Sample Category Title

What’s GBPCAD Going To Do Here?

As shown in the weekly chart below, it looks as though something is on the horizon for GBPCAD as price lingers around some pretty heavy resistance.

We're presented with two possible scenarios – Price either gets rejected, or we see price breaking through resistance. Let's go down to a daily chart for further analysis.

It looks as though momentum has slowed significantly at our resistance area, which is holding for now. If price can break through our minor support area of 1.75ish we could possibly see a move to 1.73 where it would likely encounter more support, or even a further move through to the 1.68 area. A suitable stop loss area could be just above the recent high, presenting a good R:R ratio. The alternative possibility is that price breaks through resistance.

A New Sheriff In Town

The markets are increasingly challenging to define as storylines shift from ECB and BoJ policy normalisation to the problematic US twin deficits and inflation. However, the dollar has remained bid against most G10 currencies of late. As equity markest near another significant inflexion point as bond yields look poised to move higher, however, fixed income was exceedingly bid entering weeks end. Regarding an outright spark in Fixed income, which is driving the bus these days, there are no easy answers. Most are pointing to positioning adjustment ahead of the weekend and other events on the near horizon. Jerome Powells Humphrey Hawkins testimony and the Italian elections do strike a chord, while others point to growing signs that all is not doom and gloom in the bond pits and tactical buying is re-emerging.

Both economic and political worlds collide this week with the lion's share of attention falls on The New Sheriff in Town, Powell's testimony, however, I suspect we will end up with more emphasis on Europe and the Italian elections.

Let's face it, Italy is not known for political stability, as governments change about as often as the weather does. And on cue, protests have broken out across Italy over the weekend on both sides of the political spectrum. Expect a messy affair, and it will be difficult for any of the primary political parties to form a new government in what is shipping up to be one of the most unpredictable calls.Complicating matters is the high number of undecided votes which could be as high as 45% if current polls are accurate. And while xenophobia runs rampant amongst the electorate, political leader are easing their Euroskeptic perimeters so all may not as bad as it seems. Given Italy's history of encouraging coalition government, why should we expect anything different?Electoral shocks should be isolated, and the fear of political contagion should remain muted.

But let us not lose sight that On Friday, the postal ballot to ratify the Grand Coalition proposal with Merkel's CDU/CSU group ends. SPD members, who have the final say on the coalition agreement for Europe's largest economy, must vote by March 2 in a postal ballot, with results to be made public on March 4.

While the markets should get through these treacherous political storms, but obviously, it's wise to respect the fact that any failure to bring the EU political environment into equilibrium could send shockwaves through the union and beyond.

With so much hype over the new Fed Chair Powell's Humphrey Hawkins testimony, it's bound to disappoint. The bar is towering for a hawkish surprise as the prepared statement is likely to be salted with familiar FOMC repetition, similar to the recent FOMC Minutes for fear of sending equity market into a tailspin given the bearish bond market overtones.

There is no incentive for Powell to pre-signal any shift in the Fed narrative instead he will probably let traders do the Fed's heavy lifting this quarter as market risk is becoming more aligned to the reality that fiscal expansion could nudge US interest rates higher this year. With that said, there little to suggest this new Fed chair will be any less dependent on economic data than his predecessor, so the jury should remain out about a quicker pace of interest rate normalisation as the market remains comfortably parked in the three rate hike camp.

From the Fed's perspective, there is nothing gained by feeding the volatility beast. But no doubt, some skillfully placed partisan questions designed to trip up the new Chair during Q and A could be useful for a kneejerk or two.

Oil Markets

Markets are coming off whippy week for crude benchmarks, but conviction and sentiment should continue to rise after a surprisingly robust EIA drawdown in oil inventories However as briefly this may last, the stars are aligning for Oil bulls as U.S. oil production also remained flat while US exports surged. Also, momentum traders caught an updraft from yet another supply outage, this time from Libyan El Feel oilfield closure due to support workers wage disputes.

We continue to get positive news from OPEC compliance cementing the floor at WTI 60.00 per barrel which is creating a positive wave of conviction that investors appear keen to ride.

Uncertainty ahead of Powell testimony could lead to some position adjustments but unlikely to change the current bullish narrative.

From a technical perspective, with the futures markets in backwardation its suggests inventories could run leaner for some time but as we move deeper into global refinery maintenance season, US crude export could face some possible headwinds balancing each others impact.

Gold Markets

Gold continues to act as less of a haven hedge and more as a proxy for USD sentiment so we could be facing a critical week for Gold prices as the USD will come under the microscope as new Fed Chair Powell takes centre stage.

