Sample Category Title

US Earnings And BoC Decision Eyed On Wednesday

- US futures flat as 10% of S&P 500 prepares to release earnings;

- BoC unlikely to raise rates for third consecutive meeting;

- Sterling pops higher as UK GDP raises rate hike expectations;

- Euro higher as German business optimism hits record high.

US futures are mixed ahead of the open on Wednesday, a day after only the Dow managed to make fresh record highs while the others made only marginal gains.

Both the S&P 500 and the Nasdaq failed to replicate the moves in the Dow on Tuesday, having also come off more heavily on Monday, but they continue to trade around record high levels. The key focus for the indices this week continues to be corporate earnings, with a tenth of the S&P 500 due to report on the third quarter today. Visa, Boeing and Coca-Cola are among those that are scheduled to report before the market open.

BoC Unlikely to Raise Rates for Third Consecutive Meeting

There will be some economic data to accompany the earnings reports on Wednesday, which has not and will not be the case for much of the week. US core durable goods orders – an important economic report offering insight into both current performance and expectations – will be released shortly before the open while new home sales will come a little later on. We'll also get the latest monetary policy decision from the Bank of Canada today, although a third consecutive rate hike is not expected.

Sterling Pops Higher as UK GDP Raises Rate Hike Expectations

Preliminary data released on Wednesday showed the UK grew by 0.4% in the third quarter – 1.5% on an annual basis – ahead of market expectations and, more importantly, above what the Bank of England had anticipated. This is a very important point as the central bank had previously claimed that as long as the economy performs in line with expectations, it would likely raise interest rates at an upcoming meeting and today's GDP data exceeded expectations, leaving the BoE with little reason not to proceed. It's also the final major data release ahead of next week's meeting leaving little opportunity for data to convince policy makers otherwise.

The only hope for those that believe it would be a mistake to raise interest rates given the uncertain economic outlook, is the fact that not all policy makers are behind such a move. With inflation having not risen above 3% last month, there is a possibility that policy makers wait a little longer before taking the decision. That said, the central bank could come in for some criticism if it doesn't follow through on warnings now, with market having now priced in an 83% chance of a hike next week. The pound rallied on the back of this morning's data, in line with the increased rate hike expectations, to trade around 1.32 against the dollar, which ultimately weighed on the FTSE 100, the only major index in Europe to trade in the red.

Euro Higher as German Business Optimism Hits Record High

The euro has also been given a small boost this morning after the German Ifo survey for October recorded its highest ever reading, with optimism about the months ahead contributing significantly to the spike. While Germany was once seen as the engine of growth for the entire euro area, it seems businesses have become increasingly confidence in the broader recovery this year which has created an environment in which the economy can prosper.

While the recovery in the eurozone has stood out this year, the global economic outlook is generally looking much better and the improved performance elsewhere – particularly China – is likely also feeding into the optimism. While there remains a number of underlying risks in the economy, there is a belief that momentum is growing and stronger growth could lie ahead, although should these risks begin to resurface, it may not take much to rattle investors and the business community.

Euro Pauses After Slide As German Business Climate Sparkles

The euro is unchanged in the Wednesday session, after two losing sessions. Currently, EUR/USD is trading at 1.1766, up 0.07% on the day. On the release front, German Ifo Business Climate continued to accelerate with a reading of 116.7, well above the forecast of 115.3 points. In the US, Core Durable Goods Orders is expected to improve to 0.5%, while the Core Durable Goods is forecast to slow to 1.0%. As well, US New Home Sales is expected to dip to 555 thousand. On Thursday, the ECB publishes its rate statement, and the US will release unemployment claims and Pending Home Sales.

The German economy continues to fire on all cylinders, with much of the credit going to a robust manufacturing sector. The global appetite for German exports remains strong and consumer spending has been steady. On Tuesday, German Manufacturing PMI posted a strong reading of 60.5, beating expectations. There was more positive news on Wednesday, as German Ifo Business Climate jumped to 116.7, an all-time high. This thumbs-up from the business confidence suggests that the German economy will enjoy a strong fourth quarter.

Spain’s constitutional crisis has been on simmer all week, but the temperature could rise dramatically on Friday, when the Spanish Senate steps into the fray. The Senate is expected to authorize the central government to invoke Article 155 of Spain’s constitution and apply direct rule over Catalonia. This would allow Madrid to dismiss the Catalan government and take control of the regional police and radio and television stations. This drastic clause has never been invoked, and it remains unclear what steps the central government will take under Article 155. Another question mark is how the Catalan parliament will respond. Catalan President Carles Puidgemont has so far avoided explicitly declaring independence from Spain, but could choose to pre-empt a move by the central government to remove him from office. The continuing uncertainty could lead to further unrest and instability. Still, Caixabank, the third largest bank in the country, does not expect the Catalonia issue to affect Spain’s GDP, which the bank projects will expand 2.7 percent in 2018.

