Sample Category Title

USD/CHF Continued Increase

USD/CHF is clearly in a strong bullish momentum. The technical structure suggests an improving short-term buying interest. Expected to show continued bullish momentum. Hourly support stands at 0.9951 (01/11/2017 low).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/JPY Stalling Below Resistance At 114.49

USD/JPY is pausing below strong resistance stands at 114.49 (11/07/2017 high). Support is located at 111.12 (20/09/2017 low).

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

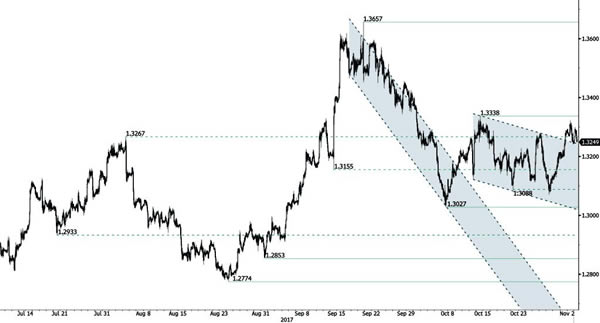

GBP/USD Monitoring Resistance At 1.3338

GBP/USD has failed to hold below broken support at 1.3088 (12/10/2017 low). The pair is monitoring resistance at 1.3338 (13/10/2017 high). Expected to show further push upwards.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. Long-term support can be found at 1.1841 (07/10/2017 low). Long-term resistance given around 1.35 is at stake and indicates a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

Elliott Wave Analysis: EURUSD Looking Lower

FX market did not move much yesterday after FOMC statement and rate decision. Price structure is basically unchanged, corrective legs that suggest stronger USD soon. We see a three leg retracement on EURUSD, AUDUSD, NZDUSD, and USDCAD, while European stocks remain in uptrend as we see DAX in minor wave four.

EURUSD made a nice rally in the last few days, back to 1.1670 area in three sub-waves so we see that as wave four within ongoing weakens that is expected to continue towards 1.1550 or even lower while we are below 1.1730 region.

EURUSD, 1H

Market Update – European Session: BOE Expected To Hike For 1st Time In Almost A Decade

Notes/Observations

BOE poised to hike rates for the 1st time in almost a decade; economist view the move as a mistake

German Unemployment Rate holds steady at post reunification lows

UK Contruction PMI moved back into expansion territory

Trump said to name Powell as the next Fed Chair (to replace Yellen)

Overnight

Asia:

China Commerce Ministry (MOFCOM): Consumption in Q4 likely to maintain steady and high growth; Concerned about US solar trade remedy proposals

Australia Sept Trade Balance registers its 11th straight surplus ( $1.8B v $1.2Be)

Europe:

European Banking Authority (EBA) said to postpone publication of bank stress test results because European banks can’t provide timely valid data for the calculations. ECB Banking Supervisor now has to adjust process of its regulatory review (SREP) in coming year

UK Parliament approved an unanimous motion to release Brexit impact studies on 58 sectors of the economy

Americas:

FOMC left its Interest Rate Range unchanged between 1.00-1.25% (as expected); core inflation remained soft even though gasoline price rise after hurricanes boosted overall inflation in Sept

President Trump to announce Fed Chairman nominee Thursday, Nov 2nd at 15:00 ET (19:00 GMT) (as speculated); to tap Fed's Powell as Chair, replacing Yellen

US House GOP members expected to release their tax plan (said to propose 12% repatriation tax rate on cash and 5% rate on non-cash holdings)

Energy:

Saudi Arabia Oil Min Al-Falih: sees OPEC+ renewing resolve to normalize oil inventories. Hoped for consensus at oil producers meeting in Vienna later this month

Economic Data

(JP) Japan Oct Consumer Confidence: 44.5 v 43.6e

(CH) Swiss Oct SECO Consumer Confidence: -2 v 0e

(HU) Hungary Oct Manufacturing PMI: 58,3 v 57.5e

(PL) Poland Oct Manufacturing PMI: 53.4 v 54.0e

(ES) Spain Oct Manufacturing PMI: 55.8 v 54.8e (48th month of expansion and highest since May 2015)

