Sample Category Title

USD/JPY Buying Demand Remains Strong

USD/JPY is riding higher within short-term uptrend channel. Key resistance stands at 114.49 (11/07/2017 high). Support is located at 111.12 (20/09/2017 low).

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

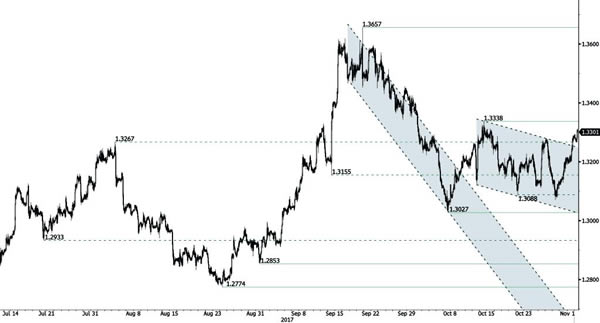

GBP/USD Pushing Higher

GBP/USD has successfully broken support at 1.3088 (12/10/2017 low) before bouncing back. Resistance lies at 1.3338 (13/10/2017 high). Expected to show further increase within uptrend channel.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. Long-term support can be found at 1.1841 (07/10/2017 low). Long-term resistance given around 1.35 is at stake and indicates a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Continued Consolidation

EUR/USD is consolidating higher after setting a new hourly support at 1.1575 (27/10/2017 low). Hourly resistance is located at 1.1658 (30/10/2017 high). Expected to show some shortterm consolidation.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

USD Holds Steady Ahead Of FOMC And ADP

Further upside in USD/CHF

Switzerland Manufacturing PMI came in at 62.0 from 61.7 and 0.7 higher than expectations. This continued a strong trend of economic improvement in manufacturing reaching the highest level since 2011. Last week Kof leading indicators jumped to 109.1 from 105.8. With a weaker CHF and further improvement in global demand Switzerland is uniquely positioning to exploit the opportunity. This fact is clearly reflecting in the increased upside surprises. Interestingly and quietly consumer price inflations has been slowly creeping higher as annual headline read stands at 0.7%.

Should the current inflation trajectory continue prices should hit the SNB 2% target in early 2019. While a year away with Swiss GDP growth outlook improving above 0.9% 2017 trend, the central bank will be faced with interesting policy choices in 2018. Yet in the current environment, CHF remains a solid short against USD and EM currencies. Accelerating outflows and dropping FX hedge ratios will further weaken the CHF. But the key of an unmoving SNB unlikely to unwind reserves of adjust policy rates higher until CHF become less “overvalued” is the primary reason investors will shift out of CHF. We remain constructive on USDCHF expecting current bullish trend will extend to 1.02.

High expectations for the US ADP data before the FOMC meeting

Today we get US labor ADP data ahead of the NFP report on Friday. Bloomberg Survey indicates new jobs creation for October of 200k compared to the prior September read of 135k. The overall sentiment is positive and it has been 7 years that the data print positive. The third quarter GDP has been released earlier last week at 3% q/q. Anyway it is worth saying that before this release GDP growth was in its second-worst year since 1959. On top of that credit demand is contracting which should weigh on growth and tax receipts remain negative.

This is why traders will clearly have the downside risks in the back of their minds. ADP has had a history of spectacular misses for predicting NFPs over the past months. Last time ADP predicted 135 new jobs while NFPs came in negative. Yet, statistically speaking, ADP has more often been a pretty accurate forecast for the NFP change.

Tonight will be held the FOMC meeting against the backdrop of the coming nomination of the new Fed Chair that will replace Janet Yellen early next year. Markets now expect a rate hike in

December. It is currently priced in at 66.8%. We suspect that ADP is likely to print below the current expectations following September NFPs. A poor labor read will keep adding downside pressures on the greenback lower, and fuel the main country equity indexes as a US weak economy will push away Fed rate-tightening policy discussion. We think that the room is open for short-term weakness on the dollar.