But with US's runaway deficit spending train stoking inflationary fears, Gold remains a crucial buy on dip strategy not only to hedge against inflation but also against another untimely correction in equity markets. With uncertainty surrounding the toxic elixir of higher inflation and the expected USD headwinds from record US debt, gold's appeal should remain healthy over the near term.

Currency Markets

On the surface, there is two-way risk heading into Powell's testimony, but likely nowhere near the level investors are positioning for a hawkish retort. But It would be a massive surprise if he departed from his predecessor script and we should expect a Yellen 2.0 delivery.

Fed Powell's testimony to the House Financial Services Committee has been moved up from Wednesday to Tuesday at 10:00 EST

In addition to this news, Bloomberg also confirms that his prepared remarks will be released at 8:30 EST Early release is not uncommon and allows both the markets and Congress to digest the statements,

Powell will then hold his Senate testimony on Wednesday.

There will be subtle nuances for the market to digest the day.While prepared remarks might help to establish how dovish or hawkish Powell is, many traders feel that Senators tend to ask more relevant questions for the market than the House. Therefore, the market might shade Tuesday's remarks with a bit of caution but will react after confirmation from Senate session on Wednesday.

However, given the policy mess Powell has inherited what should be crucial for the USD is how the Fed moves forward with the unenviable task of QE tapering while massive waves of Treasury notes come online. This burdening task should give the Chairman more cause to tow current policy lines while avoiding any hawkish surprises. Regardless, it's clear that most traders are preferring to wait until Powell's ” coming out” to re-engage with USD shorts in size.

Across the pond, ECB President Draghi will deliver his usual testimony to the European Parliament Monday. Softer economic data continues weighing on near-term sentiment, but political considerations dwarf all else.

G-10 Currencies

The British Pound

Most of this mornings focus has been on the pound after Sir Dave Ramsden sees a faster pace on interest rate normalisation. A bit of departure from usual decorum for a centeral banker to lay his cards on the table with regards to interest rates.But perhaps more significant, until now one of the most active doves on the Bank's monetary policy committee (MPC). But The general market drift is to fade GBP rallies into March EU summit given rate expectations are firmly entrenched, and hawkish expectations could leave GBP vulnerable to Brexit headline noise and the recent soft patch in data. So the markets are tentatively fading this morning opening move higher

The Japanese Yen

The Yen traded heavy on Friday, but with everyone watching the intraday support level at 106.60 on a closing basis, the pairs bounced off session lows into the close, finishing the week at 106.90. Although the reappointment of dovish Kuroda should keep YCC tweak rumours at bay, for now, the USDJPY was trading with higher sensitivity to US yields ahead of Powell testimony so it should be interesting to see if this holds true later in the week. But we expect today's session to be more about position prepping ahead of Powell testimony

While the focus is squarely on Jerome Powell this week, but with the recent decoupling of Yen's movements to US 10 year bond yields, the market could be looking for different triggers. While uncertainty over equity market keeps dollar bulls at bay, the USD selling requirements from exporters as we near Japanese fiscal year end and bond funds looking to adjust dollar hedges against the prospect of a broader US dollar sell-off could pressure the USDJPY despite the possibility of higher US interest rates. As we pointed out last week, the supply of dollars to go between 107.50 -90 remains large and while this continues to be the case, USDJPY shorts should stay in favour.

The Euro

It's tough trading the Euro with much conviction these days ahead of the Italian election as the market remains very wary of building longs ahead of the vote. And while the short-term market is favouring the propensity to sell EUR on rallies, the lack of downside break out makes jobbing the Euro even less appealing.

The Australian Dollar

The USD doesn't want to give it up yet, and while the small uptick in quarterly wage growth was encouraging for Aussie bulls, the markets quickly deduced this would not alleviate RBA's concerns. Overall the USD should continue to dominate near-term price action, but the prospects of another equity market wobble should keep topside Aussie momentum in check. But longer term and given the likely hood for dollar weakness to re-emerge as intense focus falls the duelling twin US deficits, interest rate differentials will be a less significant part of the equation, and the Aussie will outperform and a weaker USD narrative alone.

Asia FX

Stronger local FX and stable US treasuries are providing some breathing room for regional investors and providing a bit of a relief rally in equities. On the currency front, there was a rapid unwind of freshly minted US longs as regional capital market returned to form on the softer US yields.

The threat of US trade sanctions was brushed off as more bark than bite and had muted impact on markets

On the tariff and trade front Liu He, the Chief Economic advisor to the Gov and of the most potent advisors in the Politburo will visit Washington sometime between 27th Feb and March 2nd with their primary task of defusing trade agitation

The Malaysian Ringgit

Bonds are consolidating at current levels, but unless there a robust unexpected move in US rates this week, we should expect higher foreign interest as the local bond yields are at some attractive levels. The next MGS auction is Feb 27 where 3.5bioMYR go up for sale. With MGS 10y yields at 4.08 %, so long as US bond market remains in check, the MYR should get a boost from foreign demand given the attractive returns.