(IT) Italy Oct Manufacturing PMI: 57.8 v 56.5e (14th month of expansion and highest since Feb 2011)

(FR) France Oct Final Manufacturing PMI: 56.1 v 56.7e (confirmed 13th month of expansion)

(DE) Germany Oct Final Manufacturing PMI: 60.6 v 60.5e (confirmed 35th month of expansion)

(DE) Germany Oct Unemployment Change: -11K v -10Ke; Unemployment Rate: 5.6% v 5.6%e

(EU) Euro Zone Oct Final Manufacturing PMI:58.5# v 58.6e (confirmed 50th month of expansion and highest since Feb 2011)

(UK) Oct Construction PMI: 50.8 v 48.5e (moves back into expansion)

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) sold total €B vs. €3.5-4.5B indicated range in 2022, 2027 and 2040 Bonds

Sold €1.42B in 0.45% Oct 2022 SPGB; Avg yield: 0.336% v 0.530% prior, Bid-to-cover: 1.82x v 2.12x prior

Sold €1.67B in 1.45% Oct 2027 SPGB; Avg yield: 1.457% v 1.627% prior; Bid-to-cover: 1.35x v 1.79x prior

Sold €0.94B in 4.9% 2040 SPGB; Avg yield 2.462% v 2.646% prior, bid-to-cover 1.57x v 1.87x prior

(ES) Spain Debt Agency (Tesoro) sold €M vs. €250-750M indicated range in 0.65% Nov 2027 Inflation-linked bonds (SPGBei); Real Yield: % v 0.371% prior; Bid-to-cover: x v 1.94x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 flat at 396.6, FTSE +0.1% at 7494, DAX -0.2% at 13445, CAC-40 flat at 5511, IBEX-35 flat at 10505, FTSE MIB +0.5% at 23110, SMI flat at 9265, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes:

European Indices trade flat this morning consolidating recent gains with another busy morning of earnings and the impending rate decision from the BoE in which analysts eye the first rate increase in a decade.

Financial giants Credit Suisse and ING reported strong results this morning, while in the retail space Hugo Boss outperforms after raising full year guidance. Edreams trades sharply higher in Spain after raising FY18 and FY20 outlook and explores strategic alternatives.

Looking ahead notable earners include AmerisourceBergen, Ralph Lauren and Hyatt, after the close notable earners include Apple.

Equities

Consumer discretionary [Hugo Boss [BOSS.DE] +5.9% (Earnings), Edreams [EDR.ES] +17.5% (Raises outlook, explores alternatives), Morrisons (MRW.UK) -1.3% (Q3 update)]

Industrials: [Pfeiffer Vacuum (PFE.DE) +5.5% (Earnings)]

Financials: [Credit Suisse [CSGN.CH] +3.8% (Earnings)]

Healthcare: [Sanofi [SAN.FR] -1.9% (Earnings), Fresenius SE [FRE.DE] -1.1%]

Speakers

Norway Central Bank (Norges) Financial Stability Report: Sector vulnerable to household debt and house prices. Largest banks were resilient to pronounced downturn in economy

ESM's Regling reiterated view of need to complete banking union. EU did not need full fiscal union. Saw only a few steps needed to make EMU region more resilient

Catalan Poll: Secessionist bloc to win 68 seats in the 135 seat regional parliament (slight majority)

Taiwan Central Bank Sept Minutes: Some members saw real rates as relatively high and concerned about domestic demand

Currencies

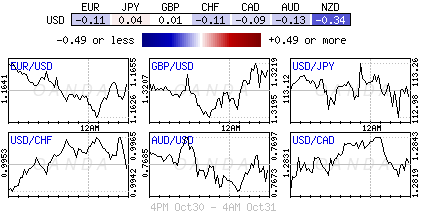

USD was softer in quiet trading but off its worst levels ahead of some key events in the session. On the US front President Trump is expected to name Powell as his nominee for the Fed Chair position while GOP members to unveil details of the tax reform plan.

