Sample Category Title

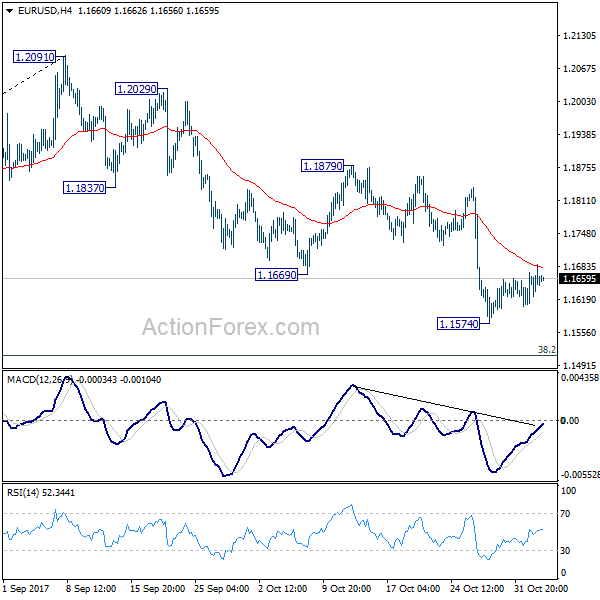

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1618; (P) 1.1652 (R1) 1.1693; More...

Intraday bias in EUR/USD stays neutral as consolidation from 1.1574 temporary low is still in progress. As noted before, break of 1.1879 resistance is needed to confirm completion of the decline from 1.2091. Otherwise, near term outlook will stay bearish. Below 1.1574 will target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

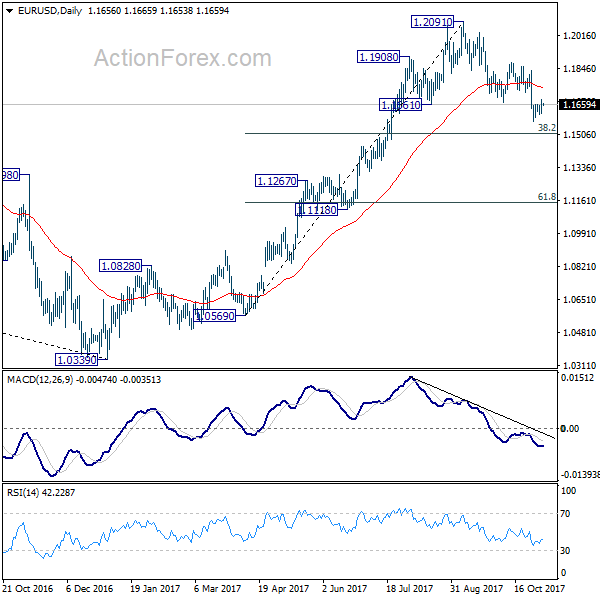

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

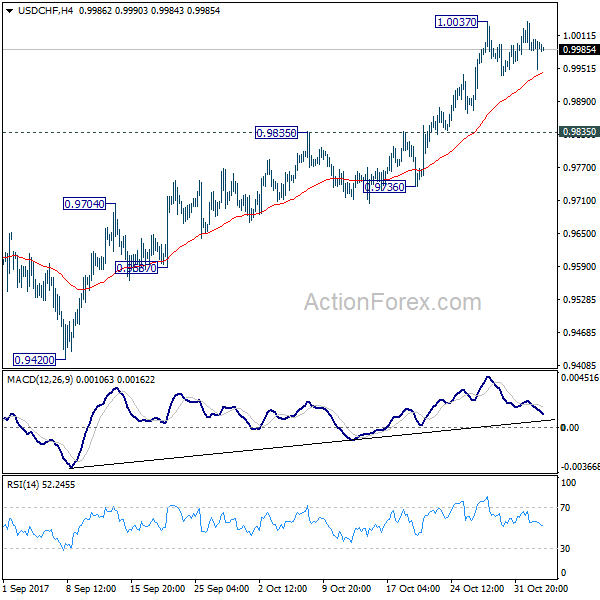

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9950; (P) 0.9991; (R1) 1.0035; More....

USD/CHF is staying in consolidation below 1.0037 temporary top and intraday bias remains neutral. On the upside break of 1.0037 will resume whole rally from 0.9420. And with sustained trading above 61.8% retracement of 1.0342 to 0.9420 at 0.9990, USD/CHF should then target a test on 1.0342 key resistance. In case of another fall, downside should be contained above 0.9835 resistance turned support and bring rally resumption.

