Sample Category Title

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9781; (P) 0.9808; (R1) 0.9843; More....

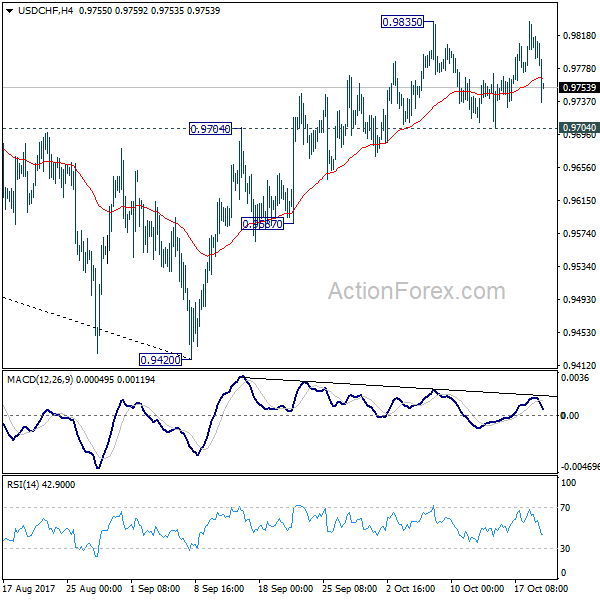

Focus on USD/CHF is back on 0.9704 support after today's sharp fall. Decisive break of 0.9704 will argue that rebound from 0.9420 has completed. This will also mixed up the near term outlook and turn bias back to the downside for 0.9587 support. On the upside, firm break of 0.9835 resistance will confirm resumption of rebound from 0.9420. In that case, USD/CHF should target 61.8% retracement of 1.0342 to 0.9420 at 0.9990 next.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could develop into a medium term move and target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9587 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

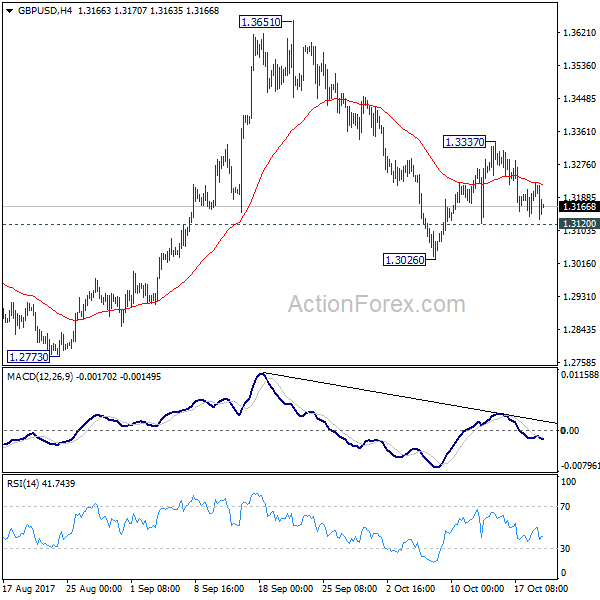

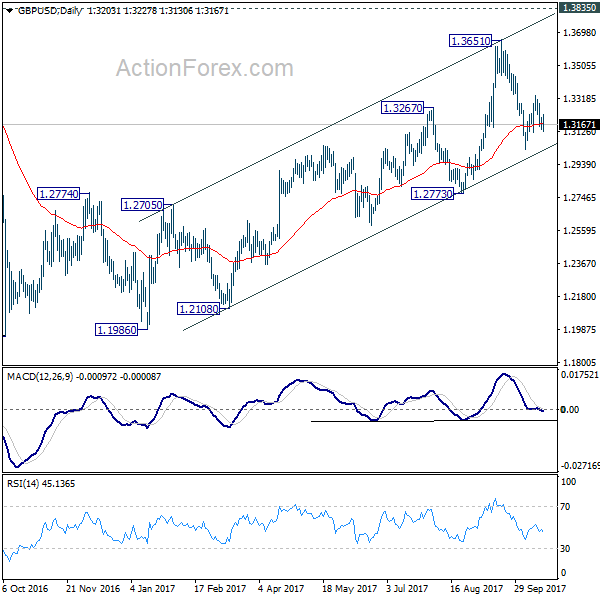

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3158; (P) 1.3183; (R1) 1.3227; More....

