Sample Category Title

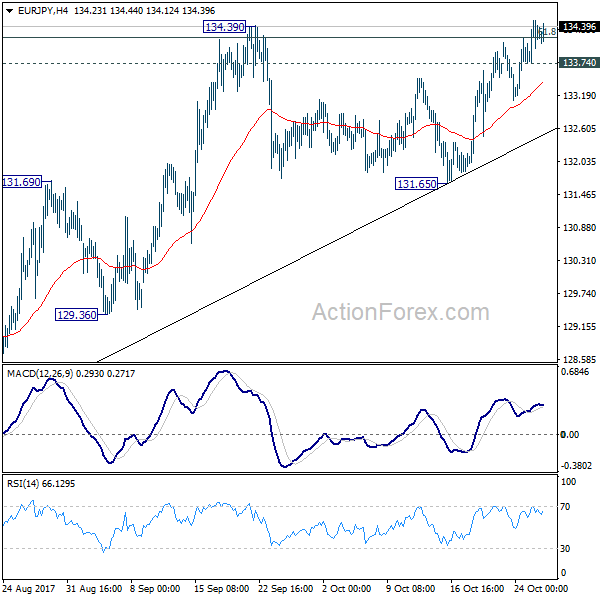

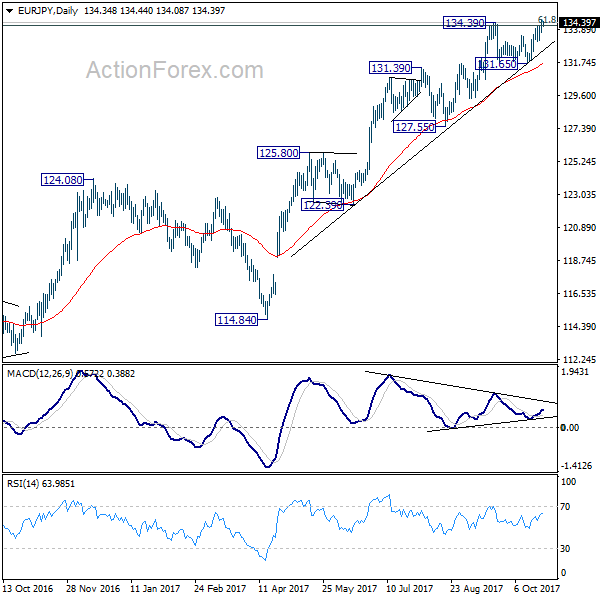

EUR/JPY Daily Outlook

Daily Pivots: (S1) 133.90; (P) 134.20; (R1) 134.64; More...

EUR/JPY's breach of 134.39 resistance argues that medium term rally is resuming. Intraday bias is cautiously on the upside. Sustained trading above 134.39 will confirm and target 141.04 long term resistance. However, break of 133.74 minor support will dampen this view and turn bias back to the downside for 131.65 support instead.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversed and will turn outlook bearish for deeper fall.

Daily Wave Analysis: EUR/USD Bullish Bounce Faces Resistance Before ECB Rate Decision

Currency pair EUR/USD

The EUR/USD is facing an interest rate decision later today by the European Central Bank (ECB), which could cause strong price movement and volatility. From a wave perspective, price could be finishing a wave 1 (blue) and ready for a retracement back to the Fibonacci levels of wave 2 (blue). These Fib levels could act as support if indeed a larger wave C (purple) of wave X (pink) indeed takes place.

Invalidation for the wave 1-2 (blue) is a break below the 100% Fibonacci level. A break above the resistance trend line could indicate a larger wave 3 (green).

Currency pair GBP/USD

The GBP/USD broke above the resistance (red) trend line could indicate that a larger wave C (orange) is taking place.

The GBP/USD could be in a wave 3 (brown) bullish breakout but needs to break above the resistance (red) before more upside is likely.

Currency pair USD/JPY

The USD/JPY is building a potential wave 4 (blue) within the uptrend. A break above resistance (red) could see price challenging the 114.50-115 target zone.

The USD/JPY bounced at the 38.2% Fibonacci level which was part of a wave 4 correction (blue). A break above resistance (red) could confirm the wave 5 (blue/purple) breakout.

