Sample Category Title

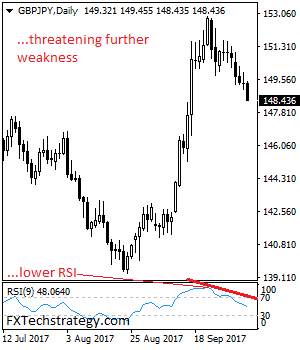

GBPJPY – Bearish, Retains Its Downside Pressure

GBPJPY - The cross remains vulnerable to the downside on further weakness as it retains its bearish bias. On the downside, support comes in at the 148.00 level where a violation will aim at the 147.50 level. A break below here will target the 147.00 level followed by the 146.50 level. Conversely, resistance is seen at the 149.00 level followed by the 149.50 level. A cut through that level will set the stage for a move further higher towards the 150.00 level. Further out, resistance resides at the 150.50 level. All in all, GBPJPY remains weak and vulnerable to the downside.

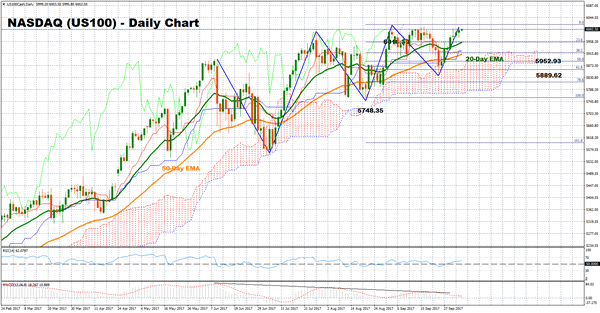

US100 Stock Index Bullish In Short- And Medium-Term, Positive Momentum Though Weakens

The tech-heavy US100 index is currently trying to post another green candle around record high levels, stretching its upleg started on September 26. The outlook in the short- and medium-term remains bullish based on oscillator signals. However, momentum has slowed down, hinting to softer upside movement in the short-term.

The RSI has entered bullish territory above 50 at the end of September and is currently positively sloped, suggesting a bullish picture in the short-term. The MACD is also above zero and its signal line but the fact that it has been making lower highs since June highlights that the index might be losing steam. This could also be seen from the last recorded top not being far above the previous peak. Additionally, the Kijun-sen recently moved below Tenkan-sen; this being a negative alignment.

A break above the previous September 1 high of 6016.30 would confirm the continuation of the long-term uptrend and the posting of new record highs. Further extensions would target the 6100 psychological level before the 6200 key mark comes into view.

If the index retreats, support could be first found around the 23.6% Fibonacci point of the upleg from 5748.38 to 6016.30 (August 21- September 1) at 5952.93 which is also where the 20-day exponential moving average (EMA) lays. Next, the focus would shift to the 50% Fibonacci at 5889.62 with the outlook turning to neutral in case the index violates that point. Further declines would turn the attention to the August 21 low of 5748.35 which is also near the bottom of the Ichimoku cloud.

In the medium-term, the outlook remains positive as long as the bullish cross between the 20-day EMA and the 50-day EMA remains in place.

Japan’s Snap Election And The Impacts On Policies

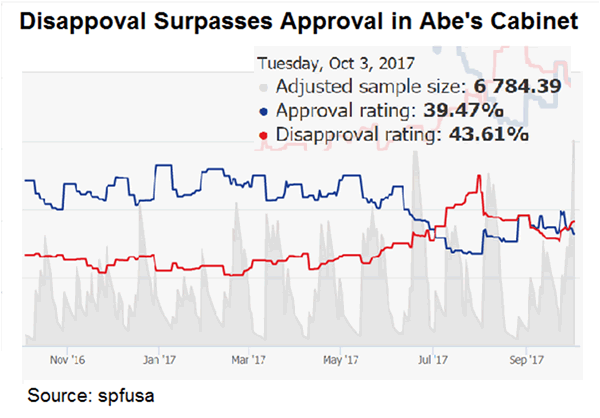

Volatility in Japanese financial markets is set to intensify as the snap election for the parliament (Lower House), scheduled on October 22, approaches. Our base case is that PM Shinzo Abe's LDP would remain the biggest party. He would continue to be the leader of the LDP/Komeito coalition in the new term. However, the rapid rise of the new party Kibo no To (Party of Hope), led by Tokyo Governor Yuriko Koike, might result in a decrease in number of seats for LDP. This, together with the decline in Abe's approval rating, has created much uncertainty in the upcoming election.

