Sample Category Title

Fed in Focus, Bitcoin Unstoppable?

Sterling received another opportunity to shine on Wednesday, after stronger-than-expected data from Britain's manufacturing sector reinforced market expectations of the BoE raising UK interest rates on Thursday.

Growth in UK's manufacturing sector picked up in October, as the Purchasing Managers' Index edged to 56.30, from September's 56.00. This has been a positive week for the Pound so far, especially when considering the encouraging comments from Brexit negotiator, Michel Barnier. Barnier recently stated that the agenda and date for the next round of Brexit negotiations would be set "in next few hours or days" and as a result, some investor anxiety over the slow progress of Brexit talks was simply washed away. While Sterling could edge higher amid the optimism, the overall price action may be limited ahead of Thursday's heavily anticipated Bank of England meeting.

With markets widely expecting the Bank of England to raise UK interest rates at November's policy meeting, the focus will likely be directed towards the MPC votes and monetary policy summary. Brexit uncertainty continues to weigh on sentiment, while the troublesome combination of elevated inflation levels and subdued wage growth has eroded consumer spending power. With Britain's consumer-driven economic growth at risk, it will be interesting to hear Carney's thoughts on Thursday. There is a suspicion that that November's rate increase will fall into the category of a "dovish hike", as the central bank attempts to put a lid on inflation. With the UK's economic landscape still fragile and Brexit uncertainty still a recurrent theme, the expected rate hike is likely to be a once-off move that ends up punishing Sterling.

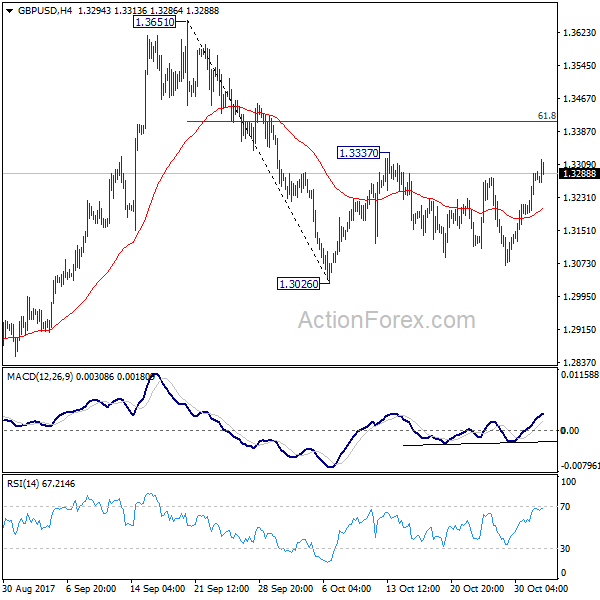

Taking a look at the technical picture, the GBPUSD currently trades around the 1.3300 as of writing. A breakout above this level could encourage an incline higher towards 1.3350. In an alternative scenario, sustained weakness below 1.3300 may open a path lower towards 1.3230.

Will November's FOMC meeting be a non-event?

King Dollar appreciated against a basket of currencies on Wednesday, ahead of the Federal Reserve decision later today, which is widely expected to conclude with monetary policy unchanged.

With it already being considered a forgone conclusion that US interest rates will be left unchanged in November, and with no press conference scheduled by Janet Yellen, today's FOMC meeting could be a snoozer. Although the lack of excitement precipitated by a press conference by Yellen and no new quarterly economic projections may put a cap on the spice, investors are likely to devote much of their attention to gleaning fresh insights on the Federal Reserve's tightening plan.

Looking beyond the FOMC statement this evening, Trump will be back in the spotlight on Thursday, as he appoints the next head of the Federal Reserve. With Trump expected to appoint Jerome Powell, who is seen as a dove, it will be interesting to see how the Dollar reacts.

From a technical standpoint, the Dollar Index is bullish on the daily charts. Daily bulls remain in control above the 94.00 dynamic support level, with the next level of interest at 95.00.

Are Bitcoin bulls here to stay?

Everyone's favorite cryptocurrency jolted to a record high above $6590 during Wednesday's trading session, as investors sprinted after the bullish train.