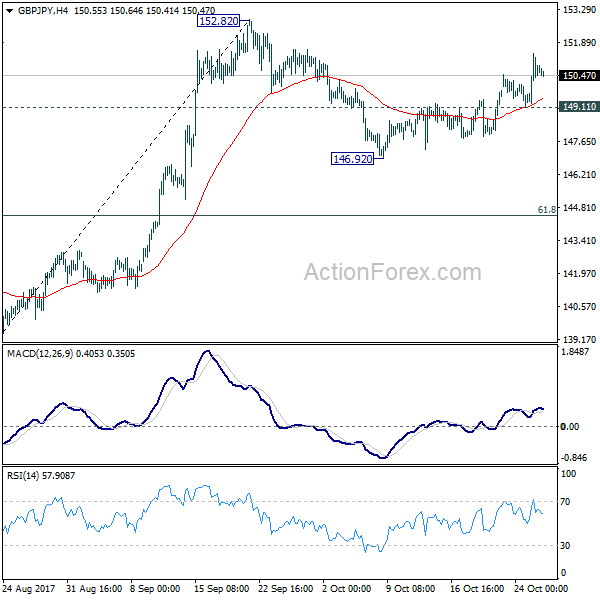

GBP/JPY Daily Outlook

Daily Pivots: (S1) 149.11; (P) 149.60; (R1) 150.06; More

Intraday bias in GBP/JPY remains on the upside as rebound from 146.92 is in progress for 152.82 high. Firm break there will confirm resumption of medium term rise from 122.36 and target 163.87 resistance next. On the downside, break of 149.11 minor support will turn bias to the downside and extend the correction from 152.82. In that case, we'd expect strong support from 61.8% retracement of 139.29 to 152.82 at 144.45 to bring rebound.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

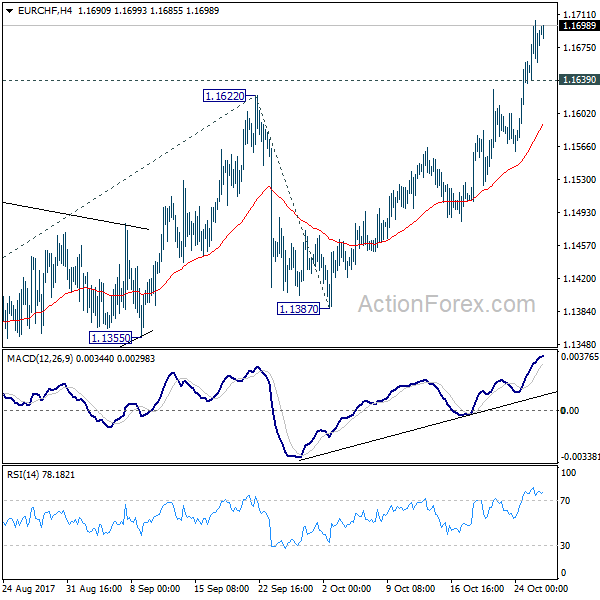

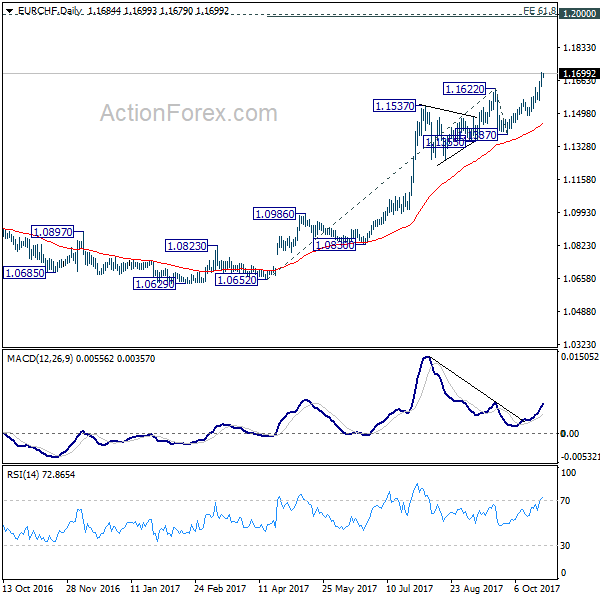

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1650; (P) 1.1678; (R1) 1.1716; More...

