Sample Category Title

Market Update – Asian Session: Upcoming FOMC Minutes In Focus

Headlines/Economic Data

General Trend:

Asian currencies continue to exhibit strength in the new year. Thai Baht (THB) hits strongest level since April 2015; PBoC set yuan (CNY) at strongest since May 2016; Taiwan Dollar (TWD) continues to trade at over 4-year highs

Japan

Nikkei 225 closed for holiday

Looking ahead: Equity markets in Japan resume trading on Thursday, following 3-day holiday; Japan Dec final manufacturing PMI to be released

Korea

Kospi opened +0.2%

Semiconductors track earlier gains in the US: Samsung Electronics +1.5%, Hynix +1.4%

Posco Steel +5%, Hyundai Steel +2.6% (US Dow Jones Iron & Steel index rose 4.6% on Tuesday; positive broker commentary)

073240.KR (Kumho Tire) +11%: KDB set up task forces to deal with Kumho Tire restructuring and M&A

LG Display (034220.KR) +3%: To begin supplying OLED panels for over 15M new iPhone units which are expected to be unveiled in H2, says a press report.

009540.KR Hyundai Heavy +9.5% (Issued FY18 sales guidance)**Reminder: On Dec 27, 2017 the company’s share price declined by over 28%, as it announced a plan to raise KRW1.29T in capital.

(KR) Bank of Korea (BOK) Gov Lee: Reiterates stance of closely monitoring FX movements

(KR) Korean press comments on rising number of mortgages in South Korea despite govt's measures to slow the housing market

(KR) Bank of Korea (BoK) sells KRW2.4T in 2-year monetary stabilization bonds: yield 2.06%

(KR) Moody's: domestic and global credit impact of Korea conflict would depend on duration and severity

(KR) North Korea Official: Kim Jong Un has given order to open boarder hotline between the Koreas at 06:30GMT to discuss inter-Korean dialogue

(KR) South Korea Q4 Foreign Direct Investment (FDI) y/y: +49.8% v -9.0% prior; 2017 FDI record high

China/Hong Kong

Hang Seng opened +0.5%, Shanghai Composite flat

Hang Seng Services Index +1.7% (strength in airlines), Consumer Goods +1.5% (automakers gain), Materials +1.3%, Information Technology +1.2%; Telecom -1% (China Mobile -1.4%), Utilities -0.1%

(CN) China researcher suggests China should allow yuan to fall this year; sees 2018 GDP at 6.5% -21st Herald

(CN) PBOC may resume open market operations (OMO) in H2 of Jan - Chinese press

(CN) China Securities Times Op Ed: PBOC should stabilize yuan fx rate

(CN) Survey of analysts expects China to raise money market rates 3 times - financial press

(CN) China PBoC: Skips OMO for 8th straight session; Net drains CNY90B v CNY290B prior

USD/CNY (CN) China PBoC sets yuan reference rate at 6.4920 v 6.5079 prior (strongest setting since May 2016)

(HK) Overnight HK$ HIBOR -66bps (most since Nov 1st); 1-week HK$ HIBOR -47bps (most since Oct 2008); 1-month HK$ HIBOR -7bps (most since Jan 2009)

Looking ahead: China Dec Caixin Services PMI to be released on Thursday

Australia/New Zealand

ASX 200 opened +0.2%; closed: +0.2%

ASX 200 Resources Index +1.4%, Energy +0.6%;Financials -0.2, Consumer Discretionary -0.5%

MWY.AU Guides FY18 H1 earnings to be lower due to delayed export shipments; -3%

YOW.AU Cuts FY18 Rev to +17% y/y (prior 55%); Names Mark Schuessler new CEO; -33%

Other Asia

(PH) Philippines Central Bank (BSP): May tweak monetary stance if there is a 2nd CPI effect; To restore 28-day term deposits in due time

North America

US equities ended higher: Dow +0.4%, S&P500 +0.8%, Nasdaq +1.5%, Russell 2000 +0.9%

S&P500 Energy Sector +1.6%, Consumer Discretionary +1.5%

SEMI: Sees 2018 global fab equipment spending $63B, +11% y/y; 2017 global fab equipment spending $57B, +41% y/y (record high)

(US) Sen Hatch (R-UT): plans to retire from the Senate at the end of term; Hatch was first elected to the Senate from Utah in 1976

Looking ahead: US Dec ISM manufacturing PMI to be released on Wednesday, along with Dec FOMC Minutes and Weekly API Crude Oil Inventories.