With CME announcing on Tuesday that it will launch Bitcoin futures later this year, some skepticism over Bitcoin was rinsed away, consequently boosting its allure to market players. It is simply remarkable how resilient Bitcoin has been in the face of significant negativity, with its value climbing more than 600%, to over $6000 this year. With the cryptocurrency repeatedly hitting record highs, are Bitcoin bulls here to stay?

The price action suggests that bulls have a very firm grip, with a breakout above $6600 potentially triggering an incline higher to uncharted territories.

Commodity spotlight - Gold

Gold was in hibernation this week as prices traded in a wide range, with support at $1267 and resistance at $1280. The yellow metal may be waiting for a catalyst to roar back to life, and this could be in the form of the FOMC on Wednesday or Trump's Fed head decision on Thursday. The technical picture continues to suggest that the price action remains tilted to the downside, with sustained weakness below $1280 opening a path back towards $1267 and $1260, respectively. In an alternative scenario, a breakout above $1280 may open a path higher towards $1290.

GBPUSD: Eyes More upside Pressure Towards Key Resistance

GBPUSD: The pair looks to strengthen further higher towards it key resistance at 1.3337. Support lies at the 1.3250 level where a break will turn attention to the 1.3200 level. Further down, support lies at the 1.3150 level. Below here will set the stage for more weakness towards the 1.3100 level. Conversely, resistance stands at the 1.3350 levels with a turn above here allowing more strength to build up towards the 1.3400 level. Further out, resistance resides at the 1.3450 level followed by the 1.3500 level. On the whole, GBPUSD continues to face further upside pressure on correction

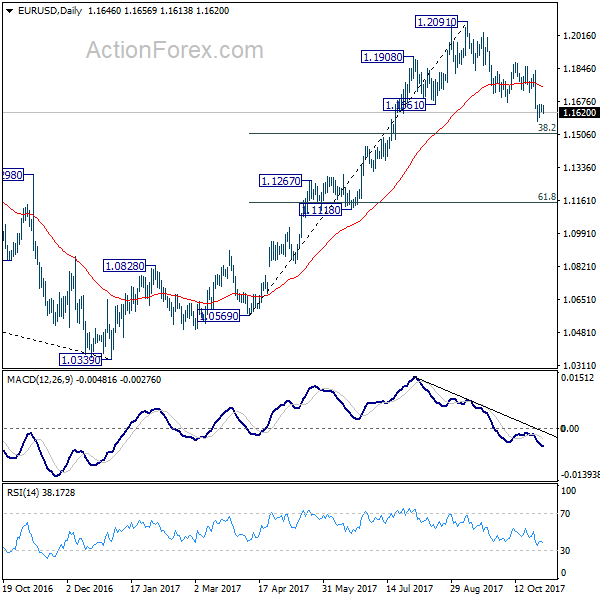

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1625; (P) 1.1643 (R1) 1.1663; More...

Consolidation from 1.1574 temporary low is still in progress and intraday bias remains neutral. As noted before, break of 1.1879 resistance is needed to confirm completion of the decline from 1.2091. Otherwise, near term outlook will stay bearish. Below 1.1574 will target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3219; (P) 1.3253; (R1) 1.3316; More....

