Sample Category Title

Australia’s Services Sector Growth Continued To Slow, Retail Sales Missed Expectations

For the 24 hours to 23:00 GMT, the AUD rose 0.47% against the USD and closed at 0.7711.

LME Copper prices declined 0.9% or $63.0/MT to $6855.0/MT. Aluminium prices declined 1.6% or $36.0/MT to $2152.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7685, with the AUD trading 0.34% lower from yesterday's close, following the release of disappointing macroeconomic indicators from the Australian economy.

Overnight data showed that Australia's AiG performance of service index declined to 51.4 in October from a reading of 52.1 in the last month, diminishing chances of a rate hike by the Reserve Bank of Australia (RBA) next week. Also, the nation's retail sales remained flat on a monthly basis in September, missing market expectations for a gain of 0.4%. In the previous month, retail sales had fallen by 0.6%.

Elsewhere in China, Australia's largest trading partner, the Caixin services PMI rose more than expected to 51.2 in October, compared to a reading of 50.6 in the prior month.

The pair is expected to find support at 0.7668, and a fall through could take it to the next support level of 0.7651. The pair is expected to find its first resistance at 0.7716, and a rise through could take it to the next resistance level of 0.7747.

In the week ahead, RBA interest rate decision and its monetary policy statement along with the AiG performance of construction index, would be closely watched by traders.

Trading trends in the pair today are expected to be determined by global macroeconomic indicators.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Eurozone Manufacturing PMI Hits An 80-Month High In October

For the 24 hours to 23:00 GMT, the EUR rose 0.32% against the USD and closed at 1.1656, after Eurozone manufacturing activity expanded at the fastest pace in more than six years to 58.5 in October, but missed preliminary reading for an advance to a level of 58.6. The manufacturing PMI had registered a level of 58.1 in the previous month.

In Germany, the final manufacturing PMI remained unchanged at a level of 60.6 in October from the prior month. Markets were expecting to ease to a level of 60.5. Additionally, the seasonally adjusted unemployment rate in Germany remained flat at 5.6% in October, meeting expectations.

The US Dollar ended lower against its peers, despite the House of Representatives unveiling a much awaited tax plan and Donald Trump’s nomination of Federal Reserve (Fed) Governor, Jerome Powell, as the next Fed Chairman. In the tax reform bill, Republicans called for slashing the corporate tax rate to 20.0% from 35.0%, cutting tax rates on companies’ profits from overseas operations and on individuals and families.

Macroeconomic releases showed that US initial jobless claims unexpectedly declined to a level of 229.0K in the week ended 28 October 2017, compared to a revised reading of 234.0K in the prior week. Market anticipation was for initial jobless claims to rise to 235.0K. Moreover, the number of planned layoffs by US companies slid 3.0% on an annual basis in October from a drop of 27.0% in the previous month.

In the Asian session, at GMT0400, the pair is trading at 1.1658, with the EUR trading a tad higher from yesterday’s close.

The pair is expected to find support at 1.1627, and a fall through could take it to the next support level of 1.1596. The pair is expected to find its first resistance at 1.1688, and a rise through could take it to the next resistance level of 1.1718.

With no major economic releases in the Eurozone today, investors will keep a tab on US non-farm payrolls report for October, along with unemployment rate and the ISM non-manufacturing PMI, all due later in the day for further direction. Also, US factory orders and durable goods orders, both for September, and the final Markit services PMI data for October, all due today would be on investors’ radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

BoE Raised Its Benchmark Interest Rate Due To Brexit Pressure, But Signalled Further Rate Hikes Would Be Gradual

.

For the 24 hours to 23:00 GMT, the GBP declined 1.48% against the USD and closed at 1.3053, following a dovish statement by the Bank of England (BoE).

The BoE's Monetary Policy Committee (MPC) increased its key interest rate to 0.50% from 0.25% by a majority vote of 7-2, its first hike since July 2007, in an effort to combat rising inflation and bring it back to its 2.0% targeted level. However, the central bank added that future interest rate hikes would be 'very gradual' and to a limited extent. BoE Governor, Mark Carney, stated that the Brexit talks would be the most important factor for the next move on interest rates, which could either go up or down.

On the data front, UK's construction PMI rose to 50.8 in October, more than market expectations of an advance to a level of 48.5. In the previous month, the construction PMI had recorded a level of 48.1.

In the Asian session, at GMT0400, the pair is trading at 1.3069, with the GBP trading 0.12% higher from yesterday's close.

The pair is expected to find support at 1.2978, and a fall through could take it to the next support level of 1.2888. The pair is expected to find its first resistance at 1.3224, and a rise through could take it to the next resistance level of 1.3380.