USD/CAD: Canadian Gross Domestic Product

The Canadian Dollar weakened significantly against the Greenback, reflecting disappointing GDP data on Tuesday. The USD/CAD currency pair added 69 base points or 0.54% to return to the past week’s high of 1.290 and remained in the area by Wednesday morning.

Statistics Canada revealed that the country’s gross domestic product contracted surprisingly 0.1% in the month of August, following the flat reading in the prior month. Data suggested that the decline was caused by maintenance shutdowns in the extractive and chemical industries. Back to the previous week, the Bank of Canada diminished its yearly growth projection to 1.8% in the Q3, and confirmed its cautious stance about the next interest rate increases.

EUR/USD: EZ Gross Domestic Product

The EZ GDP report failed to change the side move in the EUR/USD currency pair on Thursday. After the release, the Euro added 1 pip against the US Dollar to reveal bulls' attempts to get back the strong footing for the currency, but the pair returned to 1.1630 on Wednesday.

The Eurostat release showed that the Euro zone's quarterly GDP growth was slightly weaker at 0.6% in the September quarter. However, the yearly GDP growth rate edged higher to 2.5% in the Q3. Data also showed the bloc's unemployment rate dropped to its nine-year low in the observed period. The Euro zone's consumer inflation showed some signs of cooling, with the CPI at 1.4% in October, though analysts suggested it could reach 2% target in the next year.

XAU/USD Analysis: Tests 200-Hour SMA

As soon as markets found out that one the leading indicators, the Consumer Confidence Index, substantially exceed expectations the rate plunged to the 1,269.37 level. Nevertheless, the upcoming FOMC meeting as well as employment data release do not allow reinforcing this success. On the other hand, in order to break to top the pair still needs to bypass the weekly PP, the upper boundary of a descending channel and, most importantly, the 200-hour SMA. Previous failed attempts suggest that until the first release these barriers are likely to constrain active rise of the yellow metal's price. In case of positive news, the pair is expected to repeat previous Thursday's downfall and reach the weekly S1 at 1.264.23.

USD/JPY Analysis: Surges Above 113.80

As it was expected, a release of positive consumer sentiment data elevated the pair to the 113.70 mark, which represented an approximate location of different moving averages. During this trading session the exchange rate most probably is going to climb even higher amid the US labour data release and the subsequent Fed meeting. If that is the case, the pair is likely to break through resistance located between the 114.25 and 114.35 marks and try to reach the July 2017 maximum at 114.50. Generally, this advance is expected to have limited effect, as two days ago the pair made breakout from a long-term rising wedge formation. From this perspective, the Yen is expected to start slowly recovering against the Dollar in the nearest future.

GBP/USD Analysis: Rapidly Climbs To 1.3280

Although the US economy showed convincing signs of growth, the Pound continued to rapidly appreciate against the Dollar yesterday. The fact that the cable managed to return to mid-October level near 1.3295 indicates how actively traders are anticipating interest rate hike by the Bank of England, which even overshadows today’s FOMC meeting. From technical point of view, there is a need to notice that both on hourly and daily timeframes the pair is free to surge up until the weekly R2 located at the 1.3370 level (after passing through the above resistance). Until release of the American data, the pair is expected to move horizontally near 1.3270. Afterwards, in case of plunge it is likely to be stopped by the 200-hour SMA fluctuating near 1.3180.

EUR/USD Analysis: Moves Horizontally In Anticipation Of FOMC Meeting

Despite a release of various macroeconomic data yesterday, including the Euro Zone CPI and CB Consumer Confidence, the pair did not make any sharp moves and continued to move horizontally between the 100- and 55-hour SMAs. Such indifference nicely illustrates how traders are anticipating the upcoming FOMC Monetary Policy Statement and appointment of the new Fed Chair by President Trump. Given that yesterday’s information appeared to be better than expected plus general consensus that today’s meeting will not bring any unexpected news suggests that the pair is likely to continue moving horizontally between the 1.1658 and 1.1625 levels with a tendency to stick to the southern direction. A major breakout to the top also looks unlikely because that side contains multiple barriers.