Sample Category Title

GBP/USD: UK Claimant Count Change

The Sterling was suffering the third straight day of weakness against the US Dollar on mixed job data for Britain yesterday morning. On the report, GBP/USD fell 28 pips or 0.21% to the 1.3159 mark, though the currency pair managed to return into the green area, offsetting losses to start Thursday session near the 1.3220 mark.

The Office for National Statistics' release showed that unemployment claims rose more than estimated by 1.7K in August, while the jobless rate remained unchanged at 4.3% in the same period. Relatively robust employment picture fell short to be translated into strong pay growth, which continued to squeeze the UK consumers and complicated the BoE plans to make interest rate hike.

Asian Equities Flat As China’s GDP Met Expectations

Equities across the Asian markets were trading in a tight, narrow range on Thursday, ignoring solid Chinese data and the new records on Wall Street, where the Dow Jones Industrial Average breached 23,000. FX markets are also struggling for direction, as traders look for signals from E.U. politics, and signs for who will lead the Federal Reserve.

China's economic growth meets expectations

China's GDP expanded 6.8% in the third quarter, slightly below the previous period of 6.9%, but still well above the full-year target of 6.5%. At the beginning of 2017, most of the discussion about the Chinese economy was a "soft vs. hard landing". However, the economy continues to grow at healthy levels, despite the government shifting the focus on the quality of growth vs. quantity. This gives Xi Jinping more leverage, as he seeks to grab greater power over the next five years. In other economic releases, retail sales and industrial production both beat expectations, coming at 10.3% and 6.6%, respectively. Meanwhile, investment growth dipped to 18-year low.

Will Rajoy trigger Article 155?

Euro traders are waiting to see whether Prime Minister Mariano Rajoy will trigger Article 155, if Catalan President, Carles Puigdemont, does not clarify what he meant in his speech last week. The deadline is 08:00 GMT, so expect to see some volatility in the Euro as the European trading session kicks off. It is still unclear how this story will develop, but triggering Article 155 would likely lead to the declaration of independence, and this is will undoubtedly be negative news for the single currency.

U.K. retails sales and E.U. summit

U.K. retail sales is the only tier one economic release in Europe today. Despite falling real wages, spending remained robust in the previous months. Economists expected retail sales to fall 0.1% last month, but figures from the British Retail Consortium, showed that like-for-like sales grew 1.9% in September, thus we can expect an upside surprise in today's release. However, this does not necessarily mean Sterling will rally. Brexit concerns will likely remain the primary driver when E.U. leaders meet later today. The probability of "no-deal" is increasing, and investors should be prepared for the worst. A hard Brexit scenario will not only drag Sterling lower, but it will also probably take European indices with it.

Dow above 23,000, despite Mnuchin warnings

U.S. Treasury Secretary Steve Mnuchin has warned that stocks will fall significantly, if Congress doesn't pass tax reforms. Maybe he's right. The Dow Jones Industrial Average and S&P 500 rallied more than 25% and 20%, respectively, and it's doubtful that this rally was only based on economic growth and earnings expectations. It seems the odds of tax reforms occurring this year, or in the first quarter of 2018 are 50/50, so risks are broadly symmetrical.

