Sample Category Title

AUDUSD Intraday Analysis

AUDUSD (0.7850): The AUDUSD was seen giving back the gains yesterday and today's price action saw prices rallying briefly. With the breakout from the falling median line, we do expect AUDUSD to push higher. However, in the near term, the downside could see prices retesting the recently broken resistance level at 0.7800. Establishing support at this price level could potentially signal a correction to the upside with 0.7957 as the eventual target. In the event that the support fails to hold near 0.7800, the bias will shift to the downside with AUDUSD likely to post further declines.

EURUSD Intraday Analysis

EURUSD (1.1798): The EURUSD managed to close on a bullish note as the common currency was seen pushing to make further gains in the early trading session today. Price action managed to recover most of the declines in the past days as the EURUSD approaches the key resistance level of 1.1822. However, as long as price action is subdued below this resistance level, the bias remains to the downside. Support at 1.1720 will be a key level for the EURUSD. A breakdown below this level could suggest further declines. However, we expect the sideways range to be maintained in the near term.

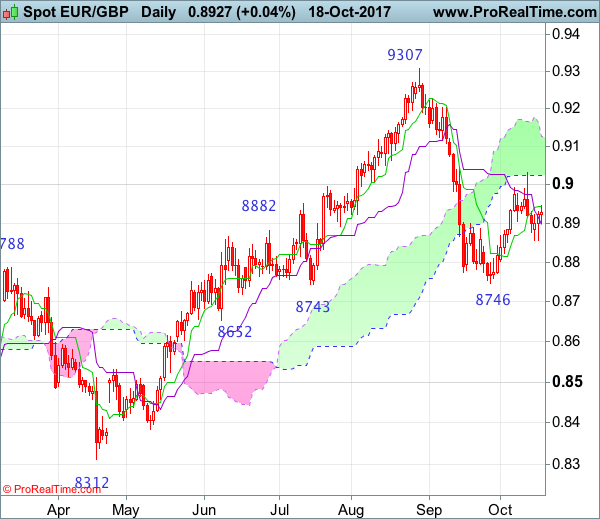

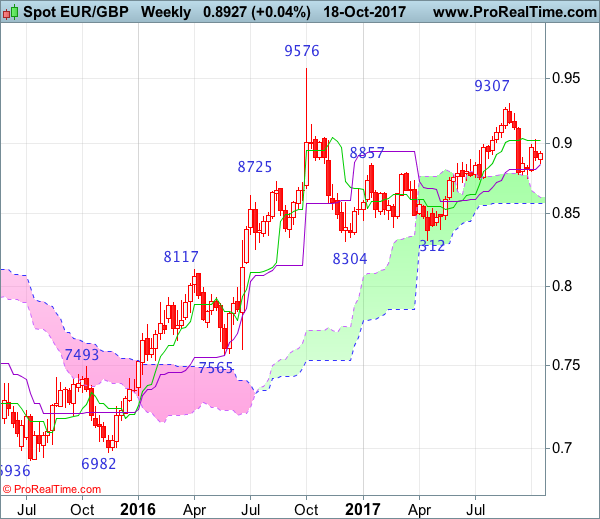

EUR/GBP Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: N/A

• ime of formation: N/A

• Trend bias: Near term up

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 29 Aug 2017

• Trend bias: Down

EURGBP – 0.8954

Although the single currency rose to as high as 0.9033 late last week, the subsequent retreat suggests top is possibly formed there and consolidation with mild downside bias is seen for weakness to 0.8855-60, then towards 0.8800 but break of latter level is needed to signal the rebound from 0.8746 has ended, bring retest of this level later. Looking ahead, only a drop below 0.8746 would signal early fall from 0.9307 top has resumed and extend weakness towards 0.8690-95 (61.8% Fibonacci retracement of 0.8312-0.9307) but previous support at 0.8652 would hold.

On the upside, whilst initial recovery to 0.8990-00 cannot be ruled out, reckon said resistance at 0.9033 would cap upside and bring further consolidation. Only break there would suggest a temporary low has been formed at 0.8746, bring a stronger rebound to 0.9050-60, however, reckon upside would be limited to 0.9110-15 and as top has been formed at 0.9307, reckon upside would be limited to 0.9150 and price should falter below 0.9203, bring another leg of corrective decline later this month.

Recommendation: Stand aside for this week.

