Sample Category Title

Gold Higher Ahead of Fed Rate Statement

Gold has posted gains in the Wednesday session. In North American trade, the spot price for an ounce of gold is $1277.20, up 0.47% on the day. On the release front, ADP Nonfarm Payrolls surged to 235 thousand, crushing the estimate of 202 thousand. On the manufacturing front, ISM Manufacturing PMI slowed to 58.7, missing the forecast of 59.5 points. Today's highlight is the FOMC rate statement, with no change expected in the benchmark interest rate. On Thursday, and the US will publish unemployment claims.

Will the Federal Reserve rate statement move gold prices? The Fed is widely expected to maintain the benchmark rate at 1.25%, but the statement could provide clues about future rate policy. The markets have priced in a December rate at 98.5%, which would mark a third rate for 2017. What can we expect in 2018? That depends to a large degree on the new chair of the Fed. Janet Yellen will wind up her 3-year term in February, and she is not expected to be reappointed by President Trump. The front runner is economist Jerome Powell, who is a proponent of much higher rates – his "Taylor Rule", which calls for higher rates when inflation is high or the labor market is at full capacity. Trump is expected to make his choice on Thursday, ahead of his trip to Asia.

The US consumer remains optimistic about the economy, and that confidence has translated into stronger spending. CB Consumer Confidence jumped to 125.9 points, and last week's UoM Consumer Sentiment climbed to an all-time high of 100.7 points. Personal spending gained 1.0% in September, its sharpest gain since April 2016. The strong reading comes on the heels of Friday's UoM Consumer Sentiment Report, which hit an all-time record in September. Consumer spending is a key driver of the economy, accounting for two-thirds of economic growth.

The Bank of England is expected to raise rates for the first time in a decade on Thursday. Bank policymakers are in a quandary with regard to rate policy. Inflation is running well above the Bank's target of 2 percent, which has eroded consumer spending. As well, a labor market that is close to capacity is a reason in favor of raising rates. However, economic growth has slowed and there are fears that Brexit will take a toll on the British economy. The deadlock in the Brexit negotiations has done nothing to calm these concerns, as investors and the business community are becoming increasingly frustrated with the government's lack of a coherent policy regarding Brexit. At the end of the day, a quarter-point rate hike should not have a huge effect on the economy, but the psychological significance of the move could boost the pound against other assets, including gold.

Pound Subdued Ahead of Expected BoE Rate Hike

The British pound has posted slight losses in the Wednesday session. In North American trade, GBP/USD is trading at 1.3266, down 0.20% on the day. On the release front, British Manufacturing PMI improved to 56.3, above the estimate of 55.8 points. In the US, ADP Nonfarm Payrolls surged to 235 thousand, crushing the estimate of 202 thousand. On the manufacturing front, ISM Manufacturing PMI slowed to 58.7, missing the forecast of 59.5 points. Today's highlight is the FOMC rate statement, with no change expected in the benchmark interest rate. On Thursday, the Bank of England is expected to raise interest rates to 0.50%. The UK releases Construction PMI and the US will publish unemployment claims.

Central banks are in focus this week, beginning with the Federal Reserve later on Wednesday. The Fed is widely expected to maintain the benchmark rate at 1.25%, but the rate statement could provide clues about future rate policy. The markets have priced in a December rate at 98.5%, which would mark a third rate for 2017. With a December rate hike a given, barring a meltdown in the US, what can we expect in 2018? That depends to a large degree on the new chair of the Fed. Janet Yellen will wind up her 3-year term in February, and she is not expected to be reappointed by President Trump. The front runner is Jerome Powell, who would likely follow Yellen's current policy of gradual, incremental rates. Another candidate is economist James Taylor, who is a proponent of much higher rates – his "Taylor Rule", which calls for higher rates when inflation is high or the labor market is at full capacity. Trump is expected to make his choice on Thursday, ahead of his trip to Asia.

