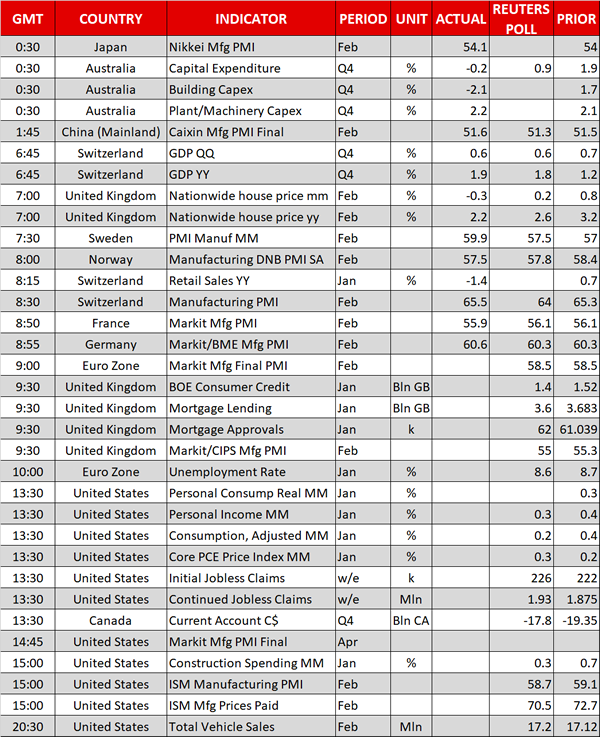

Sample Category Title

Equities In Red And USD Better Bid Ahead Of Powell Testimony And PCE Inflation

Market nervousness rises ahead of PCE inflation and Powell testimony

The Fed's favourite measure of inflation for the month of January, the core personal consumption measure or Core PCE, is due for release this afternoon. The tension is mounting among investors as this indicator is closely monitored by the Fed and could therefore influence significantly the path of monetary policy in the US. Indeed, the publication of January's CPI sparked strong reactions across financial markets as market participants adjusted their positions for a stepper path of interest rate. The headline PCE is expected to have remained stable at 1.7%y/y in January, while the core measure should come in at 1.5%y/y.

The second key event of the day is the testimony of Fed chair Powell before the Senate banking committee. We believe that Powell will be keen to soften its hawkish stance regarding the US economy. During a congressional testimony, Powell suggested that the Fed could increase borrowing rates four times this year, compared to three hikes expected by market participants and signalled by the central bank so far.

So what can investors should expect from this day? On the one hand, an upside surprise in inflation could definitely trigger a dollar; however, as discussed yesterday, higher interest rates could slowly dampen US growth against the backdrop of a leveraged private sector and an already stretched federal budget. On the other hand, Powell may use a more dovish tone today during his Senate hearing. Therefore, we believe that all-in-all the risk is skewed to the downside for the US dollar.

EUR/USD is currently trading around the bottom of its monthly range. A break of the strong 1.2165 support will open the door towards 1.20, then 1.1916 (low from January 9th). On the upside, a first resistance can be found at around 1.2350 (previous highs), then 1.2555 (high February 16th).

Indian growth wonders

Indian quarter (October – December) Gross Domestic Product published on Wednesday provided Prime Minister Narendra Modi with a big relief, given at 7.20% (consensus at 6.90%) against July-September and April – June quarters at 6.30% and 5.70%, making it the largest quarterly growth of the year. India becomes the fastest growing economy in relative numbers (India and China GDP 2017: 7.10% and 6.80%), as China starts seeing signs of slowdown in consumption and manufacture (January CPI at slowest pace since July 2017, PPI lowest rate since November 2016 and Manufacturing PMI low since July 2016).

Indian Sensex declines though the release, valued at 34'153 (-0.56%) along world equity indexes decline.

EUR/USD – Euro Takes Breather After Recent Slide

The euro is unchanged in the Thursday session, after considerable losses this week. Currently, EUR/USD is trading at 1.2188, down 0.05% on the day. Om the release front, the focus is on manufacturing PMIs, which performed well in Germany and the eurozone. German Manufacturing PMI dipped to 60.6, above the estimate of 60.3 points. It was a similar trend for the eurozone indicator, which dropped to 58.6, just above the estimate of 58.5 points. In the US, there are a host of key events, led by unemployment claims and personal spending. As well, Fed chair Jerome Powell testifies before the Senate Banking Committee. On Friday, Germany releases Retail Sales and the US publishes UoM Consumer Sentiment.