On the weekly chart, despite last week’s brief bounce to 0.9033, the subsequent retreat formed a black candlestick with a long upper shadow (a shooting star alike), suggesting the recovery from 0.8746 has possibly ended there and consolidation with mild downside bias is seen for weakness to 0.8800-05, however, break there is needed to signal another leg of decline from0.9307 top is underway for test of said support at 0.8746, break there would bring retracement of early upmove to 0.8690-95 (61.8% Fibonacci retracement of 0.8312-0.9307) and possibly support at 0.8562 but reckon downside would be limited to the lower Kumo (now at 0.8571) and previous resistance at 0.8531 should turn into support and contain euro’s downside.

On the upside, expect recovery to be limited to 0.9000 and said resistance at 0.9033 should hold, bring further consolidation, break of 0.9033 would suggest the retreat from 0.9307 has possibly ended, bring recovery to 0.9060-70, however, if our view that top has been formed at 0.9307 is correct, upside would be limited to 0.9120-25 and price should falter well below 0.9203, bring another leg of decline later this month.

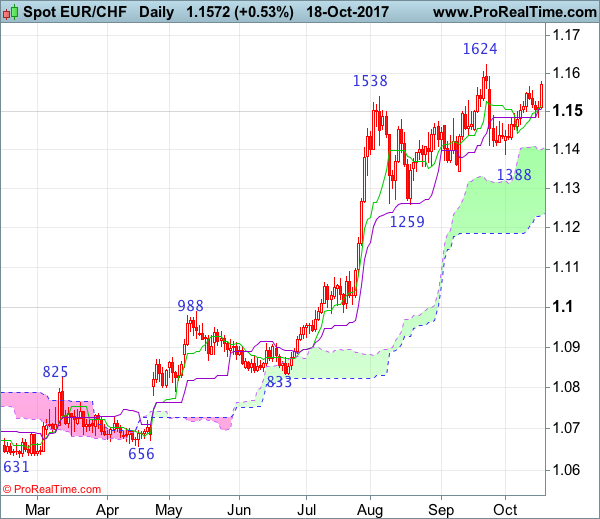

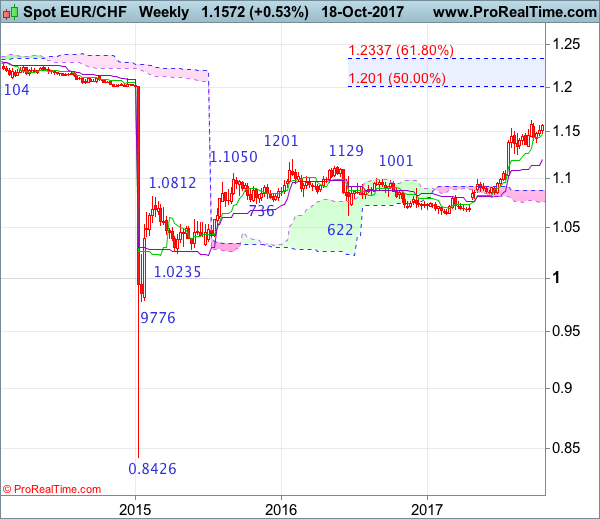

EUR/CHF Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 24 Jul 2017

• Trend bias: Up

Daily

• Last Candlesticks pattern: Morning doji

• Time of formation: 25 Jul 2017

• Trend bias: Up

EUR/CHF – 1.1570

As the single currency found renewed buying interest at 1.1485 and has risen again, suggesting near term upside risk remains for the rebound from 1.1388 to extend gain towards recent high at 1.1624, however, break there is needed to signal recent upmove has resumed and extend gain towards 1.1695-00 (61.8% projection of 1.0833-1.1538 measuring from 1.1260), having said that, loss of upward momentum should prevent sharp move beyond 1.1770-80 and reckon 1.1800-10 would hold from here, risk from there is seen for a retreat to take place later.

On the downside, below said support at 1.1485 would prolong consolidation and bring weakness to the upper Kumo (now at 1.1402), however, break of support at 1.1388 is needed to revive our bearishness and signal a temporary top has been formed at 1.1624, bring retracement of recent upmove to support at 1.1345, then towards 1.1300 but another previous support at 1.1259 should hold from here and euro shall head north again from there.

Recommendation: Exit short entered at 1.1520 for 1.1320 with stop above 1.1620.