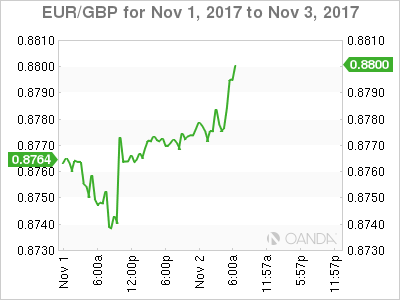

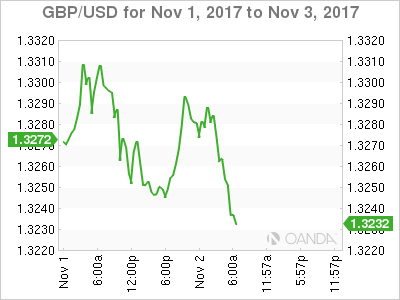

BOE was said to be poised to raise interest rates for the first time in almost a decade. Dealers noted that the central bank’s policy outlook had been the main driver for sterling in recent months. For the time being the increased expectations of a hike have temporarily overshadowed Brexit concerns. However, a poll of economists believed that a rate hike at this time would be a mistake for the UK economy. GBP/USD saw its earlier gains evaporate with the pair trading at 1.3250 just ahead of the NY morning.

EUR/USD was off its best levels ahead of the NY morning with the pair up 0.1% at 1.1635

Fixed Income

Bund futures trade at 162.71 up 1 ticks as core euro-bonds are little changed during a public holiday for Austria, Belgium, France, Portugal and Spain. Support lies at 161.00, followed by 160.38. Resistance stands initially at 163.51, followed by 164.25.

Gilt futures trade at 124.19 down 2 ticks, with the focus remaining on the BOE meeting. Continued downside eyeing 123.26. Upside targets 124.90 then 125.24.

Thursday’s liquidity report showed Wednesday’s excess liquidity rose to €1.838T from €1.825T and use of the marginal lending facility rose to €237M from €172M

Corporate issuance saw 3 issuers raise $2.5B in the primary market

Looking Ahead

(IL) Israel Central Bank (BOI) Oct Minutes

05:50 (FR) France Debt Agency (AFT) to sell €7.5-8.5B in 2028, 2031 and 2048 Oats

06:00 (CY) Cyprus Oct CPI M/M: No est v 0.3% prior; Y/Y: No est v -0.4% prior

06:00 (EU) Daily Euribor Fixing

06:30 (HU) Hungary Debt Agency (AKK) to sell Floating Bonds

06:30 (HU) Hungary Debt Agency (AKK) to sell 12-month Bills

07:00 (ZA) South Africa Sept Electricity Production Y/Y: No est v 0.8% prior; Electricity Consumption Y/Y: No est v 1.7% prior

07:15 (NO) Norway Central Bank (Norges) Dep Gov Matsen in Trondheim

07:30 (US) Oct Challenger Job Cuts: No est v 32.4K prior; Y/Y: No est v -27.0% prior

07:45 (US) Daily Libor Fixing

08:00 (UK) Bank of England (BOE) Interest Rate Decision: Expected to raise Interest Rates by 25bps to 0.50%

08:00 (UK) BOE Nov Minutes

08:00 (UK) BOE Inflation Report

08:00 (CZ) Czech Central Bank (CNB) Interest Rate Decision: Expected to raise Repurchase Rate by 25bps to 0.50%

08:30 (US) Initial Jobless Claims: 235Ke v 233K prior; Continuing Claims: 1.89Me v 1.893M prior

08:30 (US) Q3 Preliminary Nonfarm Productivity: 2.5%e v 1.5% prior; Unit Labor Costs: 0.4%e v 0.2% prior