EUR/CHF's rally is still in progress and intraday bias remains on the upside. Current up trend should target 61.8% projection of 1.0652 to 1.1622 from 1.1387 at 1.1986, which is close to 1.2 key level. On the downside, below 1.1639 minor support will turn bias neutral and bring consolidations. But near term outlook will remain bullish as long as 1.1387 support holds.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds.

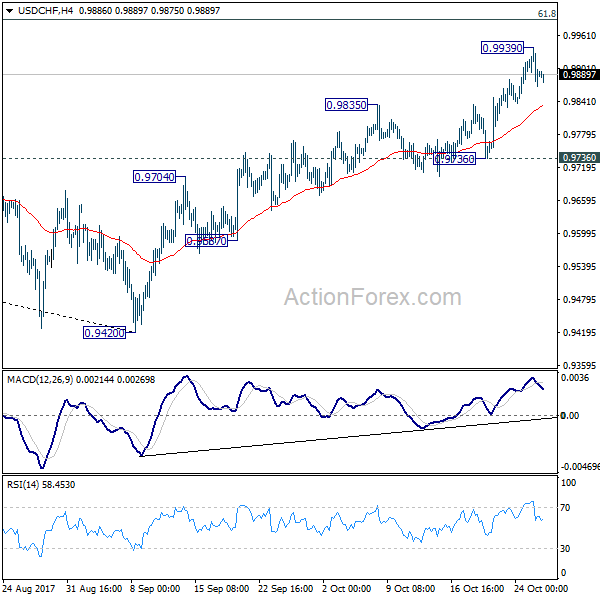

US Dollar In Monstrous Uptrend Vs Swiss Franc

Key Highlights

- The US Dollar climbed higher this week and moved above 0.9840 against the Swiss Franc.

- There is a short-term bullish trend line forming with support at 0.9880 on the 4-hours chart of USD/CHF.

- The US New Home Sales in Sep 2017 increased by 18.9% (MoM), better than the forecast of -0.9%.

- Today, the US Pending Home Sales for Sep 2017 will be released, which is forecasted to increase by 0.2% (MoM).

USDCHF Technical Analysis

The US Dollar surged higher during the past few days and moved above the 0.9800 handle against the Swiss Franc. The USD/CHF pair is now placed well in the bullish zone above 0.9840.

The pair recently traded as high as 0.9939 and started correcting lower. It tested the 23.6% Fib retracement level of the last wave from the 0.9736 low to 0.9939 high.

On the downside, there is a short-term bullish trend line forming with support at 0.9880 on the 4-hours chart. However, the most important support is close to 0.9840 and the 50% Fib retracement level of the last wave from the 0.9736 low to 0.9939 high.

The overall trend remains bullish for USD/CHF and dips towards 0.9850-40 are most likely to find buyers in the near term.

US New Home Sales

Recently in the US, the number of New Home Sales for Sep 2017 was released by the US Census Bureau. The forecast was slated for a decline in sales by 0.9% compared with the previous month.

The actual result was better than the forecast, as there was a rise in sales by 18.9% to a seasonally adjusted annual rate of 667,000. However, the last reading was revised down from -3.4% to -3.6%.

Looking at the Housing Price Index in August 2017, there was a rise of 0.7% compared with the previous month, and more than the forecast of +0.4%.

The report stated:

For the nine census divisions, seasonally adjusted monthly price changes from July 2017 to August 2017 ranged from -0.1 percent in the New England division to +1.4 percent in the Pacific division. The 12-month changes were all positive, ranging from +5.0 percent in the Middle Atlantic division to +9.3 percent in the Pacific division.

Overall, the USD/CHF pair has no reason to move down and likely to remain supported above 0.9880-0.9860 in the near term.

Economic Releases to Watch Today

ECB Interest Rate Decision – Forecast 0%, versus 0% previous.

US Initial Jobless Claims – Forecast 253K, versus 222K previous.

US Pending Home Sales for Sep 2017 (MoM) – Forecast +0.2%, versus -2.6% previous.

US Goods Trade Balance Sep 2017 – Forecast $-63.80B, versus $-62.94B previous.