Moving ahead, UK Markit services PMI data for October, set to release in a few hours, would be closely assessed by market participants.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Marginally Higher In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.09% against the JPY and closed at 114.05.

In the Asian session, at GMT0400, the pair is trading at 114.02, with the USD trading marginally lower from yesterday’s close.

The pair is expected to find support at 113.63, and a fall through could take it to the next support level of 113.25. The pair is expected to find its first resistance at 114.31, and a rise through could take it to the next resistance level of 114.61.

Going forward, investors would focus on the minutes from the Bank of Japan’s (BoJ) September meeting, a speech by the BoJ Governor Kuroda, Japan’s Nikkei services PMI data and trade balance figures, all due next week.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Switzerland’s Consumer Confidence Improved Slightly And Real Retail Sales Unexpectedly Fell

For the 24 hours to 23:00 GMT, the USD declined 0.33% against the CHF and closed at 0.9995.

Macroeconomic indicators revealed that Switzerland’s SECO consumer sentiment rose to -2.0 in the fourth quarter of 2017 from a level of -3.0 in the previous quarter. Markets had expected the consumer confidence to improve to 0.0. Separately, the nation’s real retail sales unexpectedly dropped by 0.4% on an annual basis in September, against market expectations for an advance of 0.3%. In the prior month, real retail sales had recorded a revised drop of 1.0%.

In the Asian session, at GMT0400, the pair is trading at 0.9988, with the USD trading 0.07% lower from yesterday’s close.

The pair is expected to find support at 0.9956, and a fall through could take it to the next support level of 0.9924. The pair is expected to find its first resistance at 1.0013, and a rise through could take it to the next resistance level of 1.0038.

Next week, investors will look forward to Switzerland’s consumer prices and unemployment rate.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Trading Marginally Lower Ahead Of Canada’s International Merchandise Trade Figures And Unemployment Rate

For the 24 hours to 23:00 GMT, the USD declined 0.48% against the CAD and closed at 1.2812.

In the Asian session, at GMT0400, the pair is trading at 1.2813, with the USD trading a tad higher from yesterday's close.

The pair is expected to find support at 1.2787, and a fall through could take it to the next support level of 1.2762. The pair is expected to find its first resistance at 1.285, and a rise through could take it to the next resistance level of 1.2888.

Moving ahead, Canada's international merchandise trade data for September coupled with the nation's unemployment rate for October, both due today, will be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD had a moderate bullish momentum yesterday topped at 1.1687. The bias is bullish in nearest term testing 1.1725/50 area but as long as stay below 1.1900 the “head and shoulders” bearish scenario remains intact and any upside pullback should be seen as a good opportunity to sell. Immediate support is seen around 1.1625. A clear break below that area could lead price to neutral zone in nearest term testing 1.1575 area. A clear break and daily/weekly close below that area would expose 1.1450 region next week. Fundamental focus today will be on the US NFP number which is expected to be around 312K.

GBPUSD

The GBPUSD had a strong bearish momentum yesterday following a failure to break above 1.3330 key resistance, bottomed at 1.3042. The bias is bearish in nearest term testing the daily EMA 200 located around 1.3000 region which remains a good place to buy with a tight stop loss as a clear break and daily/weekly close below 1.3000 would stop the major bullish trend with a potential bearish reversal scenario. Immediate resistance is seen around 1.3135. A clear break above that area could lead price to neutral zone in nearest term testing 1.3200 region. Fundamental focus today will be on the US NFP number which is expected to be around 312K

USDJPY

The USDJPY attempted to push lower yesterday bottomed at 113.53 but closed higher at 114.08. The bias is neutral in nearest term probably with a little bullish bias testing 114.50 key resistance which remains a good place to sell with a tight stop loss as a clear break above that area would expose 115.50 or higher. Immediate support is seen around 113.75. A clear break below that area could trigger further bearish pressure testing 113.20 support area. Fundamental focus today will be on the US NFP number which is expected to be around 312K. Overall I remain neutral.

USDCHF

The USDCHF attempted to push lower yesterday bottomed at 0.9949 but closed higher at 0.9993. The bias is neutral in nearest term. Overall I remain bullish but need a clear break above 1.0037 key resistance to resume the bullish scenario testing 1.0100 or higher. Immediate support is seen around 0.9940. A clear break and daily/weekly close below that area would expose 0.9835 next week. Fundamental focus today will be on the US NFP number which is expected to be around 312K.

Market Update – Asian Session: Next Week’s RBA Meeting In Focus Amid Weaker Australia Retail Sales

Asia Summary

With the Nikkei 225 closed in observance of a holiday, Asian equity markets opened the session generally higher. Australia's S&P ASX 200 index has hit a fresh high for 2017, amid gains in the mining and energy sectors. BHP has gained over 1%, while shares of gold miner Newcrest are up over 2%.