Electoral Platform: LDP vs Party of Hope

Party of Hope's draft platform, announced on October 5, focuses on following areas: 1) Constitutional amendment, 2) Phase out of nuclear power, 3) Freeze of the consumption tax increase, 4) Enhancement of national security 5) Reduction of the number of Diet members and their annual allowances, 6) Economic growth through loosened regulations, 7) Education and welfare, 8) Diversity in society, and 9) Decentralization of power.

Constitutional Amendment and Revision of Article 9

As former allies (Koike served as defence minister during Abe's first term as prime minister), Abe and Koike are both categorized as conservative and populist. They are in support of constitutionals amendment, including the most sensitive issue of the war-renouncing Article 9

LDP in its election pledge unveiled the intention to revise the Constitution in four areas. Among which the most sensitive is clarification of the legal status of the self-defence force (SDF) in Article 9. Acknowledging the controversy of this proposal, Abe announced that his party also proposes to keep the first and second paragraphs* unchanged.

Party of Hope also proposes discussions on revising Article 9, possibly allowing the country to exercise its right to collective self defense when it is required in the actual situation.

*Article 9: 1. Aspiring sincerely to an international peace based on justice and order, the Japanese people forever renounce war as a sovereign right of the nation and the threat or use of force as a means of settling international disputes. 2. In order to accomplish the aim of the preceding paragraph, land, sea and air forces, as well as other war potential, will never be maintained. The right of belligerency of the state will not be recognized.

Consumption Tax and Nuclear Power

Indeed, the biggest divisions are on consumption tax and nuclear power. Abe calls for raising the consumption tax rate to 10% from 8% in October 2019. Rather than using the revenue to repay debts, he proposes to allocate the spending on free education and social welfare. Koike, however, proposes to freeze the increase in the consumption tax. She believes a tax hike would suffocate domestic demand growth which has been sluggish. Nuclear power would continue to be key energy source under the leadership of LDP. As indicated in the election pledge, LDP noted that it would restart nuclear power reactors that have confirmed to be safe, after getting consensus from local government. By contrast, Koike's Party of Hope plans to completely end on nuclear power by 2030 while increasing the share of renewable energy to 30%.

Impact of Monetary and Fiscal Policies

Abe noted that it would be considered as victory if the LDP/Komeito could get the majority of seats. Indeed, opinion polls continue to suggest so despite the dropping approval rate of the prime minister. Note at the current parliament, LDP has secured 287 out of 475 seats. Together with Komeito's 35 seats, the coalition government has dominated over two-third of the parliament. This is sufficient to propose constitutional change and reapprove bills rejected by the House of Councilors (Upper House). The number of seats in the next parliament is reduced to 465. As such, 233 seats are sufficient for a majority and 310 seats for two-third. We doubt if Abe could retain his grip on power if he ends up losing 89 (287+35-233) seats to barely secure the majority.

Below we consider three possible outcomes and see how they would affect Japan's monetary and fiscal policy outlooks.

1. LDP/Komeito Majority with Abe as PM (Status Quo)

BOJ would maintain the existing accommodative monetary policy. Abe would continue to push his three arrows in the Abenomics. One of which is aggressive monetary easing. Haruhiko Kuroda would also stay as the central bank head as he was handpicked by Abe, thanks to his dovish stance. Consumption tax would increase in 2019 under Abe's leadership. As he promised, educational and socal welfare spending would rise. Moreover, the second arrow in Abenomics is robust fiscal policy, i.e. the government increases spending to stimulate the economy.

