Sample Category Title

Trade Idea Update: EUR/USD – Sell at 1.1850

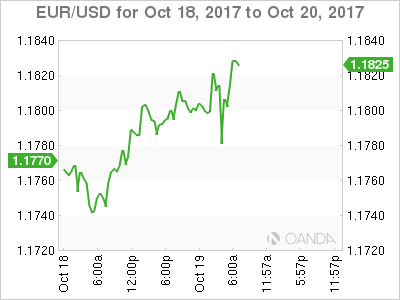

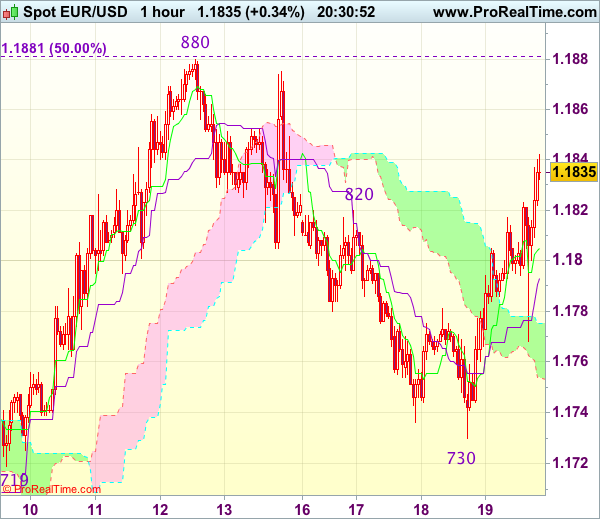

EUR/USD - 1.1830

Original strategy :

Sell at 1.1850, Target: 1.1750, Stop: 1.1885

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1850, Target: 1.1750, Stop: 1.1885

Position : -

Target : -

Stop : -

Although the single currency has risen again and near term upside risk remains for the rise from this week’s low at 1.1730 to extend gain to 1.1845-50, if our view that top has been formed at 1.1880 is correct, upside would be limited and bring retreat later, below the Kijun-Sen (now at 1.1777) would suggest an intra-day top is formed, bring weakness to 1.1755-60 but said support at 1.1730 should remain intact.

In view of this, we are inclined to turn short on further rise but one should exit on subsequent decline. Above said resistance at 1.1880 would shift risk back to upside and extend early rise from 1.1669 to 1.1900-10 first.

Trade Idea Update: USD/JPY -Stand aside

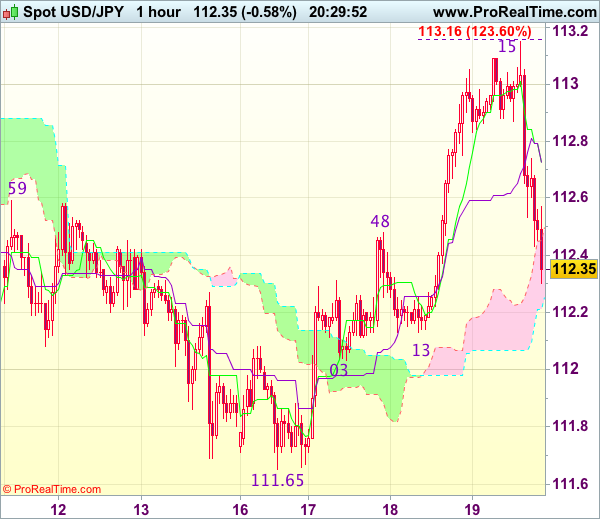

USD/JPY - 112.35

Original strategy :

Bought at 112.70, stopped at 112.35

Position : - Long at 112.70

Target : -

Stop : - 112.35

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite intra-day brief rise to 113.15, the subsequent much deeper than expected retreat has dampened our bullishness and signals a temporary top has been formed there, hence consolidation with mild downside bias is seen for test of indicated strong support area at 112.03-13 but break there is needed to add credence to this view and signal the rebound from 111.65 has ended, bring another fall towards this level later.

On the upside, whilst recovery to the Kijun-Sen (now at 112.73) cannot be ruled out, price should falter well below said resistance at 113.15 and bring another retreat later. Only break of said resistance at 113.15 would revive bullishness for retest of recent high at 113.44 which is likely to hold on first testing.

