Korea Feb Trade Balance: $3.31B v $2.39Be; Exports y/y: 4.0% v 0.5%e; Imports y/y: 14.8% v 12.0%e

According to KDB GM Korea may have FY17 Net loss of KRW900B (4th consecutive year of losses) - Korean press

China/Hong Kong

Hang Seng opened -0.3%, Shanghai Composite +0.1%

Hang Seng Info Tech Index +2%, Energy -0.9%

Shanghai Composite Property index has moved between gains and losses

ASM Pacific Technology [522.HK] rises over 3% after reporting Q4 earnings

(CN) China National People’s Congress to start on March 5th, will set economic targets for the coming year; Expected to keep GDP growth near or above 6.5%; Proactive fiscal policy is expected to be maintained - Xinhua

(CN) China PBoC Open Market Operation (OMO): injects CNY150B in 7-day, 28-day and 63-day reverse repos v skipped prior; Net drains CNY10B

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.3352 V 6.3294 PRIOR

(CN) CHINA FEB CAIXIN PMI MANUFACTURING: 51.6 V 51.3E (6-month high)

(CN) China Securities Regulator (CSRC) said to have asked some funds to avoid net selling during National People's Congress, which may account for the selling seen this week - press

(HK) Macau Feb Casino Rev (MOP) 24.3B v 26.3B prior; Y/Y: +5.7% v 9.0%e

Australia/New Zealand

ASX 200 opened -0.4%; closed -0.7%

ASX 200 Energy Index -2.2%, Utilities -1.6%, Resources -1.6%, Consumer Discretionary -0.8%, Financials -0.5%

(NZ) New Zealand Q4 Terms of Trade Index Q/Q: 0.8% v 0.5%e

(AU) Australia Feb AiG Perf of Manufacturing Index: 57.5 v 58.7 prior

(AU) AUSTRALIA Q4 PRIVATE CAPITAL EXPENDITURE (CAPEX) Q/Q: -0.2% V 1.0%E; Equipment, plant, machinery investment +2.2% q/q; Buildings, structures investment -2.1% q/q; Sees 2017/18 Capex estimate +2.5% y/y; Australia companies plan to spend A$114.6B; Sees 2018/19 Capex estimate +3.5% y/y; Australia companies plan to spend A$84B

(NZ) New Zealand sells NZ$100M in 2.5% 2040 inflation indexed bonds; avg yield 2.1987%

(AU) Australia Prudential Regulatory Authority (APRA) Chairman Byres: 10% cap on bank lending to residential property investors was probably reaching the end of its useful life

(AU) Australia ACCC exec general manager of specialized enforcement Bezzi: As a general matter we are concerned about potential collusion in forex markets and we do have some investigations, that I am not able to go into in any detail, that touch on some of these issues - AFR

(AU) Australia Feb Commodity Index (AUD): 139.8 v 135.3 prior; Commodity Index SDR Y/Y: -1.0% v -0.6% prior

Other Asia

(TW) Taiwan Central Bank Gov Yang: NT$ gains help ease import driven inflation pressures; will take appropriate monetary policy to keep inflation stable

North America

US equity markets ended broadly lower: Dow -1.5%, S&P500 -1.1%, Nasdaq -0.8%, Russell 2000 -1.6%

S&P500 Energy -2.3%, Materials -1.8%

(VE) US Trump Administration Official: Does not rule out complete US oil embargo on Venezuela, says it would cause fairly strong shock to the oil market in the short-term

(US) US said to plan announcement on Thursday, Mar 1st related to steel and aluminum imports - US press

(US) SEC launches investigation into cryptocurrency, issued subpoenas and information requests to technology companies and advisers - financial press

(US) DOE CRUDE: +3.0M V +2ME

Looking Ahead: US Feb ISM Manufacturing PMI to be released

Europe

Carrefour [CA.FR]: Reports FY net -€531M v +€746M, Rev €88.2B v €85.7B y/y

Looking Ahead: UK Feb Manufacturing PMI due to be released

Levels as of 01:00ET

Nikkei225 -1.6%, Hang Seng -0.4%; Shanghai Composite +0.0%; ASX200 -0.7%, Kospi -1.2%

Equity Futures: S&P500 -0.3%; Nasdaq100 -0.2%, Dax -0.6%; FTSE100 -0.5%

EUR 1.2199-1.2184; JPY 106.87-106.55; AUD 0.7766-0.7717;NZD 0.7211-0.7187

Apr Gold -0.2% at $1,315/oz; Apr Crude Oil +0.0% at $61.66/brl; May Copper +0.3% at $3.14/lb