Intraday bias in GBP/USD remains neutral at this point. On the downside, break of 1.3120 will indicate that recovery from 1.3026 is completed at 1.3337. And fall from 1.3651 is resuming for 1.2773 support. That will revive that case that medium term rise from 1.1946 has completed at 1.3651. Meanwhile, above 1.3337 will bring retest of 1.3651 high instead.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll turn neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Canadian Dollar Unchanged, US Jobless Claims Next

The Canadian dollar is unchanged in the Thursday session, after posting gains on Wednesday. In European trade, USD/CAD is trading at 1.2469, up 0.03% on the day. On the release front, US unemployment claims are expected to dip to 240 thousand, while the Philly Fed Manufacturing Index is forecast to slow to 21.9 points. There are no Canadian indicators on the schedule. On Friday, Canada will release key consumer spending and inflation data. CPI is expected to accelerate to 0.3%. The markets are predicting that retail sales will also improve to 0.3%. The US will release Existing Home Sales and Fed Chair Janet Yellen speaks at an event in Washington.

With the Canadian economy performing well, could another rate hike be in the cards? The Bank of Canada surprised with a rate hike in September, but policymakers are concerned over tensions about NAFTA. Talks between Canada, the US and Mexico over re-negotiating NAFTA have floundered, raising the possibility that Donald Trump will scrap the agreement. The BoC would prefer not to raise rates until the NAFTA negotiations are settled. However, the Federal Reserve is widely expected to raise rates in December and the BoC will be under pressure to follow suit and protect the Canadian dollar.

There was good news out of the Canadian manufacturing sector on Wednesday. Manufacturing Sales jumped 1.6% in August, ending a streak of two declines. The excellent reading was the highest gain this year, and points to a manufacturing sector which has benefited from strong global demand for Canadian products.

Federal Reserve Chair Janet Yellen is due to retire in February, and the markets are keeping close tabs on who will replace her at the helm of the powerful central bank. President Trump is leaning towards nominating economist John Taylor, who is considered more hawkish on policy than Yellen. Under Taylor, interest rates would likely move substantially higher than the current 1.25%, and a rate hike early in 2018 could strengthen the US dollar against gold. Other candidates for the Fed Chair include current Fed Governor Jerome Powell and former Fed official Kevin Warsh.

EURUSD Extends Recovery and Shifts n/t Bias Higher; Catalonia Remains in Focus

The Euro advanced on Thursday as US dollar stood at the back foot and rallied to 1.1840, pressuring barriers at 1.1840/44 (converged 55/30 SMA's).

Recovery rally sidelines downside risk of testing daily cloud base at 1.1702 after bear-leg from last week's high at 1.1879 was repeatedly rejected at 1.1730.

Close above 55/30SMA's will generate bullish signal for further recovery towards 12 Oct high at 1.1879, break of which would trigger stronger bullish acceleration towards daily cloud top at 1.1924.

Setup of daily studies is mixed, with 14d Momentum breaking in the positive territory and supporting further advance.

Heated situation in Catalonia is still seen as key factor for the single currency.

Spain's central government said it would suspend Catalonia's autonomy and impose direct rule after Catalan leader ignored the deadline to drop secession campaign and threatened government in Madrid with a formal declaration of independence.

Spanish PM said he would hold a special meeting of the cabinet on Saturday that could trigger the unprecedented move in revoking Catalan independence.

Res: 1.1844; 1.1851; 1.1879; 1.1924

Sup: 1.1800; 1.1767; 1.1730; 1.1702

EURUSD Recovers, Eyes Further Bull Pressure Towards 1.1879 Region

EURUSD: With the pair seen following through on the back of its Wednesday gains on Thursday, more strength is expected in the days ahead. Resistance comes in at 1.1850 level with a cut through here opening the door for more upside towards the 1.1900 level. Further up, resistance lies at the 1.1950 level where a break will expose the 1.2000 level. Its daily RSI is bullish and pointing higher suggesting more strength. Conversely, support lies at the 1.1750 level where a violation will aim at the 1.1700 level. A break of here will aim at the 1.1650 level. Below here will open the door for more weakness towards the 1.1600. All in all, EURUSD continues to face recovery threats with eyes on 1.1879 zone.