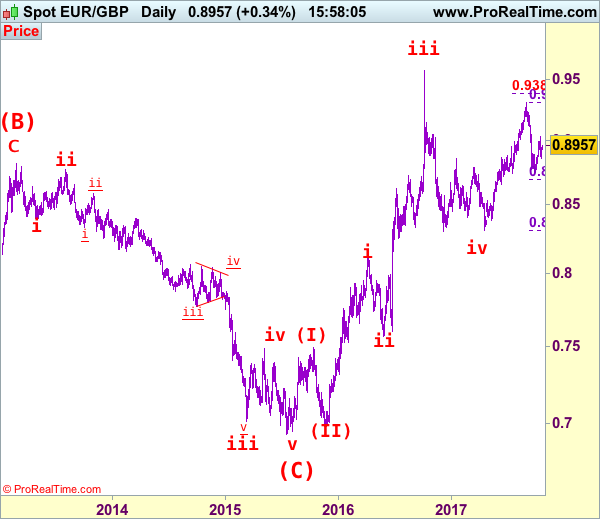

EUR/GBP Elliott Wave Analysis

EUR/GBP – 0.8955

Although the single currency retreated after running into resistance at 0.9033, as low has been formed at 0.8746 late last month, reckon downside would be limited to 0.8850-55 and bring another rebound later, above said resistance at 0.9033 would add credence to this view, bring a stronger rebound to 0.9050-60 and possibly 0.9080, having said that, reckon upside would be limited to previous support at 0.9115-20 and price should falter well below resistance at 0.9203, bring another decline later this month.

Our latest preferred count is that the wave V of a 5-wave series from 0.5682 ended at 0.9805 earlier and major from there has possibly ended at 0.8067 as A-B-C-X-A-B-C. We are keeping our view that the entire correction from 0.9805 has possibly ended at 0.7756 and as labeled as the attached daily chart and impulsive move from 0.9084 has ended at 0.6938 as a 5-waver which marked as the (C) wave, recent impulsive rise is labeled as (I) (II), (i) (ii) series, indicated upside target at 0.9084 had been met, the retreat from 0.9576 suggest wave iii ended there and next upside target for wave v of (III) should head towards 0.9700 but price should falter well below parity .

On the downside, expect downside to be limited to 0.8900 and 0.8850-55 should hold, bring another rebound later. Below 0.8800-05 would suggest the rebound from 0.8746 has ended instead, bring weakness to 0.8770-75, break there would confirm and bring retest of 0.8746, once this support is penetrated, this would signal the decline from 0.9307 top has resumed for correction of early uptrend to 0.8690-95 (61.8% Fibonacci retracement of 0.8312-0.9307) and possibly towards previous support at 0.8652.

Recommendation: Hold long entered at 0.8880 for 0.9080 with stop below 0.8780

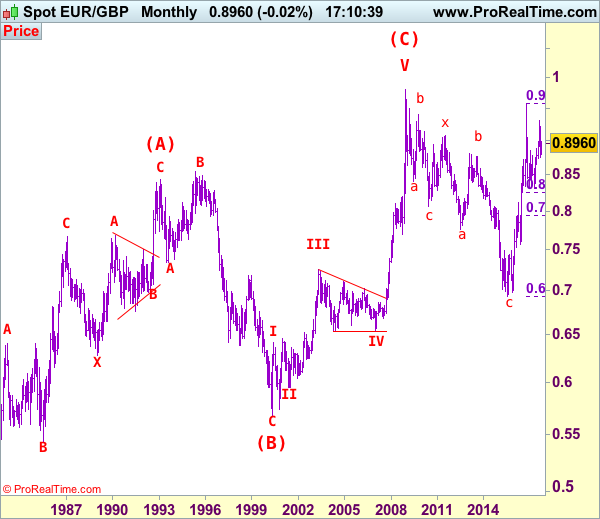

Euro's long term uptrend started in Feb 1981 at 0.5039 and is unfolding as a (A)-(B)-(C) move with (A): 0.8433 (Feb 1993), (B): 0.5682 (May 2000) and impulsive wave (C) should have ended at 0.9805 with wave III ended at 0.7254 (May 2003), triangle wave IV at 0.6536 (23 Jan 2007) and wave V as well as wave (C) has ended at 0.9805.

We are keeping an alternate count that only wave III ended at 0.9805 and the correction from there is the wave IV and has possibly ended at 0.6936, however, it is necessary to see a daily close above resistance at 0.9576 in order to change this to be the preferred count.

