Sample Category Title

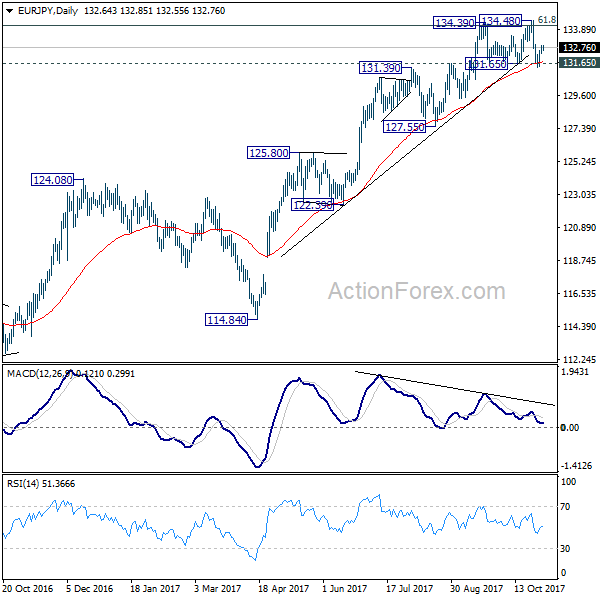

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.36; (P) 132.59; (R1) 132.90; More....

Intraday bias in EUR/JPY remains neutral for the moment. Focus remains on 131.65 key support. On the downside, decisive break of 131.65 will confirm rejection from 134.20 fibonacci level. That will also complete and double top pattern (134.39, 134.48) and confirms near term reversal. 55 day EMA will also be firmly taken out. In that case, deeper decline should be seen back to 127.55 key support. On the upside, decisive break of 134.39/48 resistance zone is needed to confirm up trend resumption. Otherwise, even in case of rebound, near term outlook is neutral at best.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversed and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

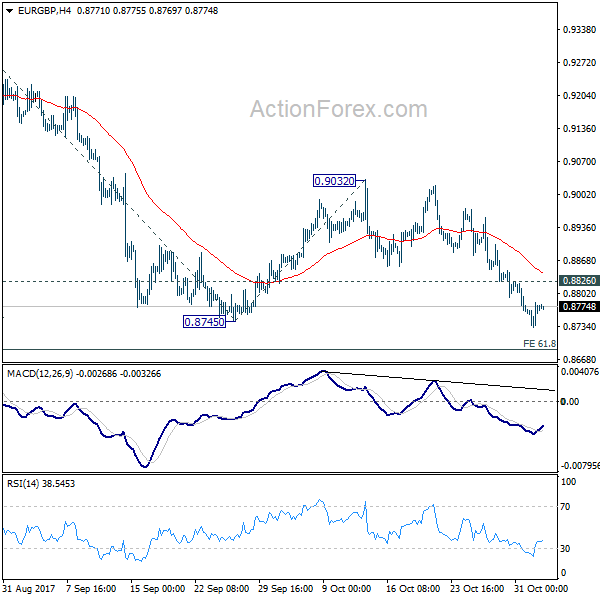

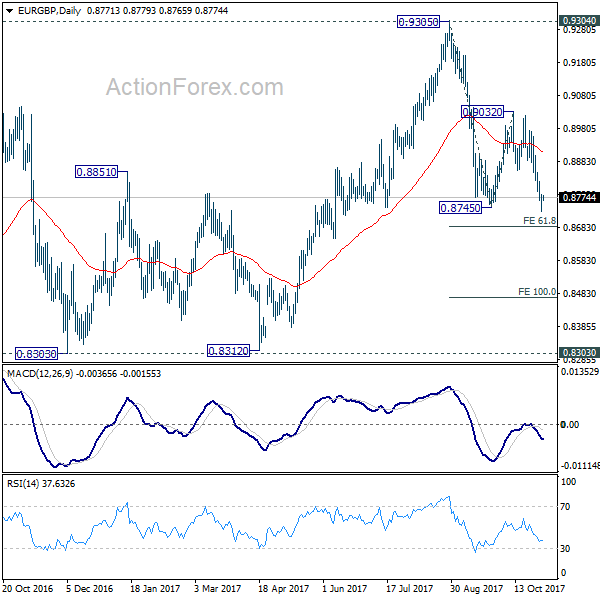

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8741; (P) 0.8762; (R1) 0.8791; More...

