Sample Category Title

Crude Oil Remains Bullish…But For How Long?

Key Points:

- Brent tops $60.00 a barrel.

- Saudi Oil Minister suggests production cuts to be extended.

- Shale oil production likely to be stood up in the coming weeks.

The past few weeks have seen crude oil prices surging as plenty of rhetoric, along with some fundamental bumps, have buoyed the commodity. Subsequently, both WTI and Brent prices have reached levels not seen since the latter part of 2016. In particular, the price of Brent has risen above the mythical $60.00 handle and looks to be gaining steam for additional gains in the coming days. However, it remains to be seen if prices can retain their buoyancy above what some in the market consider being an advantageous level for shale production stand ups.

Subsequently, you would be forgiven for questioning the sustainability of the recent rally given that the U.S. shale oil industry is presently hanging over the market like a hammer. The $60.00 handle has long been seen as the marginal profit level for even the high cost American shale producers which suggests that we could see some significant increases in rig counts and production as prices exceed this level. So you would be forgiven for expecting Brent and WTI prices to start falling any moment.

However, as always within energy markets, there are multiple variables at play impacting the commodity. Subsequently, last week's rhetoric from the Saudi Oil Minister on extending the production cuts has been met with plenty of bullishness as the markets grapple with to what extent OPEC is able to impact world prices on a long term basis. Additionally, U.S. crude inventories, along with the rig count actually declined in the past day which certainly provides some contradictory signals.

Regardless, the reality is that any rally is likely to be defeated by increasing U.S. shale production over the medium term until a total rebalancing of crude markets is completed. Also, the actual compliance with the OPEC production caps is slowly declining as domestic economies feel the pinch of reduced sales. Subsequently, if compliance continues to decline we could see further fracturing amongst various OPEC member states and this means lower oil prices in the short-medium term.

Ultimately, there is plenty of more pain to come for producers within the Crude Oil sector and the recent topping of prices simply puts us back to square one with the ongoing need to rebalance supply. The most likely scenario that we see for the near term is for Brent to range between $54.00 - $57.00 a barrel as we move towards the winter season. However, keep a close watch on the commodity because, regardless of any buoyancy, prices will still need to come down in the long term prior to stabilising.

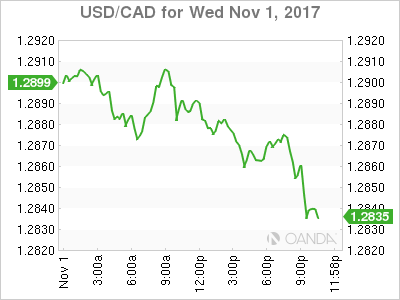

USD/CAD Canadian Dollar Higher After Fed Holds Rates As Expected

The Canadian dollar gained on Wednesday after the U.S. Federal Reserve ended its two day Federal Open Market Committee (FOMC) meeting and left the benchmark borrowing rate untouched at 100–125 basis points. The move was expected by the market with investors looking ahead to the December meeting for a third rate hike in 2017.

The loonie gained back some of the losses in the week, but it still down 0.49 in a weekly basis. The Canadian currency reached a high after the surprise rate hike by the Bank of Canada (BoC) on September 6 took the benchmark interest rate back to 1.00 percent. Governor Poloz had proactively cut twice in 2015 to help the Canadian economy withstand the fall in oil prices. With a more stable energy market and a strong economic growth the BoC withdrew that stimulus.

The contraction of Canada's monthly GDP by 0.1 percent in August had been foretold by various indicators. The Canadian economy was slowing down and the tone of the central bank was changing from the hawkish tone seen in the summer.

Growth in the United States in the meanwhile has been strong with the only concern for the Fed the persistent low inflation. It is that inflation that divides the FOMC ahead of the December meeting. The Fed has surprised this year by ditching the cautious script from years past and into a more proactive role. Chair Yellen has said that at this point waiting on raising rates could be more harmful. The December rate hike could end up being the last monetary policy action from Yellen. She is not a favourite to retain her Chair position. The Fed's Jerome Powell and Stanford's John Taylor are now in the lead, with the scenario of one become Vice Chair and the other Chair a growing possibility.

The USD/CAD lost 0.11 percent on Wednesday. The currency is trading at 1.2870 after the Federal Open Market Committee (FOMC) statement saw the Fed hold interest rates again. The lack of new information on what the Fed will do on December make it easier for the loonie to recover some of the lost ground.