Europe

(UK) UK reportedly considering joining the Trans Pacific Partnership (TPP) following Brexit - FT

(EU) ECB's Nowotny (Austria): sees a risk of a European stock market bubble - press interview

Levels as of 01:00ET

Nikkei225 closed, Hang Seng +0.0%; Shanghai Composite +0.5%; ASX200 +0.2%, Kospi +0.3%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax +0.2%; FTSE100 +0.0%

EUR 1.2066-1.2042; JPY 112.39-112.17; AUD 0.7837-0.7806;NZD 0.7109-0.7073

Feb Gold +0.0% at $1,316/oz; Feb Crude Oil +0.0% at $60.38/brl; Mar Copper -0.5% at $3.26/lb

Aussie Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.24% against the USD and closed at 0.7828.

LME Copper prices rose 0.3% or $24.0/MT to $7181.0/MT. Aluminium prices rose 0.7% or $14.5/MT to $2256.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7811, with the AUD trading 0.22% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7796, and a fall through could take it to the next support level of 0.7780. The pair is expected to find its first resistance at 0.7836, and a rise through could take it to the next resistance level of 0.7860.

Looking forward, Australia’s AiG performance of services index for December, set to release overnight, would garner significant amount of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Manufacturing Sector Activity Confirmed At A Record High Across The Euro-Zone In December

For the 24 hours to 23:00 GMT, the EUR rose 0.42% against the USD and closed at 1.2058, following upbeat economic data across the Euro-zone which suggested that the upturn in the manufacturing sector would continue to surge in the new year.

The Euro-zone’s final Markit manufacturing PMI advanced to a record high level of 60.6 in December, confirming the preliminary print. The PMI had registered a level of 60.1 in the previous month.

Separately, activity in Germany’s manufacturing sector jumped as initially estimated to a level of 63.3 in December, expanding at its fastest pace on record and compared to a level of 62.5 in the prior month.

The US Dollar nursed losses against its major peers, as investors turned sceptical about the Federal Reserve’s monetary policy outlook.

On the economic front, the US final Markit manufacturing PMI was revised higher to a level of 55.1 in December, surging at its quickest pace in nearly three years and signalling a solid improvement in the health of the nation’s manufacturing sector. The preliminary figures had indicated an advance to a level of 55.0, compared to a reading of 53.9 in the prior month.

In the Asian session, at GMT0400, the pair is trading at 1.2047, with the EUR trading 0.09% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.2012, and a fall through could take it to the next support level of 1.1976. The pair is expected to find its first resistance at 1.2082, and a rise through could take it to the next resistance level of 1.2116.

Moving ahead, market participants would eye the release of Germany’s unemployment rate data for December, scheduled to release in a few hours. Later in the day, investors will turn their attention to the minutes of the Fed’s December policy meeting as well as the US ISM manufacturing PMI for December and construction spending data for November.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving averages.

UK’s Manufacturing Sector Growth Came In Weaker-Than-Expected In December

For the 24 hours to 23:00 GMT, the GBP rose 0.58% against the USD and closed at 1.3592.

Macroeconomic data revealed that Britain's Markit manufacturing PMI dropped more-than-expected to a level of 56.3 in December, after recording a four-year high level of 58.2 in the prior month, while markets were expecting for a fall to a level of 57.9.

In the Asian session, at GMT0400, the pair is trading at 1.3596, with the GBP trading marginally higher against the USD from yesterday's close.

The pair is expected to find support at 1.3538, and a fall through could take it to the next support level of 1.3479. The pair is expected to find its first resistance at 1.363, and a rise through could take it to the next resistance level of 1.3663.

