Sample Category Title

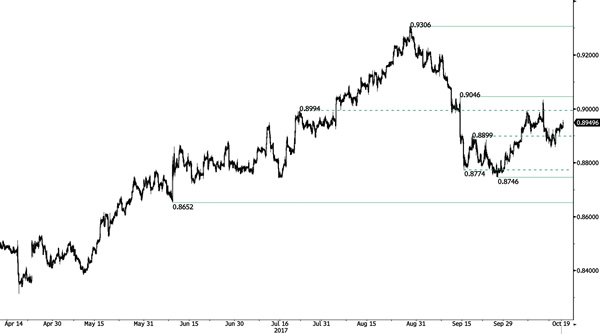

EUR/GBP Recovery Bounce

EUR/GBP continues to bounce higher yet not important resistances have been broken. The pair is back below former resistance at 0.8899 (19/09/2017 low). Hourly support is given at a distance at 0.8746 (27/09/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

AUD/USD Bouncing

AUD/USD recovery has been weak indicating further downside risk. Hourly resistance is given at 0.7897 (13/10/2017 high). Support lies at at 0.7786 then 0.7733 (06/10/2017 low). Expected to show continued consolidation.

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Reversal Within Channel

USD/CAD continues to bounce within uptrend channel. Strong support is located at a distance at 1.2062 (08/09/2017 low). Hourly support lies at 1.2331 (26/09/2017 high). Resistance is given at 1.2663 (31/08/2017 high). Expected to show continued short-term bullish pressures within uptrend channel.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head further lower.

USD/CHF Recovery Bounce Losing Momentum

USD/CHF has failed to test resistance 0.9838. Hourly support stands at 0.9712 (12/10/2017 low). The technical structure suggests an improving short-term buying interest. Expected to show continued bullish pressures within uptrend channel.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/JPY Bullish Momentum Gaining

USD/JPY is preparing to challenge resistance at 113.26. Strong hourly resistance is given at 113.44 (06/10/2017 high). Support is located at 111.12 (20/09/2017 low). However downside risks are definitely rising as markets are now taking some short-term profit after the strong increase during September,

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Weak Recovery Bounce

GBP/USD is weakening and is now close to the support at 1.3155. key support can be found at 1.3122 12/10/2017 low). Hourly resistance stands at 1.3338 (13/10/2017 high).

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. Long-term support can be found at 1.1841 (07/10/2017 low). Long-term resistance given around 1.35 is at stake and indicates a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Still Bouncing

EUR/USD momentum is again heading towards hourly resistance at 1.1878 (12/10/2017 high). Strong support is given at a distance at 1.1662 (17/08/2017 low). Expected to show some shortterm consolidation.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

Technical Outlook: US CRUDE OIL – Risk Of Deeper Pullback On Break Below $51.00

WTI oil fell $1 on Thursday after repeated failure to sustain break above $52.00 barrier. Probes above $52.00 were repeatedly rejected in past few days with stronger indecision signal and possible rally stall being generated in double Doji in past two days.

Techs also support scenario of reversal as slow stochastic reversed from overbought territory on daily chart and daily RSI turned south, moving also below its 7d moving average.

Dips is so far holding above pivotal $51.00 support zone (Fibo 38.2% of $49.09/$52.35 upleg / converged 10/20SMA’s), with sustained break here needed to signal deeper pullback and expose Fibo supports (50% and 61.8%) at $50.72 and $50.34 respectively.

On the other side, fundamentals remain firm and supportive for further advance as oil sectors is nearing rebalancing after long period of oversupply which depressed oil prices, concerns about output disruption from Iraqi oilfields has faded and US crude stocks fell for the fourth consecutive week.

Limited downside action is needed to keep focus at the upside for final attack at key $52.84 barrier (28 Sep high).

Res: 52.16, 52.35, 52.84, 53.18

Sup: 51.00, 50.72, 50.34, 50.00

Technical Outlook: USDJPY Pulls Back On Safe-Haven Buying

The pair was sharply lower on Thursday, pulling back after renewed probe above 113.00 barrier, which was dented on Wednesday’s strong rally.

Fresh weakness comes in reaction on sharp fall of Japanese stocks, triggered by latest rising uncertainty over Catalonia, which sparked fresh safe-haven buying.

Pullback found footstep at 112.57 (Fibo 38.2% of 111.65/113.14 upleg) but deeper pullback cannot be ruled out if situation in Catalonia deteriorates.

Break below 112.57 and converged 10/20SMA’s at 112.43 would generate stronger bearish signal and risk further downside.

Wednesday’s low at 112.13 marks next pivotal support, loss of which would risk fresh attack at key 200SMA support (111.74).

Conversely, extended consolidation ahead of final attack at key 113.25/43 barriers could be expected while pullback stays limited.

Res: 113.14, 113.25, 113.43, 114.00

Sup: 112.57, 112.43, 112.13, 111.85

The 19th CCP Congress – A Summit For Xi To Crown Himself

Predominantly the most important political event in China, the twice-in-a-decade National Congress of the Chinese Communist Party began on October 18. As a kick start, President Xi delivered a Party Work Report which reviewed the achievements in his first five years and outlined the challenges and goals for the next five years and beyond. Xi outlined his thoughts on the 'new era of socialism with Chinese characteristics' On the economic reform, he suggested further developments in the "advanced manufacturing industry", which includes medium and high end consumption, green and low carbon industry, sharing economy, modern logistics and human capital services. He has also pledged to deepen interest rate and exchange rate reforms, develop a comprehensive financial regulation system and reduce systematic financial risk. These are nothing new as the key aspects of the monetary and fiscal policies have already been lain down at the National Financial Work Conference in July.

Xi's Power Consolidation

There are several events that worth attention in the following days. Yet, we believe the focus of the week-long Congress is on consolidation of Xi Jinping's power. The Central Committee would be elected at the end of the Congress, likely on October 24. This would be followed by the first Central Committee Plenary session for election of the Politburo members (25 members) and the 7-member Politburo Standing Committee (the top leadership for the coming 5 years). The name list would be announced on October 25. Since he has become the General Secretary of the Central Committee of CCP in 2012 and the 7th Chinese President in 2013, Xi has been removing personnel he deemed disloyal using the reason of cracking down corruption. Undoubtedly, Xi's cabinet would be composed of his loyalists so that he would cling to absolute power. To further cement his power, the authoritarian party would discuss amendment of the constitution at the summit. This is expected to incorporate 'Xi's thought' in the constitution and Xi would be named the 'party chairman', a title never been used after Mao Zedong.

Dataflow Surprisingly Strong During Sensitive Moment

The macroeconomic data released over the past weeks have been positive. GDP expanded +6.8% y/y in 3Q17, in line with expectations but decelerated from +6.9% in the prior quarter. For the month of September, retail sales grew +10.3% y/y, beating consensus of +1.2% and August's +10.1%. Urban fixed asset investment grew +7.5% y/y in the first 9 months of the year, moderating from +7.8% in the year through to August. The market had anticipated a growth of +7.7%. IP growth accelerated to +6.6% y/y in September, from +6% in the prior month. This came in better than expectations of +6.4%. During the weekend, the government released the inflation data. CPI eased to +1.6% y/y in September from +1.6% a month ago. This came in line with expectations. PPI, however, accelerated to +6.9% y/y, from +6.3% in August. The market had anticipated a mild improvement to +6.4%. The set of data is of particular political importance during this period of time. A strong set of data allows Xi to cement his power and claim that his thoughts/ theories are at work to building a 'strong' and 'new era' of China.