Canadian manufacturing showed more signs of slowdown. Manufacturing PMI fell to 54.3 and is now the lowest it has been since January. The reading is still above 50, which is the gauge of growth. Weather related shortages in the United States affected Canadian companies.

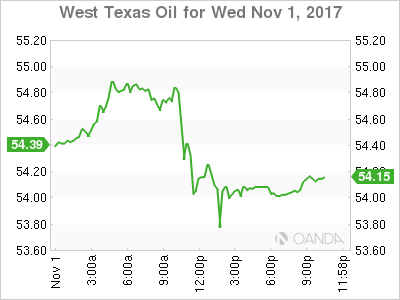

Oil prices fell slightly in the last 24 hours. The price of West Texas Intermediate is trading at $54.06 on a day with see-saw trade action after the American Petrol Institute released on Tuesday night had created anticipation around a 5.1 million barrel drawdown. The Energy Information Administration (EIA) weekly crude inventories showed a larger than forecasted 2.4 million barrels but still short of the API shortfall which prompted a correction in prices.

The cuts to production agreed by Organization of the Petroleum Exporting Countries (OPEC) and other major producers have achieved stability in the oil market and the promise of extending those cuts have taken oil prices to mid 2015 levels. Doubts still remain on how much demand has really recovered. The stability in prices can be easily disrupted as soon as the US shale industry shakes off the effects of the hurricane season and increases the rig count to take advantage of the rising price of crude.

Market events to watch this week:

Thursday, November 2

5:30 am GBP Construction PMI

8:00 am GBP BOE Inflation Report

8:00 am GBP MPC Official Bank Rate Votes

8:00 am GBP Monetary Policy Summary

8:00 am GBP Official Bank Rate

8:30 am GBP BOE Gov Carney Speaks

8:30 am USD Unemployment Claims

8:30pm AUD Retail Sales m/m

Friday, November 3

5:30 am GBP Services PMI

8:30 am CAD Employment Change

8:30 am CAD Trade Balance

8:30 am CAD Unemployment Rate

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

8:30 am USD Unemployment Rate

10:00 am USD ISM Non-Manufacturing PMI

FOMC Upgraded Growth Assessment First Time In Two Years, December Hike On Track

As widely anticipated, the November FOMC meeting contained few changes from the previous one. The members left the target range of the Fed funds rate unchanged at 1-1.25%. One surprise came from the upgrade of the growth assessment to 'solid' for the first time since 2015, despite disruptions by hurricanes. Inflation stayed below the +2% target and the members acknowledged that core inflation 'remained soft'. However, the encouraging growth outlook and further decline in the unemployment rate suggest that a December rate hike remains on track.

Policymakers upgraded the growth outlook and shrugged off the impacts of hurricanes. As noted in the accompanying statement, 'economic activity has been rising at a solid rate despite hurricane-related disruptions. Although the hurricanes caused a drop in payroll employment in September, the unemployment rate declined further'. In September, they noted that that economic activity has been 'rising moderately so far this year. Job gains have remained solid in recent months, and the unemployment rate has stayed low'. Recognizing growth as 'solid' for the first time in 2 years signaled that Fed's confidence in the economic firm-footing. In shorts, the members were not concerned about the hurricane-related disruptions. They believed that 'rebuilding will continue to affect economic activity, employment, and inflation in the near term, but past experience suggests that the storms are unlikely to materially alter the course of the national economy over the medium term'. At the same time, the Fed acknowledged the weakness on inflation, although hurricanes had boosted gasoline prices, which in turn lifted headline inflation in September. The members indicated that 'inflation for items other than food and energy [core inflation] remained soft'. They noted that CPI measures 'have declined this year and are running below +2%'. On net, the Fed continued to characterize the near-term risks to the economic outlook as 'roughly balanced', and it would continue 'monitoring inflation developments closely'.

A highlight of the meeting was the update of the balance sheet reduction program which took effect in October. However, there was only brief touch on this issue. The statement suggested that balance sheet normalization was 'initiated' in October and 'is proceeding'. There were no dissents. Last month, the Fed began the process of reducing its US$ 4.5 trillion balance sheet which is comprised mainly of bonds. In the plan announced in June, the Fed set an initial cap at US$ 10B/month. That is, the caps start for the first three months at US$6B and US$4B for Treasuries and MBS respectively, before rising each quarter until they reach US$30B and US$20B per month Treasuries and MBS respectively, by October 2018.

