Sample Category Title

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.73; (P) 151.32; (R1) 151.84; More

GBP/JPY drops sharply after hitting 151.92 but downside is contained above 148.88 minor support so far. Outlook is unchanged. While choppy recovery from 149.62 could still extend, firm break of 152.82 is needed to confirm medium term rally resumption. Otherwise, consolidative trading from 152.82 should extend with another falling leg. Break of 148.88 minor support will turn bias to the downside through 146.92 to 61.8% retracement of 139.29 to 152.82 at 144.45.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

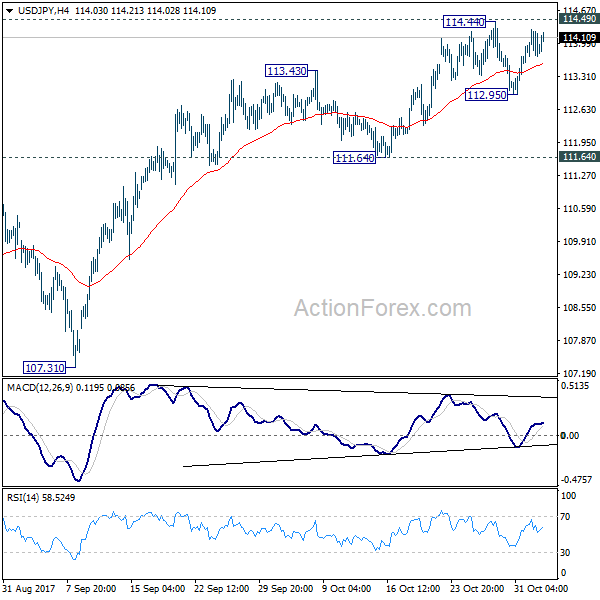

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.75; (P) 114.01; (R1) 114.43; More...

Intraday bias in USD/JPY remains neutral as consolidation from 114.44 is still in progress. Another fall cannot be ruled out. But after all, near term outlook will remain cautiously bullish as long as 111.64 support holds. Decisive break of 114.49 key resistance will confirm that correction pattern from 118.65 has completed at 107.31 already. And USD/JPY should then target a test on 118.65. However, sustained break of 111.64 will argue that rebound from 107.31 has completed and bring retest of this low.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9986; (P) 1.0011; (R1) 1.0059; More....

Intraday bias in USD/CHF remains neutral as the consolidation from 1.0037 is still in progress. Another fall could be seen. But still, downside should be contained above 0.9835 resistance turned support and bring rally resumption. Since 61.8% retracement of 1.0342 to 0.9420 at 0.9990 is already met, break of 1.0037 will turn bias to the upside for 1.0342 key resistance next.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

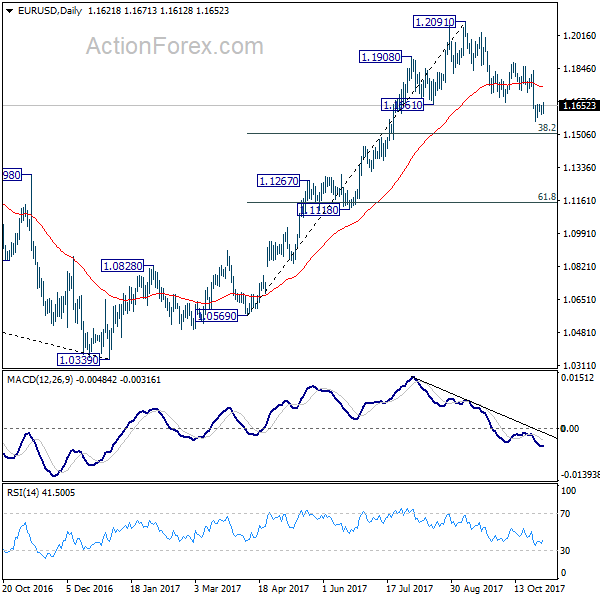

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1596; (P) 1.1626 (R1) 1.1648; More...