Jerome Powell is barely settled in his new office, but it’s been an eventful few weeks for the new Federal Reserve chair. Powell was greeted by a sharp correction in US stock markets, as investors headed for the hills on fears that the Fed might accelerate its pace of rate hikes if inflation moves higher. On Tuesday, Powell testified before a congressional committee, and will speak before the Senate Banking Committee on Thursday. Powell’s message to Congress was decidedly hawish, as the Fed chair said that the current policy of gradual rate increases would continue. He added that the economy was strong and that he expected inflation to move up to the Fed target of 2 percent. Importantly, Powell did not address the question of an acceleration of rate hikes, but his hawkish stance has increased the likelihood that the Fed will increase it projection from three to four rate hikes this year.

Inflation in eurozone edged lower to 1.2% in February, down from 1.3% in January. This reading met expectations, but underscores that inflation levels remain well below the ECB target of around 2 percent. Economic growth has rebounded, led by a robust German economy. Still, there is plenty of slack in the eurozone economy and the ECB is not under pressure to tighten policy. The Bank will meet on March 8, and major changes are expected. Policymakers could deliberate the possibility of removing the Bank’s easing bias towards increasing bond purchases if needed. A removal of the easing bias would likely be interpreted as a plan to tighten policy and would be bullish for the euro.

Technical Outlook: AUDUSD Extends Weakness After Taking Out Key Supports

The pair continues to trend lower and extends weakness from 0.7893 (26 Feb lower top) into third straight day.

Wednesday’s close below key supports provided by 200/100SMA’s and daily cloud base was strong bearish signal which was boosted by today’s extension through 0.7743 (Fibo 61.8% of 0.7500/0.8135 ascend), after weak

Australian data overnight further inflated bears.

Round-figure support at 0.7700 is now under pressure, with the pair capable of travelling to 0.7650 (Fibo 76.4% of 0.7500/0.8135).

Daily techs in firm bearish setup support, with slow stochastic continuing to head south in deep oversold territory and so far lacking any signal of recovery.

Senate testimony of Fed Chairman Powell due later today could be another risk for the Aussie, as previous testimony was quite hawkish and boosted the greenback.

Broken former key supports at 0.7780/0 zone (100/200SMA’s / daily cloud base) now act as strong resistances which should keep the upside protected.

Res: 0.7743, 0.7780, 0.7790, 0.7825

Sup: 0.7700, 0.7650, 0.7617;0.7583

Technical Outlook: USDJPY – Hopes For Stronger Recovery While 106.37 Holds But Overall Bias Remains Bearish

The pair trades in narrow consolidation on Thursday, following previous day's fall, which found footstep above Monday's low at 106.3.

Scope for stronger recovery remains in play while the price holds above 106.37 support, however, daily techs in firm bearish setup keep the downside at risk.

Today's action was so far capped by 10SMA (106.92), with firm break above 10 SMA and 107 barrier (daily Tenkan-sen) required to generate fresh bullish signal for extended recovery.

Conversely, loss of 106.37 handle (also near Fibo 61.8% of 105.54/107.90 recovery leg) would generate bearish signal and risk return to 105.54 (16 Feb low).

Res: 106.90, 107.00, 107.52, 107.67

Sup: 106.54, 106.37, 106.10, 105.54

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2208

The overall bias remains bearish, for a slide towards 1.2090 major support. Key resistance lies at 1.2270.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2270 | 1.2460 | 1.2160 | 1.2160 |

| 1.2350 | 1.2560 | 1.2090 | 1.2090 |

USD/JPY

Current level - 106.80

Allow an intraday dip to 106.00 area before bouncing back towards 107.60, en route to 108.30.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 107.00 | 108.30 | 106.50 | 105.40 |

| 107.60 | 110.40 | 106.00 | 102.40 |

GBP/USD

Current level - 1.3759

The downtrend is intact, heading towards 1.3620 support area. Initial resistance is projected at 1.3850.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3850 | 1.4280 | 1.3700 | 1.3620 |

| 1.4070 | 1.4340 | 1.3620 | 1.3620 |

EUR/USD Confluence Zone is 1.2163-1.2178

EUR/USD dropped more than 140 pips after the Head and Shoulders pattern neckline break. Subsequently, the descending channel has been formed, and at this point, the pair is stuck around D H3 / W H4 camarilla pivot. 1.2163-78 is the critical POC zone. Rejections above could spike the pair towards 1.2207, and 1h close above should provide a continuation towards 1.2222 and 1.2246. However, 1.2246-50 is a powerful confluence zone due to D H5 / W L3 resistance, and we might see selling from this zone towards 1.2207 retest.