2. LDP/Komeito Majority with new PM

If Abe has to step down, his successor would determine the monetary and fiscal policy stances. The media has identified that Taro Aso, Yoshihide Suga, Fumio Kishida and Shigeru Ishiba as potential candidates. We expect the monetary policy would largely remain accommodative no matter who becomes the new PM. However, the fiscal policy might differ. Aso, Kishida and Ishiba propose fiscal adjustment while Suga advocates bold fiscal policy. Aso, at his capacity as the deputy PM and finance minster, warned last month that the government needs to maintain its efforts to achieve fiscal consolidation on soaring debts. Meanwhile, Ishida indicated that a primary fiscal surplus is a must. Chief Cabinet Secretary Suga believes the current fiscal policy is aimed at boosting economic growth and raising tax revenue.

3. Coalition of Party of Hope and other Smaller Parties

This scenario brings very high uncertainty to Japan's outlook. Koike has yet to reveal her platform on the monetary policy. Yet, judging from her aim to 'rest' Japan, it is possible that she might prefer a less accommodative monetary policy. Indeed, she suggested on September 25 that it is a 'mistake' to rely on monetary policy alone. On the fiscal front, she objects a consumption tax hike. The party has yet to announce more details on the fiscal policies.

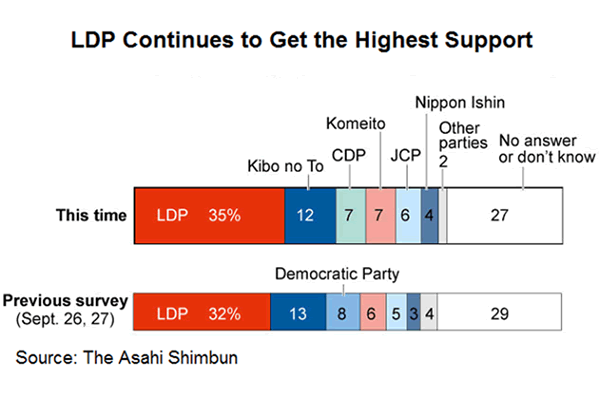

Abe called the snap election when his popularity was at peak, hoping to have a landslide victory with increase in the number of seats. This wishful thinking is reminiscent of what UK PM Theresa May did in June. However, Conservatives eventually lost the majority in the election, amidst the surging support of the Labor Party. In Japan, support for the LDP remains the highest despite the decline after Abe's announcement of the snap election. It is also surprising as the Party of Hope has managed to secure over 10% of support, given this party was launched last week. We expect Japanese market volatility would be high as we approach the election day. Investors fear uncertainty. As we witnessed in the elections (France, UK Germany, New Zealand) so far this year, the country's currency fall if uncertainty increase and investors become more risk-averse. We might see some difference in this time. As a safe-haven currency, Japanese yen rises during time of risk aversion.

Expect U.S Jobs To Be Affected By Summer Hurricanes

Thursday October 5, 2017: Five things the markets are talking about

The U.S. dollar continues to fluctuate against the major currencies as investors pause ahead of tomorrow's North American jobs data. Minimal non-farm payroll (NFP) risk is being priced in to USD majors, as seasonal factors and recent hurricanes may give the data less credence.

One in 13 U.S workers are employed in counties ravaged by this summer's hurricanes in Florida and Texas.

Yet, any signs of solid U.S jobs growth will help justify an additional interest-rate increase by the Fed again this year. The U.S economy added +156k jobs in August while the unemployment rate held at +4.4%.

Note: The median forecast for tomorrow's release is a +80k gain in NFP, less than half the average +182k rise since the start of last year.

Fed fund futures is pricing in a +78% probability that the Fed will hike interest rates by the end of the year, up from around +44% last month.