Oil prices should remain firm given OPEC's production cut compliance which should continue to provide a boost to the Ringgit's fortunes

The Chinese Yuan

Given the upcoming trade meeting in Washington, the Pboc will be more inclined to temper the RMB complex upside if the USD exhibits any strength this week. But local traders will likely remain in stasis ahead of The National People's Congress (NPC) will start on March 5. Premier Li will present a draft of his work plan for 2018 on March 5, which will be discussed and revised at the NPC.

The Philippine Peso

The current account weakness has been the primary driver of Peso's underperformance a surge in imports, which has led to a widening of the country's trade deficit and helped push the current account into the red. But with the markets more worried about the BSP falling behind the curve, shaving the countries RRR reinforced that sentiment and this has been the primary driver for the last leg of weakness. But with the Philippine central bank call to action last week by selling dollar to curb excessive peso volatility, perhaps the view of a hands-off central bank may be changing.But for those that follow my blog, you should know my long-standing belief when it comes to centeral bank intervention to curb local currency weakness; it accomplishes little more than eroding precious reserves while providing the market with better level to buy the dollar after the broader long USD Macro positions unwind.

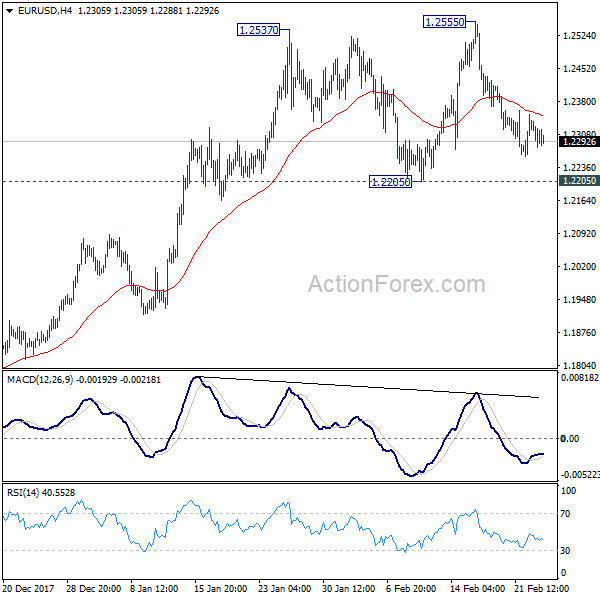

EUR/USD Weekly Outlook

EUR/USD still struggled to sustain above 1.2516 key fibonacci level and stayed in range last week. Initial bias remains neutral this week first. On the upside, break of 1.2555 will revive the bullish case of up trend resumption and target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075. However, break of 1.2205 will confirm rejection by 1.2516 key fibonacci level and trend reversal.