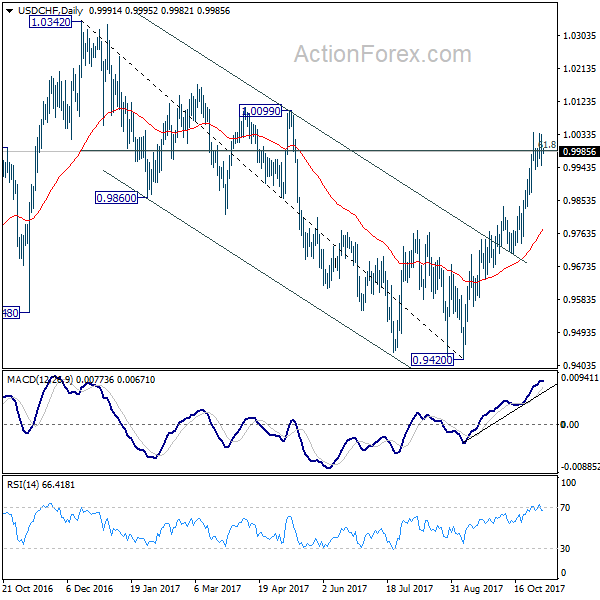

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

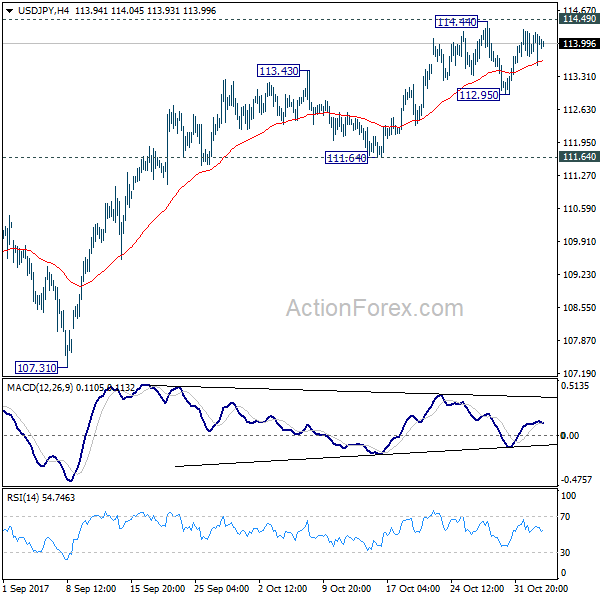

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.67; (P) 113.94; (R1) 114.35; More...

Intraday bias in USD/JPY remains neutral as it's still bounded in consolidation from 114.44. Decisive break of 114.49 will confirm that correction pattern from 118.65 has completed at 107.31 already. And USD/JPY should then target a test on 118.65. In case of another fall, strong support should be seen from 111.64 support to maintain bullishness and bring rebound.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