U.K. Retail Sales Disappoint, Catalonia in Focus

Sterling found itself under immediate selling pressure on Thursday morning, after British retail sales tumbled in September.

U.K retail sales slumped -0.8% in September, dragging the annualized figure lower to 1.2%, as rising inflation and subdued wage growth sapped consumers' spending power. With wage growth still struggling to keep up with inflation and squeezing incomes, concerns are likely to mount further, over the longevity of Britain's consumer-driven economic growth.

It has been another painful trading week for Sterling;sentiment was driven by an unpalatable cocktail of soft economic fundamentals, dovish comments from some BoE officials and Brexit uncertainty. With inflation jumping to a five and a half year high in September, wage growth remaining subdued and retail sales disappointing - is this really the right environment to raise interest rates?

There is a growing suspicion that the central bank will implement a dovish rate hike in November to contain inflation. With the current economic landscape looking bleak and Brexit uncertainty still weighing on sentiment, the rate hike that markets are heavily anticipating next month, may be a "once-off".

From a technical standpoint, the GBPUSD is coming under increasing pressure on the daily charts. A breakdown below 1.3150 should encourage a further decline lower towards 1.3050.

Spain to trigger Article 155 on Saturday

The Euro was surprisingly resilient during Thursday's trading session, despite reports of Spain proceeding with suspending Catalonia's political autonomy on Saturday.

Catalan leader, Carles Puigdemont, was given until 09:00 BSTtoday to declare his intention to pursue independence, following the referendum on 1 October. With his response in the form of a letter to Spanish Prime Minister Mariano Rajoy, threating to declare independence if no talks were offered, the Spanish government responded by arranging a special Cabinet meeting on Saturday, where they intend to enact Article 155.

I believe the Euro still remains vulnerable to heavy losses, as the political drama in Spain will sparkconcern over political instability in Europe. With uncertainty potentially mounting after Spain's government triggersArticle 155 this weekend, the Euro remains exposed to downside risks. Investors should keep in mind that although the Catalan drama is limited to Spain, it could still spark fears over the rise of other separatist movements in Europe. Such a situation is likely to threaten the stability of the European Union.

Taking a look at the technical picture, the EURUSD has rebounded back towards 1.1850. A failure for prices to break and secure a daily close above this level, may open a path back towards 1.1730. In an alternative scenario, a breakout above 1.1850 could open a path towards 1.1920.

Commodity spotlight – WTI Oil

The sharp decline witnessed on WTI Crude today, may suggest that bulls are displaying early signs of exhaustion.

Although there are heightened geopolitical tensions between the United States andIran over the Joint Comprehensive Plan of Action (JCPOA) and ongoing conflicts in Iraq, optimism over global demand for oil increasing in 2017, have supported oil markets - the question is, for how long? Investors should keep in mind that OPEC's production rose 32.7 million in September, which was the second highest level this year. The increase in production, despite the cartel's optimism and efforts to limit output, may call into question the effectiveness of the production cuts.

Much attention should be directed to how OPEC deals with rising production from Nigeria and Libya. With increased output from these two suppliers potentially disrupting the efforts made by the rest of the group to tackle the oversupply woes, OPEC may request that they also cut production.

From a technical standpoint, WTI Crude is at risk of depreciating further, if bears can conquer $51. A breakdown below this level may encourage a further decline back towards the $50 level.

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 0.9754

Original strategy :

Bought at 0.9790, stopped at 0.9755

Position : - Long at 0.9790

Target : -

Stop : - 0.9755

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite rising to 0.9837, the greenback failed to penetrate this resistance and has retreated sharply, dampening our bullishness and signaling recent upmove is not ready to resume yet, hence near term downside risk remains for weakness to 0.9730 support, however, as broad outlook remains consolidative, reckon downside would be limited and support at 0.9705 should hold from here, bring rebound later.