However, a break below 1.2163 provides bearish continuation towards 1.2139 and 1.2118.

W H3 -Weekly Camarilla Pivot (Weekly Interim Resistance)

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

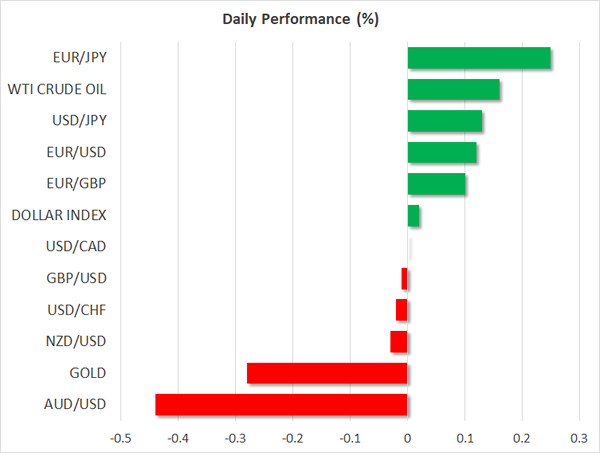

Dollar Hits 6-Week High Ahead Of Powell, Trade Tariffs And Key US Data Eyed

Here are the latest developments in global markets:

FOREX: The dollar recorded a six-week high versus a basket of currencies ahead of Fed chief J. Powell’s hearing before the Senate Banking Committee and key data out of the US. The aforementioned high came mostly on the back of gains from previous days though, as the dollar index was little changed on the day.

STOCKS: US markets closed lower once again yesterday, ending February on an uncertain note. The Dow Jones led the way lower, tumbling by 1.5%, while the S&P 500 fell 1.1%. The Nasdaq Composite declined by 0.8%. Futures tracking the Dow, S&P and Nasdaq 100 are all currently in positive territory, but only marginally so. Overall, the wild price swings in these indices have continued in recent days, which indicates that stock investors remain quite cautious still. Japanese indices took their cue from their American counterparts and tumbled as well, with the Nikkei 225 and Topix indices both falling by 1.6%. In Hong Kong, the Hang Seng was up by 0.3%. In Europe, futures tracking all the major indices were flashing red, signaling that these benchmarks may open lower today.

COMMODITIES: In energy markets, oil prices rose marginally today, recovering some of the notable losses they posted yesterday following the weekly EIA inventory data. Crude stockpiles rose by more than anticipated, enhancing concerns that the rapid rise in US production may be finally showing up. Besides inventories, oil prices were probably also pressured by the rebound in the US dollar yesterday, as well as the broader decline in equity markets, which usually weighs on risk-sensitive commodities like oil. In precious metals, gold was 0.3% lower today, with the latest pullback likely being owed to the recovery in the greenback.

Major movers: Dollar at multi-week high ahead of Powell hearing and busy data day; euro and sterling consolidate losses; aussie at 2-month low

The dollar index touched 90.74 earlier on Thursday, this being its highest since January 19. The “milestone” though was for the most part attributed to advancing from previous sessions, with the index little changed on the day.

Fed chief J. Powell’s optimism on the economy in his comments on Tuesday led market participants to revise their rate hike projections, now expecting a more “aggressive” Fed in terms of tightening policy. This in turn boosted the greenback.

Rising expectations for a higher interest rate environment though are weighing on stocks, with major Wall Street indices recording notable declines for the second straight day on Wednesday. Powell’s hearing before the Senate Banking Committee later on Thursday might give him the opportunity to clarify certain of the comments made a couple of days ago, and in a way “endorse” or not the market’s interpretation of his remarks. It remains to be seen whether more equity blood is on the horizon.

Besides Powell’s hearing, other key data are on the agenda during Thursday’s trading, including figures on consumption and the core PCE price index, the Federal Reserve’s preferred inflation measure.

Dollar/yen was up by 0.1% at 106.82. It is interesting that the US currency has posted notable gains relative to majors recently with the exception of the yen. Uncertainty over equity markets in conjunction with the Japanese currency’s perceived safe-haven status is one of the factors contributing to this.

The euro was up 0.1% versus the dollar at 1.2208, after touching 1.2182 earlier in the day, its lowest since January 18. It is noteworthy that euro/yen touched a six-month low of 129.84, though the pair was 0.25% up at 130.39 at 0732 GMT. February’s flash inflation figures undershooting the ECB’s target by a large margin are weighing on expectations for further policy tightening by the central bank, while risk events including Sunday’s Italian elections are looming.