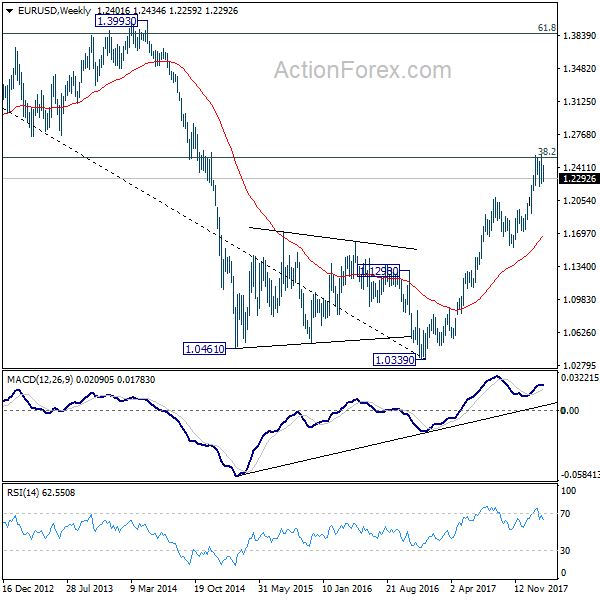

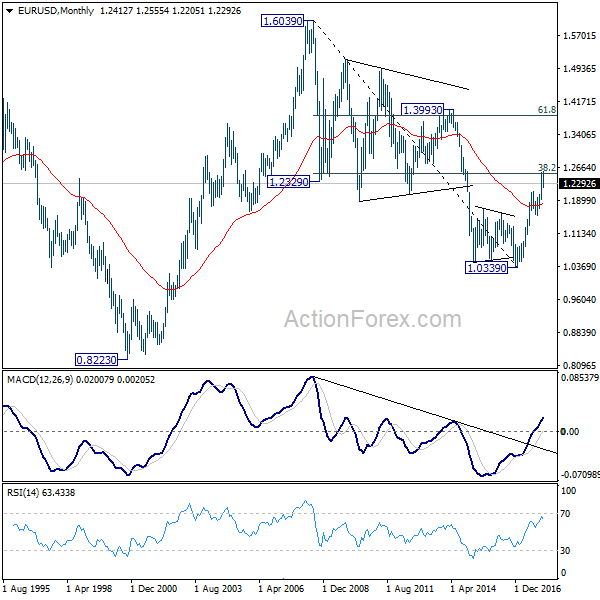

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

In the long term picture, 1.0339 is seen as an important bottom as the down trend from 1.6039 (2008 high) could have completed. It's still early to decide whether price action from 1.0339 is developing into a corrective or impulsive pattern. Reaction to 38.2% retracement of 1.6039 to 1.0339 at 1.2516 will give important clue to the underlying momentum.

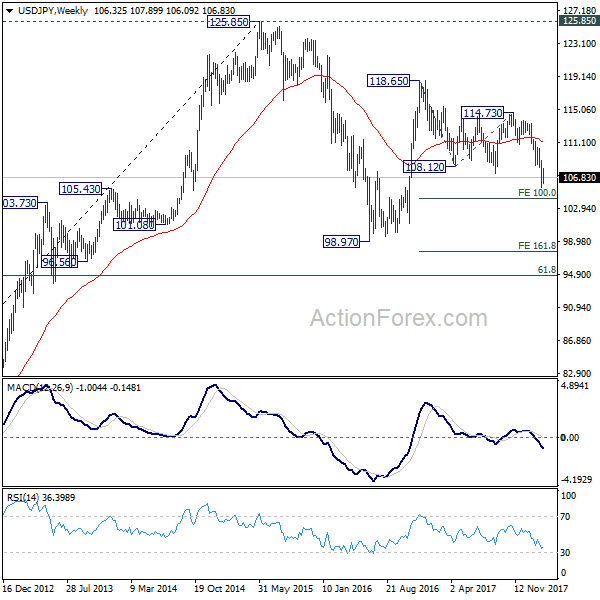

USD/JPY Weekly Outlook

USD/JPY stayed in consolidation above 105.54 last week and outlook is unchanged. Initial bias remains neutral this week first. With 108.27 resistance intact, deeper fall is expected. On the downside, break of 105.54 will extend the larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. However, break of 108.27 will be the first sign of near term reversal and will target 110.47 resistance for confirmation.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

In the long term picture, the rise from 75.56 (2011 low) long term bottom to 125.85 top is viewed as an impulsive move, no change in this view. Price actions from 125.85 are seen as a corrective move which could still extend. In case of deeper fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77. Up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.

