Sample Category Title

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

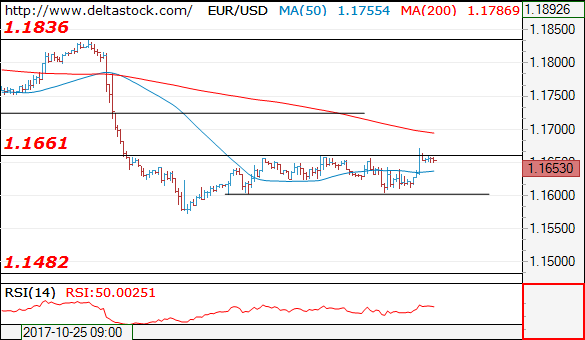

EUR/USD

Current level - 1.1653

Yesterday's attempts at 1.1600 support failed and the intraday bias is positive, for a brief rise to 1.1720 hurdle. The latter should set the beginning of a slide towards 1.1480 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1660 | 1.1840 | 1.1600 | 1.1480 |

| 1.1720 | 1.1940 | 1.1480 | 1.1300 |

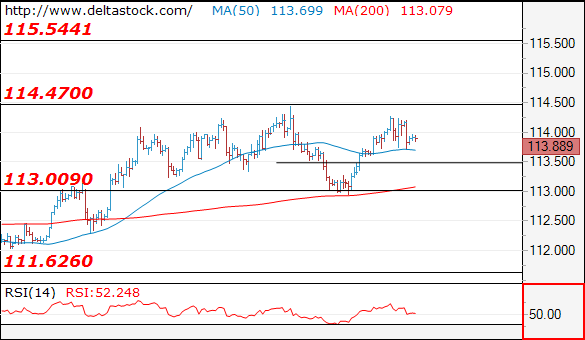

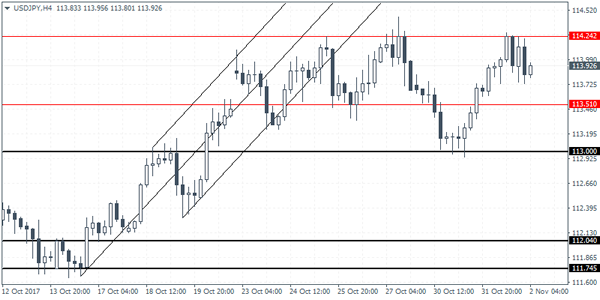

USD/JPY

Current level - 113.89

The consolidation pattern below 114.50 is still underway, with a risk of another slide towards 113.00 area, before breaking towards 115.50. Key resistance lies at 114.50.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 114.50 | 114.50 | 113.50 | 111.00 |

| 114.50 | 115.50 | 113.05 | 107.30 |

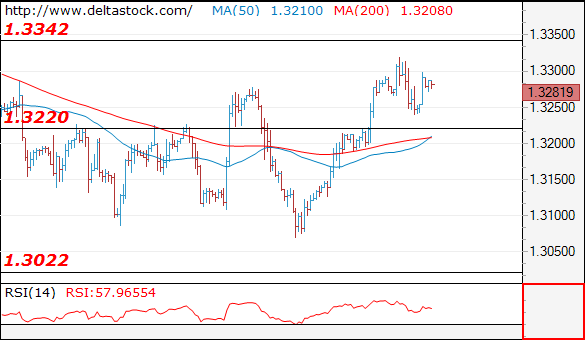

GBP/USD

Current level - 1.3281

Yesterday's rise peaked below 1.3340 resistance, but the pullback is not impulsive in nature, so while trading remains above 1.3220 support, there is a risk of another attempt at the mentioned hurdle. On the senior frames the zone around 1.3340 should provoke a renewal of the bearish bias, for 1.3020, en route to 1.2760.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3340 | 1.3340 | 1.3220 | 1.3020 |