On the upside, expect recovery to be limited to the Kijun-Sen (now at 0.9787) and reckon 0.9810 would hold and bring another decline later. Above 0.9810 would bring a retest of said strong resistance at 0.9837 but break there is needed to confirm recent rise from 0.9421 low has resumed for headway to 0.9870 and possibly towards 0.9900. As near term outlook is mixed, would be prudent to stand aside for now.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1742; (P) 1.1773 (R1) 1.1818; More...

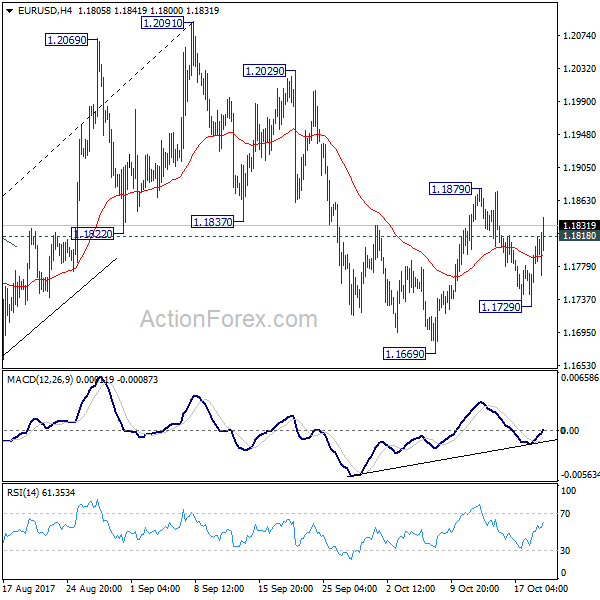

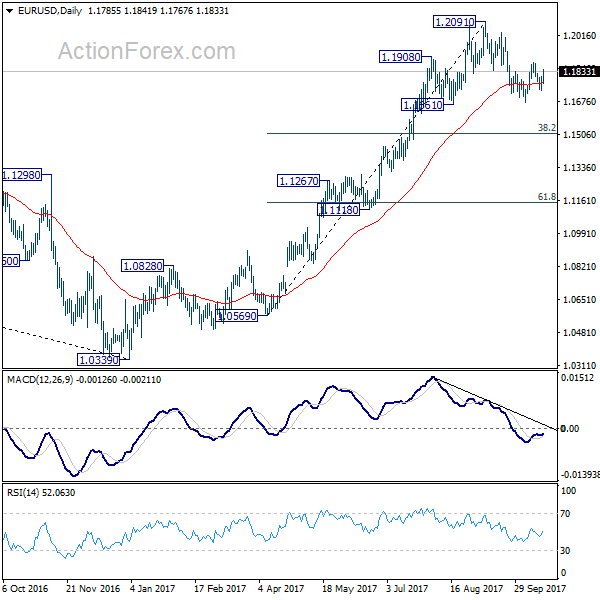

EUR/USD's break of 1.1818 minor resistance suggests that pull back from 1.1879 is completed at 1.1729. And, rebound from 1.1669 is resuming. More importantly, it revives that case that corrective fall from 1.2091 has completed at 1.1669, ahead of 1.1661 support. Intraday bias is now back on the upside for 1.1879 first. Break will pave the way to retest 1.2091 high. On the downside, below 1.1729 will bring retest of 1.1669 instead.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

Euro Shows Resilience after Catalonia Turmoil, Yen and Franc Strike Back

Japanese Yen and Swiss Franc strike a strong come back today as markets are haunted by political developments. Spanish Prime Minister Mariano Rajoy announces to invoke the so called Article 155 of Constitution to suspend autonomy of Catalonia. That came after Catalan leader Carles Puigdemont refuses to withdraw the declaration of independence. Euro initially dipped against all major currencies after the news. But then, the common currency recovered strongly against all but Yen and Swiss Franc only. German DAX is trading down down more than -0.9% at the time of writing. US futures also point to a lower open.

But so far for the day, New Zealand dollar is the weakest one on political uncertainty after announcement of the new coalition government. Sterling is trading as the second weakest after terrible retail sales data. Yen and Swiss Franc are the stars today. Dollar is trading mixed.