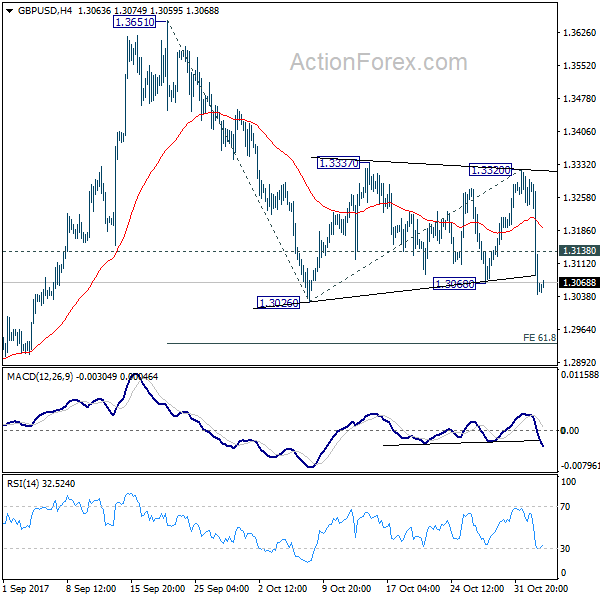

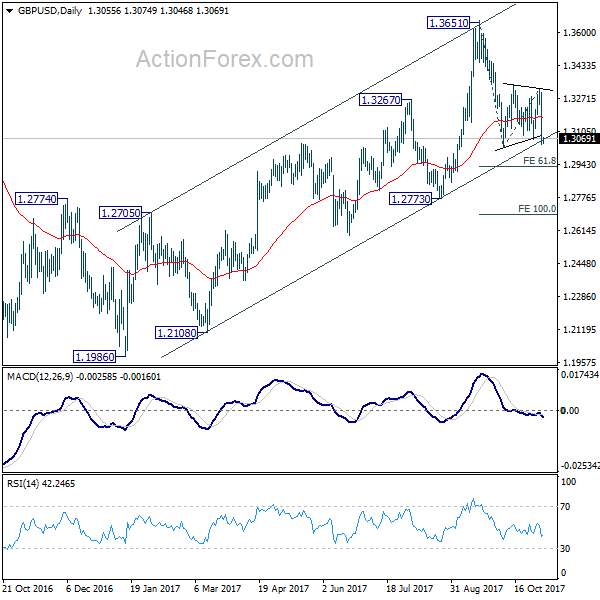

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2966; (P) 1.3133; (R1) 1.3224; More....

GBP/USD's break of 1.3068 minor support argues that the fall from 1.3651 is ready to resume. Focus is now on 1.3026 support. Firm break there will confirm and target 61.8% projection of 1.3651 to 1.3026 from 1.3320 at 1.2934 first. Break will bring deeper decline to 1.2773 key support level. On the upside, above 1.3138 minor resistance will extend the consolidation from 1.3026 with another rise.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

Powell Confirmed as Trump’s Nomination for Fed Chair, Tax Bill Released, Non Farm Payrolls Next

Fed Governor Jerome Powell was finally confirmed as US President Donald Trump's nomination as the one to succeed Janet Yellen as Fed Chair next year. House republicans also released the tax bill finally. Stock markets responded well to the news with DOW closing up 81.25 pts, or 0.35% at new record high. S&P 500 also reversed earlier loss and closed up 0.02% at 2579.85. But judging from the reactions in bonds, Powell is taken as a dovish Fed chair. 10 year yield lost 0.029 to close at 2.347, notably lower comparing to last week's close at 2.428. Powell is seen as a safe choice that would largely follow Yellen's path of gradual tightening. Focus will now turn to non-farm payrolls report.

House released Tax Cuts and Jobs Act

The House of Republicans eventually released the tax bill, the Tax Cuts and Jobs Act. The key reforms include: trimming the number of income tax brackets to 4 from 7; cutting the top corporate tax rate from 35% to 20%, and the pass-through rate for certain business partnerships is reduced to 25%; introducing a one-time repatriation tax of 12%; limiting the mortgage deductions and a 10% tax on profits for overseas subsidiaries of US corporations, etc.

Most of the bill are scheduled to take effect on January 1. Or, if the passage in Congress drags into next year, the lawmakers are expected to make it retroactive. The House Ways & Means Committee will begin a multi-day "markup" of the bill on November 6. House Speaker Paul Ryan intends to pass the legislation through House by thanksgiving. In the mean time, the Senate Finance Committee will launch a panel process. And the two would hope to resolve all the differences and pass a final bill by year end.

High expectations on Non-Farm Payrolls

Expectations on today's non-farm payroll report is high. Markets expect 310k growth in the US employment market in October, a strong rebound from hurricanes dragged -33k contraction back in September. Unemployment rate is expected to be unchanged at 4.2% in October. Average hourly earnings are expected to grow 0.2% mom. The figures could be heavily skewed as the aftermath of hurricanes. But judging from other employment related data, the job market in US remained pretty healthy.

ADP private payroll showed 235k growth in October, up from September's 110k. Four week moving average of initial jobless claims dropped notably from 267k to 233k during the month. Employment component of ISM manufacturing dropped from 60.3 to 59.8 but stayed high. Conference Board consumer confidence hit 17 year high at 125.9. These are solid readings that point to a strong labor market.