The BoE will take center stage on Thursday, but unlike the Fed, the BoE is expected to raise rates at its policy meeting. A rate hike of 25 basis points would raise rates to 0.50%, and would mark the Bank's first rate increase since 2007. Investors have stayed on the sidelines on Wednesday, and shrugged off a strong Manufacturing PMI, which could have been a catalyst for purchasing pounds. Bank policymakers are in a quandary with regard to rate policy. Inflation is running well above the Bank's target of 2 percent, which has eroded consumer spending. As well, a labor market that is close to capacity is a reason in favor of raising rates. However, economic growth has slowed and there are fears that Brexit will take a toll on the British economy. The deadlock in the Brexit negotiations has done nothing to calm these concerns, as investors and the business community are becoming increasingly frustrated with the government's lack of a coherent policy regarding Brexit. At the end of the day, a quarter-point rate hike should not have a huge effect on the economy, but the psychological significance of the move could boost the pound against the US dollar.

The Federal Reserve is also in focus this week, with the release a rate statement on Wednesday. The Fed is not expected to raise rates, so analysts will be combing through the rate statement, looking for clues about future rate moves. The markets have priced in a December rate hike at whopping 96 percent, and the markets are focusing on what the Fed has planned for 2018. This will depend, of course, on the new head of the Fed, who will take over from Janet Yellen in February. The two front-runners, John Taylor and Jerome Powell, have very different stances on monetary policy, which has created some suspense ahead of President Trump's nomination. Trump is expected to choose the new head before departing for Asia at the end of the week. Powell is expected to continue Yellen's incremental approach to raising rates, while Taylor is a proponent of much higher rates, as underscored in his "Taylor Rule", which calls for higher rates when inflation is high or the labor market is at full capacity.

Dollar and Pound Bolstered by Upbeat Data ahead of Rate Decisions

The prevailing risk-on mood ahead of key risk events in the next few days lifted the US dollar and weakened the yen in European trading on Wednesday. Upbeat economic data also boosted the greenback along with the British pound. The aussie and kiwi were other notable gainers, while the euro joined the yen in being the day's worst performers.

Manufacturing PMI out of the UK was the main data release in Europe. The index rose from an upwardly revised 56.0 in September to 56.3 in October, beating expectations of a fall to 55.8. The solid data reinforced expectations that the Bank of England will raise rates on Thursday, especially as, apart from stronger manufacturing growth, the IHS Markit report showed input and output prices also accelerated in October.

The pound extended its gains, climbing to a near three-week high of $1.3319 before settling around $1.3290 in late European trading. It was also up sharply against the euro, rising to a 4½-month high of 0.8730 pounds per euro. Reports that the European Union is ready to intensify the Brexit talks with the UK had lifted the pound earlier in the day, but the British currency remains vulnerable to downside moves if the Bank of England decides against raising rates when it concludes its two-day monetary policy meeting tomorrow or delivers a dovish hike.

Prior to the BoE's decision tomorrow the Fed will announce the outcome of its policy meeting at 18:00 GMT. The Fed is expected to keep rates unchanged despite growing signs that the US economy is gaining momentum, as it waits for inflation to recover from a soft patch. However, the FOMC statement will likely signal a December rate hike, although the event has been overshadowed by the highly anticipated choice of the next Fed chair. President Trump is due to reveal tomorrow his nominee to replace Janet Yellen when her term expires in December.

Another major dollar event tomorrow is the unveiling of the tax bill by House Republicans, while the ongoing investigation into Russian collusion with the Trump election campaign team poses a threat to the current risk-on sentiment following the first charges being filed this week against three of Trump's former aides.

In the meantime though, the dollar advanced higher on the back of more positive indicators out of the US. The ADP report on private-sector employment showed 235k jobs were added last month as US employers hired more workers after the disruption from the hurricanes in September. This compares with a downwardly revised figure of 110k in the prior month and forecasts of 200k. The strong number comes ahead of Friday's official nonfarm payrolls report.

The greenback hit a session high of 114.27 against the yen after the data but fell back towards the 114 level after the ISM manufacturing PMI missed expectations. The ISM's manufacturing gauge had hit a 13-year high of 60.8 in September but slipped to 58.7 in October, coming in below forecasts of 59.5. In contrast, the Markit manufacturing PMI improved during the month, rising from 53.1 to 54.6 in October's final reading.

In other currencies, the euro struggled for direction, falling against most of its major peers. The single currency was last trading at 1.1633 versus the dollar and at 132.65 versus the yen.