08:30 (US) Weekly USDA Net Export Sales

08:30 (UK) BOE Gov Carney press conference on QIR

08:30 (US) Fed’s Powell (voter, moderate) at event

09:00 (RU) Russia Gold and Forex Reserve w/e Oct 27th: No est v $425.6B prior

09:00 (SG) Singapore Oct Purchasing Managers Index: 51.9e v 52.0 prior

09:00 (US) Republican Tax Plan announcement

09:05 (UK) Baltic Dry Bulk Index

09:15 (CZ) Central Bank Gov Rusnok to hold post Rate Decision press conference

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (DK) Denmark Oct Foreign Reserves (DKK): No est v 464.3B prior

12:00 (CA) Canada to sell 2-Year Bonds

12:20 (US) Fed's Dudley (dove, FOMC voter) at alternative rate round-table event

13:00 (IT) Italy Oct New Car Registrations Y/Y: No est v 8.1% prior

15:00 (US) President Trump expected to announce Fed Chair position

BoE Decision To Rock Sterling

In the U.K the Bank of England (BoE) is expected to hike interest rates for the first time in more than a decade (+0.25 bps to +0.5% at 08:00 am EDT) on the back of inflation running well ahead of the central banks +2% target. Nevertheless, there is a large degree of uncertainty on the vote split. The median consensus is 6-3 in favor of a rate rise, but it could even be larger.

In the MPC's updated economic projections, the consensus believes that the BoE's inflation forecasts are likely to continue to show an overshoot of the +2% target at the 2- and 3-year forecast horizon, leaving the door ajar for additional tightening in the coming months.

However, given the market's uncertainty around the U.K's political and economic outlook, it would not be a surprise to hear Governor Carney at the press conference (08:30 am ETD) to continue to stress that additional interest rate rises will be highly data dependent, with any increases likely to be 'limited' and 'gradual.' Not matter what, expect sterling (£1.3260).

Finally, watch out for Carney's Brexit assumptions. A change in the BoE's language on how Brexit is expected to pan out would have an implication on market expectations of future rate rises. To date, the BoE has expected a “smooth adjustment.”

Uneventful Fed dislodges U.S dollar and Treasury yields momentarily

Yesterday's Federal Open Market Committee (FOMC) did not stray too far from what capital markets had been expecting – no rate hike, and the committee reiterating their view that U.S economic growth is “solid” and are considering raising rates once more by year's end.

President Trump is due to announce the next Fed Chair at 03:00 pm ETD. His pick is expected to be Jerome Powell, who is a current Fed Governor, and would represent continuity in monetary policy.

Aside from central banks, investors remain focused on the progress toward U.S tax reform, corporate earnings and tomorrow's U.S and Canadian job numbers.

1. Stocks see green

In Japan, the Nikkei share average extended its strong rally to trade atop a new 21-year peak overnight, ahead of a long weekend, supported by robust earnings prospects. The Nikkei ended up +0.5%, its best close since late June 1996. For the week, the index rallied +2.4%, its eighth straight weekly gain and longest winning streak since PM Abe's Abenomics reforms started five-years ago. The broader Topix gained +0.4%.

Down-under, Australia's S&P/ASX 200 Index dipped -0.1% and South Korea's Kospi index lost -0.4%.

In Hong Kong, stocks slipped, mirroring some market nervousness as investors waited for key policy events in the U.K and the U.S. Both the Hang Seng index and the China Enterprises Index fell -0.3% respectively.

Note: Investors are also weighing up the impact of a possible policy change that could change the share structure of “H-shares,” or mainland companies listed in Hong Kong.

In China, Shanghai stocks weakened on Thursday, dragged lower by industry and material shares, as investors worried about a possible economic slowdown and tighter liquidity before year-end. The blue-chip CSI300 index was unchanged, while the Shanghai Composite Index closed down -0.4%.

In Europe, regional indices are trading relatively flat, consolidating gains ahead of another busy session of earnings and the impending BoE rate decision.