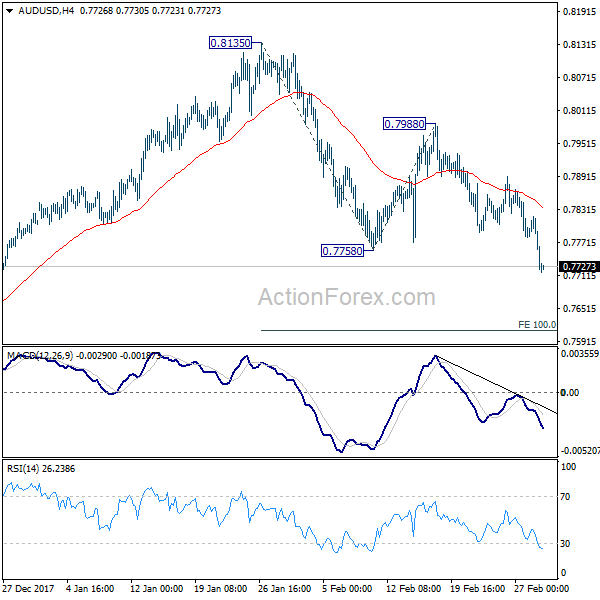

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7741; (P) 0.7780; (R1) 0.7799; More...

AUD/USD's strong break of 0.7758 confirm resumption of fall from 0.8135. Intraday bias back on the downside. Current fall should target 100% projection of 0.8135 to 0.7758 from 0.7988 at 0.7611. On the upside, break of 0.7988 resistance is needed to confirm completion of the fall. Otherwise, near term outlook will be mildly bearish even in case of recovery.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

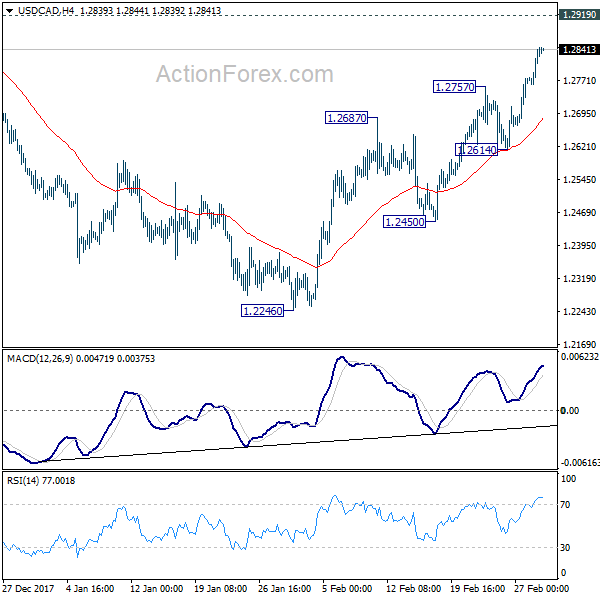

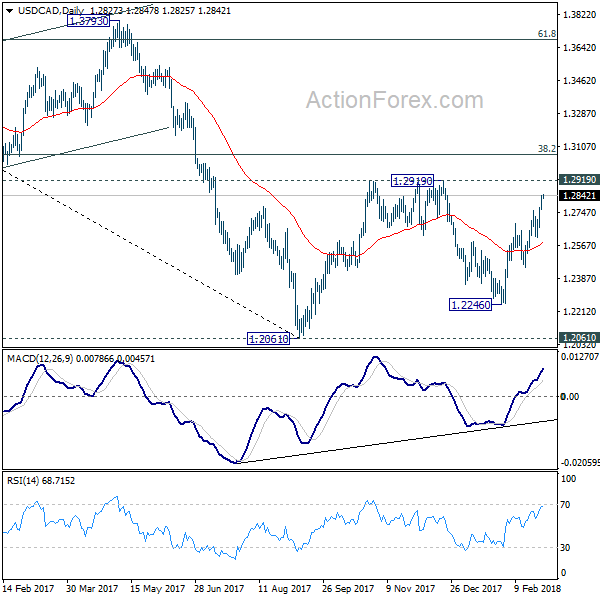

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2781; (P) 1.2811; (R1) 1.2861; More....

Intraday bias in USD/CAD remains on the upside as rebound from 1.2246 extends. Further rise should be seen to 1.2919 key resistance. We'd be cautious on strong resistance from there to limit upside. But a firm break there will carry larger bullish implication. On the downside, break of 1.2614 support is needed to signal completion of the rebound. Otherwise, outlook will remain cautiously bullish in case of retreat.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA (now at 1.2771), hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

USD/JPY Daily Outlook

Daily Pivots: (S1) 106.31; (P) 106.92; (R1) 107.27; More...

USD/JPY continues to stay in tight range and intraday bias remains neutral. On the upside, break of 108.27 will be the first sign of near term reversal and will target 110.47 resistance for confirmation. On the downside, below 106.37 minor support will bring retest of 105.54 low. Break of 105.54 will extend the larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

Australia’s Manufacturing Sector Growth Cooled In February

For the 24 hours to 23:00 GMT, the AUD declined 0.36% against the USD and closed at 0.7762.