Pound/dollar was little changed at 1.3757, falling as low as 1.3740, a level last experienced on January 16. The pair declined significantly yesterday, as Brexit uncertainty is acting as a drag on sterling. UK PM Theresa May said on Wednesday that the EU’s draft legal text would undermine Britain and threaten its constitutional integrity. This development further complicates discussions. Euro/pound was 0.1% up, recording a two-week high of 0.8876.

The aussie was 0.45% down versus its US counterpart at 0.7726. At its lowest it touched 0.7714, a level last seen around two-months ago. Disappointing data on Australian business investment contributed to weakness in the currency. Kiwi/dollar was not much changed at 0.7207.

Day ahead: Powell testifies again; Trump set to introduce new tariffs; raft of key US data on the agenda

The economic calendar is packed with key releases today, most notably out of the US. Also attracting interest in the US will be a testimony by Fed Chair Jerome Powell, this time before the Senate, as well as a potential announcement by the White House regarding new tariffs on steel imports.

In the UK, the manufacturing PMI for February is due out at 0930 GMT. The index is anticipated to slip to 55.0 from 55.3 previously, signaling that the sector may have lost some momentum lately. Another potential market mover for the British pound may be any Brexit updates, in light of the notable developments yesterday and ahead of UK PM Theresa May’s keynote Brexit speech tomorrow. It is not uncommon for such major speeches to be leaked to the media ahead of time, perhaps as early as today.

In the Eurozone, the unemployment rate for January (1000 GMT) is anticipated to tick down to 8.6%, from 8.7% prior.

Turning to the US, new Fed Chair Jerome Powell will be testifying before the Senate Banking Committee (1500 GMT). His introductory remarks will be identical to Tuesday’s, but markets will still pay close attention to the Q&A session, in case he touches on something new. Considering how optimistic he was perceived as being on Tuesday, the risks surrounding the dollar from his remarks today may be asymmetrical. More hawkish comments would be no surprise to anyone, and are thus unlikely to push the greenback meaningfully higher. The surprise would be if he changes tune and appears more cautious, which could lead to a notable tumble in the greenback.

In terms of trade, media reports suggest that the White House is set to announce steep tariffs on steel and aluminum imports today. If these reports are accurate, this would mark yet another step towards an escalation in global trade tensions. In terms of market action, such tariffs could prove harmful for the currencies of nations that export steel and aluminum to the US, such as China, Canada and Mexico. The Australian dollar may be also negatively impacted, considering the currency’s sensitivity to changes in risk sentiment and developments in China.

Turning to US data, the core PCE price index for January will probably attract the most attention (1330 GMT), as it is the Fed’s preferred inflation measure. The yearly rate is projected to hold steady at 1.5%, but considering the upside surprise in the core CPI rate for the same month, investors may be looking for a similar reaction in this indicator as well. At the same time as the core PCE print, the US will also release its personal income and spending data for January, both of which are anticipated to slow on a monthly basis. Later (1500 GMT), the ISM manufacturing PMI for February is due out and expectations are for the index to decline somewhat, but to still remain at an elevated level, consistent with robust expansion in the sector.

In Canada, current account data for the final quarter of 2017 are due out at 1330 GMT, while the Markit manufacturing PMI for February will be released at 1430 GMT.

As for the speakers, besides Fed Chair Jerome Powell, New York Fed President William Dudley (voter) will also step up to the rostrum, at 1600 GMT. He is considered one of the most influential Fed officials and thus investors will look for any signals as to whether he would entertain the prospect of four rate hikes this year.

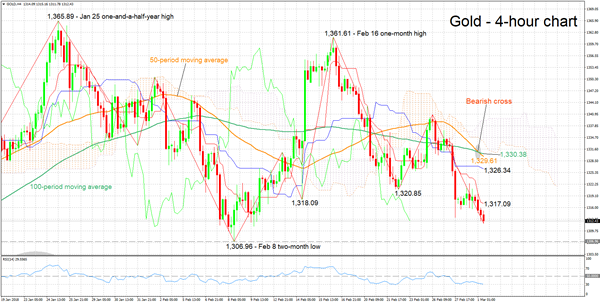

Technical Analysis: Gold posts three-week low; RSI oversold

Gold has notably declined, hitting a three-week low of 1,311.78 earlier on Thursday. The Tenkan- and Kjun-sen lines are negatively aligned, projecting a bearish picture in the short-term. The RSI which is falling adds to the view for negative momentum. Notice though that the indicator has marginally moved below the 30 oversold level; a rebound in the short-term is not to be ruled out.