No change in EUR/USD's outlook as consolidation pattern from 1.1574 temporary low continues. Intraday bias stays neutral at this point. As noted before, break of 1.1879 resistance is needed to confirm completion of the decline from 1.2091. Otherwise, near term outlook will stay bearish. Below 1.1574 will target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Sterling Tumbles on Dovish BoE Rate Hike, Focus Turns to Fed Chair Nomination and Tax Plan

Sterling dives sharply as respond to BoE's dovish rate hike that suggests it's a one-off. Indeed, selling has already started around 30 minutes ahead of the announcement. At the time of writing, the Pound is still holding above key near term support level against Dollar, Euro and Yen. That is, GBP/USD is holding above 1.3026/68 support zone. GBP/JPY is staying above 148.88 support. EUR/GBP is staying well below 0.9032 resistance. More is needed to confirm underlying weakness in the Pound. For now, while traders will have one eye on Sterling, focus will also turn to US President Donald Trump's expected nomination of Jerome Powell as Fed chair, as well as Republican's release of the tax plan.

BoE hikes but statement suggests it's a one-off

BoE finally delivered the highlight anticipated rate hike as expected. The Bank Rate is raised by 25bps to 0.50%, first hike in a decade. The decision is made by 7-2 vote, with Jon Cunliffe and Dave Ramsden dissented. The asset purchase target was held unchanged at GBP 435b by unanimous vote. In the prior statement, MPC noted that "monetary policy could need to be tightened by a somewhat greater extent over the forecast period than current market expectations." Such language is taken out in the current statement. Instead, "MPC now judges it appropriate to tighten modestly the stance of monetary policy in order to return inflation sustainably to the target." This is taken by the markets that today's rate hike is a one-off.

Meanwhile, BoE also reiterated that there are "considerable risks" to the outlook including Brexit. And it pledged to "monitor closely the incoming evidence on these and other developments, including the impact of today's increase in Bank Rate, and stands ready to respond to changes in the economic outlook as they unfold to ensure a sustainable return of inflation to the 2% target."

Regarding the updated economic projections, growth and inflation forecasts are largely unchanged. Inflation is projected to hit 2.2% in three years, slightly above BoE's 2% target. And the projections are based on market projections on the Bank Rate, which is expected to hit 1% over that period.

More in BOE Increased Policy Rate for First Time in More than A Decade

Japan FM and PM hailed BoJ Kuroda

Japan Finance Minister Taro Aso hailed that BoJ Governor Haruhiko Kuroda has "overhauled the Bank of Japan's monetary policy and eased policy, as a result the yen has fallen from around 80 yen to some 113 yen, which has improved export conditions for Japanese firms." Also, Aso said that "coordination between fiscal and monetary policies has worked well."

Yesterday, Prime Minister Shinzo Abe expressed his recognition on Kuroda's achievements. He said that "we have created a situation in a short period of time that Japan is no longer in deflation as a result of strengthening policy coordination between the government and the BOJ." And, "the government and the BOJ have achieved a major result on employment, which is the most important responsibility of politics."

These comments raised the chance that Kuroda will be given another term as the current one expires next April.

On the data front

US initial jobless claims dropped -5k to 229k in the week ended October 28. That's below market expectation of 235k. The four week moving averaged dropped to 232.5k, hitting the lowest level since 1973. Continuing claims dropped -15k to 1.88m, lowest since 1973. Non-farm productivity surged 3.0% in Q3, above expectation of 2.5%. Unit labor costs rose 0.5%, above expectation of 0.4%.

UK PMI construction rose to 50.8 in October, up from 48.1 and beat expectation of 48.5. Markit noted that "greater house building was the sole bright spot in an otherwise difficult month for the construction sector. Sustained declines in civil engineering and commercial activity meant that large areas of the building industry have become stuck in a rut."

German unemployment dropped -11k in October, larger than expectation of -10k. Unemployment rate was unchanged at 5.6%. Eurozone PMI manufacturing was finalized at 58.5, revised down -0.1. Italy PMI manufacturing rose to 57.8 in October, up from 56.3, above expectation of 56.5. Swiss retail sales dropped -0.4% yoy in September, below expectation of 0.3% yoy. Swiss SECO consumer confidence improved to -2 in October, but missed expectation of 0.