Moving ahead, traders would closely monitor UK's Markit construction PMI for December, scheduled to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.37% against the JPY and closed at 112.25.

In the Asian session, at GMT0400, the pair is trading at 112.34, with the USD trading 0.08% higher against the JPY from yesterday’s close.

The pair is expected to find support at 112.02, and a fall through could take it to the next support level of 111.70. The pair is expected to find its first resistance at 112.70, and a rise through could take it to the next resistance level of 113.06.

Going ahead, traders would focus on Japan’s final Nikkei manufacturing PMI for December, set to release overnight.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Marginally Lower This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.21% against the CHF and closed at 0.9721.

In the Asian session, at GMT0400, the pair is trading at 0.9723, with the USD trading a tad higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9702, and a fall through could take it to the next support level of 0.9681. The pair is expected to find its first resistance at 0.9742, and a rise through could take it to the next resistance level of 0.9761.

Ahead in the day, traders would keep a close watch on Switzerland’s real retail sales for November and SVME–PMI for December.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Canada’s Manufacturing Sector Growth At A 3-Month High In December

For the 24 hours to 23:00 GMT, the USD declined 0.36% against the CAD and closed at 1.2513.

The Canadian Dollar gained ground against the USD, after Canada's Markit manufacturing PMI climbed to a level of 54.7 in December, notching to a three-month high level, thus suggesting that manufacturers ended the fourth quarter on a strong footing. The PMI had registered a level of 54.4 in the prior month.

In the Asian session, at GMT0400, the pair is trading at 1.2521, with the USD trading 0.06% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2497, and a fall through could take it to the next support level of 1.2474. The pair is expected to find its first resistance at 1.2547, and a rise through could take it to the next resistance level of 1.2574.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 152.08; (P) 152.40; (R1) 152.94; More...

Intraday bias in GBP/JPY remains on the upside as rebound from 149.40 continues to 153.39 resistance. Break will resume medium term rally. On the downside, below 151.51 minor support will extend the corrective pattern with another fall through 149.40 before completion.

In the bigger picture, outlook is mixed up a bit with last week's sharp decline. But still, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. And the corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