The Australian and New Zealand dollars held their ground against the resurgent greenback, with the aussie extending its gains to $0.7691, but the kiwi eased slightly from its earlier highs to around $0.6900. The Canadian dollar was flat, finding some support from surging oil prices after yesterday's surprise drop in Canadian GDP during August further dented expectations of additional rate hikes by the Bank of Canada in the near term. Dollar/loonie last stood at C$1.2877, not far from last week's 3½-month high of C$1.2916.

Crude oil prices enjoyed another day of gains, reaching fresh highs, boosted by strong compliance by OPEC members in October to the output deal. WTI crude hit a 10-month high of $55.22 a barrel, while Brent crude scaled a more than two-year high of $61.70 per barrel. There was little reaction to the latest US inventories data.

The EIA's weekly report showed a bigger-than-expected drawdown of 2.435 million barrels of crude stocks. Gasoline stocks also fell by more than forecast but distillate stocks dropped by less than expected.

Gold prices rebounded sharply today to briefly top the $1280 level amid some investor caution ahead of tomorrow's announcement on the new Fed chair. The precious metal was last trading 0.5% up on the day at $1277 an ounce. Other metals also performed well, with copper jumping 1.1% to $3.1265 a ton on hopes of higher Chinese demand, and nickel prices soared to a two-year high to break above $13,000 a ton, driven by rising demand for lithium batteries used in electric cars (of which nickel is a key component).

ISM Manufacturing Remains Near Cycle Highs

Manufacturing activity moderated slightly in October with the ISM index shedding 2.1 points off its September high. The underlying details are encouraging and signal continued strength in the factory sector.

Despite Modest Retreat in Headline, Production Remains Strong

The ISM manufacturing index retreated ever so slightly in October, losing 2.1 points to post a still solid figure of 58.7. The composite index is coming off a cycle high of 60.8 and continues to signal firmness in the manufacturing sector. As effects from the recent hurricanes fade from the data, we can get a more accurate read of how the manufacturing sector is performing.

While the majority of the index's subcomponents experienced a negative monthly change, the details are still encouraging. The production subcomponent lost 1.2 points but remains above 60.0, and has done so for 5 consecutive months. Likewise, the new orders component lost 1.2 points but posted a 63.4 reading, suggesting that future orders will remain strong in the coming months (top graph). This marks the 14th consecutive month of new orders growth.

Despite the 0.5 point decline in the employment subcomponent, hiring in the manufacturing sector continues to exhibit strength (middle graph). Of the 18 manufacturing industries, 15 reported employment growth in October. Friday's employment report will provide us with more detailed figures of the actual number of hires. We look for the factory sector to add to payroll growth in Friday's employment report.

Law of Supply Chain Disruptions

A line item that has perhaps not yet escaped the hurricanes' power is the supplier delivery component. Last month, supplier deliveries jumped 7.3 points to 64.4, reflecting storm disruptions from the Gulf area that caused delivery times to lengthen (bottom graph). The 3.0 point decline in October represents a partial normalization of the delivery supply chains. However, the 61.4 reading still remains elevated above its 6-month average of 55.1. We expect this component to continue to moderate in the coming months as businesses are able to return to their normal delivery schedules.

The inventory index came in at 48.0, a 4.5 point decline from September and is firmly below its 6-month average. The contraction partially reflects the supply chain disruptions, which has made it difficult for companies to deliver materials on their scheduled times. Customer inventories registered 43.5 in October, representing a 1.5 percentage point increase from September, indicating that customers' inventory levels are still considered too low.

Another area where hurricane effects were still lingering was in prices. Although the prices paid index fell to 68.5 in October, the index is still at elevated levels. Prices for raw materials have now increased for 20 consecutive months.

Construction Spending Rises Modestly in September

Construction spending rose 0.3 percent in September but outlays for August were revised lower and now show a gain of just 0.1 percent, compared to the initially reported 0.5 percent rise.

Longer-Run Trends Show Only a Slight Hint of Improvement

Overall construction spending rose slightly more than expected in September but the larger gain was largely due to a downward revision to the prior month's data. The monthly data are extremely volatile and the initially reported figures are often revised substantially. Moreover, deviations due to sampling error are typically much larger than the reported monthly change in the series.