| 1.3340 | 1.3440 | 1.3150 | 1.2760 |

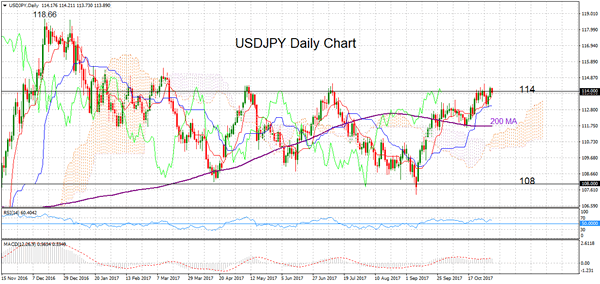

USDJPY Neutral After Recent Bullish Run Pauses At Top Of Broader 7-Month Range

USDJPY has been trading in a broad range during the past 7 months, roughly between 108.00 and 114.00. In the shorter time frame, the pair has turned neutral after a bullish run took it to the top of the longer-term range.

Strong resistance at the October 27 high of 114.45 needs to be broken in order to indicate the start of a new bullish phase and target the next major highs at 115.52. and then 118.60.

A drop below Tuesday's low of 112.95 would turn the focus to the 200-day moving average at 111.72. Breaking below this would bring further weakness and open the way to the bottom of the range at 108.00.

USDJPY is expected to remain neutral in the 112.95-114.45 range in the short-term but price signals are leaning towards bullish, suggesting that risk is tilted to the upside. Technical indicators such as RSI and MACD are in their respective bullish territories, although lacking momentum. The Ichimoku cloud analysis is also bullish. The market is above the cloud, while the Tenkan-sen and Kijun-sen lines are positively aligned.

Dollar Moderates After Reports Powell Will Be Next Fed Head, Kiwi, Aussie Keep Gains

There was some profit-taking on the US dollar following reports that President Trump has decided to nominate Fed Governor Jerome Powell for the post of new Fed Chair. The kiwi and the aussie were doing well following upbeat trade and housing data out of Australia, while all eyes later today will be on the Bank of England interest rate decision and the reaction of sterling.

Powell was seen as an on-balance dovish choice, but Trump's choice is understandable given that he might be hesitant to upset markets by introducing fresh uncertainty with an inexperienced appointee. Governor Powell has sided with current chair Janet Yellen throughout most his tenure on monetary policy and he is seen as a steady hand. Reappointing Yellen might have been a good option given her successful track record, but such a decision would have left Trump open to criticism that he was not ‘shaking things up' as he had promised to do during his campaign. Both Yellen and Powell are perceived as slightly on the dovish side of the scale, but not excessively, therefore for the Powell Fed, it looks to be pretty much business-as-usual after Yellen steps down in February 2018. Powell is also expected to be approved by the Senate without too many problems.

The policy statement by the Fed during late Wednesday trading did little to boost the dollar as it was in line with expectations. The Fed seemed to set the stage for a December rate hike as it cited “solid” growth of economic activity and continued “strength” in the labor market. There will be an update on the labor market in tomorrow's release of the October employment report. Euro/dollar rose to around 1.1660 before easing to 1.1635, while dollar/yen once again rose above the 114 mark to 114.08.

In today's best performing currencies, the aussie reached an 8-day high versus the greenback following positive Australian housing and trade data. Exports grew by 3% in September and the Trade Balance was at 1.74 billion Australian dollars instead of 1.2 billion expected by analysts. Building approvals for the same month grew by 1.5% month-on-month rather than contracting by 1% as economists were forecasting. The aussie reached as high as 0.7725 against the dollar.

The main event of Thursday will be the Bank of England rate-setting meeting, where the Bank is expected to raise rates to 0.5% from their current 0.25% level. Perhaps the outcome of today's meeting is much less important than the signals that the committee and Mark Carney himself will give in the press conference that will follow the release of the quarterly inflation report. The voting count as well as the minutes and Carney's guidance will determine whether this is seen as a ‘one-and-done' type of rate hike (more likely scenario according to the markets) or whether the Bank of England is considering more hikes in coming months. It is said that uncertainty around Brexit could prevent the Bank from hiking further, but doing nothing in the short-term in the face of inflation possibly topping 3% was also inappropriate. So Carney will probably have to perform a balancing act today. The pound fell below the 1.33 level to 1.3261 against the dollar.