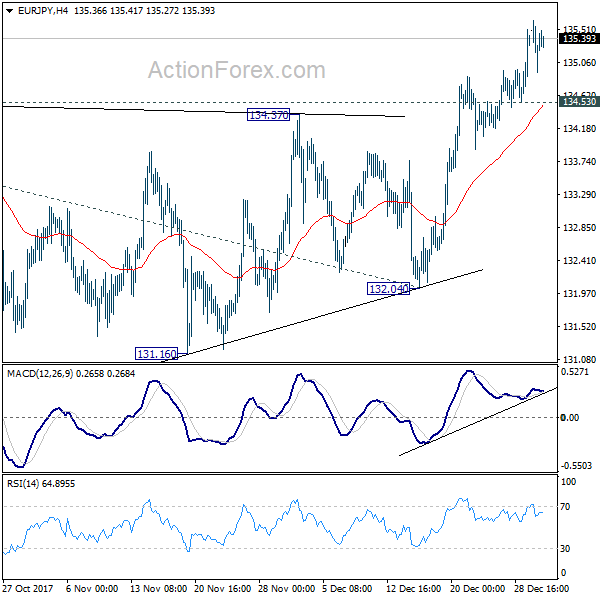

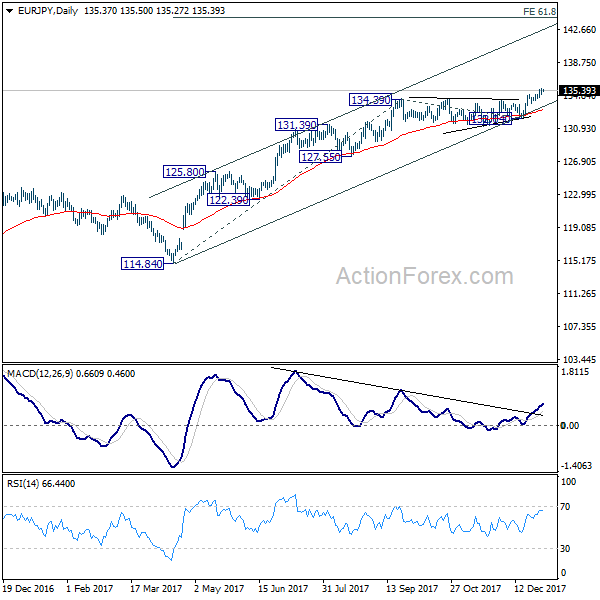

EUR/JPY Daily Outlook

Daily Pivots: (S1) 135.01; (P) 135.32; (R1) 135.70; More....

With 134.53 minor support intact, intraday bias in EUR/JPY remains on the upside. Current medium term rally would target 61.8% projection of 114.84 to 134.39 from 132.04 at 144.12. On the downside, below 134.53 minor support will turn intraday bias neutral again.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). Sustained break of 61.8% retracement of 149.76 to 109.03 at 134.20 will pave the way to key long term resistance zone at 141.04/149.76. However, break of 132.04 support will suggest medium term topping and will turn outlook bearish for deeper fall back 55 week EMA (now at 128.34).

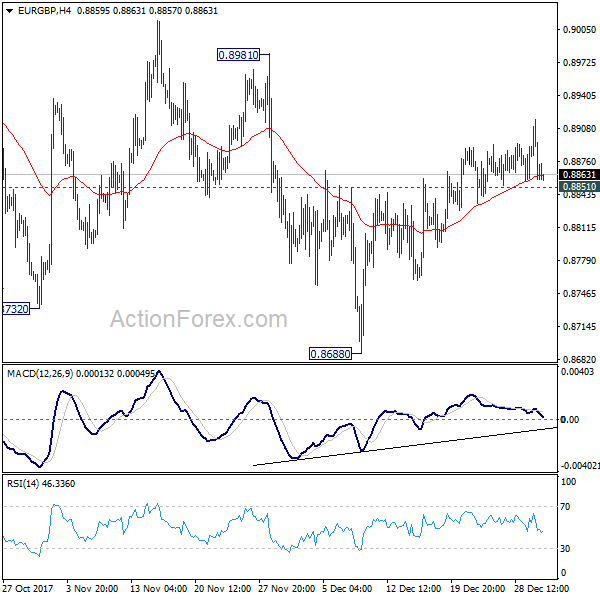

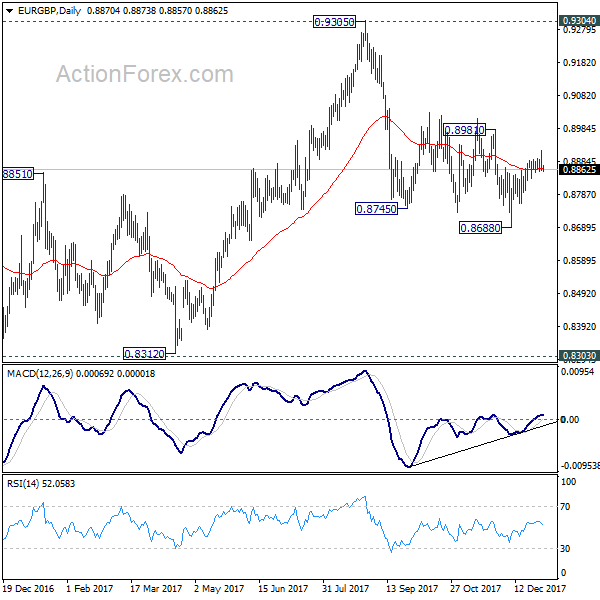

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8846; (P) 0.8882; (R1) 0.8905; More...

At this point,f further rise is mildly in favor in EUR/GBP to 0.8981 resistance. Sustained break there will indicate that whole decline from 0.9305 has completed. In such case, EUR/GBP will target a test on 0.9304/5 key resistance. On the downside, below 0.8851 minor support will turn bias back to the downside for 0.8668 instead.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.