The September data were likely impacted by the hurricanes, which disrupted building activity in Texas, Florida and some other parts of the South during August and September. Hurricane damages may have boosted public construction spending. Total public construction outlays rose 2.6 percent in September, with spending for power projects jumping 11.0 percent and outlays for conservation and development surging 12.6 percent. That latter category includes outlays for dams, levees and jetties. Spending for highway and street projects rose 1.1 percent during the month and spending for transportation projects rose 5.0 percent. Public spending for all of these categories remains down year-to-year, however, which is a testament to the sustained drag that government spending cuts have placed on overall construction spending and the economy.

Within public construction spending, outlays for state and local government projects rose 2.5 percent, while outlays for federal projects increased 3.4 percent. That marks the first increase for federal government construction spending since May and is only the second increase in the past six months. We like to utilize a 12-month change of a 12-month moving average for both series, which smooths out much of the monthly volatility. On this basis, state and local government spending is the weak spot, with outlays down 3.5 percent year-to-year. Federal government outlays are essentially flat on this basis.

Overall construction spending in the private sector fell 0.4 percent in September, with spending on nonresidential projects falling 0.8 percent and spending for residential construction unchanged. Oddly enough, spending for both single-family and multi-family construction rose modestly in September, climbing 0.2 percent and 0.6 percent, respectively. Spending on home improvements tumbled 0.6 percent, however. We expect to see that drop reversed in coming months, as homes are repaired following the recent hurricanes.

Private nonresidential construction has seen persistent weakness with reduced spending for manufacturing projects accounting for much of the recent slide. Within manufacturing, most of the drop has been in construction of new petrochemical facilities, which had surged around the middle of the decade but have pulled back considerably in recent years.

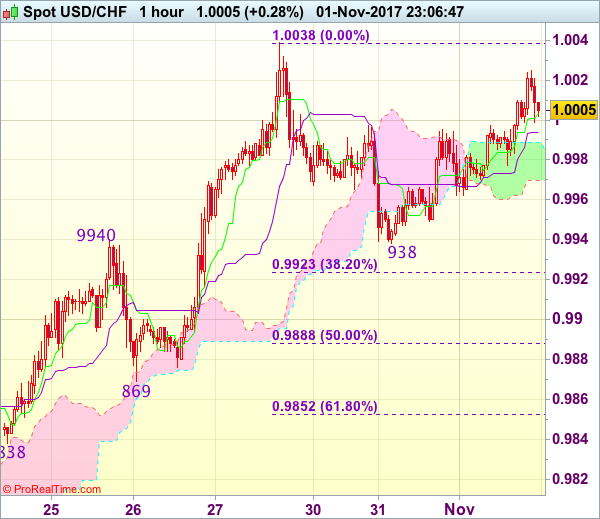

Trade Idea Wrap-up: USD/CHF – Buy at 0.9980

USD/CHF - 1.0009

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.0004

Kijun-Sen level : 0.9994

Ichimoku cloud top : 0.9987

Ichimoku cloud bottom : 0.9970

Original strategy :

Buy at 0.9980, Target: 1.0080, Stop: 0.9945

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9980, Target: 1.0080, Stop: 0.9945

Position : -

Target : -

Stop : -

As the greenback has continued moving higher after breaking indicated level at 1.0000, suggesting the pullback from 1.0038 has ended at 0.9938 and a retest of this level would be seen, break there would confirm recent upmove from 0.9421 low has resumed and may extend further gain to 1.0050-55, then towards 1.0075-80 but price should falter below 1.0100 resistance.

In view of this, we are looking to buy dollar again on pullback as 0.9975-80 should limit downside, bring another rise later. Below 0.9960 would prolong consolidation and risk weakness towards support at 0.9938, however, reckon downside would be limited to 0.9920-23 (38.2% Fibonacci retracement of 0.9737-1.0038) and 0.9885-90 (50% Fibonacci retracement) should remain intact.