Elsewhere, elections in the eurozone have rattled currency markets recently. The EUR (€1.1774) outright trades atop of this week's intraday low after an illegal independence vote in the Spanish province of Catalonia took place on the weekend. The prospect of secession has increased pressure on PM Rajoy while rattling Spanish markets.

Note: That came a week after the ‘single unit' was jarred by German Chancellor Merkel's conservative alliance losing ground in the federal election. Austria's legislative election this month (Oct 15) and Italian elections expected to be held by May 2018 could also raise risks for the EUR.

Investors are also watching for developments as President Trump considers replacing Fed Chairwoman Janet Yellen. The U.S administration has interviewed former Fed governor Warsh and Fed governor Powell about taking the helm at the Fed.

1. Stocks stay close to home

Japan's Nikkei share average ended little changed (-0.1%) overnight after hitting a two-year high Wednesday – investors remain cautious ahead of tomorrows U.S data. The broader Topix fell -0.1%.

Note: The Shanghai Composite and Korea Kospi remained closed for Golden Week, while the Hang Seng was closed for a holiday.

Down-under, Australia's S&P/ASX 200 slipped -0.1%, pressured by financial and energy shares.

In Europe, regional bourses are little changed with banking shares underperforming while utilities are supporting. Investors seem to be getting used to uncertainty in Catalonia as peripherals return to positive.

Note: Market attention is turning to ECB minutes to be released at 07:30 am EDT and tomorrow's release of non-farm payroll (NFP).

U.S stocks are set to open unchanged.

Indices: Stoxx600 -0.3% at 389.3, FTSE +0.1% at 7477, DAX -0.2% at 12940, CAC-40 -0.1% at 5359, IBEX-35 +0.4% at 10005, FTSE MIB -0.1% at 22429, SMI -0.3% at 9254, S&P 500 Futures flat

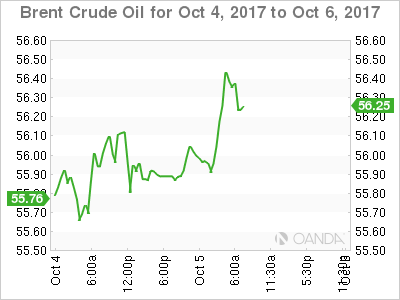

2. Oil steady as talk of new OPEC deal balances U.S exports, gold unchanged

Oil prices are steady on expectations that Saudi Arabia and Russia would extend production cuts, although record U.S exports and the return of supply from a Libyan oilfield are dragging on the market.

Brent crude is up +20c at +$56.00 a barrel, while U.S light crude (WTI) is unchanged at +$49.98.

Note: Both crude benchmarks have fallen more than -5% over the last week as investors booked profits after almost three months of gains.

The Energy Information Administration (EIA) said yesterday that U.S crude oil exports jumped to +1.98m bpd last week, surpassing the +1.5m bpd record set last week.

Ahead of the open, gold is holding steady within a tight trading range as the ‘mighty' dollar holds firm on stronger U.S services sector growth data Wednesday, as investors wait for tomorrow's key U.S employment data. Spot gold is at +$1,274.11 an ounce.

3. Sovereign yields remain atop lofty heights

Firming expectations that the Fed will hike rates in December coupled with domestic data pointing to steady growth in the U.S and talk of a potentially more ‘hawkish' successor to Fed Chair Janet Yellen is helping to support higher U.S yields.

Ten-year yields are trading atop of +2.33%; it's highest yield since mid-July, which has also pushed the dollar higher against G10 currencies. Elsewhere, Germany's 10-year yield gained +1 bps to +0.46%, the highest in a week, while

Spain's 10-year yield climbed less than +1 bps to +1.789%, the highest in more than six months.

Note: The volatility of Spanish government bonds is to become stronger; with yields potentially rising further versus its regional peers (Italian BTP yields) if the standoff between Catalonia's regional government and the central government escalates.