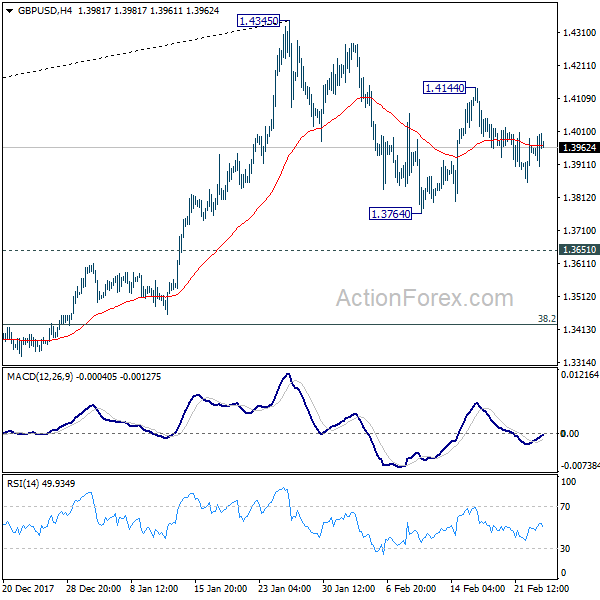

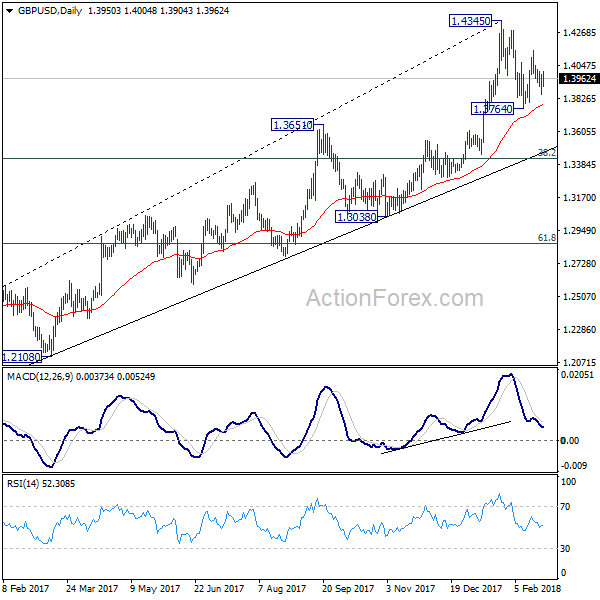

GBP/USD Weekly Outlook

GBP/USD stayed in range below 1.4144 last week and outlook is unchanged. Initial bias remains neutral this week first. On the upside, break of 1.4144 will extend the rebound from 1.3764 and target a test on 1.4345 resistance. Break there will resume larger up trend and target long term trend line resistance (now at 1.5056). On the downside, below 1.3764 will extend the correction from 1.4345 to 1.3651 resistance turned support instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

In the longer term picture, rise from 1.1946 should at least be correcting the whole long term down trend form 2.1161 and should target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. It too early to tell if it's developing into a long term up trend. We'll monitor the upside momentum and reaction to 1.5466 to decide later.

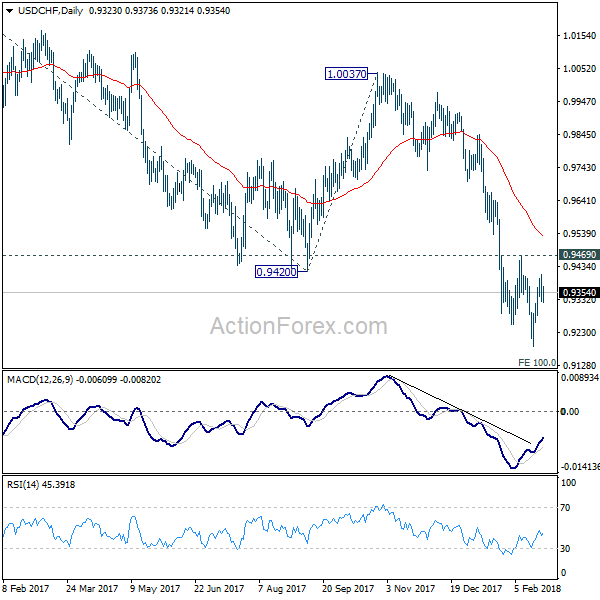

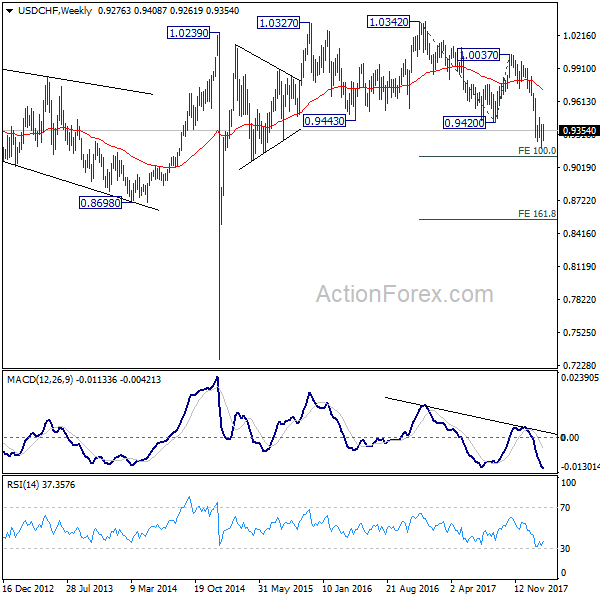

USD/CHF Weekly Outlook

USD/CHF stayed in consolidation above 0.9186 last week and outlook is unchanged. Initial bias remains neutral this week first. With 0.9469 resistance intact, deeper fall is still expected. On the downside, break of 0.9186 will extend the larger down trend to 0.9115 medium term projection level next. However, considering bullish convergence condition in 4 hour MACD, break of 0.9469 will indicate near term reversal and turn outlook bullish for 55 day EMA (now at 0.9533) and above.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

In the long term picture, the strong break of 0.9420 support and downside acceleration turns the long term outlook rather bearish. Corrective rebound from 0.7065 (2011 low) could have already completed at 1.0342. 0.8698 support will be a key level to watch. Sustained break there could bring retest of 0.7065.