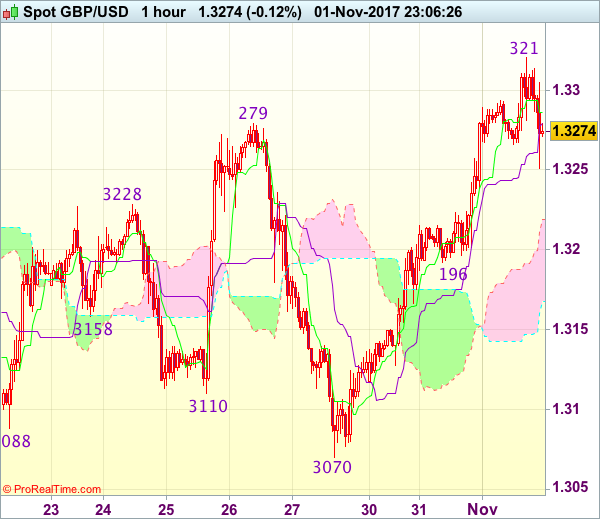

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.3268

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3286

Kijun-Sen level : 1.3280

Ichimoku cloud top : 1.3219

Ichimoku cloud bottom : 1.3167

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As cable surged and broke above indicated previous resistance at 1.3279-87 earlier today, suggesting early erratic rise from 1.3027 low is still in progress and near term upside risk remains for this move to bring retracement of early decline towards resistance at 1.3338, however, as broad outlook remains consolidative, reckon upside would be limited and price should falter below 1.3380-90, bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside for now. below 1.3245-50 would bring pullback to 1.3215-20 but only break of minor support at 1.3196 would signal top is formed, bring further fall to 1.3170.

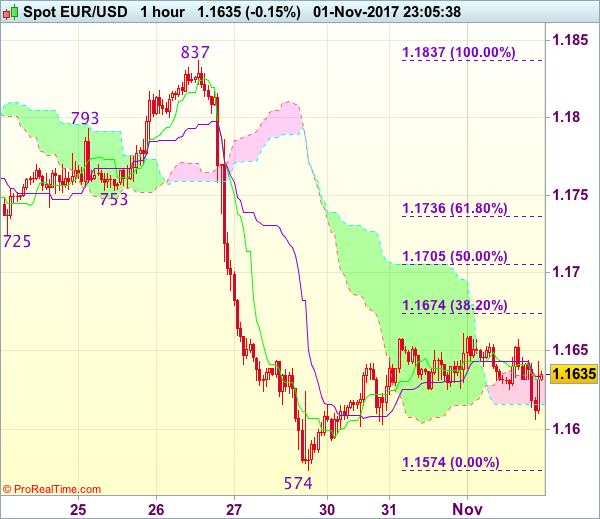

Trade Idea Wrap-up: EUR/USD – Sell at 1.1700

EUR/USD - 1.1629

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.1632

Kijun-Sen level : 1.1635

Ichimoku cloud top : 1.1634

Ichimoku cloud bottom : 1.1616

Original strategy :

Sell at 1.1700, Target: 1.1595, Stop: 1.1735

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1700, Target: 1.1595, Stop: 1.1735

Position : -

Target : -

Stop : -

Euro’s near term sideways trading is likely to continue and although initial upside risk remains for the rebound from 1.1574 low to extend gain to 1.1670-75 (38.2% Fibonacci retracement of 1.1837-1.1574), as this move is still viewed as retracement of recent decline, reckon upside would be limited to 1.1700-05 (50% Fibonacci retracement) and bring retreat later, below 1.1600-05 would signal the rebound from 1.1574 low has ended, bring retest of this level first. A drop below said support at 1.1574 would extend recent decline from 1.2093 top to 1.1550-55 but loss of downward momentum should prevent sharp fall below 1.1520-25 and reckon 1.1500 would hold.

In view of this, we are looking to sell euro on further subsequent recovery as 1.1700-05 should limit upside and bring another decline. Only above previous support at 1.1725 (now resistance) would signal low is formed instead, bring retracement of recent decline to 1.1750-55 first.