On the weekly chart, although euro has continued edging higher after finding support at 1.1388, as long as last month’s high at 1.1624 holds, further consolidation would be seen and prospect of another retreat remains, below 1.1485 would bring weakness towards 1.1388, however, break there is needed to suggest a temporary top is possibly formed, bring test of 1.1345 support, once this level is penetrated, this would provide confirmation, bring retracement of recent rise to 1.1300, then towards another previous support at 1.1259 but price should stay above the Kijun-Sen (now at 1.1140) and bring rebound later.

On the upside, only break of said last month’s high at 1.1624 would signal the major rise from 0.8426 low has once again resumed and extend headway to 1.1695-00 (61.8% projection of 1.0833-1.1538 measuring from 1.1260), then towards 1.1760-70 but overbought condition should prevent sharp move beyond 1.1840-50 and reckon 1.1900-10 would hold from here, risk from there has increased for a retreat to take place later.

Australia Unemployment Rate Falls To 5.5%

The monthly employment report from Australia released earlier today showed that the unemployment rate fell to 5.5% in September and down from 5.6% seen the month before. In the monthly employment change, the economy was seen adding 19.8k jobs, which was higher than the estimated 14.1k. Previous month's figures were adjusted down to show 52k jobs being added, down from 54.2k.

Data from China showed that the GDP registered a 6.8% expansion in the third quarter. This was in line with estimates, and the data comes as the China party congress gets underway.

The US dollar was seen stalling after data released yesterday showed that building permits and housing starts rose less than expected.

Looking ahead, economic data includes the UK's retail sales figures which are expected to show a decline of 0.1% on the month. The US trading session will see the weekly unemployment claims followed by the Philly Fed manufacturing index.

Trade Idea : USD/CHF – Hold long entered at 0.9790

USD/CHF - 0.9806

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 0.9802

Kijun-Sen level : 0.9810

Ichimoku cloud top : 0.9784

Ichimoku cloud bottom : 0.9770

Original strategy :

Bought at 0.9790, Target: 0.9890, Stop: 0.9755

Position : - Long at 0.9790

Target : - 0.9890

Stop : - 0.9755

New strategy :

Hold long entered at 0.9790, Target: 0.9890, Stop: 0.9755

Position : - Long at 0.9790

Target : - 0.9890

Stop : - 0.9755

As dollar has retreated after rising to 0.9837 yesterday, suggesting consolidation below this strong resistance would be seen, however, reckon the upper Kumo (now at 0.9784) would limit downside and bring another rise later, above said resistance at 0.9837 would retain bullishness and confirm recent rise from 0.9421 low has resumed for headway to 0.9870 and possibly towards 0.9900.

In view of this, we are holding on to our long position entered at 0.9790. Below 0.9760 would defer and suggest the rebound from 0.9705 has ended instead, risk weakness to support at 0.9730, however, as broad outlook remains consolidative, reckon downside would be limited and said support at 0.9705 should remain intact.

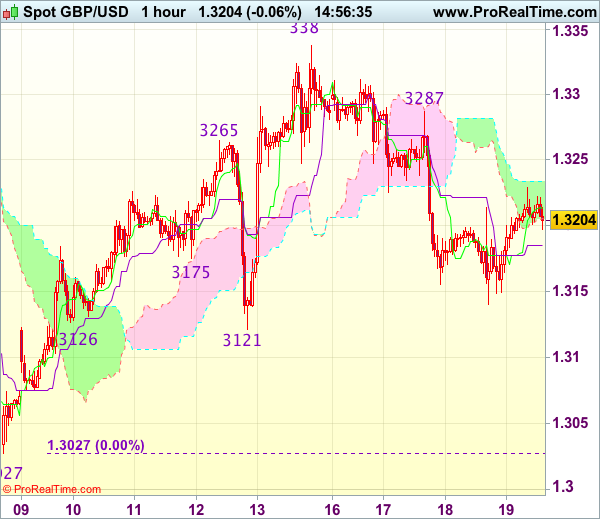

Trade Idea : GBP/USD – Sell at 1.3265

GBP/USD - 1.3197

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3210

Kijun-Sen level : 1.3185

Ichimoku cloud top : 1.3234

Ichimoku cloud bottom : 1.3204

Original strategy :

Sell at 1.3265, Target: 1.3145, Stop: 1.3300

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3265, Target: 1.3145, Stop: 1.3300

Position : -

Target : -

Stop : -

Although cable rebounded after falling to 1.3140 yesterday and consolidation above this level would be seen with initial upside bias for corrective bounce to 1.3260-70, as top has been formed earlier at 1.3338 late last week, upside would be limited and resistance at 1.3287 should hold, bring retreat later, below said support at 1.3140 would extend the fall from 1.3338 towards support at 1.3121, however, break there is needed to retain bearishness and bring further subsequent decline to 1.3090-00.