A stronger US currency – for example on the back of hawkish comments J. Powell or strong US data later today – is expected to lead to additional weakness in the dollar-denominated precious metal, with the area around the two-month low of 1,306.96 from February 8 coming into view as potential support.

A weaker dollar on the other hand, could lend support to gold. In this case, resistance might come around current level of the Tenkan-sen at 1,317.09. Notice that the range around this level also encapsulates a couple of bottoms from the recent past, perhaps increasing its significance.

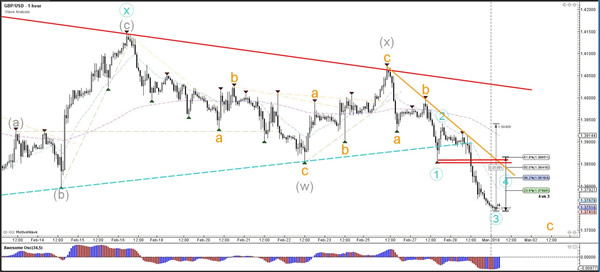

Technical Outlook: GBPUSD Consolidates After Strong Fall Previous Day, Outlook Remains Negative

Cable holds within tight consolidation in early Thursday’s trading after suffering heavy losses on Wednesday, which resulted in cracking key supports at 1.3780/64 (55SMA / 09 Feb low) and break into rising daily cloud.

Sterling remains under pressure on stronger dollar and Brexit concerns and could extend lower after bearish signals were generated on Wednesday’s close below former key supports.

Also, formation of failure swing on daily chart is negative signal, which could spark further weakness and harm broader longs.

Bearishly aligned daily techs (MA’s in bearish setup / 14-d momentum in negative territory and Wed’s long bearish candle weighing) work in favor of extension of bear-leg from 1.4069 (26 Feb lower top) towards 1.3703 (daily cloud base), to generate fresh bearish signal.

Broken 55SMA marks initial resistance at 1.3780, with daily cloud top (1.3841) expected to cap upticks.

Key events for sterling today are release of UK Manufacturing PMI (Feb f/c 55.1 vs 55.3 in Jan) and meeting of UK PM Theresa May with the chairman of EU leaders Donald Tusk.

Res: 1.3780, 1.3841, 1.3856, 1.3916

Sup: 1.3742, 1.3703, 1.3674, 1.3618

Daily Wave Analysis: EUR/USD Reaches Bounce Or Break Spot At 1.22 Support Zone

Currency pair EUR/USD

The EUR/USD is trying to break below the previous bottom (green) but the bearish price action is mild and candles are small. The support zone and the 50% Fibonacci level of wave 4 (pink) is a key decision level for a bullish bounce or bearish breakout. A bearish break makes a wave 4 (purple) pattern less likely.

The EUR/USD is probably building a wave 4 (orange) unless price breaks above the bottom of wave 1 (red line), which indicates a potential bullish breakout.

Currency pair GBP/USD

The GBP/USD broke belowthesupport (dotted blue) of the triangle chart pattern and reached the 61.8% Fibonacci level. This Fib is a new bounce or break spot.A bearish break invalidates the wave 4 (green) pattern.

The GBP/USD created strong bearish momentum yesterday which is most likely a wave 3 (blue), unless price breaks above the bottom of the wave 1 (red line).

Currency pair USD/JPY

The USD/JPY is probably in a wave 4 (blue) but price will need to break below support (blue) to confirm a wave 5 (blue) pattern.

The USD/JPY Is building a larger correction on the 1 hour chart.

GBPUSD Strongly Bearish Below 1.3765 Level

The British pound has fallen towards the key 1.3765 support level against the U.S dollar, as the European Union showed a hardened stance towards Brexit negotiations with the United Kingdom. The GBPUSD pair quickly fell through the 1.3800 support level yesterday, after the EU’s Chief negotiator Michel Barnier send a draft document presenting the possibility of suspending the UK’s access to the single market. Sterling traders now look towards the release of the United Kingdom’s February Manufacturing PMI and the key 1.3765 technical level.

The GBPUSD pair remains bearish whilst trading below the 1.3765 level, key intraday technical support is now found at the 1.3665 and 1.3612 levels.

Should GBPUSD price-action trade back above the 1.3800 level for an extended period, traders may test towards the 1.3838 and 1.3859 resistance levels.