Looking ahead, Eurozone final manufacturing PMIs for October and UK construction PMI will be the highlights of the European session. Weekly jobless claims out of the US as well as labor costs and productivity will also be monitored, while speeches by the Fed's Powell and Dudley could also prove interesting – especially with the appointment of Powell expected to be confirmed by Trump at some point today.

USDJPY Intraday Analysis

USDJPY (113.92): The USDJPY was seen closing on a bullish note for the second consecutive day. Price action was pushed back to the resistance level of 114.00 price level. The longer term consolidation remains in play, and we expect to see a potential correction in the near term. However, watch for a breakout above the 114.00 level which could indicate further gains in the currency pair. To the downside, price action is supported near the short-term price level of 112.80. On the 4-hour chart, we expect to see a potential inverse head and shoulders continuation pattern taking shape. Near-term declines could be limited to 113.51. A successful reversal at this level could indicate a move to the upside, above 114.25.

EURGBP Intraday Analysis

EURGBP (0.8777): The EURGBP fell to a 5-month low yesterday, but price action managed to recover by the end of the day. The decline below 0.8750 signals a retest of the familiar support level and indicates a short-term bounce to the upside. On the 4-hour chart, EURGBP will need to rise above 0.8778 in order for theprice to test the next resistance level at 0.8857 - 0.8867 level. We expect the currency pair to maintain this short-term range in the near term. Further gains can be expected only on a breakout to the upside above this resistance level. To the downside, in the event of a bearish close below the support level of 0.8750, the currency pair could resume the bearish trend.

EURUSD Intraday Analysis

EURUSD (1.1653): Price action in the EURUSD was rather muted following last Thursday's sharp declines. With the euro clearing the support level at 1.1700 - 1.1672, we now expect the declines to continues. The daily chart shows the validation of the head and shoulders pattern as we expect EURUSD to decline towards the minimum target level of 1.1440. The muted price action currently is also showing signs of a temporary consolidation following which we can expect to see strong declines being resumed. There is a short-term potential for the EURUSD to briefly retest the 1.1672 - 1.1674 level where resistance could be established. However, watch the bearish flag pattern that indicates potential downside.

GBP Turns To The BoE Rate Hike

The US dollar continued to trade firm against its peers amid a busy Wednesday. Data showed that the US ISM manufacturing PMI declined to 58.7 in October which was slightly below estimates. The ADP private payrolls firm showed that the US economy added 235k jobs in the private sector. The numbers for September were revised down to 110k.

The FOMC meeting yesterday was a non-event as the central bank maintained the short term interest rates steady. The Fed signaled that it would continue hike rates gradually.

Looking ahead investors turn to the UK as the Bank of England holds its monetary policy meeting. The central bank is expected to hike interest rates by 25 basis points although it is most likely to retain a dovish bias. The BoE Governor Carney is also scheduled to speak later after the release of the monetary policy statement.

Will Super Thursday Live Up To Its Name?

BoE Has Prepared Markets For a Rate Hike, Will it Deliver?

On Thursday, the Bank of England is widely expected to do something that a large group of people will never have experienced, raise interest rates.

For the first time in a decade and the first since the global financial crisis, policy makers will discuss the merits of a rate hike in a bid to prevent inflation moving too far above target. Or at least, that's what we're being told despite the acknowledgement that higher inflation is almost entirely down to the one-off currency depreciation that occurred since the Brexit referendum last year.

Inflation reached 3% in September, far above the central bank's 2% target and at the top of the range that the government deems acceptable before Governor Carney must write a letter to the Chancellor explaining why the central bank is failing to achieve its mandated target.