U.S stocks are set to open in the 'red' (-0.1%).

Indices: Stoxx600 flat at 396.6, FTSE +0.1% at 7494, DAX -0.2% at 13445, CAC-40 flat at 5511, IBEX-35 flat at 10505, FTSE MIB +0.5% at 23110, SMI flat at 9265, S&P 500 Futures -0.1%.

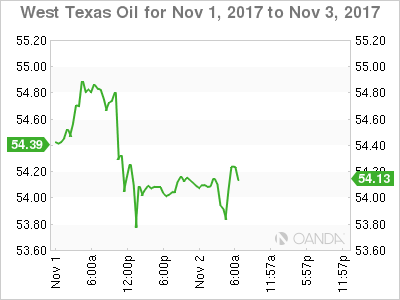

2. Oil steady on OPEC led supply cuts, tight U.S. market, and gold higher

Oil prices are trading steady as supply cuts by OPEC and non-OPEC members have tightened the market despite higher production in the U.S.

Brent crude is down -20c at +$60.29 a barrel. Yesterday, Brent reached its highest intraday level in two-years and it is up +36% from its June low. U.S light crude (WTI) is -20c lower at +$54.10 and almost +30% above its July low.

Earlier this morning, the Saudi Energy Minister Khalid al-Falih said supply and demand balances were tightening and oil inventories falling, while compliance with the OPEC-led pact to curb supplies had been “excellent”.

Note: Overall, oil markets have been slightly undersupplied this year, resulting in inventory drawdowns and the OPEC pact to withhold supplies runs to March 2018, but there is growing consensus to extend the deal to cover all of next year.

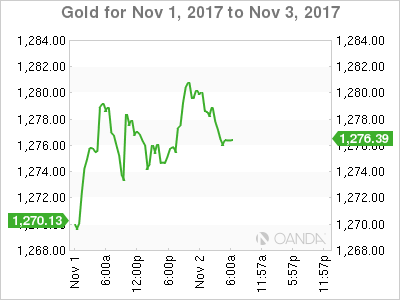

Ahead of the U.S open, gold has rallied to a one-week high overnight amid a weaker dollar and on increased demand from Chinese retail investors and as the market waits for the announcement of a new chair of the U.S Federal Reserve. Spot gold is up +0.3% at +$1,278.10 per ounce, after earlier rising to +$1,281.43.

3. Sovereign yields little changed

U.S Treasuries stalled Wednesday after the Fed held interest rates steady as expected. The yield on the benchmark U.S 10-year note settled at +2.378%.

Fed officials expect “that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate,” the FOMC statement said.

Note: At their September policy meeting, Fed officials suggested they expect three-rate increases in 2018, two in 2019 and one in 2020 – a path that is deemed rather 'hawkish' given the lag in inflation.

For the new Fed head, it does not matter for the interest rate cycle who replaces Janet Yellen. Today's front-runner, Jerome Powell is seen as a tad more hawkish than Yellen, but still on the dovish side, and John Taylor, who is on the hawkish side.

Elsewhere, German 10-year Bund yields are little changed at +0.38%, while U.K 10-year Gilts have backed up +1 bps to +1.35% ahead of the BoE decision.

4. Will Sterling buck the trend?

The BoE are expected to raise interest rates by +25 bps, but it is also likely they will hint at two further rate increases in the next two or three years, so that sterling (£1.3240) can strengthen enough to bring inflation back to +2%.

A rate increase is nearly all priced in, but sterling can still rise if the BoE follows through with its hints that it will raise rates.

However, if they don't hike, the pound is expected to come under considerable pressure. The pull back could be temporary, as investors will shift their focus on prospects of Brexit talk progress.

A 'no' rate rise would see EUR/GBP rise modestly and GBP/USD would probably test back towards stronger support atop of £1.3070 area. But further out, positioning for a Brexit deal and sufficient progress at the EU Council in December could open the door for the EUR/GBP to return to a €0.84-0.86 trading range and GBP/USD could rise towards £1.3500 handle.