Elsewhere, Australia trade surplus widened to AUD 1.75b in September, above expectation of 1.2b. Building approvals rose 1.5% in October versus expectation of -1.0% fall. Japan monetary base rose 14.5% yoy in October. Japan consumer confidence rose to 44.5 in October, above expectation of 43.6.

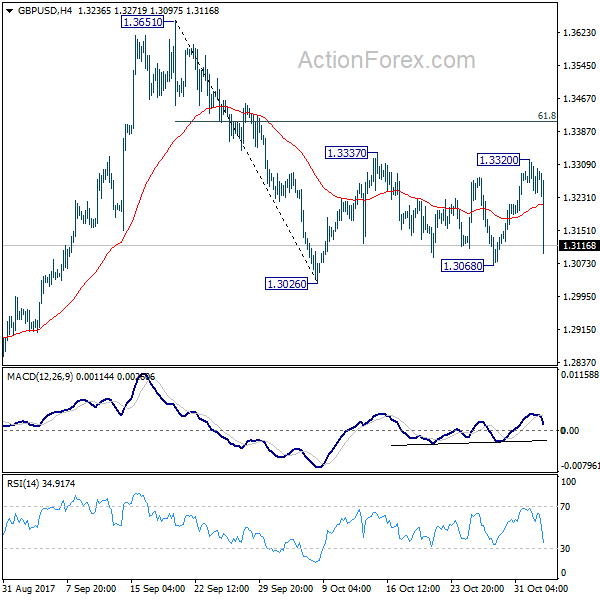

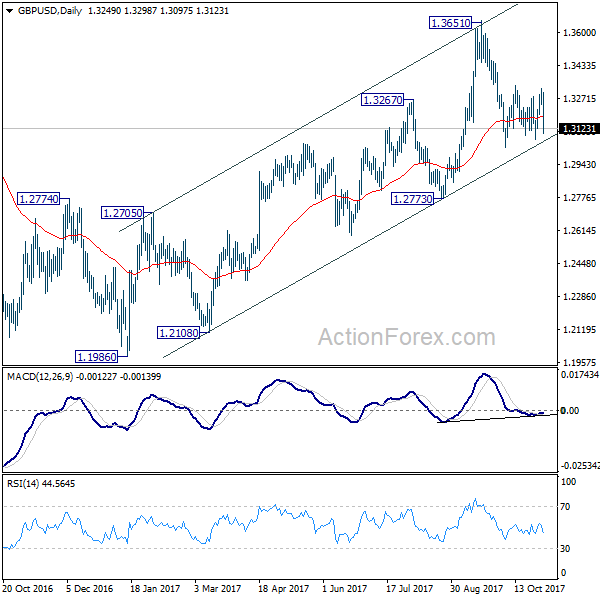

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3216; (P) 1.3268; (R1) 1.3297; More....

GBP/USD failed to break out 1.3337 resistance, reversed after hitting 1.3320 and drops sharply from there. At this point, it's staying in consolidation pattern from 1.3026 short term bottom. Intraday bias remains neutral first. Outlook is unchanged that even in case of another rise, upside should be limited by 61.8% retracement of 1.3651 to 1.3026 at 1.3412 to bring fall resumption finally. On the downside, firm break of 1.3026 support will resume the decline from 1.3651 and target 1.2773 key support level. This will also revive the case of medium term reversal. However, sustained break of 1.3412 will turn focus back to 1.3651 high.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll stay neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Oct | 14.50% | 15.70% | 15.60% | |