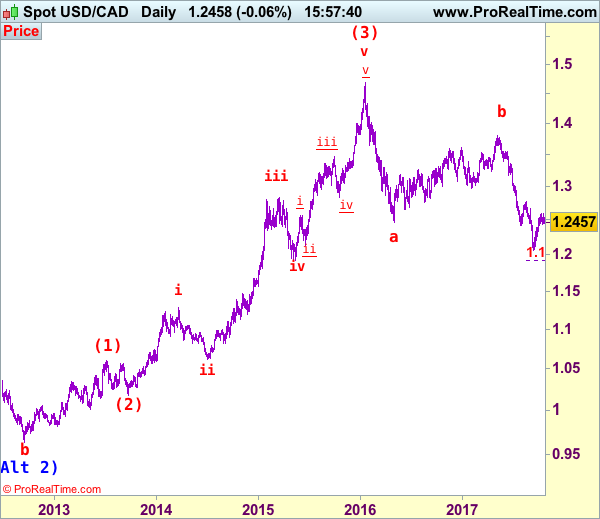

USD/CAD Elliott Wave Analysis

USD/CAD – 1.2460

Although the greenback continued trading with a relatively firm undertone after rebounding to 1.2599 earlier this month, a break of this level is needed to signal the corrective rise from 1.2061 low is still in progress for retracement of recent downtrend, then mild upside bias is seen for further gain towards resistance at 1.2663 but loss of near term upward momentum should limit upside to 1.2700-10 and price should falter well below resistance at 1.2778, bring retreat later.

We are keeping our view that the wave b from 1.0657 (a leg top) has possibly ended at 0.9633 with (a): 0.9800, wave (b): 1.0447 and wave c at 0.9633, the subsequent rise from there is now treated as wave c exceeded indicated upside target at 1.3770-80 and 1.4000 and wave (3) has possibly ended at 1.4690 and wave (4) correction has commenced for retracement back towards 1.2000.

On the daily chart, our latest preferred count remains that the A of (B) rally from 0.9059 low (7 Nov 2007) unfolded into an impulsive wave with i: 0.9059-1.0380, ii ended at 0.9819, iii at 1.3019 followed by triangle wave iv at 1.2026 , then wave v formed a top at 1.3066 and also ended the wave A. The wave B is unfolding as an double three a-b-c-x-a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c at 1.0784, followed by wave x at 1.1725, another set of a-b-c unfolded with 2nd a at 0.9931, 2nd b at 1.0674. the 2nd c has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3900 had been met and gain to 1.4700 would follow.

On the downside, whilst initial pullback to 1.2433, then 1.2400 cannot be ruled out, reckon downside would be limited to support at 1.2336 and if our view that low has been formed at 1.2061 is correct, renewed buying interest should emerge around support at 1.2254 and bring another rebound later. Only a daily close below said support at 1.2254 would suggest the rebound from 1.2061 has ended, bring test of another previous support at 1.2197 first. We are keeping our bearish count that wave b ended at 1.3794 and wave c has commenced for further fall towards psychological support at 1.2000.

Recommendation: Buy at 1.2255 for 1.2555 with stop below 1.2155.

Longer term - The selloff from 1.6194 (21 Jan 2002) to 0.9059 (07 Nov 2007) is viewed as (A) wave which is a 5-waver as labeled on the monthly chart as below, the subsequently rally is labeled as (B) with impulsive A leg of (B) ended at 1.3066, wave B of (B) is unfolding which has either ended at 0.9407 or would extend one more fall but downside should be limited to 0.9200 and 0.9000 should hold.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

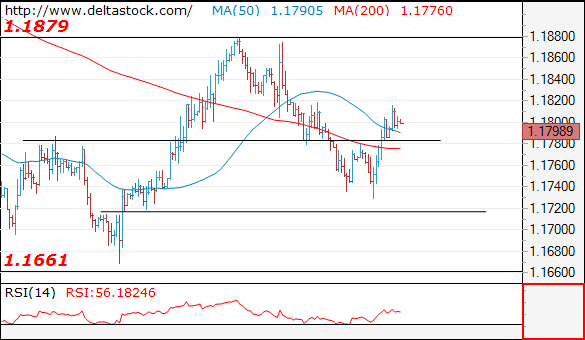

EUR/USD

Current level - 1.1798

The intraday bias is positive above 1.1780 static support, but my outlook is rather counter-trend, for a reversal and another downswing towards 1.1720 target mark.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1820 | 1.1940 | 1.1780 | 1.1660 |