Interestingly, this is also around the level that the central bank expects inflation to peak at which begs the question why they've waited so long to raise interest rates. Also, why do they now deem it to be the right time to do so before we have a chance to find out how far it will fall again once the initial impact of the currency move falls out of the calculation?

If Inflation is Above Target, Why is a Rate Hike So Controversial?

As is to be expected in post-Brexit Britain, the decision on whether or not to raise interest rates is far from straightforward. This is clearly evident when listening to one of Carney's press conferences or appearances before the Treasury Select Committee, as well as in the rhetoric from his colleagues on the Monetary Policy Committee.

Not only does the inflation data and outlook not necessarily warrant a rate increase but the uncertain economic outlook muddies the water even further, which explains the divide on the committee.

It's quite clear that the economy has slowed since the vote last year, with the country falling from the top of the G7 growth table to the bottom in the first half of the year. Employment may have remained strong for now but with real wage growth having turned negative and spending slowed, it's clear that the economy is stalling which begs the question, is it really the correct time to raise interest rates?

The argument for the hawks on the MPC is that the economy hasn't slowed as much as was feared in the months after the referendum – partly due to the actions it took – and so a reversal of the rate cut in August 2016 makes sense.

While this hasn't been acknowledged by policy makers, there may also be a case that the BoE took a risk when cutting interest rates last year, taking base rate below the level that for the seven years previous was deemed to be the lower bound. Perhaps this is no longer seen as being a risk worth taking.

If this is the case then the BoE may refrain from committing to, or even hinting at, further rate hikes in the foreseeable future, which you would expect if this was in fact the beginning of a tightening cycle. Instead it may opt for the ECB approach of data dependent decision making. In other words, the less we know the better.

How Will Markets React to a Rate Hike?

Despite the divisions that we've seen within the MPC and the fact that the decision appears far from straightforward, investors are almost entirely convinced that the BoE will raise interest rates. In fact, according to Reuters, a rate hike is almost 90% priced in. That would suggest to me that a rate hike alone won't be enough to lift the pound or UK yields too much. A change of heart on the other hand could deal a big blow to both, not to mention the central banks credibility.

How the pound trades – and the FTSE for that matter given the inverse correlation that the two share - in the aftermath of the decision will likely depend on the minutes, economic projections and press conference that accompanies the decision.

Any indication that more rate hikes are planned for next year could trigger a sharp rally in the pound as I'm not convinced this is currently priced in, while anything else may weigh on the currency once the initial volatility – of which I expect a lot – has passed.

Super Thursday may for once live up to its name and I'm sure markets will be very sensitive to what policy makers have to say about the path of interest rates going forward, whatever the decision. Given the range of outcomes that we could see, UK markets could get extremely volatile and the upside and downside potential should not be underestimated.

A hawkish rate hike from the BoE could see GBPUSD blow through 1.33 and 1.36 being tested once again while no rate hike could see 1.30 severely tested, the success of which may depend on whether the increase is slightly delayed or postponed. In the case of the latter, I wouldn't be surprised to see 1.28 tested in the not-too distant future.

Dollar Falls Despite Hawkish Fed, BoE Next

Despite a relatively hawkish statement from the Federal Reserve on Wednesday, the dollar edged lower against its major peers early Thursday. The assessment of economic activity seemed to have given the green light for a December rate hike. Policy makers see economic activity rising at a solid rate, despite hurricane-related disruptions. No amendments were made on household spendingand business fixed investment, which continues to pick up. On the inflation front, FOMC is no longer worried about a temporary boost to prices from storm-disruptions, and continues to see market-based measures of inflation compensation remaining low.

Rate hike expectations for December climbed to 98.2%, according to CME’s FedWatchTool, indicating that a third rate hike this year is completely priced in, and investors require new catalysts to act upon. The White House is likely to endspeculation on who will serve as the next chair of the Federal Reserve later today. Many reports have confirmed that Jerome Powell will be Donald Trump’s nominee. While it is believed that Mr. Powell will resume a very gradual normalization of monetary policy, he is expected to be more flexible in terms of financial deregulation. Unless we see a surprise,expect little or no impact on Treasury Yields and the U.S. dollar. Investors are also keeping a close eye on the announcement of tax reforms. There have been many conflicting reports on when and how much the tax rate on U.S. corporates would be lowered; any delay on that front will likely put some pressure on equities and the dollar.