| 00:30 | AUD | Trade Balance Sep | 1.75B | 1.20B | 0.99B | 0.87B |

| 00:30 | AUD | Building Approvals M/M Sep | 1.50% | -1.00% | 0.40% | |

| 05:00 | JPY | Consumer Confidence Oct | 44.5 | 43.6 | 43.9 | |

| 06:45 | CHF | SECO Consumer Confidence Oct | -2 | 0 | -3 | |

| 08:15 | CHF | Retail Sales Real Y/Y Sep | -0.40% | 0.30% | -0.20% | -1.00% |

| 08:45 | EUR | Italy Manufacturing PMI Oct | 57.8 | 56.5 | 56.3 | |

| 08:50 | EUR | France Manufacturing PMI Oct F | 56.1 | 56.7 | 56.7 | |

| 08:55 | EUR | German Unemployment Change Oct | -11K | -10K | -23K | |

| 08:55 | EUR | German Unemployment Claims Rate Oct | 5.60% | 5.60% | 5.60% | |

| 08:55 | EUR | Germany Manufacturing PMI Oct F | 60.6 | 60.5 | 60.5 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Oct F | 58.5 | 58.6 | 58.6 | |

| 09:30 | GBP | Construction PMI Oct | 50.8 | 48.5 | 48.1 | |

| 11:30 | USD | Challenger Job Cuts Y/Y Oct | -3.00% | -27.00% | ||

| 12:00 | GBP | BoE Bank Rate | 0.50% | 0.50% | 0.25% | |

| 12:00 | GBP | BoE Asset Purchase Target | 435B | 435B | 435B | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 7--0--2 | 9--0--0 | 2--0--7 | |

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--9 | 0--0--9 | 0--0--9 | |

| 12:00 | GBP | Bank of England Inflation Report | ||||

| 12:30 | USD | Initial Jobless Claims (OCT 28) | 229K | 235K | 233K | 234K |

| 12:30 | USD | Nonfarm Productivity Q3 P | 3.00% | 2.50% | 1.50% | |

| 12:30 | USD | Unit Labor Costs Q3 P | 0.50% | 0.40% | 0.20% | 0.30% |

| 14:30 | USD | Natural Gas Storage | 64B |

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3216; (P) 1.3268; (R1) 1.3297; More....

GBP/USD failed to break out 1.3337 resistance, reversed after hitting 1.3320 and drops sharply from there. At this point, it's staying in consolidation pattern from 1.3026 short term bottom. Intraday bias remains neutral first. Outlook is unchanged that even in case of another rise, upside should be limited by 61.8% retracement of 1.3651 to 1.3026 at 1.3412 to bring fall resumption finally. On the downside, firm break of 1.3026 support will resume the decline from 1.3651 and target 1.2773 key support level. This will also revive the case of medium term reversal. However, sustained break of 1.3412 will turn focus back to 1.3651 high.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll stay neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

Pound Plummets 1% on BoE Decision

- BOE Nov Minutes: MPC Voted 7-2 to Raise Bank Rate to 0.5%

- BOE Nov Minutes: 2 Voted to Keep Rate Unchanged

- BOE Nov Minutes: 7 Voted to Increase Rate

- BOE Deputy Governors Ramsden and Cunliffe Voted To Leave Rate At 0.25%

- BOE Rate Rise Is First Since Global Financial crisis

- BOE Cites Lowered Economic "Speed Limit" As Reason For Rate Rise

- BOE Sees Potential Growth Rate At 1.5%, Down From 1.75% In Aug

- BOE Signals Two Further Rate Rises Likely By End Of 2020

- BOE Sees Inflation Falling Close To Its 2% Target By 2020

- BOE Forecasts Based On Assumption Bank Rate Rises To 1% By End 2020

- BOE Cuts 2018 Growth Forecast To 1.7% From 1.8% In August

- BOE Continues To Forecast 2019 Growth At 1.7%, Sees Same In 2020

- BOE Dissenters Saw Little Sign Of Pickup In Wages, Domestic Cost Pressures

- BOE: Brexit Process Having "Noticeable Impact" On U.K. Economy

- BOE: Response Of Households, Businesses To Brexit A "Considerable Risk" To Outlook

Sterling has fallen sharply, quickly reversing initial gains after the BoE raised interest rates by +0.25 bps to +0.5%, as expected, but said future rate rises would be "at a gradual pace and to a limited extent."

