Sample Category Title

Aussie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the AUD slightly rose against the USD and closed at 0.7837 on Friday.

LME Copper prices rose 0.6% or $41.5/MT to $7073.5/MT. Aluminium prices rose 0.7% or $16.0/MT to $2210.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7860, with the AUD trading 0.29% higher against the USD from Friday’s close.

The pair is expected to find support at 0.7820, and a fall through could take it to the next support level of 0.7779. The pair is expected to find its first resistance at 0.7885, and a rise through could take it to the next resistance level of 0.7909.

With no macroeconomic releases in Australia today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Annual Inflation Slowed As Initially Estimated In January

For the 24 hours to 23:00 GMT, the EUR declined 0.12% against the USD and closed at 1.2298 on Friday, after data confirmed that annual inflation in the Euro-zone slowed in January.

The Euro-zone's final consumer price index (CPI) rose 1.3% on an annual basis in January, confirming the preliminary print, thus indicating that inflation is shifting further away from the European Central Bank's (ECB) goal of just under 2.0%. In the previous month, the CPI had advanced 1.4%.

Separately, Germany's seasonally adjusted final gross domestic product (GDP) climbed 0.6% on a quarterly basis in the fourth quarter of 2017, in line with the flash print. The nation's GDP had recorded a rise of 0.8% in the previous quarter.

On Friday, the Federal Reserve (Fed), in its semi-annual Monetary Policy Report to the Congress, indicated that officials expect the ongoing strength in the US economy to warrant further gradual increases in the federal funds rate. Further, policymakers highlighted a pickup in inflation towards the end of last year.

In the Asian session, at GMT0400, the pair is trading at 1.2310, with the EUR trading 0.1% higher against the USD from Friday's close.

The pair is expected to find support at 1.2286, and a fall through could take it to the next support level of 1.2263. The pair is expected to find its first resistance at 1.2327, and a rise through could take it to the next resistance level of 1.2345.

Moving ahead, market participants would closely monitor a speech by the ECB President, Mario Draghi, due in a few hours. Additionally, the US new home sales data for January, slated to release later in the day, will be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Pound Rises On Hopes For A Post-Brexit UK-EU Trade Deal

For the 24 hours to 23:00 GMT, the GBP rose 0.09% against the USD and closed at 1.3969 on Friday, amid renewed hopes of a softer Brexit, following reports that the 11-member Brexit cabinet committee reached an agreement on a proposal for post-Brexit trade with the European Union.

In the Asian session, at GMT0400, the pair is trading at 1.3997, with the GBP trading 0.2% higher against the USD from Friday’s close.

The pair is expected to find support at 1.3932, and a fall through could take it to the next support level of 1.3866. The pair is expected to find its first resistance at 1.4036, and a rise through could take it to the next resistance level of 1.4074.

Going ahead, traders would look forward to UK’s BBA mortgage approvals data for January, slated to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Stronger Footing In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.11% against the JPY and closed at 106.71 on Friday.

In the Asian session, at GMT0400, the pair is trading at 106.56, with the USD trading 0.14% lower against the JPY from Friday’s close.

The pair is expected to find support at 106.27, and a fall through could take it to the next support level of 105.97. The pair is expected to find its first resistance at 107.03, and a rise through could take it to the next resistance level of 107.49.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Reverses Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.21% against the CHF and closed at 0.9360 on Friday.

In the Asian session, at GMT0400, the pair is trading at 0.9345, with the USD trading 0.16% lower against the CHF from Friday’s close.

The pair is expected to find support at 0.9328, and a fall through could take it to the next support level of 0.9312. The pair is expected to find its first resistance at 0.9368, and a rise through could take it to the next resistance level of 0.9392.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canada’s Annual Inflation Climbed Above Expectations In January

For the 24 hours to 23:00 GMT, the USD declined 0.47% against the CAD and closed at 1.2654 on Friday.

The Canadian Dollar gained ground against the USD on Friday, after Canada's consumer price index (CPI) rose more-than-estimated by 1.7% on an annual basis in January, compared to a gain of 1.9% in the previous month, while markets were anticipating for an advance of 1.5%.

In the Asian session, at GMT0400, the pair is trading at 1.2631, with the USD trading 0.18% lower against the CAD from Friday's close.

The pair is expected to find support at 1.2593, and a fall through could take it to the next support level of 1.2554. The pair is expected to find its first resistance at 1.2698, and a rise through could take it to the next resistance level of 1.2764.