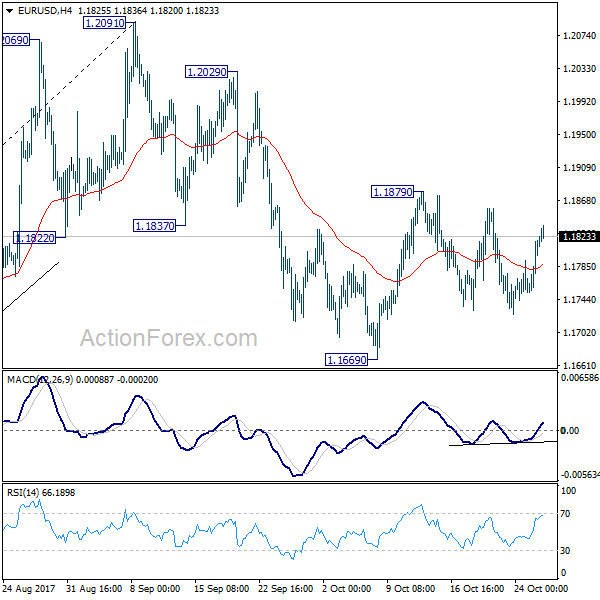

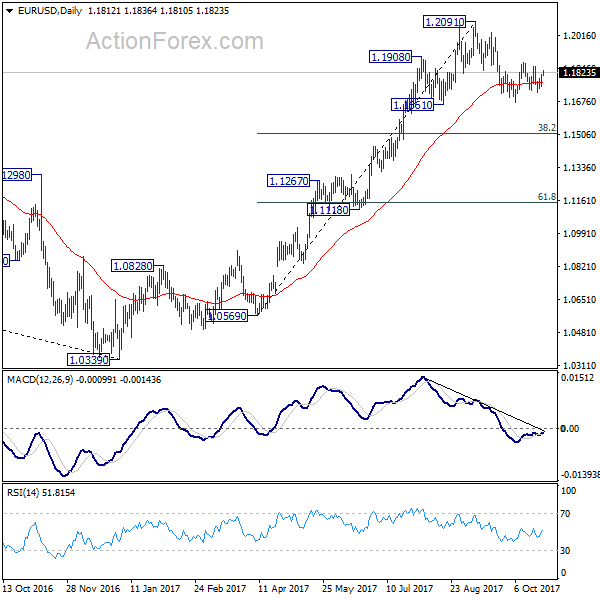

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1770; (P) 1.1794 (R1) 1.1835; More...

Intraday bias in EUR/USD remains neutral at this point. On the downside, break of 1.1669 will resume the corrective fall from 1.2091 to 38.2% retracement of 1.0569 to 1.2091 at 1.1510. We'd expect strong support from there to complete the correction. On the upside, break of 1.1879 will revive the case that pull back from 1.2091 has already completed at 1.1669. In such case, intraday bias will be turned back to the upside for retesting 1.2091 high.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

Forex: Strong Economic Data From The UK & US

On Wednesday, the UK Office for National Statistics released Gross Domestic Product, that beat expectations, coming in with growth of 0.4% in Q3. Improving by 0.1% on the previous quarter of 0.3%, UK Chancellor Phillip Hammond commented that it showed a “resilient economy which is supporting a record number of people in employment”. The mainstay of the UK, the services sector, which accounts for nearly 80% of economic growth, grew by 0.4% as it did in the previous quarter. Industrial production also grew by 1% during Q3, helped by a 1% jump from manufacturing and a 1.5% increase from mining and quarrying. Despite the growth in GDP, the estimate for annual growth is below the 1.8% last year and is the slowest for 5 years. The better-than-expected data helped push GBP higher against its peers with GBPUSD rising to a near 3-week high.

The US Census Bureau released Durable Goods Orders and ex Transportation data for September on Wednesday that increased more than expected. Durable goods for September climbed to 2.2%, beating expectations of a 1% rise, to $238.7 billion. The bulk of the increase was a result of higher transportation orders which rose by 5.1%. Durable Goods have now increased in 3 out of the last 4 months. The data indicated a favorable manufacturing sector, despite the recent Hurricanes that disrupted employment data. Following the release, the USD saw initial buying interest before retracing lower.