Investors will shift attention to Bank of England’s monetary policy decision later today. The BoE is in a tough situation, given that inflation is running above the 2% target and growth is likely to slow in the coming quarters. Expectations of a 25-basis point rate hike is standing at around 90%, which indicates that Sterling has been pricing in the first-rate hike since 2007, for couple of months. However, traders are likely to act upon the MPC’s voting split, the updated economic forecast (Quarterly Inflation Report), and forward guidance. For instance, Sterling’s reaction on a 9-0 vote in favor of a rate increase, will differ a lot from 5-4. If the BoE decides to keep policy unchanged, Sterling would come under pressure, unless the BoE sends a clear message for a rate hike in December. Trading the BoE will prove to be a tricky one, given the many possible scenarios;however, I think the central bank will hike rates today and reassure markets that further monetary policy tightening will remain limited for the foreseeable future.

Currencies: Dollar Fails To Extend Gains

Sunrise Market Commentary

- Rates: Core bonds little moved after Fed meeting.

The FOMC statement upgraded the economic situation to “solid” from “moderate” confirming its intention to raise rates in December. Today, Trump's announcement of the nomination of Mr. Powell as next Fed chair and the BoE rate hike will be the focus, but as these events are largely anticipation, the effect on core bonds should be modest ahead of the US payrolls. - Currencies: Dollar fails to extend gains

The dollar was better bid at the end of last week, but for now there are no follow-through gains. Today's eco data are no market movers for the dollar. A cautious risk-off sentiment and ‘political issues' might keep USD bulls on the sidelines ahead of tomorrow's US payrolls. EUR/GBP is testing key support as the BoE is largely expected to raise its policy rate today.

The Sunrise Headlines

- US equity indices ended narrowly mixed yesterday as strong opening gains gradually evaporated. Asian equities trade with modest losses overnight except for Japan that goes up about 0.5%.

- Jay Powell is expected to be the US president's nominee to serve as the next chair of the Fed, according to two White House officials. An official announcement is expected today.

- The BOE is set to increase rates for the first time in a decade. Mark Carney may signal even more tightening if the economy performs in line with new forecasts, but that's unlikely.

- The Fed reinforced expectations for a December rate hike. FOMC officials upgraded the economic activity to solid from moderate previously. It confirmed they expect inflation to eventually reach the 2% target.

- The House GOP tax bill expected today will impose a one-time tax of 12% on U.S. firms' offshore cash earnings. Tax writers also plan to phase out the 20% proposed corporate rate after a decade. Other measures include removing estate tax and restrictions on certain tax deductions.

- Australian dollar rallies the most in three weeks as trade and building data for September beat estimates. AUD/USD jumps again above the 0.77 handle.

- US and EMU eco data are unlikely to have much market impact, but the BoE meeting and Trump's Fed announcement will be highlights. Corporate earnings reports out today include Apple, Alibaba, Hugo Boss, Royal Dutch Shell, Credit Suisse and L'Oreal. Spain and France tap the bond market

Currencies: Dollar Fails To Extend Gains

USD fails to extend gains

On Wednesday, the dollar traded with a cautiously positive bias. The US eco data (ADP, ISM) were OK but close to expectations. The Fed left its policy unchanged. It kept a positive assessment on the economy, leaving the door open for a December rate hike. ‘Political issues' were a source of caution for USD bulls. Markets are pondering the impact of president Trump likely nomination of Mr. Powell as next Fed chairman. There is also a lot of uncertainty on the new tax bill. EUR/USD finished session at 1.1619 (from 1.1646). USD/JPY finished at 114.19 (from 113.64) but the key 114.45 area stays out of reach.