| 1.1880 | 1.2030 | 1.1720 | 1.1480 |

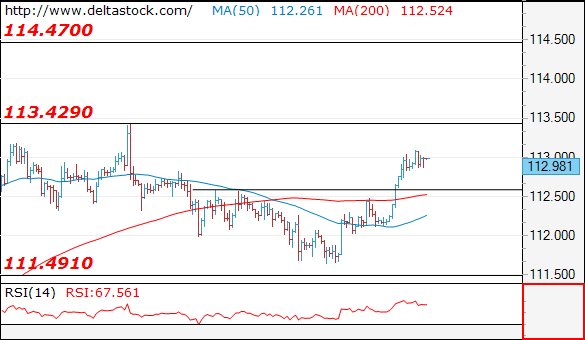

USD/JPY

Current level - 112.98

The bias remains positive, for a rise towards 113.40, en route to 114.50. Key support lies at 112.60.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 113.40 | 114.50 | 112.60 | 111.00 |

| 114.50 | 114.50 | 111.50 | 107.30 |

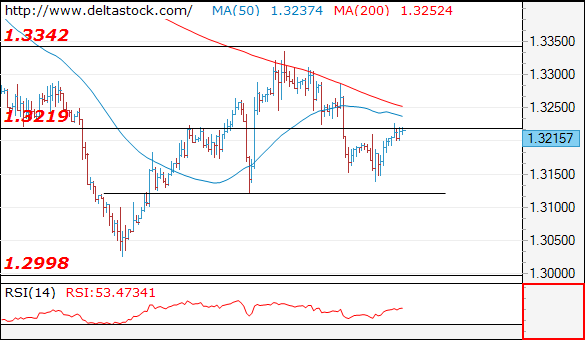

GBP/USD

Current level - 1.3215

Still in the consolidation range between 1.3220 and 1.3120 and I favor a break on the downside, towards 1.3000 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3220 | 1.3340 | 1.3220 | 1.2910 |

| 1.3340 | 1.3650 | 1.3120 | 1.2760 |

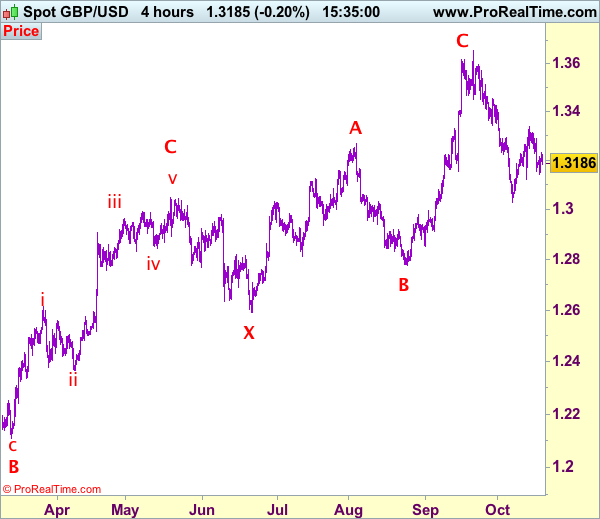

Trade Idea: GBP/USD – Hold short entered at 1.3315

GBP/USD – 1.3192

Original strategy :

Sold at 1.3315, Target:1.3115, Stop: 1.3290

Position: - Short at 1.3315

Target: - 1.3115

Stop: - 1.3290

New strategy :

Hold short entered at 1.3315, Target:1.3115, Stop: 1.3290

Position: - Short at 1.3315

Target: - 1.3115

Stop:- 1.3290

Although cable found support at 1.3140 yesterday and recovered, if our view that top has been formed at 1.3338 late last week is correct, upside should be limited and price should falter well below indicated resistance at 1.3287 and bring another decline to 1.3140, then test of indicated support at 1.3121, however, break there is needed to signal the rebound from 1.3027 has ended, bring further fall to 1.3065-75, then retest of said support at 1.3027.