The Bank of Canada held its benchmark interest rate at 1% on Wednesday, but raised concerns about the Canadian economy. Policy makers, led by Governor Stephen Poloz, left the benchmark overnight rate at 1%, after consecutive hikes at the bank's last two decisions in July and September, and warned they will remain “cautious” when considering future hikes. Following the announcement, the markets are now discounting the likelihood of another interest rate hike this year, which caused CAD to weaken by 1%. Many are now expecting a hike in Canadian interest rates by March of next year and not January as many had forecast.

The markets are now focusing on today's ECB Meeting at 12:45 BST.

EURUSD is 0.1 higher in early trading, around 1.1825.

USDJPY is 0.1 lower in early trading, around 113.52.

GBPUSD is little changed, trading around 1.3265.

Gold is 0.2% higher overnight, trading around $1,280.

WTI is 0.2% lower in early trading, around $52.18.

Major data releases for today:

At 08:45 BST, the Reserve Bank of Australia Assistant Governor Guy Debelle is scheduled to speak at the ABS Auditorium, Abercrombie Business School at the University of Sydney.

At 12:45 BST, the European Central Bank will announce its Interest Rate decision. The markets are not expecting any change.

At 13:30 BST, the US Department of Labor will release Initial Jobless Claims for the week ending October 20th, along with Continuing Jobless Claims for the week ending October 13th. Initial claims are expected to have risen to 253K from the previous 222K. Continuing claims are forecast to come in at 1.890M, a slight increase on the previous 1.888M. Any significant deviation from the forecasts are likely to see USD volatility.

At 13:30 BST, following the 12:45 BST ECB interest rate decision there will be the ECB Monetary policy statement and press conference. The markets will be keen to hear news of changes in policy which may affect EUR.

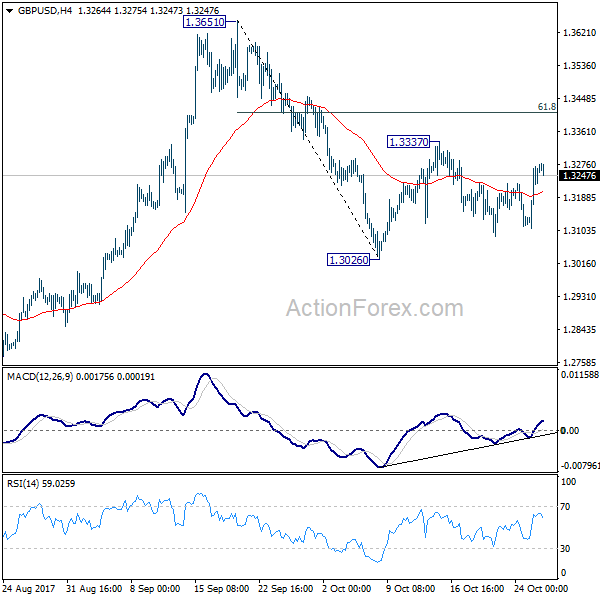

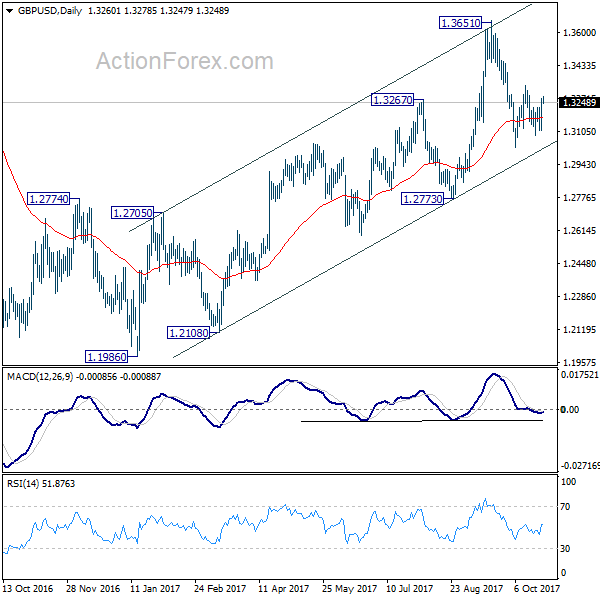

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3157; (P) 1.3214; (R1) 1.3319; More....