Overnight, Asian equities outside Japan mostly trade with modest losses. The US equity rally shows signs of fatigue. This weighs on Asian indices and on US yields. It also prevents the dollar to return to the recent highs against the euro and the yen. USD/JPY returned below the 114 handle while EUR/USD trades again in the mid 1.16 area. The Aussie dollar regained some ground after last week's setback supported by stronger than expected eco data. AUD/USD regained the 0.77 mark.

Politics rather than data to guide USD trading.

The EMU eco calendar contains only the final manufacturing PMI report and the German unemployment data, no market movers. In the US, the weekly initial jobless claims and the Q3 productivity figures are up for release. US president Trump is expected to nominate Jerome Powell as the next Fed Chairman. Markets also continue to look forward to additional details on the Tax reform plans. The proposition of tax cuts as such is a USD positive, but markets also want details on how these cuts will be funded. A lack of details on this issue might cap any further USD enthusiasm. Markets will also look forward to tomorrow's US payrolls

The dollar made a new up-leg at the end of last week. The move was partially a repositioning out of the euro after a soft ECB assessment. At the same time, the US data/news flow as was also USD supportive. The dollar maintained those gains this week, but there were no additional gains. Today, we keep a neutral to cautiously negative bias on the dollar. The data won't help and a cautious risk-off sentiment, recently often weighed more on US yields than on European ones. USD investors will look forward to tomorrow's US payrolls. LT we maintain a cautious EUR/USD sell-on-upticks bias. Of late, the dollar failed to gain against the euro despite widening interest rate differentials since early September. This trading dynamic was broken after the ECB decision last week Policy divergence between the ECB and the Fed is again on the radar. However, any additional rate support for the dollar will probably be modest near term, especially if Powell is nominated to succeed Yellen. So, further EUR/USD decline might develop gradually.

From a technical point of view, EUR/USD dropped below 1.1670/62 support, but there are no convincing follow-through gains yet. If the break is confirmed, it would signal that the recent EUR/USD uptrend is broken. EUR/USD 1.1423 (38% retracement of 2017 rise) is the next downside target on the charts. USD/JPY's momentum was positive in September. The pair regained 110.67/95 resistance, a positive. The 114.49 correction top is the next resistance. Sentiment improved last week, but the first test on Friday failed. We don't preposition for a sustained break higher.

EUR/USD broke below 1.1662 support, but breaks still needs to be confirmed

EUR/GBP

Sterling tests 0.8740/50 support ahead of BoE

Yesterday, sterling made some intraday swings against the euro, but at the end of the day the changes were limited. The UK eco data, including the UK manufacturing PMI, came out slightly stronger than expected. EUR/GBP touched a minor correction low after the report. However, a sustained break below 0.8743 support didn't occur. EUR/GBP finished the session at 0.8772; hardly changed from Tuesday. Cable finished the session at 1.3245 (from 1.3283).

Today, the UK construction PMI sis expected to rebound slightly from 48.1 to 48.5. However, the focus will be on the BoE policy decision and on the UK inflation report. The BoE is largely expected to raise rates by 25 basis points to 0.50%. Markets will keep a close eye at growth and inflation projections in the inflation report, looking for clues on additional rate hikes next year. Carney and Co will keep this option open. However, we doubt that there is room for a further rate hike anytime soon as long as the uncertainty on Brexit persists. In this context, we assume that there is a lot of good news discounted for sterling of late.

EUR/GBP staged a strong uptrend from April till late August with a top at 0.9307. Rising UK inflation and the BoE preparing markets for a rate hike caused a sterling rebound. This rebound did run into resistance. EUR/GBP tried to regain the 0.890.90 area, but there were no follow-through gains. The drop below the 0.8855 area (neckline minor double top) on Friday opened the way for a return to 0.8743 or even 0.8652 supports. The jury is still out, but we maintain the working hypotheses that this area will be tough to break in a sustainable way

EUR/GBP: testing first important support at 0.8743 ahead of the BoE decision