In view of this, we are holding on to our short position entered at 1.3315. Only above indicated resistance at 1.3312-15 would risk test of said resistance at 1.3338 (last week’s high), break there would abort and signal low has been formed at 1.3027 instead, bring at least a correction of the fall from 1.3658 top to 1.3390-00 later. Our preferred count is that (pls see the attached chart) the wave IV is unfolding as a complex double three (ABC-X-ABC) correction with 2nd wave B ended at 1.2774, hence 2nd wave C could have ended at 1.3658.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

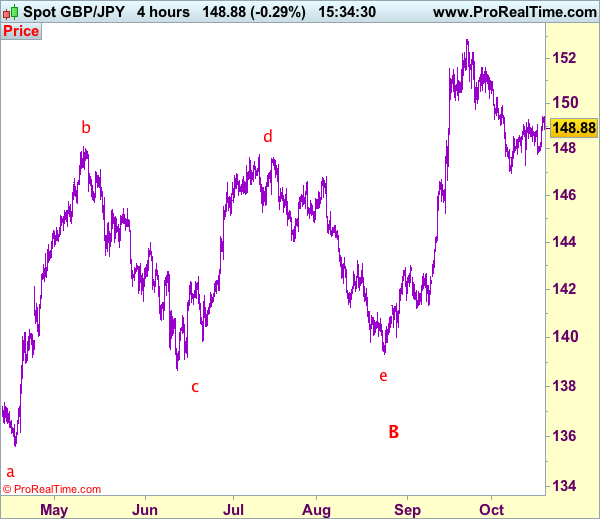

Trade Idea: GBP/JPY – Stand aside

GBP/JPY - 148.82

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Despite intra-day marginal rise to 149.44, lack of follow thorough buying and current retreat suggest consolidation would be seen and pullback to 148.40-45 cannot be ruled out, however, reckon downside would be limited to 148.00 and support at 147.80 should hold, bring further consolidation. Above said resistance at 149.44 would signal the erratic rise from 146.95 is still in progress for retracement of the fall from 152.85 to 149.90-00 and possibly test of resistance at 150.25 but still reckon upside would be limited to 150.90-00 and bring another decline later.

On the downside, only a break below said support at 147.78 would shift risk to downside and signal the rebound from 146.95 has ended, bring weakness to another previous support at 147.30, below would confirm and then retest of 146.95 would follow. Looking ahead, once this level is penetrated, this would confirm the fall from 152.85 top has resumed for retracement of recent upmove to 146.60-65 and then 146.00, having said that, loss of momentum should limit downside and previous support at 145.25 should remain intact.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

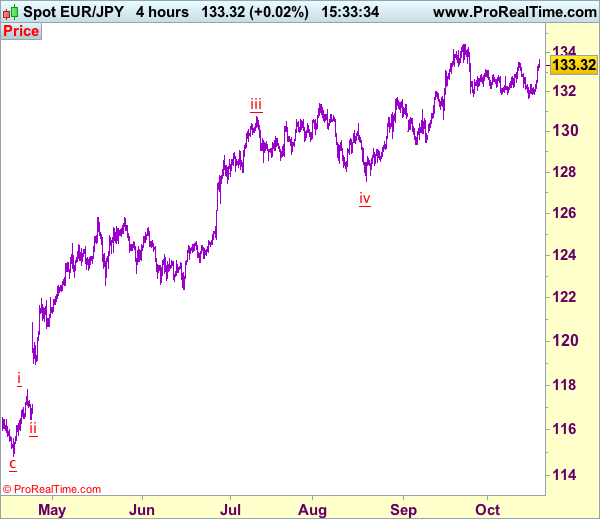

Trade Idea: EUR/JPY – Stand aside

EUR/JPY - 133.21

Original strategy:

Sold at 132.90, Target: 130.90, Stop: 133.50

Position: - Short at 132.90

Target: - 130.90

Stop: - 133.50

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Euro’s rise from 131.66 turned out to be much stronger than expected and indicated resistance at 133.50 was penetrated, dampening our bearishness and upside risk remains for further gain to 133.90-00, however, only break of previous resistance at 134.41 would confirm early upmove has resumed and extend headway to 135.00-10 and later towards 135.50-60.