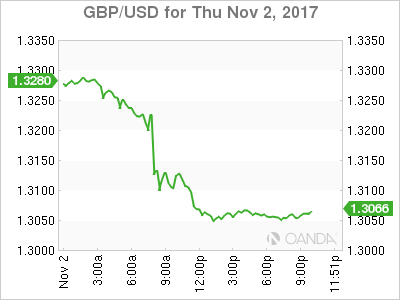

Sterling turning technically bearish

Sterling recovers mildly today but remains the weakest major one after yesterday's post BoE steep selloff. Technical development in the Pound has turned "slightly" dovish but key support levels are still intact. With break of 1.3068 support, GBP/USD is heading to 1.3026 level. Decisive break there will resume whole decline from 1.3651 and target key support level at 1.2773. And such development will also raise the chance of medium term bearish reversal. EUR/GBP is still far off 0.9032 resistance and thus, technically maintaining bearish outlook in the cross. GBP/JPY breached 148.88 support and is now in favor to break through 146.92 to resume the decline from 152.82. But such price actions in GBP/JPY from 152.82 are viewed as a correction pattern only.

More on BoE:

- BOE Increased Policy Rate for First Time in More than A Decade

- BoE Keeps its Flexibility on Further Rate Hikes Next Year

- Bank of England Raises Interest Rates for the First Time in Over a Decade

- "Dovish Hike" Excites Sterling Bears

- "One and Done" Rate Hike Triggers GBP Selling

Elsewhere

Australia retail sales rose 0.0% mom in September, below expectation of 0.4% mom. China Caixin PMI services rose to 51.2 in October. UK PMI services will be a key focus in European session and could trigger deeper selloff in Sterling. US will release trade balance, non-farm payrolls, ISM services and factory orders. Canada will also release trade balance and employment data later today.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2966; (P) 1.3133; (R1) 1.3224; More....

GBP/USD's break of 1.3068 minor support argues that the fall from 1.3651 is ready to resume. Focus is now on 1.3026 support. Firm break there will confirm and target 61.8% projection of 1.3651 to 1.3026 from 1.3320 at 1.2934 first. Break will bring deeper decline to 1.2773 key support level. On the upside, above 1.3138 minor resistance will extend the consolidation from 1.3026 with another rise.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | Retail Sales M/M Sep | 0.00% | 0.40% | -0.60% | |

| 1:45 | CNY | Caixin PMI Services Oct | 51.2 | 50.8 | 50.6 | |

| 9:30 | GBP | Services PMI Oct | 53.3 | 53.6 | ||

| 12:30 | CAD | International Merchandise Trade (CAD) Sep | -2.95B | -3.41B | ||

| 12:30 | CAD | Net Change in Employment Oct | 15.5K | 10.0K | ||

| 12:30 | CAD | Unemployment Rate Oct | 6.20% | 6.20% | ||

| 12:30 | USD | Trade Balance Sep | -43.5B | -42.4B | ||

| 12:30 | USD | Change in Non-farm Payrolls Oct | 310K | -33K | ||

| 12:30 | USD | Unemployment Rate Oct | 4.20% | 4.20% | ||

| 12:30 | USD | Average Hourly Earnings M/M Oct | 0.20% | 0.50% | ||

| 14:00 | USD | ISM Non-Manufacturing/Services Composite Oct | 58.5 | 59.8 | ||

| 14:00 | USD | Factory Orders Sep | 1.20% | 1.20% |

Market Morning Briefing: There’s Been A Sharp Fall In The Pound

STOCKS

Dow (23516.26, +0.35%) continues to move up and the 3-day line charts show a possibility of a rise towards 24000 maybe in this month. Near to medium term looks strongly bullish.

Dax (13440.93, -0.18%) is testing resistance on the 3-day candles but at the same time has more room on the upside towards 13600-13700 on the line charts. Either a rejection from current levels is possible with resumption of the upward rally later on or the index may continue to rise in the next week. While other global indices are rising the Dax would prefer to move up too with the other major indices.

Nikkei (22539.12, +0.53%) is all set to test 22666 on Monday but would it rise higher to make fresh highs would be a big cue for Dollar Yen in the medium term. A break above 22666 would be a trigger to more upside in the coming sessions. Need to be careful above current levels.

Shanghai (3372.59, +0.32%) has support at 3360 and could bounce back from there towards 3400 in the next week. Near term looks bullish.

Nifty (10423.80, -0.16%) dipped slightly yesterday but while it trades above 10400, a rise towards 10500-10600 is a possibility.