Break of 0.8745 suggests that fall from 0.9305 is resuming. Intraday bias is back on the downside for 61.8% projection of 0.9305 to 0.8745 from 0.9032 at 0.8686 first. Break will target 100% projection at 0.8472. On the upside, above 0.8826 minor resistance will turn intraday bias neutral first. But near term outlook will remain bearish as long as 0.9032 resistance holds.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of another fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Australia’s Trade Surplus Surged To Its Highest Level In Four Months In September, Building Approvals Gained

For the 24 hours to 23:00 GMT, the AUD rose 0.27% against the USD and closed at 0.7675.

LME Copper prices rose 1.7% or $116.0/MT to $6918.0/MT. Aluminium prices gained 2.2% or $48.0/MT to $2188.0/MT.

Overnight data showed that Australia's trade surplus widened more than expected to A$1.75 billion in September on the back of a boost in exports, from a revised surplus of A$873.0 million in the prior month. Markets had expected the trade surplus to increase to A$1.20 billion. Also, the nation's exports rose 3.0% in September, while imports remained unchanged. Separately, building approvals in Australia rose 1.5% MoM in September, confounding market expectations for a 1.0% decline. In the previous month, building approvals had risen 0.4%.

In the Asian session, at GMT0400, the pair is trading at 0.7725, with the AUD trading 0.65% higher from yesterday's close.

The pair is expected to find support at 0.7679, and a fall through could take it to the next support level of 0.7634. The pair is expected to find its first resistance at 0.7748, and a rise through could take it to the next resistance level of 0.7772.

Traders will now keep an eye on Australia's AiG performance of service index for October, set to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the EUR declined 0.26% against the USD and closed at 1.1619.

The US Federal Reserve (Fed), at its recent policy meeting, decided to keep its benchmark interest rate target between 1.00% and 1.25%, as widely expected by market participants, and struck a positive tone on the current state of the US economy. In its policy statement, the central bank highlighted that the US labour market has continued to strengthen and that economic growth has been rising at a robust pace, despite some disruptions caused by recent hurricanes, suggesting that an interest rate hike is most likely in December.

On the macro front, the US ISM manufacturing PMI dropped more than anticipated to 58.7 in October, compared to a level of 60.8 in the previous month. Markets had expected the ISM manufacturing activity index to fall to a level of 59.5. Also, the final US Markit manufacturing PMI rose to 54.6, compared to market expectations of a rise to a level of 54.5. In the prior month, the manufacturing PMI had registered a reading of 53.1. In the job market report, the private sector employment in the US advanced by 235.00K in October, following a revised increase of 110.00K in the prior month. Markets were anticipating the private sector employment to gain 200.00K.

Moreover, US construction spending unexpectedly climbed by 0.3% in September, compared to a revised rise of 0.1% in the previous month. Market anticipation was for construction spending to ease 0.2%. Additionally, US mortgage applications slid 2.6% in the week ended 27 October 2017 from a drop of 4.6% in the prior week.

Separately, news surfaced that US President, Donald Trump, might appoint Fed Governor, Jerome Powell, as the next Fed Chairman. The announcement is expected to be made by the President today.

In the Asian session, at GMT0400, the pair is trading at 1.1657, with the EUR trading 0.33% higher from yesterday’s close.

The pair is expected to find support at 1.1618, and a fall through could take it to the next support level of 1.1579. The pair is expected to find its first resistance at 1.1684, and a rise through could take it to the next resistance level of 1.1711.

Moving forward, Eurozone’s final manufacturing PMI for October, and Germany’s unemployment rate and manufacturing PMI, would be closely assessed by traders. In the US, weekly initial jobless claims and non-farm productivity data for the third quarter, both due later today, would be on investors’ radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Pound Trading Higher Ahead Of BoE’s Monetary Policy Meeting

For the 24 hours to 23:00 GMT, the GBP declined 0.29% against the USD and closed at 1.3249.