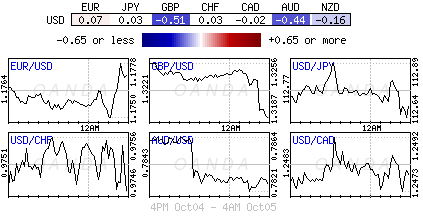

4. Dollar trades in a tight range

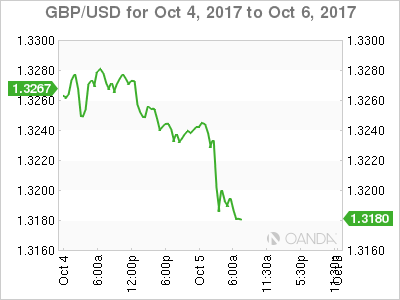

Sterling (£1.3190) is trading close to its three-week low on reports that over two dozen U.K members of parliament are prepared to call for PM May to resign before the end of 2017. With the Tory party conference concluded; the market focus has swung back to Brexit and the negotiations. Germany's BDI Industry Association noted that it had concern at current Brexit talks and added that German companies with presence in U.K must make provision for the possibility of a hard Brexit

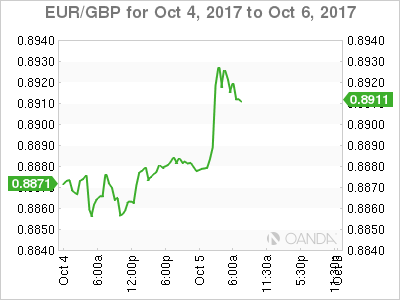

The EUR (€1.1766) trades steady despite the Spanish region of Catalonia threatening to declare independence next week. Should Catalonia turn independent, the E.U would have to apply the ‘Prodi doctrine' from 2004, suggesting Catalonia would leave the E.U and the Eurozone.

Down-under, AUD is trading atop of its two-month low outright (A$0.7820) after last nights Aussie retail sales headline missed market expectations -0.6% vs. +0.3% m/m.

5. U.K new car registrations slides in September

U.K. new car registrations fell sharply in the key month of September for the first time in six-years. New registrations fell -9.3% to +426,170 units. September is a key month of the year, which normally accounts for up to +20% of annual demand, making it highly likely sales this year will be down for the first time since 2011.

Business and political uncertainty is reducing buyer confidence, with consumers and businesses more likely to delay big ticket purchases.

The figures show a fall in registrations of petrol vehicles of -1.2%, with diesel declining by -21.7%, while demand for alternatively fuelled vehicles was up +41%. Year-to-date, new car registrations have fallen -3.9%.

Catalan Independence Threat Shaking Investors | US NFP And Trump Pick Under Focus

Traders are mindful of Catalonian Independence news could hit the newswire anytime

The US ADP data is always parsed for hints about the upcoming US NFP number

European markets and US futures are trading lower as investors are caught on Catalan independence situation. Even though Catalan President Carlos Puigdemont didn’t announce independence last night, which was widely expected of him, traders are mindful of the fact that the announcement could hit the newswire anytime. This datum is triggering the sell-off in the market. As long as the guessing game carries on, we expect the Spanish equity market to remain under pressure.

Over in the US, the US ADP data is always parsed for hints about the upcoming US NFP number (due tomorrow). There is a correlation between the ADP and NFP but not a strong one. Traders usually take their clues from the ADP number. The impact of the hurricanes was prominent. Companies employed the least number of workers (135K) in a year. Back in 2005, Hurricane Katrina had an even worse influence on the ADP number as it was pushed into the negative territory. Similarly, Hurricane Sandy wasn’t pleasing either as the ADP printed 130K in November 2012, which was below from the three month average of 189K.