COMMODITIES

Gold (1276.80) is almost stable at current levels. While above 1265-1270, view remains bullish.

The resistance seen on the 3-day line chartsseem to be holding well for now and could push Brent (60.78) towards 58-55 levels in the near to medium term. Only on a break above 62, we would focus on higher levels of 65. Preferred view is a downward correction towards 58 and lower. Some sideways movement is possible just now.

Brent-WTI (6.03) is coming off sharply from levels near 6.75 and could head to lower levels of 5.5 in the near term. WTI (54.77) could face some rejection near 55.00-55.08.

Copper (3.1520) is likely to trade in the 3.05-3.25 region for now.

FOREX

Most currencies are trading at crucial juncures just now with perhaps greater chances of further weakness ahead.

There's been a sharp fall in the Pound (1.3071) despite the 25bp increase in interest rates by the BOE yesterday, with chances of more hikes to come. This is in keeping with our suggested view of range trade between 1.31-33. Careful now as a further decline from here could herald 1.2750 in the medium/ long term. Watch today.

Overall Dollar strength prevails and the Dollar Index (94.70) has chances of rising further towards 95.50. If so, the Euro (1.1659) could weaken next week, as it was unable to sustain a rise to 1.1687 yesterday.

Dollar-Yen (114.02) trades higher, but just below important Resistance at 114.50. A break of Resistance, if seen, could propel the market much higher, but we would not like to pre-empt such a move. The Euro-Yen (132.89) may have potential for a near-term dip towards 130.

The Support at 0.7630 has held well on the Aussie (0.7685) giving it a bit of a bounce, but it also has a relatively strong Resistance at 0.7750 overhead. A strong rise can be seen if that Resistance breaks.

Dollar-Yuan (6.6157) has recovered a bit after a dip below 6.60 yesterday and might try to rise towards 6.64 while above 6.58. Dollar-Rupee (64.61) also bounced from 64.50 yesterday and can try to test 64.70 in the near term.

INTEREST RATES

Yields have been coming down across the developed world over the last two days.

Strangely, UK yields (5Yr 0.71%. 10Yr 1.26%, 20Yr 1.76%) have dipped despite a 25bp rate hike by the BOE yesterday. The 5yr and 20Yr have Supports near current levels. We need to see if they will hold/ break today.

In USA, the 30Yr (2.83%) may have Support near 2.75% while the 10Yr (2.35%) may have Support near 2.25%. The market expects to see a post-hurricane rebound in US NFP today. Any disappointment could lead to these Supports being tested. Longer term, however, the market is looking for a rate hike by the Fed in December.

The German 10Yr (0.38%) is holding above Support near current levels while the 30Yr (1.25%) has some room to dip to 1.125% in the near-term. The German-US 10Yr Spread (-1.97%) has bounced from -2.05% over the last few days (resulting in the ongoing consolidation in the Euro). We now have to see if it can break above the now crucial Resistance at -1.95%.

In India, the 10Yr GOI (6.8611%) dipped a bit from 6.893% earlier, but remains in an overall uptrend for now. Resistance may be available near 7.00%.

What’s Next For The Dollar ?

What's Next for the Dollar?

There remains a high level of uncertainty around tax reform but USD picture remains guardedly optimistic based on the fact that something is better than nothing when it comes to lower taxes.

As for today, the Greenback remains in limbo more or less susceptible to positioning nuances as dealers attempt to figure out this tangled mess of confusion. But on a net on a net basis, the song remains the same, and from a forward-looking interest rate differential perspective, the USD should prevail on this guardedly optimistic presumption despite a tentative bid to UST 10Y yields

Meanwhile and perhaps Washington's worst kept secret, Jerome Powell will steer the Fed mandate suggesting a status quo guidance from the FOMC but it's far too early to rule out a catch -as a catch -can veer in policy. Frankly, after four years of a dovish Fed narrative, it's unlikely the new Fed Chair will be looking to rock the boat too aggressively and will likely remain as data dependent as Dr Yellen, but let's see where this morning's very animated discussion about the next Vice Char takes us. But overall despite the dearth of headline risk, US markets have been relatively subdued overnight.