Macroeconomic data showed that UK's manufacturing PMI rose to 56.3 in October due to a surge in new orders, from a revised reading of 56.0 for September. Analysts had forecasted a reading of 55.9. Moreover, the seasonally adjusted house prices recorded a rise of 0.2% in October in the UK, in line with market expectations. In the previous month, house prices had registered a revised rise of 0.4%.

In the Asian session, at GMT0400, the pair is trading at 1.3285, with the GBP trading 0.27% higher from yesterday's close.

The pair is expected to find support at 1.3244, and a fall through could take it to the next support level of 1.3202. The pair is expected to find its first resistance at 1.3324, and a rise through could take it to the next resistance level of 1.3362.

Later in the day, all eyes would be on Bank of England's (BoE) interest rate decision, where the central bank is widely expected to raise interest rates for the first time since July 2007.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Canada’s Manufacturing Sector Activity Slowed In October

For the 24 hours to 23:00 GMT, the USD declined 0.18% against the CAD and closed at 1.2874.

Data showed that Canada's manufacturing PMI eased to a level of 54.3 in October as supply chains at firms were disrupted by Hurricane Harvey in the US and as new export orders slumped last month. In the previous month, the index had recorded a reading of 55.0.

Meanwhile, the Bank of Canada (BoC) Governor, Stephen Poloz, indicated in his testimony that while monetary policy decisions would have an effect on the nation's currency, crude oil prices would also have a huge long-term impact on the Canadian Dollar.

In the Asian session, at GMT0400, the pair is trading at 1.2833, with the USD trading 0.32% lower from yesterday's close.

The pair is expected to find support at 1.2807, and a fall through could take it to the next support level of 1.278. The pair is expected to find its first resistance at 1.2885, and a rise through could take it to the next resistance level of 1.2936.

Amid a lack of any major economic releases in Canada today, investors will focus on global macro events for further direction.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Switzerland’s Manufacturing PMI Surprisingly Rose In October

For the 24 hours to 23:00 GMT, the USD rose 0.55% against the CHF and closed at 1.0028.

On the data front, Switzerland's SVME PMI unexpectedly rose to 62.0 for October, compared to a level of 61.7 in the previous month. Market had expected the index to fall to 61.4.

In the Asian session, at GMT0400, the pair is trading at 0.9992, with the USD trading 0.36% lower from yesterday's close.

The pair is expected to find support at 0.9967, and a fall through could take it to the next support level of 0.9943. The pair is expected to find its first resistance at 1.0027, and a rise through could take it to the next resistance level of 1.0063.

Moving ahead, traders will await the release of Switzerland's real retail sales data for September, scheduled for today.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Japan’s Consumer Confidence Climbed In October

For the 24 hours to 23:00 GMT, the USD rose 0.45% against the JPY and closed at 114.15.

Overnight data revealed that Japan's monetary base rose 14.5% on an annual basis in October, from a gain of 15.6% in the prior month.

In the Asian session, at GMT0400, the pair is trading at 113.89, with the USD trading 0.23% lower from yesterday's close.

Early today, data showed that Japan's consumer confidence index unexpectedly rose to 44.5 in October, compared to a reading of 43.9 in the previous month. Market expectation was for the consumer confidence index to ease to a level of 43.6.

The pair is expected to find support at 113.65, and a fall through could take it to the next support level of 113.42. The pair is expected to find its first resistance at 114.2, and a rise through could take it to the next resistance level of 114.52.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