We expect the US non-farm to yield a number which could be below the consensus forecast of 60K. Small businesses have felt the most influence of destruction caused by Irma which hit Florida in September. However, past experience explains that this negative impact does fade away fairly quickly and the evidence of this can be seen in the auto sales number which has experienced a sharp rise. We expect developers to hire more workers to construct and rebuild the impacted areas.

The dollar rally is dependent on two things; the economic data and Trump’s pick for the next Fed chair. Despite the blowout ISM non-manufacturing number yesterday, the dollar index hasn’t exploded and this tells us that the economic data isn’t providing the kind of tail which helped the dollar rally. So, it must be Trump’s pick for the next Fed chair. It is almost given that how the market could perceive each candidate depends on who becomes the next Fed chairperson. Kevin Warsh is perceived as the most hawkish person amid other candidates which would trigger flattening treasury yield and aggressive rate hikes. Yellen coming back would keep the volatility suppressed.

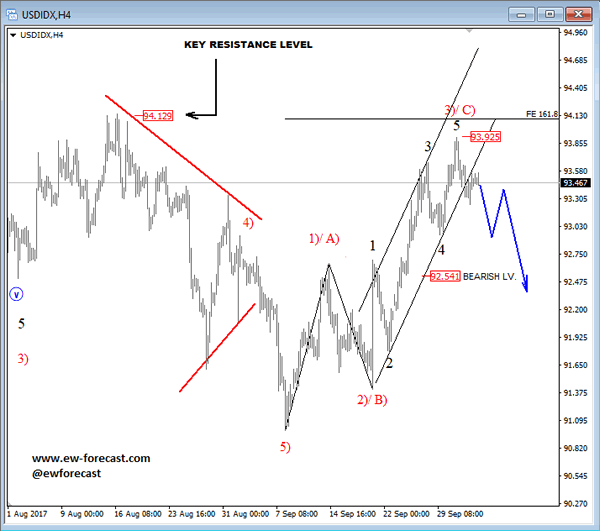

Elliott Wave Analysis: USD Index Can Face A Reversal

USD Index touched levels near the 93.92 level and later made a new intra-day drop lower. This intra-day fall can now be an early indication of a completed three-wave recovery and more weakness to follow. If that is the case and price breaches below the 92.54 level then we would be certain that more weakness will follow and that price completed a three-wave recovery. A decisive breach below the lower channel line would also be a confirmation for a change in trend.

USD Index, 4H

Market Update – European Session: Hard Brexit Concerns Resurface, Spain Bond Auction Results Seen As ‘Solid’

Notes/Observations

UK Tory Party conference failed to unify the party

Catalonia threatens to declare independence next week; Central govt assures it won’t happe

Spain's launch of a new five-year government bond prompted solid demand

Overnight

Asia:

Australia Aug Retail Sales miss expectations (M/M: -0.6% v +0.3%e)

Shanghai Composite and Korea Kospi remained closed for Golden Week; Hang Seng closed for holiday as well

Europe:

Spain region Catalan govt President Puigdemont stated that was obliged to apply the results of the independence referendum; to seek a mediation process. Catalonian Govt to discuss the outcome of region’s referendum in an extraordinary session on Monday, Oct 9th

Spanish PM Rajoy said to be threatening to trigger Article 155 of the constitution which allowed the central government to force a region to obey laws when disobedience “gravely threatened the general interest of Spain.” 155 had never been used.

S&P rating agency placed Catalonia B+/B ratings on CreditWatch negative; saw risk that escalation with Spain’s govt might damage the coordination and communication between the two govts which was essential for Catalan to service its debt on time and in full

Over two dozen UK members of parliament said to be prepared to call for PM May to resign; could be out of office before end of year

Americas:

Sec of State Tillerson refutes press specuklation that he might resign. Stated that he was committed to the President and the country

US Senate advanced nomination of Randall Quarles to be member of Fed Board of Governors with vote next Thursday, Oct 12th (**Reminder: Fed Vice Chair Fischer to step down on or around Oct 13th)