In absence of any macroeconomic releases in Canada today, investor sentiment would be determined by global macroeconomic factors.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Nikkei 225 Index Is Up More Than 1%

Market movers today

The key focus for financial markets this year (and t rigger of the surge in market volatility) has been inflation and this week will by no means be different . On Wednesday , both preliminary core and headline HICP numbers for the eurozone are due out and on Thursday t he Fed's preferred inflation gauge, the PCE core inflation (and headline) numbers are due.

This morning, we are launching a one -week research series on inflation with a piece on global inflation pressures,.This will be followed by deep dives into inflation dynamics in the euro area, Scandi region and emerging markets, ending with FX and fixed income implications.

ECB President Mario Draghi is attending a hearing in the European Parliament at 15:00 CET: It is the first time in three weeks he will have spoken publicly and the second time since the January meeting. We doubt he will reveal new thoughts on the revisit of forward guidance, but as the hearing could be quite lengthy, we will watch out for any hints, also when he goes off script /introductory remarks.

In the US, speeches by St . Louis Fed President James Bullard and Fed Governor Randal Quarles are due, focusing on the state of the US economy

Selected market news

Market sentiment in Asia is positive following the rise in US stocks on Friday, where S&P 500 rose more than 1.5%. The Nikkei 225 index is up more than 1%. Asian currencies are also stronger versus the USD. One of the drivers of the positive market sentiment may be the lower US treasury yields with 10-year yields dropping toward 2.85% after touching 2.95% last week.

Certainly, financial markets will be on their toes looking for clues on US monetary policy today when Fed members Bullard and Quarles speak today followed by Fed Chair Powell 's hearing before the Financial Services Commit tee in Congress tomorrow. Prior to the Fed meeting in March, this is an opening for Powell to signal whether the Fed aims to do four rate hikes instead of three as signalled back in December in the latest project ions due to even more expansionary fiscal policy following the budget deal.

In China, the news agency Xinhua yesterday reported that the Cent ral Commit tee of the Communist Party has made a proposal to change the Constitution and remove the phrase that says the President can only sit for two terms (each five years). This paves the way for Xi Jinping being able to stay as President when his current term expires in 2023. With Xi Jinping most likely to stay in power for another ten years or even more, it means that the current Chinese economic reform path should be secured for the foreseeable future. The Chinese markets responded positively to the news this morning, although gains have faded a bit .

In the UK, the Labour Party said over the weekend that it wants Britain to seek a new customs agreement wi th the European Union after Brexit . This raises the pressure on Prime Minister Theresa May by leaving her at the mercy of t he ‘rebels' in her own Conservative Party, who also want such a deal with the bloc in contrast to Brexit hardliners.

Draghi Speech Eyed In Notable Week For Prominent Central Bankers

- Europe Poised For Decent Start After Week of Consolidation;

- Draghi, Powell and Carney Speeches in Focus This Week.

Europe Poised For Decent Start After Week of Consolidation

European equity markets are set to open around half a percentage point higher on Monday, taking a lead from Asia where markets also got the week off to a strong start.

This follows a week in which markets steadied themselves after a very volatile start to the month. Investors were left shocked earlier this month when stock markets went into a sudden tailspin, shedding more than 10% in a week and sending the VIX to levels not seen in more than two years in the process.

Higher inflation and interest rate expectations were blamed for the sharp sell-off following some more hawkish commentary from central banks and stronger economic data. While the situation has since settled down a lot and volatility has returned back to more normal levels, stocks remain around 5% off their highs in the US, more in Europe, while rates are not far from their recent highs.

Draghi, Powell and Carney Speeches in Focus This Week

This should make the week ahead all the more interesting as inflation figures will be released for the US and eurozone and we’ll also hear from a number of central bankers including the heads of the Federal Reserve, European Central Bank and Bank of England. ECB President Mario Draghi will get things underway on Monday with his appearance before the European Parliament this afternoon.

Draghi, Powell and Carney Speeches in Focus This Week

The ECB has long been preparing the markets for the end of bond buying and recent statements, minutes and comments from Draghi himself have indicated that the central bank intends to give plenty of warning of upcoming changes leading many to expect such a warning in the not too distant future. Draghi may therefore drop further hints on the timing of such a policy shift in today’s hearing which the euro will be particularly sensitive to.

Draghi will be followed later in the week by an appearance from BoE Governor Mark Carney who used his appearance in last week’s inflation reporting hearing to reaffirm the central banks desire to raise interest rates this year. The one not to miss this week though will be new Fed Chair Jerome Powell’s appearances before the House Financial Services Committee (Tuesday) and Senate Banking Committee (Thursday) as he lays out his plans for interest rates this year and beyond and we learn whether the central bank under his leadership will differ from that of Yellen’s.