The BoE also warned on Brexit uncertainty, saying it was "having a noticeable impact on the economic outlook."

GBP/USD has fallen as much as -1%, last down at £1.3124, compared with £1.3269 before the decision. EUR/GBP last up +1.23% at €0.8885, compared with around €0.8811 beforehand.

Canadian Dollar Steady, US and Canadian Job Numbers Next

The Canadian dollar is showing little movement in the Thursday session. Currently, USD/CAD is trading at 1.2849, down 0.13% on the day. In economic news, there are no Canadian events on the schedule. The US will release unemployment claims, which is expected to tick upwards to 235 thousand. Traders should be prepared for some movement from the pair on Friday, as the US and Canada release key employment numbers. As well, Canada releases Trade Balance and the US publishes ISM Non-Manufacturing PMI.

BoC Governor Stephen Poloz testified before a parliamentary committee this week, and his remarks did not exude confidence in the Canadian economy. Poloz said that the country is at a "crucial" spot in the economic cycle, noting concern over soft inflation and wage growth, and high household debt. Poloz said that the BoC will be cautious before raising interest rates. The markets are not expecting any moves before 2018, with the likelihood of a rate hike in December at just 21 percent. Canadian GDP declined in August, disappointing the markets. The decline of 0.1% was the first drop since October 2016. The soft reading extended the Canadian dollar's misery, pushing USD/CAD above 1.29 and coming close to a 10-week low. The currency has endured a miserable October, slipping 3.5 percent.

As expected, the were no dramatic announcements from the Federal Reserve at the end of their policy meeting. The Fed indicated that a rate increase is very likely at the December meeting, and was careful not to change any of the wording in its statement regarding future rate hikes. The rate statement noted that hurricanes had caused a decline in payrolls in September, but the Fed did not expect the hurricanes to "materially alter the course of the national economy over the medium term." The markets appear in line with this sentiment, as the forecast for Friday's nonfarm payrolls is a robust 311 thousand, after a dismal decline of 33 thousand in September.

The markets have priced in a December rate hike in the US at 96 percent, but what can we expect in 2018? This will depend to a large degree on the new chair of the Fed, who will take over from Janet Yellen in February. Janet Yellen will wind up her 3-year term in February, and she is not expected to be reappointed by President Trump. The front runner is economist Jerome Powell, who is expected to maintain the Fed's current policy of small, incremental rates. Trump is expected to make his choice on Thursday, ahead of his trip to Asia.

(BOE) Bank Rate Increased to 0.50%

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 1 November 2017, the MPC voted by a majority of 7-2 to increase Bank Rate by 0.25 percentage points, to 0.5%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion.

The MPC's outlook for inflation and activity in the November Inflation Report is broadly similar to its projections in August. In the MPC's central forecast, conditioned on the gently rising path of Bank Rate implied by current market yields, GDP grows modestly over the next few years at a pace just above its reduced rate of potential. Consumption growth remains sluggish in the near term before rising, in line with household incomes. Net trade is bolstered by the strong global expansion and the past depreciation of sterling. Business investment is being affected by uncertainties around Brexit, but it continues to grow at a moderate pace, supported by strong global demand, high rates of profitability, the low cost of capital and limited spare capacity.

CPI inflation rose to 3.0% in September. The MPC still expects inflation to peak above 3.0% in October, as the past depreciation of sterling and recent increases in energy prices continue to pass through to consumer prices. The effects of rising import prices on inflation diminish over the next few years, and domestic inflationary pressures gradually pick up as spare capacity is absorbed and wage growth recovers. On balance, inflation is expected to fall back over the next year and, conditioned on the gently rising path of Bank Rate implied by current market yields, to approach the 2% target by the end of the forecast period.

As in previous Reports, the MPC's projections are conditioned on the average of a range of possible outcomes for the United Kingdom's eventual trading relationship with the European Union. The projections also assume that, in the interim, households and companies base their decisions on the expectation of a smooth adjustment to that new trading relationship.