Economic data

(NL) Netherlands Sept CPI M/M: -0.2% v +0.2%prior; Y/Y: 1.6% v 1.5%e

(NL) Netherlands Sept CPI EU Harmonized M/M: -0.4% v +0.2%prior; Y/Y: 1.4% v 1.7%e

(IN) India Sept PMI Services: 50.7 v 47.5 prior (1st expansion in 3 months); PMI Composite: 51.1 v 49.0 prior

(CH) Swiss Sept CPI M/M: 0.2% v 0.2%e; Y/Y: 0.7% v 0.6%e

(CH) Swiss Sept CPI EU Harmonized M/M: +0.2% v -0.1% prior; Y/Y: 0.8% v 0.5% prior

(SE) Sweden Aug Industrial Production M/M: -1.7% v -0.3%e; Y/Y: 7.3% v 10.0%e

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) sold total €4.3B vs. €3.75-4.5B indicated range in 2022 and 2029 bonds

Sold €3.21B in new 0.45% Oct 2022 SPGB; Avg yield: 0.530% v 0.213% prior, Bid-to-cover: 2.12x v 1.88x prior

Sold €1.09B in 6.0% Jan 2029 SPGB; Avg Yield: 1.867% v 1.880% prior, bid-to-cover: 2.5x v 1.67x prior

(ES) Spain Debt Agency (Tesoro) sold €304M vs. €250-750M indicated range in 1.80% Nov 2024 I/L bonds (Bonoei/SPGbi); Real Yield: -0.520% v 0.113% prior; Bid-to-cover: 3.2x v 1.99 prior

(FR) France Debt Agency (AFT) sold total €8.498B vs. €7.5-8.5B indicated range in 2025, 2028 and 2048 Oats

Sold €2.735B in 1.00% Nov 2025 Oat; Avg Yield: 0.46% v 0.64% prior; Bid-to-cover: 1.99x v 2.34x prior

Sold €4.00B in 0.75% May 2028 Oat; Avg Yield: 0.88% v 0.67% prior; Bid-to-cover: 1.85x v 1.99x prior

Sold €1.765B in 2.00% May 2048 Oat; Avg Yield: 1.82% v 1.79% prior, Bid-to-cover 1.78x v 1.57x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.3% at 389.3, FTSE +0.1% at 7477, DAX -0.2% at 12940, CAC-40 -0.1% at 5359, IBEX-35 +0.4% at 10005, FTSE MIB -0.1% at 22429, SMI -0.3% at 9254, S&P 500 Futures flat]

Market Focal Points/Key Themes: European indices open down but reverse course as the session progressed; banking shares underperform while utilities supported; markets getting used to uncertainty in Catalonia and peripherals return to positive; Israel closed for holiday; attention turning to ECB minutes to be released later today and tomorrow's release of NFP in the US; earnings releases in the upcoming US session include Constellation Brands and Costco.

Equities

Consumer discretionary: DFS Furniture DFS.UK -4.3% (results), Norwegian Air NAS.NO -3.1% (traffic data), Scout24 G24.DE -0.4%(stake sale)

Industrials: Assa Abloy ASSAB.SE -4.8% (CEO considering resignation), Evonic EVK.DE +1.2% (analyst action), Technotrans TTR1.DE -2.1% (analyst action)

Financials: Credito Valtellinese CVAL.IT -9.2%(analyst action)

Technology: Osram Licht OSR.DE -0.7% (Stake sale)

Telecom: Telecom Italia TIT.IT +2.5% (potential asset sale)

Healthcare: Cosmo Pharmaceuticals +3.1% (FDA NDA approval), TiGenix TIG.BE 1.5% (study results)

Energy: Electricite de France EDF.FR +4.3% (analyst action)

Speakers

SNB President Jordan: Inflation remained very, very weak; need to continue with current monetary policy of negative rates and FX intervention pledge. Forex market remained fragile; CHF currency (Franc) remained strong