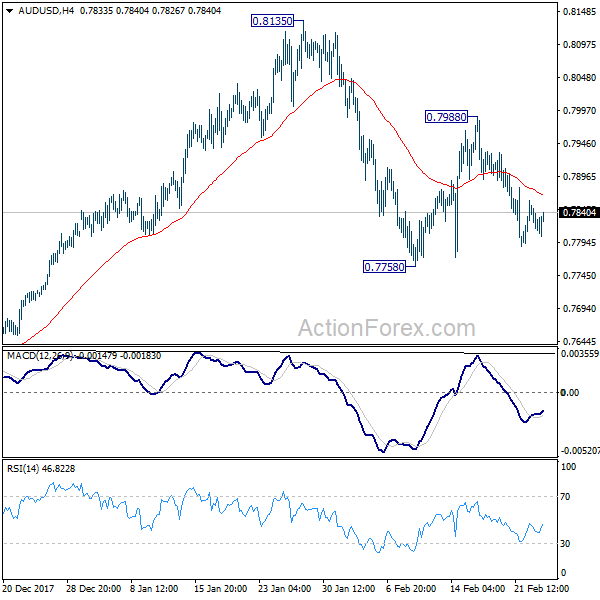

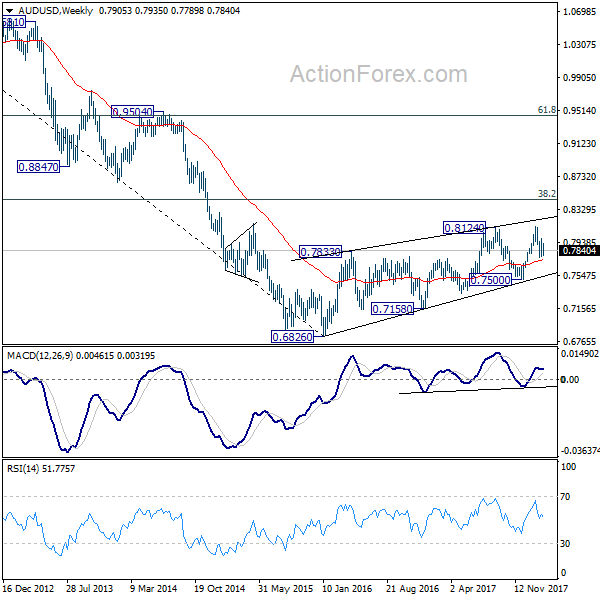

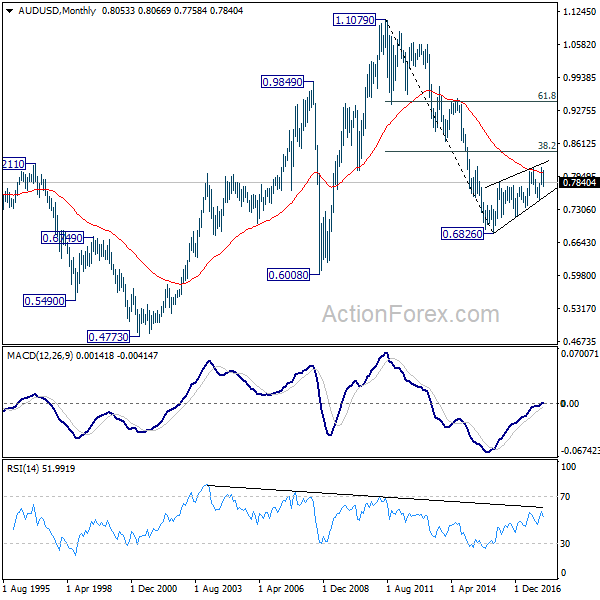

AUD/USD Weekly Outlook

AUD/USD stayed in range of 0.7758/7988 last week and outlook is unchanged. Initial bias remains neutral this week first. On the upside, above 0.7988 will extend the rebound to retest 0.8135. On the downside, below 0.7758 will resume the fall from 0.8135 and target 0.7500 key near term support. At this point, there is no strong case for a range breakout yet and 0.7500/8135 could hold for a while.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

In the longer term picture, 0.6826 is seen as a long term bottom. Rise from there could either reverse the down trend from 1.1079, or just develop into a corrective pattern. At this point, we're favoring the latter. And, as long as 38.2% retracement of 1.1079 to 0.6826 at 0.8451 holds, we'd anticipate another decline through 0.6826 at a later stage. But strong support should be seen between 0.4773 (2001 low) and 0.6008 (2008 low).