Market Update – Asian Session: Equity Markets Strengthen As Yields Fall A Bit Lower, Chinese Home Prices Fall, China...

Headlines/Economic Data

General Trend: Asian equity markets open generally higher after Friday's gains in the US

Hang Seng supported by Chinese automakers

China confirmed move which could allow President Xi to remain in power indefinitely

Shanghai Composite Property Index declines over 3%, later pares some of loss: In Jan, China property prices rose in fewer cities vs prior month

Shanghai traded rebar steel futures rise over 1% following speculation of additional output cuts; US President Trump said to favor 24% global tariff on steel imports.

China Feb official Manufacturing and Non-Manufacturing PMIs due on Wed

Fed Chair Powell due to hold Congressional testimony on Tuesday Feb 27th and Thursday March 1st.

US Feb Nonfarm payrolls and Average Hourly Earnings due for release on Friday

Japan

Nikkei 225 opened +1.1%; closed +1.2%

TOPIX Real Estate Index +1%, Information & Communications +1.4%, Securities +1.2%

(JP) Japan PM Abe cabinet approval rating 56% v 55% prior - Nikkei

(JP) BoJ Gov Kuroda: Reiterates BoJ will persistently continue powerful monetary easing to achieve price goal

(JP) Japan Govt to set up 5 zones for promotion of offshore wind power by 2030,with certification for operators to last as long as 30-yrs - financial press

(JP) Unions for mega banks in Japan not expected to seek wage increase - Japanese Press

(JP) Japan Dec Final Leading Index: 107.4 v 107.9 prelim; Coincident Index: 120.2 v 120.7 prelim

Korea

Kospi opened +0.6%

Energy companies gain: Kumho Petro Chemical rises over 3%

Steel makers trade generally higher.

005935.KR Launched Galaxy S9 at a Barcelona mobile trade show, looks physically very similar to last year's model, many software upgrades

(KR) South Korea total financial firms assets under management (AUM) in 2017were KRW950T, +4.7% y/y, fresh record high - Korean press

(KR) South Korea sells 20-year bonds: avg yield 2.76% v 2.65% prior

Looking Ahead: Bank of Korea to hold policy decision on Tuesday (expected unchanged at 1.50%)

China/Hong Kong

Hang Seng opened -0.3%, Shanghai Composite +0.1%

Hang Seng Consumer Goods Index +1.3%, Materials +1.3%, Energy +1%, Property/Construction +0.4%, Financials+0.3%

Geely [175.HK] rises over 5% after announcing stake in Daimler

(CN) CHINAJAN PROPERTY PRICES M/M: RISE IN 52 OUT OF 70 CITIES V 57 PRIOR; Y/Y: RISE IN59 OUT OF 70 CITIES V 61 PRIOR; ChinaJan Avg New Home Prices M/M: -0.1% (1st decline in 32-months) v +0.5% prior; Y/Y: 5.4% v 5.8% prior

(CN) Communist Party has moved to repeal language from the constitution that says the head of state “shall serve no more than two consecutive terms”, which would allow China President Xi to stay in power indefinitely - Chinese press

(CN) China President Xi confidant Liu He saidto be a front runner to be next PBOC Gov – press

(CN) China CIRC orders three insurers to fixoverseas investment rule breaches – press

(CN) China Politburo statement: Reiterates Chinawill continue proactive fiscal policy and prudent monetary policy in 2018

USD/CNY (CN) PBOC SETS YUAN REFERENCERATE AT 6.3378 V 6.3482 PRIOR

(CN) China PBoC OMO: Injects CNY150B v CNY230B injected in 7-day, 28-day and63-day reverse repos prior; gross injection is equal to the net injection (3rdconsecutive day)

Great Wall Motor (+10%), 2333.HK Signs LOI with BMW for JV for new energy vehicle

(CN) China Standing Committee of the National People's Congress: To extend the preparation period for reforms that will change the stock listing system from approval-based to registration-based, for another two years to Feb 29th, 2020

Sinopec: Sees 2018 crude oil imports from the US at over 10M tons v 5.57M y/y

Australia/New Zealand

ASX 200 opened +0.1%; closed +0.7%

ASX 200 Telecom Index +1.1%, Energy +0.8%, REIT +1.1%, Financials +1.2%; Utilities -0.6%

Bluescope Steel [BSL.AU] rises over 4% as H1 profits beat ests

QBE Insurance, QBE.AU Reports FY17 (A$) Cash loss 258M v loss 215Me; Statutory net loss 1.25B* vloss 834Me