LME Copper prices declined 1.1% or $75.0/MT to $6953.0/MT. Aluminium prices declined 0.6% or $14.0/MT to $2158.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7732, with the AUD trading 0.39% lower against the USD from yesterday's close, after overnight data revealed that Australia's AiG performance of manufacturing index dropped to a level of 57.5 in February, compared to a level of 58.7 in the previous month.

Elsewhere in China, Australia's largest trading partner, the Caixin/Markit manufacturing PMI unexpectedly climbed to a 6-month high level of 51.6 in February, defying market consensus for a fall to a level of 51.3. the PMI had recorded a level of 51.5 in the previous month.

The pair is expected to find support at 0.7693, and a fall through could take it to the next support level of 0.7654. The pair is expected to find its first resistance at 0.7795, and a rise through could take it to the next resistance level of 0.7858.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Annual Inflation Eased To A 14-Month Low Level In February

For the 24 hours to 23:00 GMT, the EUR declined 0.2% against the USD and closed at 1.2196, after data revealed that annual inflation in the Euro-zone slowed in February.

The Euro-zone's flash consumer price index (CPI) advanced 1.2% on an annual basis in February, in line with market expectations and rising at its weakest pace since December 2016, thus justifying the European Central Bank's cautious approach in unwinding its policy stimulus, despite growth exceeding expectations. In the previous month, the CPI had registered a rise of 1.3%.

Separately, Germany's seasonally adjusted unemployment rate remained steady at a record low of 5.4% in February, as widely expected. On the contrary, the nation's GfK consumer confidence index dropped more-than-estimated to a level of 10.8 in March, compared to market expectations for a fall to a level of 10.9. In the prior month, the index had registered a reading of 11.0.

In economic news, the second estimate of US annualised gross domestic product (GDP) was revised lower to 2.5% on a quarterly basis in the final three months of 2017, compared to a rise of 3.2% in the prior quarter. The preliminary figures had recorded a rise of 2.6%. Moreover, the nation's pending home sales unexpectedly fell 4.7% on a monthly basis in January, hitting its the lowest reading since October 2014. Market anticipation was for pending home sales to rise 0.5%, following a revised flat reading in the previous month.

Other data revealed that the US Chicago Fed purchasing managers index eased more-than-anticipated to a level of 61.9 in February, marking a 6-month low level. The index had posted a level of 65.7 in the prior month, while investors had envisaged for a drop to a level of 64.1. On the other hand, the nation's MBA mortgage applications rebounded 2.7% in the week ended 23 February, compared to a fall of 6.6% in the prior week.

In the Asian session, at GMT0400, the pair is trading at 1.2196, with the EUR trading flat against the USD from yesterday's close.

The pair is expected to find support at 1.2173, and a fall through could take it to the next support level of 1.2149. The pair is expected to find its first resistance at 1.2231, and a rise through could take it to the next resistance level of 1.2265.

Going ahead, traders would keep a close watch on the final Markit manufacturing PMI for February, scheduled to release across the Euro-zone. Additionally, the region's unemployment rate data for January, will also be eyed by traders. Later in the day, the US initial jobless claims, personal income and spending data, both for January, followed by the ISM and the final Markit manufacturing PMIs for February as well as construction spending data for January, all would garner a lot of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

UK Must Speed Up Brexit Negotiations In Order To Reach A Deal This Year, Warns Michel Barnier

For the 24 hours to 23:00 GMT, the GBP declined 1.0% against the USD and closed at 1.3757, as Brexit talks with the European Union’s (EU) hit another stumbling block, after the UK Prime Minister, Theresa May, rejected EU’s draft of Brexit withdrawal agreement.

The EU suggested to keep British-ruled Northern Ireland in a customs union if a solution to the border dispute cannot be found.

Additionally, EU’s chief negotiator, Michel Barnier, warned that a Brexit transition deal was not guaranteed and that negotiations on a post-Brexit transition period had confirmed “significant divergences”. Further, he added that Britain must accelerate the pace of talks if it wants a deal this year.

In the Asian session, at GMT0400, the pair is trading at 1.3759, with the GBP trading marginally higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3696, and a fall through could take it to the next support level of 1.3633. The pair is expected to find its first resistance at 1.3869, and a rise through could take it to the next resistance level of 1.3979.

Going ahead, traders would focus on UK’s net consumer credit and mortgage approvals data both for January coupled with the Nationwide house prices data for February, all slated to release in a few hours, will be on investors’ radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japan’s Manufacturing Sector Activity Fell Less Than Initially Estimated In February

For the 24 hours to 23:00 GMT, the USD declined 0.59% against the JPY and closed at 106.63.