In view of this, would not chase this rise here and would be prudent to stand aside for now. below 132.50-60 would suggest the rebound from 131.66 has ended instead, bring weakness to previous resistance at 132.38 but only break there would add credence to this view and revive bearishness for weakness to 132.00, then test of 131.84 support but said support at 131.66 should hold from here.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

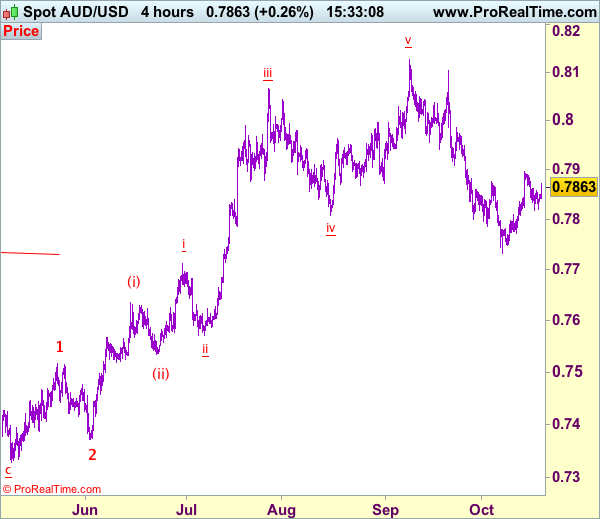

Trade Idea: AUD/USD – Hold short entered at 0.7875

AUD/USD – 0.783365

Original strategy:

Sold at 0.7875, Target: 0.7700, Stop: 0.7900

Position: - Short at 0.7875

Target: - 0.7700

Stop:- 0.7935

New strategy :

Hold short entered at 0.7875, Target: 0.7700, Stop: 0.7890

Position: - Short at 0.7875

Target: - 0.7700

Stop:- 0.7890

Aussie found support at 0.7818 and has rebounded again today, suggesting caution on our short position entered at 0.7875 but as long as indicated resistance at 0.7897 (last week’s high) holds, prospect of another retreat remains, below said support at 0.7818 would retain bearishness and bring weakness to 0.7800, break there would add credence to our view that top has been formed at 0.7897, bring test of 0.7770-75, then retest of said support at 0.7733, below there would signal recent fall from 0.8125 top has resumed for weakness to 0.7700-10 and later towards 0.7660-65.

In view of this, we are holding on to our short position entered at 0.7875. Only above previous support at 0.7908 (now resistance) would defer and risk a stronger rebound to 0.7950 but resistance at 0.7986 should remain intact and bring another decline later.

On the 4-hour chart, recent upmove from 0.7329 is unfolding as an impulsive rise with wave 3 as well as smaller degree wave (iii) extending, only minor wave v of (iii) has ended at 0.8125, hence bullishness remains for this move to extend headway to 0.8200, then towards 0.8300, however, reckon upside would be limited to 0.8400 and the final wave 5 should falter below 0.8500, bring correction later.

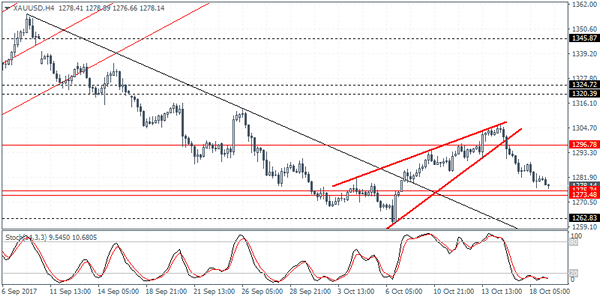

XAUUSD Intraday Analysis

XAUUSD (1287.14): Gold prices were seen extending the declines yesterday as price approaches the support level of 1275 - 1274. The declines come following the breakdown from the rising wedge pattern and the test of support will complete the measured move. From the support level, gold prices could be seen establishing support which could see an upside bounce in prices. Resistance at 1296 will be in focus as a result, and a breakout above this resistance level is required to post further gains.