Kiwi Tumbles as Labour/NZ First Government Means Status Quo No More

With no single party being able to secure over half of the seats in the parliament in last month's election, the right-wing, populist NZ First party has become a kingmaker. Its leader Winston Peters has just announced that his party would form a government with the Labour Party. Kiwi's sell off after the announcement as the outcome has not been quite priced in. NZ First had cooperated with both National and Labour previously (National/ NZ First from 1996 to 1998, and Labour/ NZ First from 2005 to 2008). It did not show preference over a certain party. Uncertainty has not abated after the decision. Rather, it has increased as it would be the first time in 9 years for the Labour Party, as well as the Labour/NZ First coalition, to be the government. The Green Party has also ratified the "confidence and supply" deal which includes promises of three ministerial positions outside Cabinet, and one undersecretary role, for the party. By not joining the cabinet but sitting in on discussions on areas relevant to the party's portfolios, the Green would be able to "retain distinctiveness". That means, the party might still dissent on certain bills. Meanwhile, with 44.4% of votes and 56 seats, National has become the single largest party in the parliament and the most powerful opposition ever. This might increase the difficult for controversial legislations to get passed.

At the press conference, Labour's leader and the next PM Jacinda Ardern indicated that Labour and NZ First "had more in common than issues that divided them". We analyze below that the policy agendas on immigration, RBNZ and the housing market of both parties would lead to a prolonged easy monetary policy and a weak New Zealand dollar.

Net Immigration

The Labour Party proposes to cut net immigration to around 30K per year, from the current 72K, while the Green Party upholds the idea of "sustainable net migration flow to limit effects on our environment, society and culture". The latter does not object the idea to cut net immigration though it has not suggested a number. NZ First proposes the most restrictive immigration policy amongst all parties. It proposes to attract highly-skilled migrants by sharply cutting numbers to around 10K per annum, from the current 72K. It also proposes to adopt strict control over immigration under "family reunion" and "make sure that Kiwi workers are at the front of the job queue". Reduction in net immigration should weigh on economic growth over coming years.

NZD and Monetary Policy

All of Labour, Green and NZ First demand material change to the RBNZ's monetary policy framework. As we mentioned at the election preview last month, with the back of the Green Party, the Labour party proposes a move to committee-based decision making and a dual mandate that includes employment (price stability already exists) in RBNZ's monetary policy setting. The change to dual mandate is prone to shake confidence in the New Zealand dollar as this would mark one of the biggest changes for the RBNZ since its establishment. Depending how the mandate is formulated, a full employment mandate, together with the current 1-3% inflation target, would theoretically lead to looser monetary policy, or a slower pace of rate hike. NZ First proposes to reform the Reserve Bank Act, aiming at achieving a "more exporter-friendly" RBNZ and "sensible exchange rate regime". This implies lower exchange rate and a more accommodative monetary policy.

Housing

Both Labour and NZ First favor increasing supply of affordable housing. The Labour proposes a KiwiBuild program which aims at building a hundred thousand of "high quality, affordable homes over 10 years, with 50% of them in Auckland". It would also create an Affordable Housing Authority to fast-track development. For NZ First, it has initiated "the New Zealand Housing Plan to revamp the New Zealand housing market covering housing availability and affordability as well as rental homes supply and affordability". If the ultimate goal of lower housing price is achieved, the RBNZ would find it more comfortable to maintain its accommodative monetary policy.

GBPUSD Selling to Accelerate Below 1.3146

The British pound has crashed lower against the U.S dollar, hitting 1.3132, as data showed that United Kingdom Retail Sales dropped 0.9 percent during the month of September. The GBPUSD pair currently trades around the 1.3155 region, with intraday sellers now firmly in control. Traders will now look to upcoming release of U.S economic data, and any news coming out of Brexit negotiations in Brussels.

The GBPUSD pair is likely to come under further selling pressure if price-action moves back below the 1.3146 level. Sellers will then likely target the former price low's at 1.3132 and 1.3121 level, and the key 1.3080 support level.

Failure to move the GBPUSD pair below the 1.3146 level should lead to buyers then pushing price-action back upwards to test the daily pivot point at 1.3186. Further extended intraday resistance is also found at 1.3200 and 1.3233.

USDJPY Sellers Take Charge Below 112.58

The USDJPY pair has fallen sharply during the European trading session, hitting 112.46, as Japanese futures decline and fears over the Catalan crisis move investors into the perceived safety of the Japanese Yen. The pair now trades around the 112.55 level, ahead of the U.S market open, after earlier hitting a nine-day trading high, at 113.14.

USDJPY intraday sellers remain in control while the pair trades below the key 112.58 technical level. Further declines remain likely towards the 112.30 and 111.98 levels. Extended intraday support is found at the 111.79 and 111.64 levels.