As of the time of writing, Nasdaq Futures have gained over 0.1%, as shares of Apple traded higher in the afterhours, following its financial results and guidance.

Amid the results, Samsung Electronics, which has gained over 4% this week, is trading lower by over 1%. Shares of Taiwan Semi are also down by about 1%. In Hong Kong, Tencent has gained over 1% and moved to a fresh all-time high.

With the Reserve Bank of Australia (RBA) due to hold its policy meeting next week (Tuesday, Nov 7th), the Aussie has declined by over 0.15%. In Sept, retail sales missed market expectations for the 3rd straight month. Amid the data, Australia's 3-year bond yield has dropped over 5bps on the session.

China's 10-year bond yield is generally stable. Earlier today, the PBoC skipped its regular open market operation (OMO) and instead confirmed a medium-term lending facility (MLF) operation, which was speculated earlier in the week. Recall, it was reported earlier in the week that liquidity conditions in China may tighten in the near term with around CNY1T in funds expected to mature this week, said the China Securities Journal.

In terms of emerging market debt, Venezuela's President Maduro said state oil company PDVSA would on Friday make a $1.1B payment of bonds due in 2017 to JPMorgan. He also said, however, that the country will restructure all of its foreign debt, following the payment by PDVSA.

Looking ahead, the later today release of the US Oct nonfarm employment report will be in focus, along with ISM Non-Manufacturing PMI.

Key economic data

(AU) Australia Sept Retail Sales M/M: 0.0% v 0.4%e; Q3 Ex Inflation Q/Q: 0.1% v 0.0%e

(CN) CHINA OCT CAIXIN PMI SERVICES: 51.2 V 50.6 PRIOR; COMPOSITE: 51.0 V 51.4 PRIOR

(KR) South Korea Sept BoP Current Account Balance: $12.2B (record) v $6.1B prior; Goods Balance: $15.0B v $9.3B prior

(KR) South Korea Oct Foreign Reserves: $384.5B v $384.7B prior

Speakers and Press

China

(CN) NDRC issues draft guidelines on overseas investment by China companies

Other

(VE) Venezuela President Maduro: Will pay bonds tomorrow morning; payment on PDVSA bond to start on Friday; To restructure all foreign debt after tomorrow

Asian Equity Indices/Futures (00:30ET)

Nikkei closed, Hang Seng +0.3%, Shanghai Composite -0.7%, ASX200 %, Kospi -0.2%

Equity Futures: S&P500 flat ; Nasdaq +0.3% , Dax flat , FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR; 1.1654-1.1666; JPY 113.90-114.09; AUD 0.7682-0.7716; NZD 0.6908-0.6929

Aug Gold flat at 1,277/oz; Aug Crude Oil +0.5% at $54.81/brl; Sept Copper +0.4% at $3.149/lb

GLD SPDR Gold Trust ETF daily holdings -0.4% at 846.0 metric tons

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6072 V 6.6196 PRIOR

(CN) PBOC CONFIRMS CNY404B MEDIUM-TERM LENDING FACILITY (MLF) OPERATION; Offers 1-year loans at 3.20% v 3.20% prior

(CN) PBoC OMO: Skips OMO v skipped prior; Weekly net drain CNY110B v CNY390B injection w/w

(AU) AUSTRALIA SELLS A$500M IN DEC 2021 BONDS, AVG YIELD 2.0919%, BID TO COVER 7.25X

US markets on close: Dow +0.4%, S&P500 0.0%, Nasdaq 0.0%, Russell +0.3%

Best Sector in S&P500: Financials +0.9%

Worst Sector in S&P500: Consumer Discretionary -0.8%; Materials -0.7%

At the close: VIX 9.93 (-0.27pts); Treasuries: 2-yr 1.616% (+1.5bps), 10-yr 2.372% (flat), 30-yr % (-2bps)

US Market Summary

US indices opened largely flat after the Bank of England raised rates for the first time in roughly a decade, but moved lower after the opening bell as the long-awaited details of the Republican tax plan were finally leaked. To this point much has been in line with the run-up speculation, but it remains clear that there remain likely key sticking points that will be heatedly debated, such as the caps on mortgage interest and state/local taxes deductability. Treasury prices firmed and yields slipped; homebuilder stocks ticked lower on the release. In the afternoon, Pres Trump officially named Jerome Powell to the Fed, which had been expected for several days, but markets got a bit of a lift from the announcement. Financials, REITs, and utilities outperformed on the day, while telecom, energy, materials and consumer discretionary lagged.