The USD is a tad softer in quiet trading, but off its worst levels, while EUR/USD is off its best levels ahead of the U.S open with the pair up +0.1% at €1.1635.

5. U.K construction activity edges higher, but outlook bleak

U.K data this morning suggests that the construction sector looks troubled.

Markit's purchasing managers' index on construction rose to 50.8 in October, from 48.1 in September. The print does signifying expansion in the sector, but only just.

Digging deeper, growth in house building partly offset lower civil engineering and commercial activity. But the sector's outlook is bleak, with the balance of firms expecting business activity to increase over the next 12 months at its weakest in five-years.

NZDUSD Makes Corrective Move Higher To Pause Broader Downtrend But Upside Momentum Fades

NZDUSD maintains its downtrend from the September 20 high of 0.7434 but downside momentum has paused at 0.6817. The short-term bias has shifted to the upside after a strong rebound lifted the pair to 0.6942 earlier today. There were bullish signals on the 4-hour chart, as the market is now trading above the 20 and 50-period moving averages. Oscillators are bullish leaning.

Good support is expected on dips in the near term but if prices break below 0.6817 this would confirm the resumption of the broader downtrend for a move to the next major low at 0.6674.

To the upside, NZDUSD needs to rise above 0.7055 to relieve immediate downside pressure but only a move above key resistance at the psychological 0.7200 level would shift the bias to a more bullish one. Further strength would see another leg up to 0.7343 and open the way for a re-test of 0.7434. At this stage the trend would turn to bullish with scope to target the 0.7557 peak.

The current corrective move may not have enough upside momentum but there are no clear signs of a reversal in the broader downtrend yet. A drop below 0.6817 would put another lower top in place.

EURUSD Analysis: Remains Undecided After FOMC Meeting

None of the yesterday's fundamental events led to notable price movements. In other words, the currency rate remained in a limbo between resistance at 1.1658 and support near 1.1610 that formed three days ago. The reason behind such weak reaction might be attributed to quite expected result of the FOMC meeting, which underlined solid economic growth, and anticipation of announcement of the next Fed Chair. Once this happens, the balance between bulls and bears will be distorted and the pair is likely to make a long awaited breakout. On the other hand, it already feels the pressure from the 55- and 100-hour SMAs, which are trying to push it towards the weekly PP at 1.1674. However, there are also signs of formation of a junior ascending channel. In that case, a rebound is expected to follow.

GBPUSD Analysis: Prepares For BoE Decision

In result of release of various American fundamental data, the cable stopped the surge and returned back to the 1.3250 mark, from which it made a rebound in the beginning of this trading session. Until announcement of the Bank of England decision, the pair most probably is going to move horizontally near the 1.3290 level. Afterwards, the Pound is widely expected to strengthen. The surge might be quite sharp, as northern side contains no barriers except for an alleged resistance at 1.3338 and the weekly R2 at 1.3370. The upside momentum might be additionally reinforced if President Trump will pick Governor Powell, as the new Fed Chair. The upward movement is also supported by existence of a medium-term ascending channel.

USDJPY Analysis: Trades In A Limbo Near 114.00

As the FOMC Meeting did not bring any unexpected news, the surge of the rate was limited. In other words, the pair once was stopped by resistance barrier at the 114.24 level. The fully-fledged rebound did not happen as well, as the 55-, 100- and 200-hour SMAs together with the weekly PP formed a strong support level. As a result, the pair found itself in a limbo between the 114.24 and 113.74 marks. Until the new Fed Chair announcement, the pair is expected to continue to move horizontally. If President Trump chooses Professor Taylor, bulls might try to elevate the rate not only to the weekly R1 at 114.34 but also to the July 2017 maximum at 144.50. If President Trump nominates Governor Powell, bears are likely to drag it down towards the monthly PP at 113.25.