If USDJPY sellers fail to defend the 112.58 level during the U.S trading session, intraday buyers will likely push price-action back towards the 112.74 and 112.89 technical resistance levels.

CAC Down On Catalan Woes

The CAC index has lost ground in the Thursday session. Currently, the CAC is trading at 5,351.00, down 0.60% on the day. On the release front, there are no French or eurozone events on the schedule. On Friday, the eurozone releases current account, which is expected to rise to EUR 26.2 billion.

All eyes are on Spain, as investors are nervously monitoring the constitutional crisis in Catalonia. The Spanish stock market is down 1.0% on Thursday, and this has dragged down other European stock markets, including the CAC. The Catalan government ignored a deadline to withdraw its independence bid, prompting Madrid to threaten it would impose direct control on the region on Saturday. Analysts continue to digest European corporate earnings for the third quarter, and the results will likely have a strong impact on European stock markets next week.

European Union leaders are meeting in Brussels on Thursday and Friday. French President Emmanuel Macron has pushed trade issues onto the agenda. Macron wants the EU to proceed with caution on trade talks that deal with agriculture, as increased imports of beef and other farm products into the EU could severely impact the French farm sector. The EU is currently holding talks with the Mercosur bloc, which includes Argentina and other South American nations, and is planning to hold free trade talks with Australia and New Zealand.

What’s next for Catalonia? The cat-and-mouse game between the Spanish and Catalan governments continues, as a Thursday deadline looms. The Spanish has given Catalan President, Carles Puigdemont until Thursday to recant his declaration of independence. If Puigdemont refuses, Madrid has threatened to trigger Article 155 of the Spanish constitution, which would allow the central government to disband the Catalan parliament and impose direct rule. However, this clause has never been used, and could set off a violent reaction in Catalonia, with emotions already at a fever pitch. The deepening constitutional crisis has led hundreds of companies to start leaving Catalonia, and the Standard and Poor’s rating agency has said that the region could face a recession if the situation is not resolve. Investment projects are at a standstill in the region, and if the situation worsens, investors could get nervous and the European stock markets could respond with losses.

How Will Traders Respond To Dip In US Stocks?

- Buy the dip mentality put to the test on Thursday;

- Madrid prepares to trigger article 155;

- Softer Chinese data partially blamed for profit taking;

- UK retail sales miss should be warning to BoE.

US futures are coming under a little pressure on Thursday, a day after the Dow closed above 23,000 for the first time ever, in what appears to be some profit taking following an impressive run for stocks.

While there were no major triggers for this morning's decline, the finger is being pointed at the softer Chinese economic data and unrest in Spain, where the government announced its intention to trigger article 155 and suspend Catalonia's autonomy. While neither of these are reason for traders to be bearish stocks right now, it has been pounced upon as reason to take some money off the table and await further opportunities.

The situation in Spain is having a greater impact on the wider European markets, particularly in the IBEX which is down around 1% as investors prepare for more unrest in Catalonia. The euro has been very unresponsive to the developments in Spain so far and the same is true again today, with the single currency trading higher against the dollar, pound and yen. This is clearly seen as being a risk unique to Spain, rather than a problem that could develop elsewhere, although the Italian FTSE MIB has shown some vulnerability to it throughout the process.

It will be interesting to see how US traders respond to the dip at the open. Sentiment has been extremely positive recently, despite the significant amount of political and geopolitical risk lingering beneath the surface. The global growth story is giving people great confidence that the rally has legs to it and earnings for the third quarter of likely to support that.

The Chinese economic data released overnight was broadly in line with expectations but did highlight the fact that the economy is slowing a little in the second half of the year. This was widely expected though as the government has reined in spending and focused more on cooling the housing market and reforms. We can expect more of the same in the fourth quarter although as we saw in the third, the improved global economic environment is likely to support the Chinese economy through this transition.

In the UK, retail sales wrapped up a week of important economic releases and left us with a bitter taste. Perhaps expectations were too high and a larger decline should have been expected following the strong showing in August but instead the data fell well short of forecasts. The numbers further highlighted what we already know, the UK consumer is feeling the strain of negative real wage growth and this will take its toll on spending. While the inflation and jobs data may be seen as justifying a rate hike from the Bank of England, today's data should be a warning to policy makers that the economy is not in a good position to take it.