The November statement signals that the Fed is on track to raise the policy rate again in December, assuming no material deterioration of the economic development. The next focuses are the announcement of the next Fed chair (US President Donald Trump has intended to announce it Thursday US Time), a drafted tax reform bill and the November employment report due Friday.

FOMC Review: Overshadowed by Fed Chair Announcement Tomorrow

As expected, the Fed decided to maintain the target range at 1.00%-1.25% at this meeting.

Also as expected, there were no major changes to the statement. As expected, the Fed still says that it is monitoring inflation closely. The Fed says that the dip in employment in September was due to hurricanes and, as it has previously said, it will not put too much weight on negative economic data caused by hurricanes. The reason is that it thinks it is temporary - a view we share.

It remains our base case that the Fed hikes again in December (in line with market pricing and consensus) and twice next year. However, it is difficult to forecast what the Fed is going to do next year, as we still do not know the new 'team' yet.

The meeting is overshadowed by the fact that President Trump is likely to announce the next Fed chair tomorrow "afternoon" (US time, so likely tomorrow night CET). It remains our base case that current Fed governor Powell is going to succeed Yellen. Powell is a 'status quo' candidate in the sense that he is considered to be a centrist like Yellen and he will most likely continue the current monetary policy strategy of gradual Fed hikes. Still, we could see a slightly dovish reaction to a Powell nomination, as we cannot rule out that Trump is going to nominate John Taylor instead, who has said he thinks US monetary policy is too easy at the moment.

Note that the Republicans are now expected to unveil the long-awaited tax plan tomorrow (likely around 14:00 CET). Originally, it was planned to be unveiled today but it was postponed due to internal disagreement between Republicans. US tax reform has become more likely after House Republicans have accepted that tax reform will be deficit-financed. That said, one problem is that the current proposal is likely too expensive given that the Republicans have only made room for a total of USD1,500bn tax cuts over 10 years.

Few Changes from the Fed as December Hike Appears on Track

Our Take:

The Fed once again showed no inclination to change monetary policy at a non-press-conference meeting, holding the fed funds rate in a 1.00-1.25% range as expected. The updated policy statement was plain vanilla with a nod to some transitory hurricane effects - higher inflation and lower employment - and a decent Q3 growth outturn despite weather-related disruptions. The usual themes of a strong labour market and soft inflation were unchanged, with the latter still expected to hit the Fed's 2% objective over the medium term.

There was no overt signal in today's statement that the Fed is set to raise rates in December, but we don't think that should dent the odds of such a move. The Fed's forecasts from September remain largely on track. If anything there is a bit of upside to their GDP forecast for the current year after Q3 growth held up at 3%. Inflation continues to be disappointing but is not far from what the Fed has penciled in for the end of the year. All told, we see little reason for the 12 of 16 FOMC members who thought another rate hike would be warranted by end of year to change their minds. Markets are of the same view with a December rate increase almost fully priced in.

We continue to think steady but gradual rate hikes are in store next year, though the Fed's 'dot plot' shows a wide range of views on how much tightening is appropriate. And a change in Fed leadership - possibly being announced as early as tomorrow - only adds to uncertainty about the future path of monetary policy.

Fed Holds the Line on Rates in November

As expected, the Federal Open Market Committee (FOMC) left rates on hold at a target range of 1 to 1-1/4 percent.

The statement noted the disruptions to economic activity and inflation caused by the late-summer hurricanes. Outside of this, the overall economic outlook remained unchanged, the labor market continues to strengthen, but inflation remains "soft" and below its 2% target.

Key Implications

There is very little to comment on in this statement. As broadly expected, the Fed held the line on rates and noted, once again, the dilemma between a strengthening economy and stubbornly weak inflation.

The inflation outlook will be central to the conduct of monetary policy over the next year. As some of the idiosyncratic factors weighing on price growth diminish, and the unemployment rate continues to push further below its natural rate, inflation is likely to gain traction in the year ahead. The Fed should see enough evidence for this proposition when it meets next in December, allowing them to raise rates by 25 basis points.

Fed Waits, BOE Next

The Fed touted better growth but the FOMC statement reiterated concerns about low inflation. The New Zealand dollar was the top performer after solid jobs figures, while the Swiss franc lagged. Australian trade balance is due next followed the BoE decision on Thursday. 2 GBP and 1 FTSE trades are in progress.