European Futures Cautious | Countdown On For US Tax Bill | Aussie And Sterling Touched Another Low

The Aussie dollar is one of the major loser among currencies

Investors are largely expecting the ECB would enlighten the markets with more details

The countdown is on for the introduction of the US tax bill

Investors over in Europe are cautious as the Asian indices posted a narrow session. The Aussie dollar is one of the major loser among currencies because of the poor economic data reading. The consumer price index data was much softer than anticipated and printed the reading of 1.8 percent versus the forecast of 2 percent- a number which made investors to push the currency to its lowest level since July.

Between today and tomorrow, the event which is going to get the most amount of spotlight would be the upcoming European Central Bank’s meeting. Investors are largely expecting that the bank would enlighten the markets with more details on the tapering of their quantitative easing program. Just how much the cautious tone would be by the president of the European Central Bank will remain the key point. The bank is still far off from achieving its inflation target of 2 percent. We expect the bank to adopt a very balanced tone tomorrow and it would remain very accommodative.

Over in the US, it is all about the US tax reform and the spat between president Trump and the Republicans remain the attention. The countdown is on for the introduction of the tax bill and House Republicans are expected to make an announcement by November 1st. The record highs for the stock market over in the US is fuelled by two elements; the US tax reforms and the sturdy quarterly earning reports. The rally would lose its mojo if any of these starts to lose steam.

Of course, the hopes around the US tax reforms are supporting the dollar index but the other major pillar is the choice for the next chairperson of the Federal Reserve bank. President Trump yesterday discussed his top two candidates with the Senate Republicans during his lunch meeting. John Taylor, the economist at the Stanford University, remains the top choice.

Talking about Sterling, nothing is working for the currency. Currently, it is mainly the negative sentiment around Brexit negotiations and uncertainty over the Bank of England’s decision on its interest rate which is keeping the currency in the dark spot. It is trading at its worst level in nearly two weeks and the picture doesn’t seem be brightening up anytime soon.

Technical Outlook: Spot Gold Extends Weakness On Speculation Of Hawkish New Fed Chair

Spot Gold extends weakness on Wednesday following previous day’s close in red and action in past two days being capped by thick daily cloud which weighs on near-term action.

Eventual firm break below daily cloud after several unsuccessful attempts and close below next pivot at $1277 ( Fibo 61.8% of $1260/$1306 upleg) were strong bearish signals for extension of bear-leg from $1306 high.

The yellow metal came under increased pressure amid speculations of more hawkish new Fed Chair, as candidate John Taylor is seen as most likely replacement for Janet Yellen.

Fresh weakness met next target at $1271 (Fibo 76.4%) and shows scope for stretch towards key supports at $1260 (06 Oct low) and $1258 (200SMA).

Today’s close below broken 100SMA ($1275) is needed to generate another bearish signal.

Broken daily cloud base marks key near-term resistance at $1281.

Res: 1275, 1277, 1281, 1283

Sup: 1271, 1266, 1260, 1258

CRUDE OIL Consolidating

Crude oil is consolidating within range defined by support at 50.43 and the strong resistance lies at 52.86 (28/09/2017). Expected to show continued increase within this range.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Further Weakness

Silver is again grinding lower. Hourly support can be founds at 16.88. Hourly resistance is given at 17.46 (13/10/2017 high). Additional support can be found at 16.13 (06/10/2017 low).

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Weak Support Breaks

Gold remains weak. The precious metal is located within a downtrend channel. The broken support at 1284 confirms an underlying bearish trend. Strong support lies at a distance at 1267 then 1204 (10/07/2017 high). Resistance is now located at 1288 (20/10/2017).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Fading Bullish Momentum

Bitcoin remains weak as long as prices remains below the key resistance at 6063. Strong support stands very far at 2975 (22/08/2017 low). However with rising trend unbroken road is wide open for further bullish momentum. Support can be located at 5325 (rising trendline). In the short-term, the digital currency should monitor $6000.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.

EUR/CHF Rising Towards The Trend Resistance At 1.1664

EUR/CHF recovery bounce continues testing key resistance at 1.1664 (rising trend line). Support is given at 1.1388 (02/09/2017 low). Rising channel suggest further bullish momentum.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

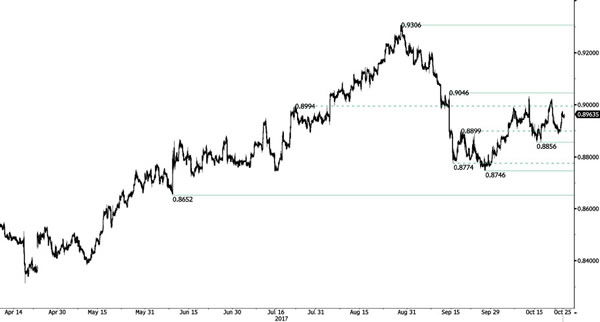

EUR/GBP Bouncing

EUR/GBP is showing increasing short-term buying interest near the weak support at 0.8899 (19/09/2017 low). However, as long as prices are below the resistance at 00.9046 (05/09/2017 high), the shortterm technical structure is biased to the downside Hourly support is given at a distance at 0.8746 (27/09/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).