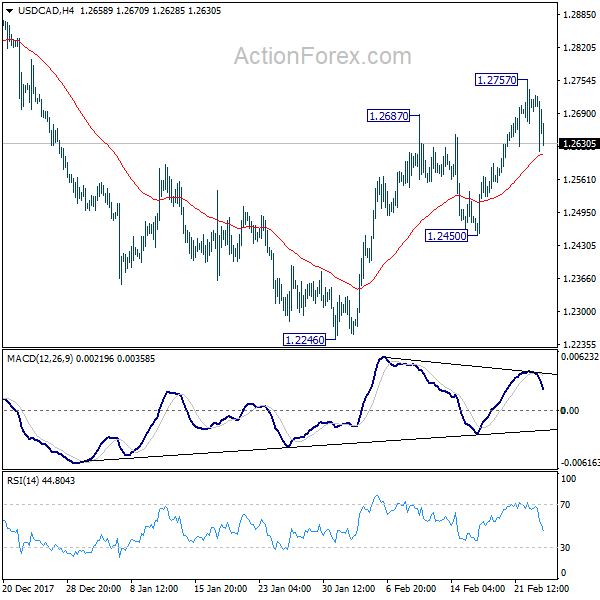

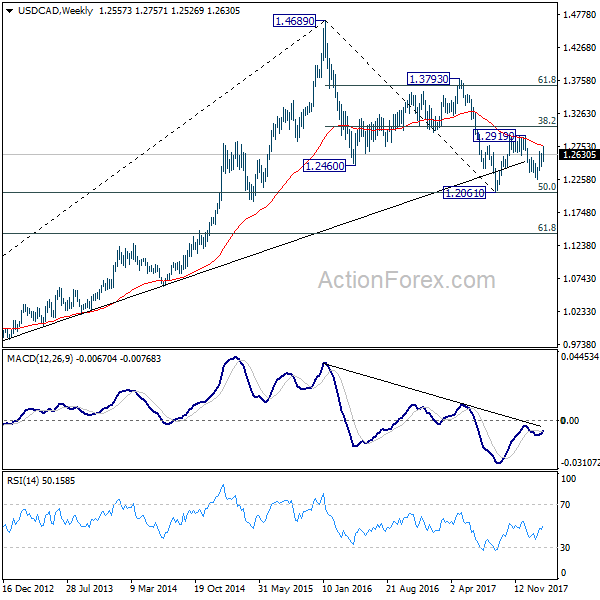

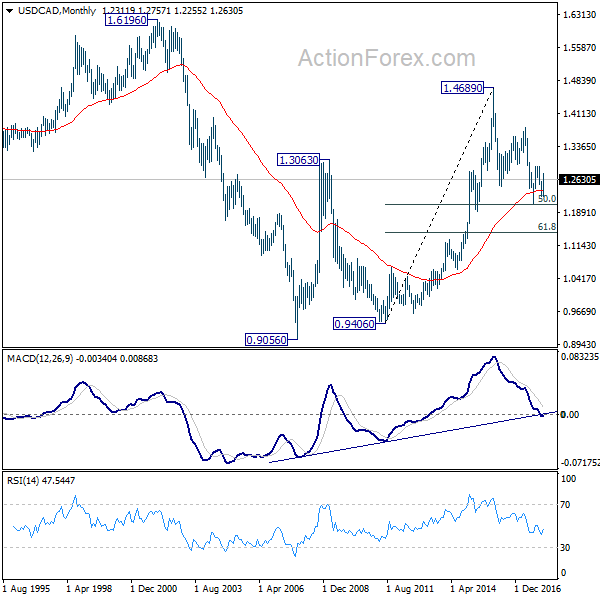

USD/CAD Weekly Outlook

USD/CAD rebounded to as high as 1.2757 last week but lost momentum since then. Initial bias remains neutral this week first. Above 1.2757 will target a test on 1.2919 key resistance. We'd be cautious on strong resistance from there to limit upside. On the downside, below 1.2450 will turn bias back to the downside for 1.2246 support.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA (now at 1.2771), hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

In the longer term picture, 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048 remains a key support level to watch. As long as this level holds, we'll treat fall from 1.4689 as a correction and expect another rally through this level. However, sustained break of 1.2048 will turn favors to the case that rise from 0.9056 (2007 low) is a three wave corrective move that's completed at 1.4689. And retest of 0.9056/9406 support zone could be seen in medium to long term.