US Afterhours Movers

AAPL Reports Q4 $2.07 v $1.87e, Rev $52.6B v $51.2Be; Guides Q1 Rev $84-87B v $83.3Be, gross margin 38-38.5%; guides op-ex $7.65-7.75B; +3.4% afterhours

SBUX Reports Q4 $0.55 v $0.55e, Rev $5.70B v $5.73Be; Raises dividend 20%; Estab $15B 3-yr buyback plan (~19% market cap); -6.7% afterhours

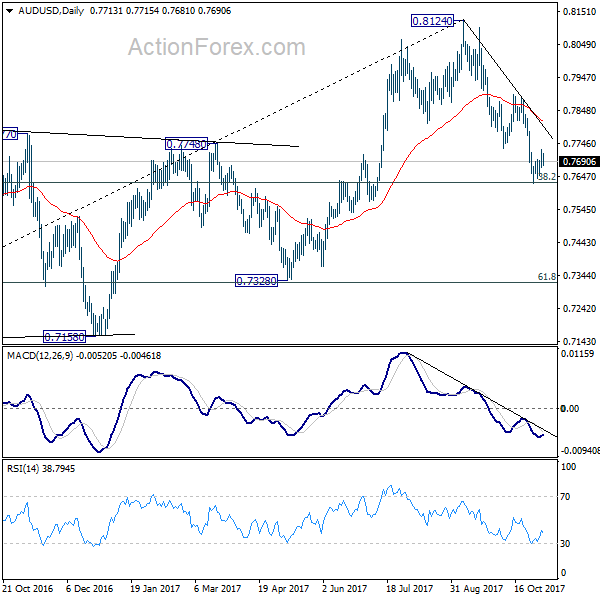

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7679; (P) 0.7704; (R1) 0.7738; More...

AUD/USD is staying in consolidation above 0.7624 temporary low and intraday bias remains neutral. On the downside, decisive of 0.7624 will resume whole decline from 0.8124 and target next key cluster level at 0.7322/8. In case of another rise, upside should be limited well below 0.7896 resistance to bring fall resumption.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

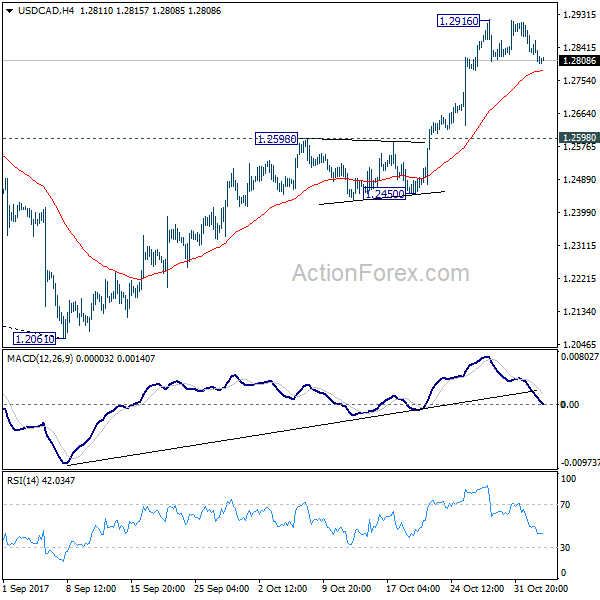

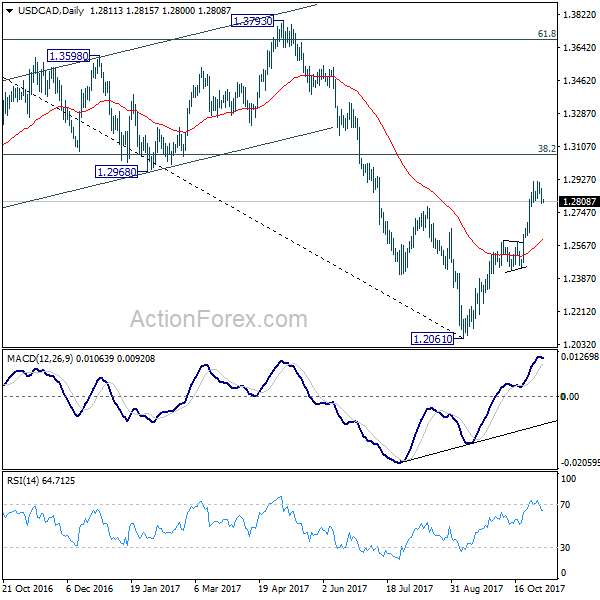

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2779; (P) 1.2827; (R1) 1.2856; More....

USD/CAD is staying in consolidation from 1.2916 temporary top and intraday bias remains neutral. In case of deeper fall downside should be contained well above 1.2598 resistance turned support and bring rally resumption. Medium term trend in USD/CAD should have reversed. Break of 1.2916 will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.