GBP/USD is still bounded in range of 1.3026/3337 and intraday bias stays neutral at this point. On the downside, break of 1.3026 will resume the decline from 1.3651 and target 1.2773 key support level. This will also revive the case of medium term reversal. Meanwhile, on the upside, break of 1.3337 will resume the rebound from 1.3026 to 61.8% retracement of 1.3651 to 1.3026 at 1.3412 and above.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll stay neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Currencies: Will Draghi Prevent Further Euro Strength

Sunrise Market Commentary

- Rates: Position for hawkish outcome ECB

The Bond market reaction will be put against the consensus scenario of a 9-month extension of APP while slashing the pace of purchases to €30 bn/month from January. If consensus is right, the lifespan of the Bund rally will be limited. Our favourite scenario of a 6 month extension will put the Bund on the defensive with key yield resistance at 0.50% unable to stand. - Currencies: Will Draghi prevent further euro strength

The euro is resilient going into the ECB meeting . The dollar struggles as sentiment on risk turns less positive. Today, the ECB policy decision will decide the short-term fate of the euro. Given recent euro resilience, any perceived signs of hawkishness might support the single currency.

The Sunrise Headlines

- US stock markets corrected around 0.5% lower yesterday. Asian risk sentiment is mixed overnight with China outperforming.

- The ECB meeting today will decide on the future of APP. Consensus expects a 9-months extension to September 2018 while halving monthly purchases to €30 bn from January onwards. Risks are on the hawkish side of expectations. We favour only a 6-month extension until June 2018.

- South Korea’s economy kicked into gear in the third quarter (1.4% Q/Q) as renewed investment in construction and a return to growth for exports helped the country’s gross domestic product expand at the fastest pace in 7 years.

- The Bank of Canada held interest rates steady even as it said the economy was at or near full capacity, signalling it was willing to let the economy run a little bit hot amid uncertainty over NAFTA renegotiations. USD/CAD surged from 1.2650 to 1.28.

- “In my opinion, in order to make a fair deal with Nafta, you have to terminate the deal and you have to see where you’re going to come. And we’ll come out,” President Trump said.

- Today’s eco calendar contains EMU M3 money supply, US weekly claims and US trade balance. Swedish and Norwegian central banks meet as well. The US (7-yr Note) and Italy (I/L) tap the market

Currencies: Will Draghi Prevent Further Euro Strength

Will Draghi be dovish enough to avoid euro gains?

On Wednesday, trading showed its recent usual pattern. Core (EMU and US) yields extended their rise supported by strong eco data (German IFO and US durable orders). This rise in yields was fairly neutral for EUR/USD. Euro investors looked forward to the ECB meeting. USD/JPY and EUR/JPY outperformed and came close to MT highs. Later in the session, the rise in yields was aborted as equities fell prey to profit taking. This time, the dollar suffered most. EUR/USD returned north of 1.18 and closed at 1.1813. USD/JPY finished the session at 113.74.

Overnight, Asian equities are trading mixed with China outperforming. Asian investors are in wait-and-see modus ahead of the ECB policy decision and ahead of the results from major tech companies, expected later today. EUR/USD trades with a slightly positive bias in the low 1.18 area. Dollar is also losing a few ticks against the yen (EUR/USD at 113.45). AUD/USD struggles not to fall below the 0.77 handle.

Today, the US jobless claims, the advance trade balance and the pending home sales reports won’t be important, while halving monthly purchases to €30 bn from January 2018. We see risks for a shorter extension. Forward guidance on the end of APP will also be important. Even more important is the forward guidance on interest rate policy. Will the ECB repeat that rates will remain at the current levels for an extended period and well past the end of the APP programme? We think so as it is key to keep market expectations about the first rate hike at bay. Over the previous days, the euro traded strong across the board. The dollar failed to gain against the single currency even as interest rate differentials have risen sharply since early September. A prolongation of the APP by nine months and the ECB maintaining the forward guidance on interest rates should be negative for the euro. However, giving recent resilience of the single currency any hawkish deviations in the ECB assessment won’t go unnoticed in FX market

In that scenario, there are upside risks for the euro, especially short-term. Further down the road, issues like Spain, the replacement of Yellen and the US tax cuts come to support the dollar. For today, any ‘perceived hawkishness’ (or e.g. a positive tone on the economy) might already be enough to trigger a substantial up-tick in the single currency.