US data positive, but no support to greenback

US initial jobless claims dropped -22K to 222K in the week ended October 14. That's much better than expectation of 240k. Also it's the lowest level since March 1973. Four week moving average of initial claims dropped -9.5K to 248.25K. Continuing claims dropped -16K to 1.89M, hitting a 44 year low. Philly Fed manufacturing index rose sharply to 27.9 in October, up from 23.8 and beat expectation of 22.0. That's also the highest level in five months. But the data provides little inspiration to Dollar.

Released from UK, retail sales dropped sharply by -0.8% mom in September, versus expectation of -0.1% mom. Also from Europe, Swiss trade surplus widened to CHF 2.92B in September.

New Zealand Dollar dives on coalition news

With no single party being able to secure over half of the seats in the parliament in last month's election, the right-wing, populist NZ First party has become a kingmaker. Its leader Winston Peters has just announced that his party would form a government with the Labour Party. Kiwi's sell off after the announcement as the outcome has not been quite priced in. NZ First had cooperated with both National and Labour previously (National/ NZ First from 1996 to 1998, and Labour/ NZ First from 2005 to 2008). It did not show preference over a certain party. Uncertainty has not abated after the decision. Rather, it has increased as it would be the first time in 9 years for the Labour Party, as well as the Labour/NZ First coalition, to be the government. More in Kiwi Tumbles as Labour/NZ First Government Means Status Quo No More

Improving labor market could allow RBA to pare back stimulus

Australia NAB business condition index rose 2 pts to 15. But business confidence dropped 1 pt to 7 in Q3. NAB chief economists Alan Oster noted that overall results point to improvements in the economy. And, "a positive byproduct of that has been solid outcomes for hiring intentions and capex plans for the year ahead." Also, "there now seems to be sufficient evidence to suggest that the labour market will continue to improve enough to allow the RBA to pare back some of its emergency stimulus."

Separately released, employment grew 19.8K in September, above expectation of 15.0K. That's also the 12 straight month of growth. Full time jobs grew 6.1K while part-time jobs grew 13.7K. Participation rate was unchanged at 65.2%. Unemployment rate dropped to 5.5%, below expectation of 5.6%. That's also the lowest reading since May, which then was the lowest since early 2013.

Japan Abe likely to have solid victory in snap election

In Japan, according to a Kydo News survey released earlier this week. Prime Minister Shinzo Abe's Liberal Democratic Party-Komeito coalition will pick up 310 seats, out of 465, in the upcoming election on Sunday. That should be enough to give the coalition a two-thirds absolute majority. It's reported that Abe is already planning a special Diet session on November 1. And new Cabinet will be promptly formed afterwards. Then, Abe will be meeting with US President Donal Trump on November 5.

Japan trade surplus narrowed, with temporary slow down in exports

Japan trade surplus narrowed to JPY 0.24T in September. Export grew 14.1% yoy, lower than expectation of 14.9% yoy, and the first slowdown in three months. Nonetheless, the 18.1% yoy growth of export back in August was the fastest in nearly four years. It's generally seen that the slowdown is temporary and recovery in global economy is still in place. Imports rose 12.0% yoy, also below expectation of 15.0% yoy. Also from Japan, all industry index rose 0.1% mom in August.

Updates on the twice-in-a-decade National Congress of the Chinese Communist Party

Predominantly the most important political event in China, the twice-in-a-decade National Congress of the Chinese Communist Party began on October 18. As a kick start, President Xi delivered a Party Work Report which reviewed the achievements in his first five years and outlined the challenges and goals for the next five years and beyond. Xi outlined his thoughts on the 'new era of socialism with Chinese characteristics'.

On the economic reform, he suggested further developments in the "advanced manufacturing industry", which includes medium and high end consumption, green and low carbon industry, sharing economy, modern logistics and human capital services.

He has also pledged to deepen interest rate and exchange rate reforms, develop a comprehensive financial regulation system and reduce systematic financial risk. These are nothing new as the key aspects of the monetary and fiscal policies have already been lain down at the National Financial Work Conference in July.