(AU) Australia sells A$400M v A$400M indicated in 2.75% Nov 21, 2027 bonds, avgyield 2.7735% v 2.6201% prior, bid to cover 5.96x v 3.46x prior

Looking Ahead: New Zealand Jan Trade Balance due to be released on Tuesday

Other Asia

(TW) Taiwan Central Bank Gov Chin-Long: Targeting to have financial and price stability; sees challenges from capital flows

Taiwanese chipmaker Nanya Technology [2408.TW] rises over 1%: Plans to spend $300M on plant in China, says Taiwanese press report

(SG) Singapore Jan Industrial Production M/M: 6.7% v 2.9%e; Y/Y: 17.9% v 7.5%e

North America

GE Planning to restate 2016, 2017earnings; FY16 EPS to be reduced by $0.13; FY17 EPS reduced by $0.16 - 10K

(US) Reportedly Pres Trump wants to set 24% global tariff on steel imports (inline with the Commerce Dept recommendations) – press (Friday)

Europe

(EU) ECB's Draghi reportedly is not happy with the lack of details about Latvia scandals - press

RealDolmen [REA.BE]: To be acquired by Gfi Informatique at €37.00/share for €196M

Looking Ahead: ECB Draghi expected to speak during NY morning

Levels as of 01:00ET

Nikkei225 +1.2%, Hang Seng +0.7%; Shanghai Composite +1.1%; ASX200 +0.7%, Kospi +0.1%

Equity Futures: S&P500 +0.1%; Nasdaq100 0.0%,Dax +0.2%; FTSE100 +0.1%

EUR 1.2325-1.2283; JPY 107.25 -106.44; AUD 0.7878-0.7829;NZD 0.7336-0.7277

Apr Gold +0.8% at $1,341/oz; Apr Crude Oil +0.4%at $63.81/brl; May Copper +0.5% at $3.24/lb

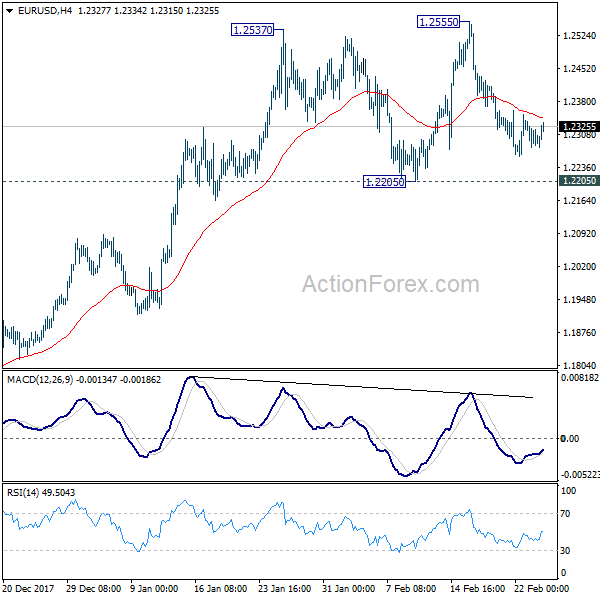

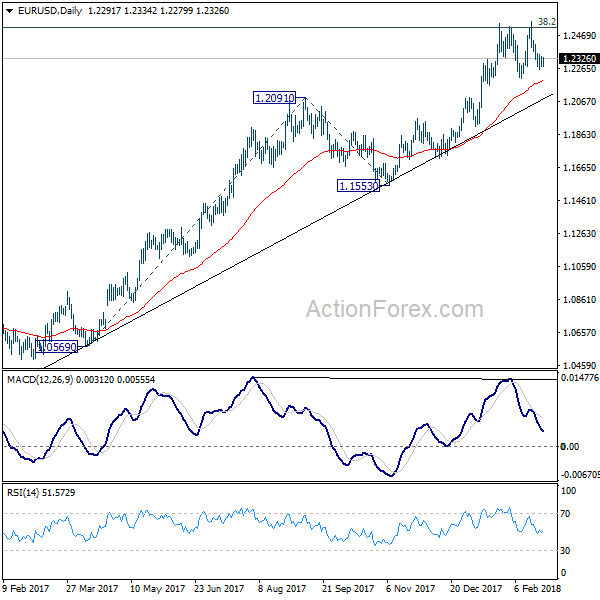

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2269; (P) 1.2303 (R1) 1.2327; More....

Intraday bias in EUR/USD remain neutral at this point. On the upside, break of 1.2555 will revive the bullish case of up trend resumption and target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075. However, break of 1.2205 will confirm rejection by 1.2516 key fibonacci level and trend reversal.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.