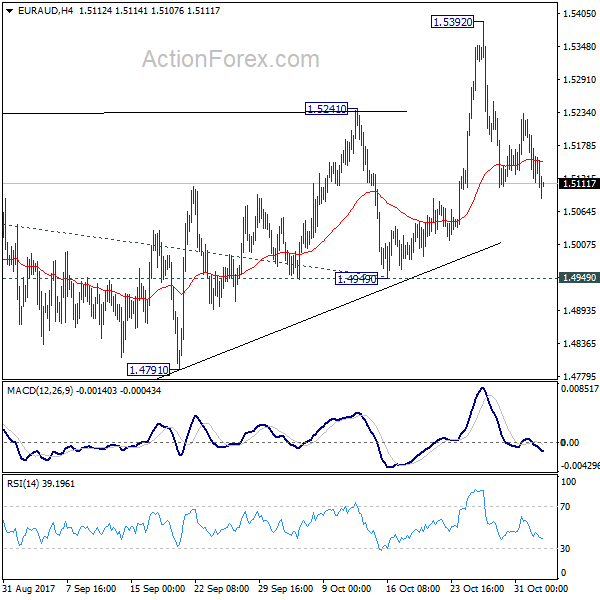

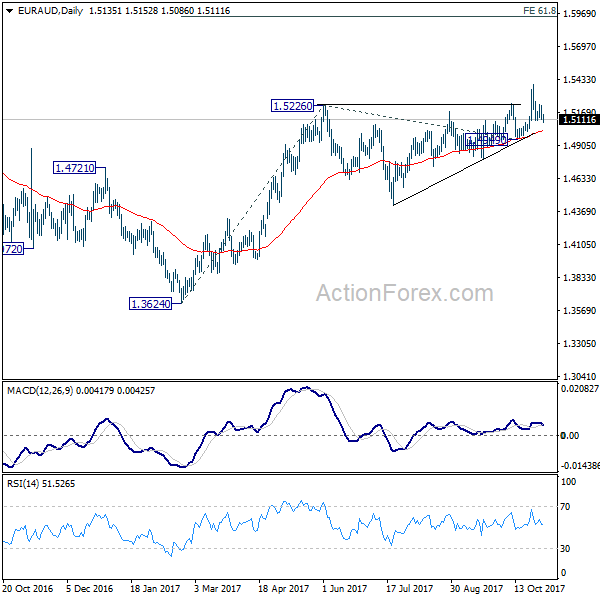

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5092; (P) 1.5158; (R1) 1.5200; More....

EUR/AUD's correction from 1.5392 is still in progress and outlook is unchanged. As long as 1.4949 support holds, outlook remains bullish. Medium term rally from 1.3624 is in favor to continue. On the upside, break of 1.5392 will resume medium term rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. However, decisive break of 1.4949 will carry larger bearish implication and turn bias to the downside.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. However, break of 1.4949 support will dampen our view and argue that rise from 1.3624 has completed. In that case, EUR/AUD would turn southward for retesting 1.3624 low.

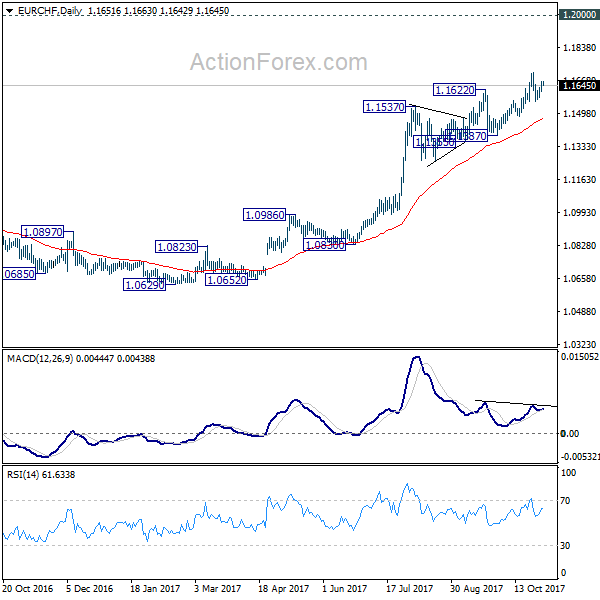

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1622; (P) 1.1643; (R1) 1.1676; More...

EUR/CHF recovered after dipping to 1.1559 but it still staying in range below 1.1709 temporary top. Intraday bias remains neutral first. Overall, near term outlook remains bullish as long as 1.1483 support holds. Break of 1.1709 will extend the medium term up trend towards 1.2 key level. However, break of 1.1483 will be an early sign of reversal. In that case, deeper decline should be seen back to 1.1355 support.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1067) and possibly below.