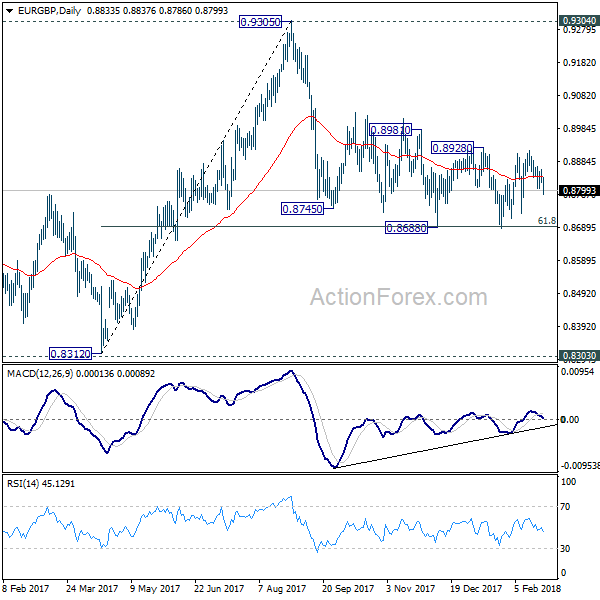

EUR/GBP Weekly Outlook

EUR/GBP's sideway trading continued last week, inside range of 0.8686/8928. Initial bias remains neutral this week first. Also, outlook stays mildly bearish with 0.8928 resistance intact. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too, deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

In the long term picture, we're holding on to the view that rise from 0.6935 (2015 low) is resuming the up trend from 0.5680 (2000 low). Hence, after the consolidation from 0.9304 completes, we'd expect another medium term up trend through 0.9799 to 100% projection of 0.5680 to 0.9799 from 0.6935 at 1.1054.

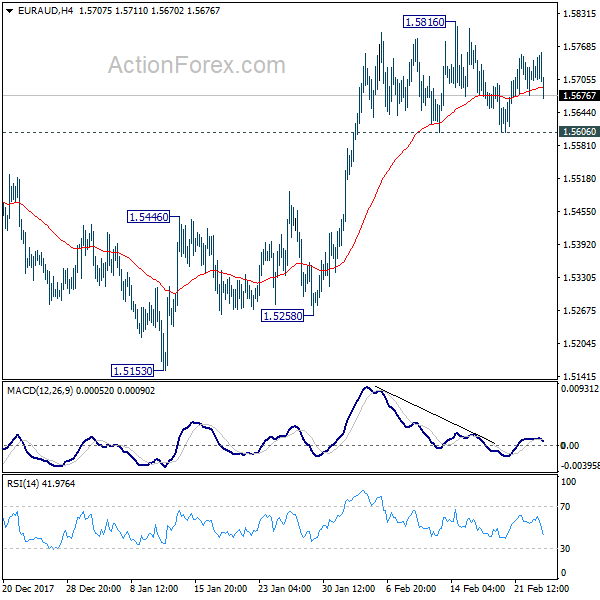

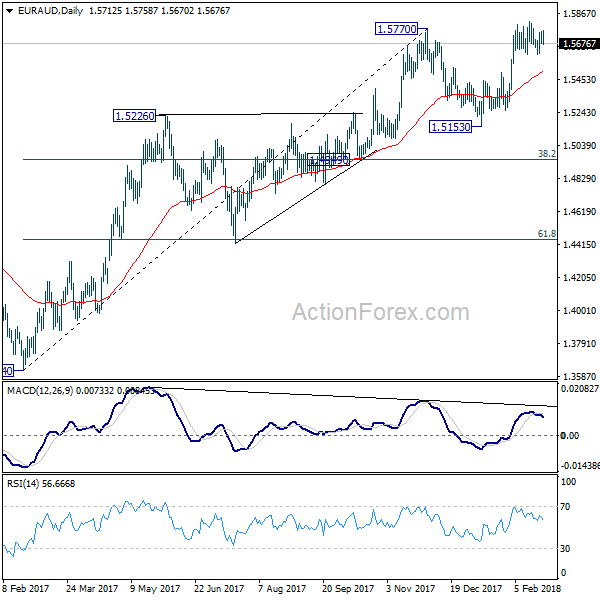

EUR/AUD Weekly Outlook

EUR/AUD stayed in consolidation below 1.5816 last week and outlook is unchanged. Initial bias remains neutral this week first. Also, near term outlook stays cautiously bullish as long as 1.5606 support holds. Break of 1.5816 should now confirm resumption of medium term rise from 1.3264. In that case, EUR/AUD should target 1.6587 key long term resistance. Meanwhile, firm break of 1.5606 will argue that a short term top is formed. Intraday bias will be turned back to the downside for 55 day EMA (now at 1.5501) and below.

In the bigger picture, medium term rise from 1.3624 is not completed yet. Sustained break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

In the longer term picture, the rise from 1.1602 long term bottom (2012 low) isn't over yet. We'll keep monitoring the development but there is prospect of extending the rise to 61.8% retracement of 2.1127 to 1.1602 at 1.7488 and above. However, sustained trading below 1.3671 should indicate long term reversal and target 1.1602 long term bottom again.