The Fed decision was a bit of a dud in terms of market moves. The initial reaction was to sell the US dollar as the Fed indicated inflation has declined this year but it quickly rebounded on an upgrade in the growth assessment to 'solid' from 'moderate'.

USD traders now shift to Thursday's tax plan. A Congresswoman said the details will be released at 9 am ET (1300 GMT). The drawback to much details is disappointment. Political spin is sure to come from deficit hawks. The grandstanding will be intense and that might prompt a move to safe havens.

The other US news to come on Thursday will be the Fed chair decision. However, a late-breaking report says Powell has been told the job is his. That decision was mostly priced in and the attention will now turn to his comments during confirmation and signals on future hikes.

Before that, data on Australian trade balance is due at 0030 GMT. The consensus is for a surplus of A$1.2B and any miss could send another jolt through AUD trading.

The bigger market mover will be the Bank of England decision. The market is pricing in a 90% chance of a hike so the bigger driver will be signals about what's next. The BoE Minutes will show the extent of unanimity, the BoE inflation report should enlighten on inflation and growth revisions and forecats, while Carney's testimony never disappoints.

Plenty of market watchers are talking about a one-and done but the market is pricing in a 37% chance of a second hike in February. That's a low bar. Carney could sound his usual neutral stance, but if he's constructive about growth then it would leave the door open for that second hike.

Few Surprises from the FOMC

Few Surprises from the FOMC

No surprises overnight as the FOMC did little more than confirm what we already knew; the economy is robust, but inflation is missing in action.

And while the FOMC was on everyone's radar, to be frank, other than tax reform uncertainty inspired position covering and sporadic bouts of profit taking the FX markets remain stuck in the muck, but that's about to change.

There's a lot of factors in play on Thursday with the BoE meeting and the House Republican tax announcement, and for all intensive purposes, the cat appears to be out of the bag as Jerome Powell is reported to be the next Fed Chair to smiles and congratulations by all those concerned.

The tax reform release will no doubt send traders into information overload as the complexities of this deal will probably challenge even the most astute Chartered Accountant.

On the economic front, investors largely overlooked a fresh cluster of data despite the ADP Employment report showing a forecast-beating increase of 235,000 jobs (which was well above the forecast for a 200,000 rise). The dollar did get a small bump. but with bigger fish to fry, few were in the mood to push the greenback higher. But if anything can be gleaned from overnight price action is that a combination of robust data and a cheery Fed has resulted in a modest gain in US equity markets and a small bounce in USD sentiment.

The British Pound

The BoE is likely hike interest rates but will probably struggle to promote any market expectations to reprice more hikes in for 2018 given uncertainty about Brexit. Regardless , the market remains tentatively bullish on GBP on the rate differential curve while betting on a cleaner Brexit divorce proceeding heading into year-end.

The Euro

Activity on the EURUSD was remarkably tame again.The anticipated USD follow through demand after the dovish ECB taper has failed to materialise, and with few surprises from the FOMC conviction, one way or the other trade remains hugely muted. I suspect traders will continue to respect the current ranges.

The Japanese Yen

The markets remain guardedly optimistic that the tax reforms will be in place by Christmas while traders discount the possibility of phasing in of tax changes on the assumption that something is better than nothing, In addition, the markets are hanging their hat on the fact that with no change in Abe's cabinet it supports pro-economic growth policies to remain intact. Without sounding like a broken record, the long USDJPY trade continues to look favourable.

The Australian Dollar

Trade balance later today is expected to come out lower but for the most part, the Aussie should remain parked in Neutral until Fridays retail sales but with traders eyeing next weeks RBA and the real possibility of stronger worded dovish guidance, the AUD remains in a state of heightened vulnerability.

(FED) FOMC Statement November 01, 2017

Information received since the Federal Open Market Committee met in September indicates that the labor market has continued to strengthen and that economic activity has been rising at a solid rate despite hurricane-related disruptions. Although the hurricanes caused a drop in payroll employment in September, the unemployment rate declined further. Household spending has been expanding at a moderate rate, and growth in business fixed investment has picked up in recent quarters. Gasoline prices rose in the aftermath of the hurricanes, boosting overall inflation in September; however, inflation for items other than food and energy remained soft. On a 12-month basis, both inflation measures have declined this year and are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. Hurricane-related disruptions and rebuilding will continue to affect economic activity, employment, and inflation in the near term, but past experience suggests that the storms are unlikely to materially alter the course of the national economy over the medium term. Consequently, the Committee continues to expect that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace, and labor market conditions will strengthen somewhat further. Inflation on a 12-month basis is expected to remain somewhat below 2 percent in the near term but to stabilize around the Committee's 2 percent objective over the medium term. Near-term risks to the economic outlook appear roughly balanced, but the Committee is monitoring inflation developments closely.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 1 to 1-1/4 percent. The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The balance sheet normalization program initiated in October 2017 is proceeding.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Patrick Harker; Robert S. Kaplan; Neel Kashkari; Jerome H. Powell; and Randal K. Quarles.