The decision to leave the European Union is having a noticeable impact on the economic outlook. The overshoot of inflation throughout the forecast predominantly reflects the effects on import prices of the referendum-related fall in sterling. Uncertainties associated with Brexit are weighing on domestic activity, which has slowed even as global growth has risen significantly. And Brexit-related constraints on investment and labour supply appear to be reinforcing the marked slowdown that has been increasingly evident in recent years in the rate at which the economy can grow without generating inflationary pressures.

Monetary policy cannot prevent either the necessary real adjustment as the United Kingdom moves towards its new international trading arrangements or the weaker real income growth that is likely to accompany that adjustment over the next few years. It can, however, support the economy during the adjustment process. The MPC's remit specifies that, in such exceptional circumstances, the Committee must balance any trade-off between the speed at which it intends to return inflation sustainably to the target and the support that monetary policy provides to jobs and activity.

The steady erosion of slack has reduced the degree to which it is appropriate for the MPC to accommodate an extended period of inflation above the target. Unemployment has fallen to a 42-year low and the MPC judges that the level of remaining slack is limited. The global economy is growing strongly, domestic financial conditions are highly accommodative and consumer confidence has remained resilient. In line with the framework set out at the time of the referendum, the MPC now judges it appropriate to tighten modestly the stance of monetary policy in order to return inflation sustainably to the target. Accordingly, the Committee voted by 7-2 to raise Bank Rate by 0.25 percentage points, to 0.5%. Monetary policy continues to provide significant support to jobs and activity in the current exceptional circumstances. All members agree that any future increases in Bank Rate would be expected to be at a gradual pace and to a limited extent.

There remain considerable risks to the outlook, which include the response of households, businesses and financial markets to developments related to the process of EU withdrawal. The MPC will respond to developments as they occur insofar as they affect the behaviour of households and businesses, and the outlook for inflation. The Committee will monitor closely the incoming evidence on these and other developments, including the impact of today's increase in Bank Rate, and stands ready to respond to changes in the economic outlook as they unfold to ensure a sustainable return of inflation to the 2% target.

USD Rally Loses Steam Ahead Of Fed Chair Decision

BoE rate Decision

It widely expected (Rates markets are pricing in a 90% probability of a hike) the Bank of England (BoE) Monetary Policy Committee will hike policy rates 25bp after 10 years. We are expecting MPC 7-2 vote split with committee members Cunliffe and Ramsden dissenting for a no action. David Ramsden indicated that he was not with the majority while Jon Cunliffe expressed concern over the timing of rate hikes (Silvana Tenreyro is data dependent and could go either way). The view is already priced into the GBP so the key issue will be the accompanying communications.

We suspect that bank will reduce its current hawkish tone by reinforcing the strategy of “one-and-done.” Our view for a softer tone is based on expectations for wage inflations decelerate which the Inflation report should provide hint towards. In addition the bank has downgraded growth forecast for 2017 to 1.7% from 1.9% as consumer spending (and slower wage growth). We anticipate that Brexit related uncertainty will damage sentiment and inflation outlook pushing the next rate hike at least 6 months away.

No surprise from the Fed ahead of the Chair nomination

That was clearly not a surprise. Fed hold rates unchanged and has hinted for a December rate hike. The key rate stays at 1% to 1.25% of the FOMC. The likelihood of a rate hike for December has now been assessed by markets above 92%. The monetary policy will then remain then loose for some more time and stocks markets have already hit new highs yesterday.

Patience is definitely a key word for the Fed even though the unemployment data as well as the growth are very decent. Last quarter growth was 3% and unemployment rate is at 4.2%. Those good figures should have pushed the Fed to raise rates. Inflation is also on the rise with crude oil prices rising due to the recent hurricanes.

The fact that the Fed has a $4.5 trillion balance sheet will make it tough for the Fed to tighten monetary policy as it could trigger massive sell-off in the bond markets. Fed monetary policy is less and less about economic fundamentals but rather on the massive debt management.