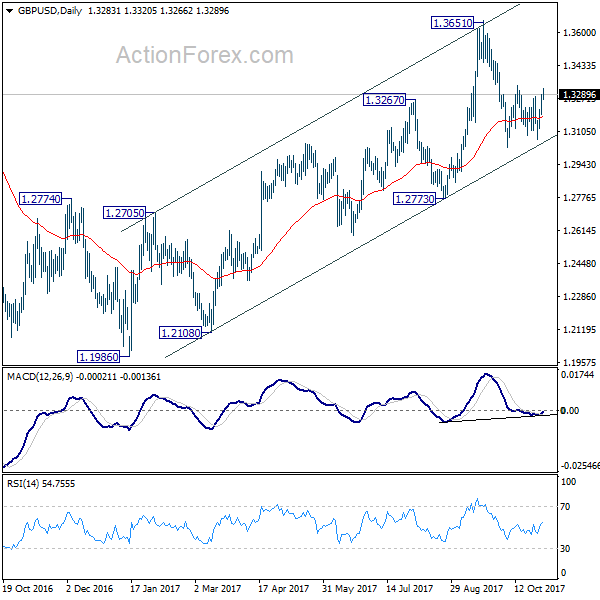

No change in GBP/USD's outlook despite current rebound. Price actions from 1.3026 is seen as a consolidation pattern. In case of further rise, upside should be limited by 61.8% retracement of 1.3651 to 1.3026 at 1.3412 to bring fall resumption finally. On the downside, firm break of 1.3026 support will resume the decline from 1.3651 and target 1.2773 key support level. This will also revive the case of medium term reversal. However, sustained break of 1.3412 will turn focus back to 1.3651 high.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll stay neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

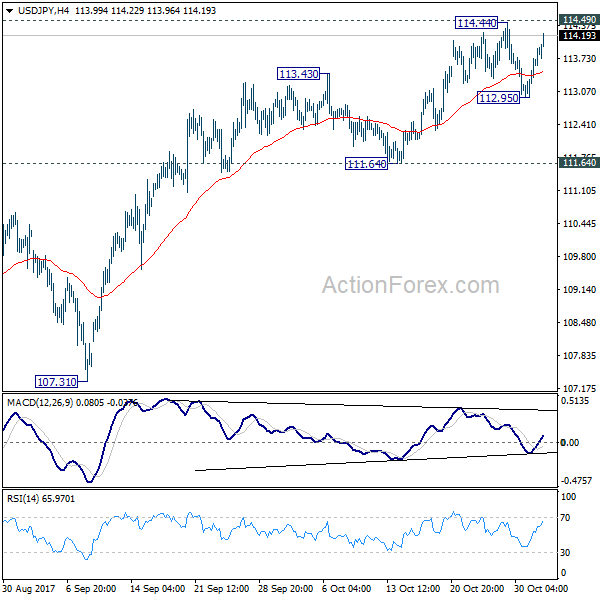

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.14; (P) 113.44; (R1) 113.92; More...

At this point, USD/JPY is still limited below 114.49 key resistance and intraday bias stays neutral first. Near term outlook will remain cautiously bullish as long as 111.64 support holds. Decisive break of 114.49 key resistance will confirm that correction pattern from 118.65 has completed at 107.31 already. And USD/JPY should then target a test on 118.65. However, sustained break of 111.64 will argue that rebound from 107.31 has completed and bring retest of this low.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

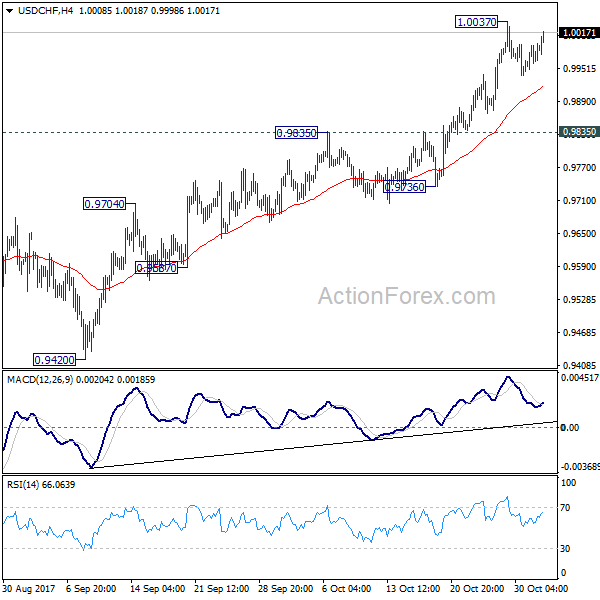

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9945; (P) 0.9969; (R1) 1.0001; More....