While the focus today is likely to be how US markets respond to early weakness, we will also get some manufacturing and jobless claims data from the world's largest economy. We'll also get third quarter earnings reports from 20 S&P 500 companies including Verizon, Paypal and Travelers. Esther George of the Federal Reserve is also scheduled to appear while Chair Janet Yellen is also believed to be meeting with President Donald Trump, who is understood to be making a decision on her successor in the coming days

DAX Drops As Catalan Tensions Worsen

The DAX has recorded losses in the Thursday session. Currently, the index is at 12,958.50 down 0.65% on the day. On the release front, there are no major indicators out of the eurozone. On Friday, Germany releases PPI and the eurozone will publish its current account surplus.

The Spanish stock market is down 1.0% on the day, and this has dragged down other European stock markets, including the DAX. The crisis over Catalan independence has worsened, as the Catalan government ignored a deadline to withdraw its independence bid, prompting Madrid to threaten it would impose direct control on the region on Saturday. Analysts continue to digest European corporate earnings for the third quarter, and the results will likely have a strong impact on the stock markets next week.

All eyes are on Spain, as investors are nervously monitoring the constitutional crisis in Catalonia. The Catalan government has refused to comply with a demand by Madrid to withdraw its declaration of independence, and the central government has responded harshly, saying it will invoke Article 155 of the Spanish Constitution and impose direct control over Catalonia. However, the government must first receive approval from the Senate before it implements this measure, and the Senate is expected to approve the move on Saturday. Madrid has said that it will not invoke this measure if the Catalan parliament calls new elections, but so far there has been no response from Catalan leaders. The deepening constitutional crisis has led hundreds of companies to start leaving Catalonia, and the Standard and Poor’s rating agency has said that the region could face a recession if the situation is not resolve. Investment projects are at a standstill in the region, and if the situation worsens, investors could get nervous and send the euro lower.

Euro Quiet, Catalonia Crisis Deepens

The euro has edged higher in the Thursday session, as EUR/USD stays close to the 1.18 line. Currently, EUR/USD is trading at 1.1812, up 0.22% on the day. On the release front, there are no major indicators out of the eurozone. In the US, unemployment claims are expected to dip to 240 thousand, while the Philly Fed Manufacturing Index is forecast to slow to 21.9 points. On Friday, Germany releases PPI and the eurozone will publish its current account surplus. The US will release Existing Home Sales and Fed Chair Janet Yellen speaks at an event in Washington.

The crisis in Catalonia continues, as the Spanish and Catalan governments remain entrenched in their positions. The Catalan government has refused to comply with a demand by Madrid to withdraw its declaration of independence, and the central government has responded harshly, saying it will invoke Article 155 of the Spanish Constitution and impose direct control over Catalonia. However, the government must first receive approval from the Senate before it implements this measure, and the Senate is expected to approve the move on Saturday. Madrid has said that it will not invoke this measure if the Catalan parliament calls new elections, but so far there has been no response from Catalan leaders. The deepening constitutional crisis has led hundreds of companies to start leaving Catalonia, and the Standard and Poor’s rating agency has said that the region could face a recession if the situation is not resolve. Investment projects are at a standstill in the region, and if the situation worsens, investors could get nervous and send the euro lower.

European Union leaders will gather in Brussels on Thursday and Friday. The meeting was expected to focus on Brexit, but with talks with Britain floundering, Brexit will likely take a back step. The EU may do little more than declare that trade talks with London will not begin until there is more progress on other issues, such as the amount Britain will pay when it leaves the club. There are a number of other topics on the agenda, including the crisis in Catalonia, the Iran nuclear agreement, and a proposal to deepen integration among EU members.

Spain To Trigger Suspension Of Catalan Autonomy On Saturday

Spain's government will trigger on Saturday the Article 155 of the constitution, which allows it to suspend Catalonia's political autonomy.

This mornings special cabinet meeting was called after Catalan leader Carles Puigdemont said the regional parliament could vote on a formal declaration of independence from Spain if the central government failed to agree to talks.

Bond Spreads

Eurozone periphery government bond spreads have widened as Catalan President Carles Puigdemont says he might formally declare independence if Madrid refuses dialogue.

Moves are limited, however. Ten-year Spanish, Italian and Portuguese bond yield spreads over equivalent German bunds are by up to +2 bps wider, with the most widening in Portuguese spreads and the least in Spanish spreads. The 10-year Spanish-German spread trades at +124 bps, up +1.2 bps.

The Spanish government have confirmed to hold an emergency Cabinet meeting on Sat, Oct 21st to begin process of suspending Catalan autonomy under Article 155

The EUR (€1.1804) is currently off its intraday Euro highs and is straddling the psychological €1.18 handle