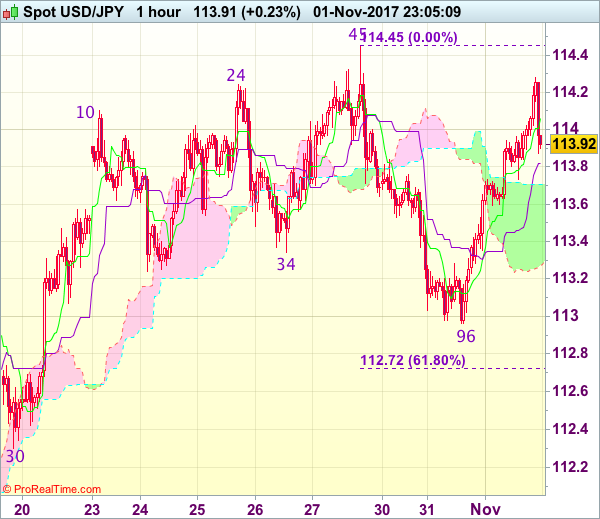

Trade Idea Wrap-up: USD/JPY – Buy at 113.40

USD/JPY - 113.94

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 114.06

Kijun-Sen level : 113.82

Ichimoku cloud top : 113.71

Ichimoku cloud bottom : 113.27

Original strategy :

Buy at 113.75, Target: 114.75, Stop: 113.40

Position : -

Target : -

Stop : -

New strategy :

Buy at 113.40, Target: 114.30, Stop: 113.05

Position : -

Target : -

Stop : -

As the greenback has continued moving higher after staging a strong rebound from 112.96 in part due to active cross-selling in yen, suggesting the retreat from 114.45 has ended at 112.96 and a retest of 114.45-50 strong resistance would be seen, however, break there is needed to retain bullishness and confirm early upmove has resumed for headway to 114.75-80 and later towards 115.00 but near term overbought condition should limit upside.

In view of this, we are looking to buy dollar on pullback as 113.35-40 should limit downside and bring another rise later. Below 113.20 would abort and suggest an intra-day top is formed, bring weakness towards said support at 112.96 which is likely to hold from here.

Average Earnings Likely to Dominate Attention Out of Friday’s Jobs Report; Fed and Tax Reforms Also Eyed

Friday's job report is undoubtedly the week's most significant data release out of the US. However, ahead of that, other events also have the capacity to steer the greenback in either direction.

Nonfarm payrolls are projected to have increased by 312k in October. This is in stark contrast to September's decline by 33k which marked the first time since 2010 that the economy experienced a reduction in positions. However, one should acknowledge that last month's fall does not point to a weak economy, but to the negative effects of the devastating storms that have hit the US during September.

Ahead of the previous month's report, expectations were for a rise in nonfarm payrolls by 90k. Despite the fall, the greenback recorded strong gains relative to majors as the numbers went public. Why so? Due to the storms, market participants assigned less weight on the number of positions and instead focused on the figures for average hourly earnings. Those surprised to the upside, growing by 2.9% year-on-year, within close distance of 3-4%, the range Fed chief Janet Yellen labelled as healthy growth in earnings.

The upcoming report will be biased upwards in terms of positions added to the economy relative to September's as a result of the recovery mode the economy has naturally entered following the extreme natural phenomena hitting US soil. It is thus likely to again be the case that investors' attention would fall on wage growth rather than on the number of jobs added to the economy.

Projections are for average earnings to increase by 0.2% m/m and 2.7% y/y, slowing down from September's 0.5% and 2.9% respectively. An upside surprise is expected to lead to a decline in euro/dollar, with the pair potentially finding support in the area around 1.1481, this being the 38.2% Fibonacci mark of the March 2 to September 8 upleg that saw the pair touching 1.2092, a near three-year high at the moment. Should wage growth fall short of expectations, then it is projected that euro/dollar would head higher with the range around 1.1717 - the 23.6% Fibonacci level of the aforementioned upleg - possibly acting as resistance.

Beyond Friday's much-anticipated release, investors are also paying attention to the Fed meeting that ends later today (no change in rates is expected), President Trump's pick to lead the Fed (he indicated that will proceed with an announcement on Thursday) and developments on the tax front (Republican lawmakers are expected to introduce a bill to cut taxes during the week).

The ADP employment numbers that reflect private-sector positions added to the economy and which are sometimes viewed as a precursor to the nonfarm payrolls report, beat expectations today with forex market participants going long the dollar versus other currencies as the figures went public. Also pertaining to October's jobs report, the unemployment rate is anticipated to remain at the 16-year low of 4.2%.