Tariff time for the Loonie

The US Commerce Department is adamant that Canadian lumber producers gained mostly from selling into the US below fair value and received unfair subsidies that hurt U.S. producers. Therefore, it looks to announce a tariff. The rate: 21%.Softwood lumber kerfuffle has been the bain of the loonie for decades, so no reason to suspect otherwise this time around. I suspect the CAD will continue to roll over given the toxic combination of dovish BOC and trade sanctions

The British Pound

Carney carnage has left Sterling bulls in a world of hurt this morning as a one-and-done deal looks more likely the course for BOE policy.

Japanese Yen

USDJPY is trading very well bid while suggesting the correlation US fixed income is wobbling sending a convincing signal that real money demand remains high.

Australian Dollar

The market was expecting a modest recovery in retail sales but with the less than convincing on the dot headline print this morning the AUD bears are back en masse

EM Asia

Asian currencies should still trade with a bullish bounce given the strong global equity market and nd stability of renminbi. But frankly, retail flows remain extremely muted despite KRW's outperformance of late.

The PHP has been trading well wholly sidestepping what was perceived to be a toxic cocktail around the Fed Chair and Tax reform narrative given the bullish USD persuasion of these storylines. Investors continue to appreciate the undervalued equity market pockets on the Philippines exchange suggesting a modicum of relief for the Peso is in store.

The MYR is a slight underperformer in the regions due to seasonality concerns as trader remain defensive despite a robust and a positively evolving global growth storyline

Dollar Weaker Ahead Of US Jobs Report

Fed Chair nomination and concerns with tax reform pressure USD

The US dollar is lower against major pairs ahead of the release of the U.S. non farm payrolls (NFP) on Friday, November 3 at 8:30 am EDT. The US is expected to have gained more than 300,000 jobs rebounding from the impact of hurricanes in the September report. The US currency has been weaker after the U.S. Federal Reserve decided to keep rates unchanged in its November meeting, President Trump nominated Jerome Powell to the position of Chair and some disappointment with the US tax reform details.

The pound fell on Thursday despite the Bank of England (BoE) hiking for the first time in 10 years. Rising inflation on a slowing economic recovery ahead of the Brexit divorce forced the hand of the central bank who is now ready to raise rates at a gradual pace and to a limited extent. The actual 25 basis points lift up to 0.50 percent was already priced in so market reaction was going to center on the actual wording of the statement and the press conference with Governor Mark Carney.

The US dollar will look ahead to the release of employment data while the market digests the appointment of Fed Governor Jerome Powell to the Chairman position. Fed Chair Janet Yellen’s term will end in February, she has already congratulated and committed to work on a smooth transition. Given that he is already a part of the FOMC Powell’s confirmation by the Senate should go without further issues.

The EUR/USD gained 0.32 percent on Thursday. The single currency is trading at 1.1655 after the USD fell following the reveal of the tax reform bill. The impact on the budget deficit is problematic because it would only pass if there is Democratic support for it, even assuming Republicans are all in favour. So either some of the tax cuts will have to be pared down to make it passable with 51 votes, or there needs to be a bipartisan outreach.

The appointment of a safe choice in Jerome Powell, who was a supporter of Yellen’s decisions at the helm of the U.S. Federal Reserve is seen as less hawkish, but it also means that the central bank will remain on a tightening path and with more positions to be filled he will get some latitude to reshape the Fed going forward.

The GBP/USD lost 1.39 percent on Thursday. The pound is trading at 1.3059 after the Bank of England (BoE) raised rates by 25 basis points as anticipated. The rate hike marks the first time in 10 years that the central bank has lifted its benchmark rate. The rate now stands at 0.50 percent as concerns about high inflation continues. Brexit is the main concern, as the aftermath of the referendum to divorce form the European Union has caused the currency to drop, making imports higher. Wages have not climbed and with big question marks around economic growth with rising inflation the BoE has been forced to hike.

The gloomy tone of BoE Governor despite the rate hike took its toll on the currency. The market is viewing the monetary policy decision as a one-and-done. The vote in the Monetary Policy Commission was a mirror image of the last meeting with 7 members voting for a rate hike and 2 against. The BoE is adamant that it will keep hiking rates, but the use of “gradual” in the statement was read as more dovish than intended by the central bank.