In the Asian session, at GMT0400, the pair is trading at 106.69, with the USD trading 0.06% higher against the JPY from yesterday's close.

Overnight data revealed that Japan's final Nikkei manufacturing PMI dropped to a level of 54.1 in February, less than a preliminary print indicating a fall to a level of 54.0. The PMI had recorded a level of 54.8 in the previous month.

Early morning data showed that the nation's consumer confidence index surprisingly slid to a level of 44.3 in February, compared to a reading of 44.7 in the previous month, and defying market anticipations for a rise to a level of 44.8.

The pair is expected to find support at 106.40, and a fall through could take it to the next support level of 106.10. The pair is expected to find its first resistance at 107.14, and a rise through could take it to the next resistance level of 107.58.

Moving forward, Japan's jobless rate for January, set to release overnight, will be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

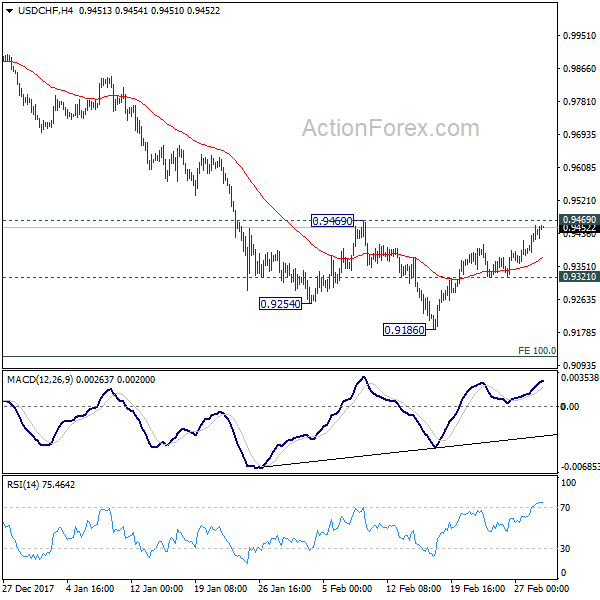

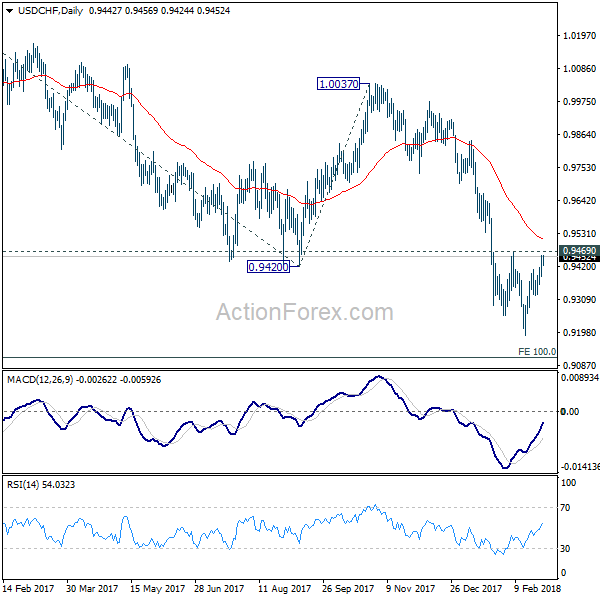

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9401; (P) 0.9429; (R1) 0.9474; More...

Despite the strong rebound from 0.9186, USD/CHF is still staying below 0.9469 resistance. Intraday bias remains neutral first. On the upside, considering bullish convergence condition in 4 hour MACD, break of 0.9469 will indicate near term reversal and turn outlook bullish for 55 day EMA (now at 0.9511) and above. On the downside, below 0.9321 minor support will bring retest of 0.9186. Break there will extend the larger down trend to 0.9115 medium term projection level next.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

Swiss ZEW Economic Expectations Index Deteriorated In February

For the 24 hours to 23:00 GMT, the USD rose 0.46% against the CHF and closed at 0.9444.

Macroeconomic data indicated that the ZEW economic expectations index in Switzerland fell to a level of 25.8 in February, compared to a reading of 34.5 in the previous month.

On the other hand, the nation’s KOF economic barometer registered an unexpected rise to a level of 108.0 in February, confounding market expectations for a fall to a level of 106.0. The index had recorded a revised reading of 107.6 in the previous month.

In the Asian session, at GMT0400, the pair is trading at 0.9449, with the USD trading 0.1% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9406, and a fall through could take it to the next support level of 0.9363. The pair is expected to find its first resistance at 0.9475, and a rise through could take it to the next resistance level of 0.9501.

Ahead in the day, traders would look forward to Switzerland’s 4Q GDP, real retail sales and manufacturing PMI data.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.