Will Super Thursday Live Up to its Name?

BoE Has Prepared Markets For a Rate Hike, Will it Deliver?

On Thursday, the Bank of England is widely expected to do something that a large group of people will never have experienced, raise interest rates.

For the first time in a decade and the first since the global financial crisis, policy makers will discuss the merits of a rate hike in a bid to prevent inflation moving too far above target. Or at least, that's what we're being told despite the acknowledgement that higher inflation is almost entirely down to the one-off currency depreciation that occurred since the Brexit referendum last year.

Inflation reached 3% in September, far above the central bank's 2% target and at the top of the range that the government deems acceptable before Governor Carney must write a letter to the Chancellor explaining why the central bank is failing to achieve its mandated target.

Interestingly, this is also around the level that the central bank expects inflation to peak at which begs the question why they've waited so long to raise interest rates. Also, why do they now deem it to be the right time to do so before we have a chance to find out how far it will fall again once the initial impact of the currency move falls out of the calculation?

If Inflation is Above Target, Why is a Rate Hike So Controversial?

As is to be expected in post-Brexit Britain, the decision on whether or not to raise interest rates is far from straightforward. This is clearly evident when listening to one of Carney's press conferences or appearances before the Treasury Select Committee, as well as in the rhetoric from his colleagues on the Monetary Policy Committee.

Not only does the inflation data and outlook not necessarily warrant a rate increase but the uncertain economic outlook muddies the water even further, which explains the divide on the committee.

It's quite clear that the economy has slowed since the vote last year, with the country falling from the top of the G7 growth table to the bottom in the first half of the year. Employment may have remained strong for now but with real wage growth having turned negative and spending slowed, it's clear that the economy is stalling which begs the question, is it really the correct time to raise interest rates?

The argument for the hawks on the MPC is that the economy hasn't slowed as much as was feared in the months after the referendum - partly due to the actions it took - and so a reversal of the rate cut in August 2016 makes sense.

While this hasn't been acknowledged by policy makers, there may also be a case that the BoE took a risk when cutting interest rates last year, taking base rate below the level that for the seven years previous was deemed to be the lower bound. Perhaps this is no longer seen as being a risk worth taking.

If this is the case then the BoE may refrain from committing to, or even hinting at, further rate hikes in the foreseeable future, which you would expect if this was in fact the beginning of a tightening cycle. Instead it may opt for the ECB approach of data dependent decision making. In other words, the less we know the better.

How Will Markets React to a Rate Hike?

Despite the divisions that we've seen within the MPC and the fact that the decision appears far from straightforward, investors are almost entirely convinced that the BoE will raise interest rates tomorrow. In fact, according to Reuters, a rate hike is almost 90% priced in. That would suggest to me that a rate hike alone won't be enough to lift the pound or UK yields too much. A change of heart on the other hand could deal a big blow to both, not to mention the central banks credibility.

How the pound trades - and the FTSE for that matter, don't forget the inverse correlation that the two share - in the aftermath of the decision will likely depend on the minutes, economic projections and press conference that accompanies the decision.

GBP Currency Index vs FTSE 100

Source - Thomson Reuters Eikon

Any indication that more rate hikes are planned for next year could trigger a sharp rally in the pound as I'm not convinced this is currently priced in, while anything else may weigh on the currency once the initial volatility - of which I expect a lot - has passed.

Super Thursday may for once live up to its name and I'm sure markets will be very sensitive to what policy makers have to say about the path of interest rates going forward, whatever the decision. Given the range of outcomes that we could see tomorrow, UK markets could get extremely volatile and the upside and downside potential should not be underestimated.

A hawkish rate hike from the BoE could see GBPUSD blow through 1.33 and see 1.36 being tested once again while no rate hike could see 1.30 severely tested, the success of which may depend on whether the increase is slightly delayed or postponed. In the case of the latter, I wouldn't be surprised to see 1.28 tested in the not-too distant future.