More in The 19th CCP Congress – A Summit For Xi To Crown Himself

Also on China: China: Xi Jinping Lays Out Path of Further Reform and Opening

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1742; (P) 1.1773 (R1) 1.1818; More...

EUR/USD's break of 1.1818 minor resistance suggests that pull back from 1.1879 is completed at 1.1729. And, rebound from 1.1669 is resuming. More importantly, it revives that case that corrective fall from 1.2091 has completed at 1.1669, ahead of 1.1661 support. Intraday bias is now back on the upside for 1.1879 first. Break will pave the way to retest 1.2091 high. On the downside, below 1.1729 will bring retest of 1.1669 instead.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance JPY Sep | 0.24T | 0.32T | 0.37T | 0.31T |

| 00:30 | AUD | NAB Business Confidence Q3 | 7 | 7 | 8 | |

| 00:30 | AUD | Employment Change Sep | 19.8k | 15.0k | 54.2k | 53.0k |

| 00:30 | AUD | Unemployment Rate Sep | 5.50% | 5.60% | 5.60% | |

| 02:00 | CNY | GDP Y/Y Q3 | 6.80% | 6.80% | 6.90% | |

| 02:00 | CNY | Retail Sales Y/Y Sep | 10.30% | 10.20% | 10.10% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Sep | 7.50% | 7.70% | 7.80% | |

| 02:00 | CNY | Industrial Production Y/Y Sep | 6.60% | 6.40% | 6.00% | |

| 04:30 | JPY | All Industry Activity Index M/M Aug | 0.10% | 0.20% | -0.10% | |

| 06:00 | CHF | Trade Balance (CHF) Sep | 2.92B | 2.47B | 2.17B | 2.20B |

| 08:30 | GBP | Retail Sales M/M Sep | -0.80% | -0.10% | 1.00% | 0.90% |

| 12:30 | USD | Initial Jobless Claims (OCT 14) | 222K | 240K | 243K | 244K |

| 12:30 | USD | Philadelphia Fed Business Outlook Oct | 27.9 | 22 | 23.8 | |

| 14:00 | USD | Leading Indicators Sep | 0.10% | 0.40% | ||

| 14:30 | USD | Natural Gas Storage | 87B |

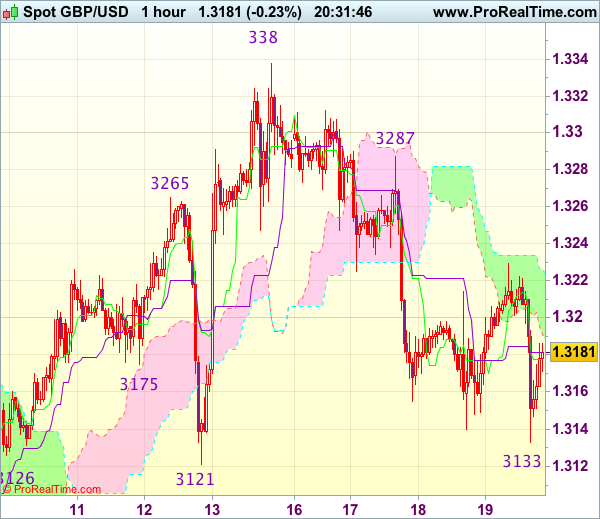

Trade Idea Update: GBP/USD – Sell at 1.3265

GBP/USD - 1.3174

Original strategy :

Sell at 1.3265, Target: 1.3145, Stop: 1.3300

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3265, Target: 1.3145, Stop: 1.3300

Position : -

Target : -

Stop : -

Although cable fell briefly to 1.3133 in London morning, lack of follow through selling and current rebound suggest consolidation would be seen and recovery to 1.3220-25 cannot be ruled out, however, reckon upside would be limited to 1.3255-65 and bring another decline later, below said support at 1.3133 would extend the fall from 1.3338 to support at 1.3121, however, break there is needed to retain bearishness and bring further subsequent decline to 1.3090-00.

In view of this, wee are looking to sell cable on subsequent recovery as 1.3255-65 should limit upside, bring another decline later. Above said resistance at 1.3287 would abort and signal low is formed instead, bring rebound to 1.3300 and possibly test of resistance at 1.3312.