In view of this, wee are looking to sell cable on subsequent recovery as 1.3255-65 should limit upside, bring another decline later. Above said resistance at 1.3287 would abort and signal low is formed instead, bring rebound to 1.3300 and possibly test of resistance at 1.3312.

GBPUSD Bullish Above 1.3200

The British pound has moved above the 1.3200 level against the U.S dollar, hitting 1.3229 during the Asian session. GBPUSD buying demand has returned, as the U.S dollar index weakens. and intraday sellers failed to break below the 1.3140 level during yesterday's U.S session. Price-action is currently trading around the 1.3218 level, ahead of the release of UK Retail Sales data.

The GBPUSD pair is expected to advance higher while trading clearly above the 1.3200 level. Buyers are expected to target the weekly pivot point, at 1.3233 and the 1.3268 resistance area.

If intraday GBPUSD sellers push price-action back below the 1.3200 level, the pair is expected to find support from the daily pivot point, at 1.3179, and the key 1.3149 support level.

EURO Buyers In Control Above 1.1780

The euro has moved sharply higher against the U.S dollar, hitting 1.1816 during the Asian trading session. The U.S dollar index started to move lower during the U.S session, as the Federal Reserve's Beige Book highlighted a lack of inflation in the U.S economy. The EURUSD pair currently trades around the 1.1800 mark, as traders await the U.S dollars next move, and any news coming from Catalonia.

EURUSD intraday buyers will remain in control while price-action trades above the key 1.1780 level. Further bullish advancement for the euro can be expected towards the 1.1833 and 1.1858 technical resistance levels.

Should the EURUSD pair move below the 1.1780 level for a sustained period, further declines towards the 1.1750 and 1.1736 level remain likely.

China GDP Kicks Off An Active Trade Session

High-profile Chinese data have set the tone for Thursday's session. British retail sales, a Catalan deadline and a US manufacturing survey are also scheduled to make headlines throughout the day.

China's National Statistics Bureau said third-quarter GDP accelerated 6.8% year-over-year, matching forecasts. That followed a faster than expected gain of 6.9% in Q2.

China also said retail sales rose 10.3% year-over-year. Industrial production climbed a faster than expected 6.6%, official data showed.

The Chinese economy is the world's second largest. What happens there is important to any investor with a stake in global trade, emerging markets and commodities.

Looking ahead to the rest of the day, Switzerland will release its latest trade figures at 06:00 GMT. Two hours later, Catalan authorities must confirm whether they have declared Independence or not following the referendum result.

UK retail sales will make headlines at 08:30 GMT. Receipts at retail stores are forecast to grow 2.1% in the 12 months through September. Excluding fuel, sales are expected to rise 2.4%.

Shifting gears to North America, the US Labor Department will release its weekly jobless claims report at 12:30 GMT. Claims are forecast to fall by 3,000 to a seasonally adjusted 240,000 in the week ended 14 October.

The Philadelphia Fed will also report its latest manufacturing survey at 12:30 GMT. The headline indicator is expected to fall to 22.0 from 23.7.

In terms of monetary policy, Fed Bank of Kansas City President Esther George will deliver a speech at 13:30 GMT. George is not a member of this year's Federal Open Market Committee (FOMC), which is scheduled to meet again in a few weeks.

AUD/USD

The Australian dollar gave back gains against the dollar despite upbeat China data. The AUD/USD exchange rate reached a session high of 0.7871 before paring gains later in the day. The pair is trading flat compared to Wednesday's close. The technical levels show immediate support at 0.7818, which is the low from Wednesday. The pair continues to trade within a 100-pip range between 0.7800 and 0.7900.

EUR/USD

Europe's common currency regained momentum on Wednesday, climbing back toward the 1.1800 handle. The EUR/USD touched a high of 1.1820 overnight before falling back toward 1.1800. The euro risks further downside should it break below that level. Immediate support is likely found at 1.1703.

GBP/USD

Cable edged slightly higher in overnight trade, although gains were tepid after Bank of England Governor Mark Carney issued a stark warning about Brexit risks. Those comments outweighed Britain's 3% inflation print, which was bigger than expected. The GBP/USD is up 0.1% to trade at 1.3210. Its immediate resistance trigger is 1.3250. On the opposite side of the ledger, support levels are found near 1.3130.