USD/CHF recovers further in early US session but stays below 1.0037 temporary top. Intraday bias remains neutral and more consolidation could be seen. In case of another retreat, downside should be contained above 0.9835 resistance turned support and bring rally resumption. Since 61.8% retracement of 1.0342 to 0.9420 at 0.9990 is already met, break of 1.0037 will turn bias to the upside for 1.0342 key resistance next.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

Markets Rally Ahead of Fed Decision

Optimism Returns After Brief Consolidation

US indices are on course to open around half a percentage point higher on Wednesday, as we enter the business end of what promised to be a very busy and important week for markets.

There's been no shortage of optimism in the equity market rally in recent weeks but as we entered month end it did appear to lose some of its spark, triggering some consolidation at record highs. With futures pointing to a higher open on Wednesday, it seems that spark may be returning, with optimism over tax reform and another solid earnings season providing the catalyst for the rally. The week has not been short of major economic events but the bulk of these, and arguably the most important ones, are still to come.

Fed Statement Eyed But Focus on Yellen Replacement

The Fed's monetary policy decision would typically be one of, if not the most important event of the week but that may not be the case today. For one, it's extremely unlikely that any change in interest rates will be announced, with December remaining far more likely for the final hike of the year. With Chair Janet Yellen not making an appearance after the announcement, we instead have to rely on the accompanying statement for clues as to whether another hike in December is still planned.

Moreover, with Donald Trump poised to announce who will succeed Yellen from February on Thursday, investors may take the statement with a pinch of salt when considering interest rates beyond the end of the year. All things considered, not only is today's announcement not the biggest market event this week, it's unlikely to even be the most important Fed event.

When it comes to the statement, I don't expect the central bank to deviate much, if at all, from previous rhetoric as the data has been broadly consistent with expectations, barring the understandable weak jobs report last month. This Friday's report is expected to be much better than normal which should mostly offset the weakness in job creation in September, something the Fed may allude to.

US Data Could Provide Pre-Fed Volatility

While Friday's jobs report will undoubtedly be the highlight of the economic data this week, there are a number of other releases today that will be of interest. The ADP number is typically eyed for insight into the direction that Friday's NFP number will take but with the September's release having been so far from the official number, expectations for the two are very different (200,000 for ADP, 312,000 for NFP). Still, it may provide some insight from a directional perspective, i.e. will the NFP bounce back and bring the average more in line with what we would expect.

The two manufacturing PMI surveys will also be tracked closely on Wednesday, as will the oil inventory data from EIA after API reported another sizable draw-down on Tuesday, almost double the number expected today. Oil has been well bid in recent months as the re-balancing efforts of oil producers brings inventories back in line with the five-year average.

With major producers discussing another extension to the output cut, it would appear that higher prices are not destabilizing efforts to bring the market back into balance. Higher global demand has been another supporting factor in the recent rally which has seen Brent hit its highest level in almost two and a half years.

Sterling Rallies Ahead of Potential BoE Rate Hike

The pound is rising ahead of Thursday's Bank of England meeting, at which the central bank is expected to announce its first rate hike in more than a decade. This morning's manufacturing PMI is largely behind the latest rally in the pound, with the survey having highlighted robust domestic demand as well as rising inflation pressures, something policy makers have become increasingly concerned about due to the already elevated price growth.

While above-target inflation is being almost entirely driven by the pound's post-Brexit drop, a growing number of policy makers now appear to be of the belief that last year's rate cut is no longer necessary and a return to the previous lower bound is warranted. Markets are heavily pricing in a rate hike tomorrow which may limit any upside in the pound in relation to this, with the accompanying commentary probably more important. With a split among policy makers being clear from recent commentary, a failure to hike tomorrow could trigger a sharp decline in the pound.

Markets Poised for a Dovish Rate Hike by Bank of England

The pound has been on an uptrend for much of 2017, led by a weaker dollar in the first half and by expectations of a UK rate rise in the second half. Its high of the year and post Brexit peak of $1.3656 was reached soon after the Bank of England's September policy meeting when MPC members signalled "some withdrawal of monetary stimulus is likely to be appropriate over the coming months".