From a technical point of view, EUR/USD dropped below the 1.1823/ 1.2070 consolidation pattern, but there was no sustained follow-through price action, which was disappointing for EUR/USD bears. The pair needs to drop below 1.1670/62 to give comfort to EUR/USD bears. ON the topside, a break of the 1.1880 area might open the way for a retest of the 1.2092 correction top. The USD/JPY momentum was positive in September. The pair regained 110.67/95 resistance, a short-term positive. The 114.49 correction top is the next resistance. Sentiment improved further last week, but we still assume that a break beyond 114.49 will be difficult. This week’s failed return above 114 confirms our view.

EUR/USD: holding within established ranges going into ECB meeting

EUR/GBP

EUR/GBP holds near 0.89 as BoE rate hike is discounted

Yesterday, the focus for sterling trading turned from Brexit to the eco data. UK Q3 GDP growth printed slightly stronger than consensus. The ‘stronger’ Q3 GDP removed most market doubts on a BoE rate hike next week and kick-started a sterling rebound. EUR/GBP returned below 0.89 and closed the session at 0.8909. The rise in cable was even more impressive. The pair jumped from the 1.3120 area and closed the session at 1.3262. USD softness also play a role.

Today, the CBI retail data will be published. For October, a substantial setback is expected after a remarkable upswing in September. The correlation between the monthly CBI data and the ONS retail sales is very loose and the market reaction is thus modest at best. A one-off BoE rate hike is now ‘discounted’ after yesterday’s better than expected GDP data. We don’t expect the CBI data to amend it. Maybe there is room for a slightly bigger reaction in case of a weak than of a strong report. The euro reaction after the ECB will also be key for EUR/GBP.

EUR/GBP staged a strong uptrend from April till late August and set a top at 0.9307. Rising UK inflation and the BoE preparing markets for a November rate hike triggered a sterling rebound, but it has run its course. EUR/GBP supports at 0.8743 and 0.8652 proved too difficult to break. The recent rebound above 0.89 improved the ST technical picture of EUR/GBP, but for now there were no convincing follow-through gains. EUR/GBP 0.9026 is 50% retracement of the recent countermove.

EUR/GBP: holding tight ranges, but bottom looks well protected

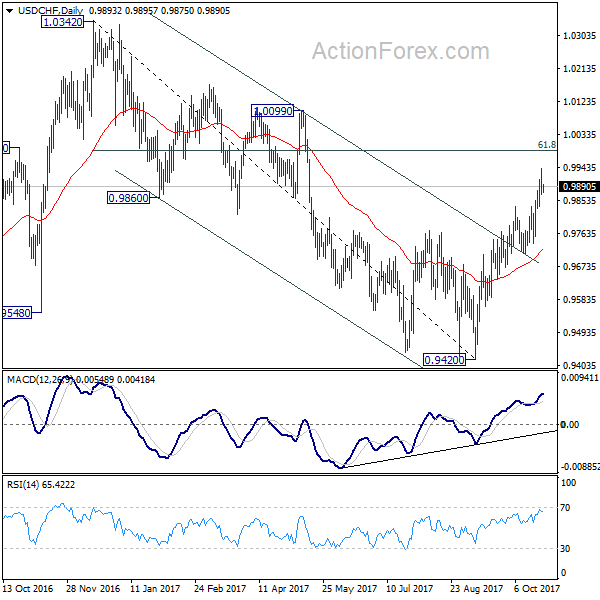

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9864; (P) 0.9901; (R1) 0.9934; More....

A temporary top in place at 0.9939 and intraday bias is turned neutral first. Near term outlook remains bullish as long as 0.9736 support holds. Above 0.9939 will target 61.8% retracement of 1.0342 to 0.9420 at 0.9990. Sustained break there will pave the way to retest 1.0342 high. However, firm break of 0.9736 support will dampen our bullish view and suggest that rebound from 0.9420 is completed.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could develop into a medium term move and target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9587 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.