Market events to watch this week:

Friday, November 3

5:30 am GBP Services PMI

8:30 am CAD Employment Change

8:30 am CAD Trade Balance

8:30 am CAD Unemployment Rate

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

8:30 am USD Unemployment Rate

10:00 am USD ISM Non-Manufacturing PMI

US Tax Cut, BoE Hike

The US House of Representatives released details of the tax cut plan Thursday and the market reaction showed a confused market. The commodity currencies were the top performers while the pound lagged after the BOE rate hike was accompanied with downward revisions in growth and inflation. Australian retail sales are up next.

USD/JPY fell more than a half-cent after the tax plan was released but slowly recovered over the remainder of the day. Part of the reason is that stock markets turned around to finish slightly higher after a 13 point dip in the S&P 500 to start the day.

The tax measures are undoubtedly stimulative and it appears as though the corporate tax rate will be cut to 20% immediately and permanently. That's a powerful boost for stocks. On the personal side, lower tax cuts are partly balanced by the elimination of deductions so economic gains might not be as robust.

On the question of whether it will pass, that likely depends on impending changes. Given some of the reaction, however, Trump's timeline of passing it before month-end is overly ambitions.

The trade may be to watch the bond market. Ten-year yields continue to flirt with 2.40% but have backed away, including a 2.5 bps dip to 2.35% on Thursday. The ebb and flow of the plan and various breaks are going to cause major volatility in the weeks ahead.

One thing that won't be causing further volatility is the Fed chair decision. Powell was introduced as the new leader on what was a telegraphed decision in the end.

The BOE stance is far less certain. The guidance was that future hikes will be limited and gradual. That sent cable more than 180 pips lower on the day. The pair is currently testing the Oct low of 1.3027 and that will be a key level into the weekend.

Looking ahead, the next event is Australian retail sales. AUD posted a strong day Thursday but a second consecutive soft reading could undercut the move. The consensus is for a 0.4% increase after a -0.6% reading in August.

In Friday's US jobs report, wages will remain the top market-mover in the non-farm payrolls report, where revisions will be closely scrutinized.

Pound Plunges as BoE Raises Rates

The British pound has posted sharp losses in the Thursday session. In North American trade, GBP/USD is trading at 1.3090, down 1.18% on the day. On the release front, the Bank of England raised interest rates to 0.50%, up from 0.25%. British Construction PMI improved to 50.8, above the forecast of 48.3 points. In the US, today's highlight is unemployment claims, which dropped to 229 thousand. This beat the estimate of 235 thousand. The focus will be on employment numbers on Friday, as the US releases Average Hourly Earnings, Nonfarm Payrolls and the unemployment rate. We'll also get a look at ISM Nonfarm Manufacturing PMI.

The BoE raised rates for the first time in a decade on Thursday. Although interest rate hikes generally boost the local currency, the precise opposite occurred, as the British pound has plunged 1.3 percent on the day. The reasons? The markets are treating today's move as a dovish rate, as the BoE indicated that any additional hikes would be gradual and dependent on Brexit. The rate hike reversed the rate cut back in August 2016, which was an "emergency cut" which the cautious BoE implemented to cushion the economy following the stunning Brexit vote in June 2016. As well, the Bank has been signaling for months that it planned to raise rates, so the markets had plenty of time to price in today's rate hike.

The Federal Reserve rate statement was expected to be little more than a run-up to the December rate decision, and indeed there were no surprises from Janet Yellen and Co. The Fed indicated that a rate increase is very likely at the December meeting, and was careful not to change any of the wording in its statement regarding future rate hikes. The rate statement noted that hurricanes which hit the US had caused a decline in payrolls in September, but the Fed did not expect the hurricanes to "materially alter the course of the national economy over the medium term." The markets are expecting a strong rebound in nonfarm payrolls – the forecast for Friday's US nonfarm payrolls is a robust 311 thousand, after a decline of 33 thousand in September. Still, wage growth, which was remained soft despite the strong economy, is expected to slow to 0.2 percent, as inflation remains the Achilles heel of a robust US economy.

With fed futures prices in at 96 percent, a December rate hike from the Fed appears a done deal. What can we expect in 2018? This will depend to a large degree on the new chair of the Fed, who will take over from Janet Yellen in February. Janet Yellen will wind up her 3-year term in February, and she is not expected to be reappointed by President Trump. The front runner is economist Jerome Powell, who is expected to maintain the Fed's current policy of small, incremental rates. Trump is expected to make his choice later on Thursday, and the markets could react once the new Fed chair is announced.