However, recent communication by some policymakers has been not as hawkish, if not dovish, casting doubt about the Bank's intentions. The BoE's newest deputy governor, Dave Ramsden, recently said he was not part of the majority who in September saw a case for tightening policy soon. Another deputy governor, Jon Cunliffe, said the timing of a rate hike was an "open question". Meanwhile, Governor Mark Carney hasn't disappointed in living up to his reputation of flip flopping on policy, changing his tone from a hawkish one to a more cautious one at a recent hearing before Parliament's Treasury Select Committee.

The mixed signals from the British central bank have led investors to pare back their expectations of UK interest rate increases, pushing sterling to the $1.30-1.33 region from a brief spell above $1.36. Although most analysts are still predicting the BoE will raise rates for the first time in a decade by 0.25% to 0.50% on November 2, expectations for subsequent rate hikes have fallen to just one quarter percentage point increase in 2018.

A possible split vote on Thursday could diminish the odds of any follow-up move. Consensus forecasts are for a 6-3 vote in favour for a hike. A 5-4 vote would be viewed as very dovish and could send the pound lower to retest the $1.30 level, while a 7-2 vote could trigger a fresh rally, driving sterling back above $1.34.

In addition to the rate decision, the Bank's quarterly inflation report should also shed some light on future policy. Carney has said he expects inflation to rise further in the coming months above September's 3.0% level. A sharp upward revision to the inflation outlook would fuel expectations of more policy tightening in the coming months. The growth forecasts will also be watched closely following the surprise beat of third quarter GDP growth. The GDP figures may have helped ease the concerns of some MPC members that the UK economy is not strong enough to support higher rates.

However, even with more optimistic projections of growth and inflation, the ongoing Brexit uncertainty and the slowdown in consumer spending would likely prevent the Bank from moving too fast on rates, with the eventual outcome of Brexit playing a larger role on the pound's longer-term prospects than BoE policy.

Elliott Wave Analysis: EURUSD Can Reach 1.1450-1.1500 Zone

EURUSD broke down last week through 1.1730 level that cause a drop to a new low of the month which impacted some of recent bullish wave structure. What is really important at this stage is that current drop is accelerating which normally occurs in wave three, so we think there can be a new five wave drop in progress right now from 1.1870 since current leg is the strongest bearish reaction since September high. It's very important to listen to the market and not get to attached to the "bullish idea". That said, we adjusted the structure and are now looking at a three wave drop from the September high which can either be a new five wave drop in progress for new euro bearish cycle, or is going to be just a deep A)-B)-C) pullback. In either case there is room for pair to touch 1.1450-1.1500 area, especially if we consider an important zone on a daily time frame.

EURUSD, 4H

CAC Rally Continues On Strong Corporate Earnings

The CAC index continues to have a quiet week. Currently, the CAC is trading at 5,530.00, up 0.50% on the day. On the release front, there are no French or eurozone indicators. In the US, today’s highlight is the Federal Reserve rate statement. On Thursday, the focus will be on manufacturing, as France and the eurozone release Final Manufacturing PMI.

The CAC continues to move upwards, and has climbed 2.8% since October 23. European stock markets have posted strong gains on Wednesday, in response to positive European corporate earnings. Strong performers on the CAC include French car makers Peugeot and Renault, which have gained 1.67% and 0.87%, respectively. On Tuesday, French data was positive, as the French economy continues to improve. Flash GDP remained at 0.5% in the third quarter, matching the estimate. Consumer spending rebounded with a gain of 0.9%, beating the estimate of 0.6%. Preliminary CPI improved to 0.1%, matching the forecast.

After staying on the sidelines for months, the ECB announced last week that it will begin tapering its asset purchase program, from EUR 60 billion/mth to EUR 30 billion/mth. The program, which was scheduled to end in December, has been extended to April 2018. However, ECB President Mario Draghi added a dovish twist to the move, stating that the program would remain open-ended. This provides the cautious ECB with the ability to keep the program in place beyond April without causing strong movement in the currency and stock markets. The euro has reacted sharply to ECB moves (or lack of a move) in the past, and Draghi would like to minimize the ECB’s involvement in market movement.