ECB’s Praet (Belgium): Sustainable convergence needed for Euro adoption

UK govt stated that resignation of PM May was not an issue (refutes recent press concerns)

Italy Stats Agency (Istat) Monthly Economic Note: Domestic growth picking up aided by manufacturing and investment

Spain Fin Min De Guindo: Catalonia independence will NOT happen, independence was irrational would be very harmful for Catalonia. Spain govt will enforce the law perfectly. Reiterated view that Catalan banking sector was solvent but banks could leave region if process goes further

Germany BDI Industry Association: Looking with concern at current Brexit negotiations. British govt lacking clear concept despite a lot of talk. German companies with presence in UK must make provision for the possibility of a hard Brexit

Turkey President Erdogan: Those who open the way for Kurdish referendum will pay

Turkey Dep PM Simsek: Monetary policy has been tight since Q4 2016 and would continue to be so. Saw CPI under 10% by end of 2017 (**Note: Sept YoY reading was 11.2%)

Japan PM Abe adviser Hamada: Supports planned timeline of planned hike in sales tax

Currencies

GBP exhibited weakness. Some dealers attributed its tone to reports that over two dozen UK members of parliament were prepared to call for PM May to resign before the end of 2017. Also the focus returned to the state of Brexit negotiations after Tory Party conference was now out of the way. Germany BDI Industry Association noted that it had concern at current Brexit negotiations and added that German companies with presence in UK must make provision for the possibility of a hard Brexit

EUR/USD was steady despite Spain region of Catalonia threatening to declare independence next week. Analysts noted that should Catalonia turn independent, the EU would have to apply the ‘Prodi doctrine’ from 2004, suggesting Catalonia would leave the EU and the Eurozone

Fixed Income

Bund futures trades at 161.29 down 3 ticks, recovering from early losses filling the morning gap to 161.13 after a well received Spanish auction. A move back lower paves the way to 160.65 base, while continued momentum higher sees 161.40.

Thursday's liquidity report showed Wednesday's excess liquidity rose to €1.787T from €1.778T prior. Use of the marginal lending facility rose to €615M from €344M.

Corporate issuance saw $4.5B come to market via 5 issuers bringing week to date issuance to above $11B. Issuance was headlined by BNS $1.25B issuance and Braskem $1.75B 2 part offering.

Looking Ahead

05:30 (ZA) South Africa Sept SACCI Business Confidence: No est v 89.6 prior

05:30 (UK) DMO to sell £2.75B in 0.75% July 2023 Gilt

05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month Bills

05:30 (HU) Hungary Debt Agency (AKK) to sell Floating Bonds

06:00 (IE) Ireland Sept Live Register Monthly Change: No est v -7.3K prior

06:00 (IE) Ireland Aug Industrial Production M/M: No est v 1.8%; Y/Y: No est v -9.5% prior

06:45 (US) Daily Libor Fixing

07:00 (ZA) South Africa Aug Electricity Production: No est v-1.8% prior; Electricity Consumption Y/Y: No est v -1.5% prior

07:30 (US) Sept Challenger Job Cuts: No est v 33.8K prior; Y/Y: No est v 5.1% prior

07:30 (EU) ECB account of the monetary policy meeting (Sept Minutes)

07:30 (CL) Chile Aug Economic Activity Index (Monthly GDP) M/M: 0.7%e v 0.9% prior; Y/Y: 2.1%e v 2.8% prior

08:00 (CL) Chile Aug Nominal Wage M/M: No est v 0.6% prior; Y/Y: No est v 5.8% prior

08:05 (UK) Baltic Dry Bulk Index

08:15 (FR) ECB’s Coeure (France) on panel in Frankfurt

08:30 (US) Initial Jobless Claims: 265Ke v 272K prior; Continuing Claims: 1.95Me v 1.934M prior

08:30 (US) Aug Trade Balance: -$42.7Be v -$43.7B prior

08:30 (CA) Canada Aug Int'l Merchandise Trade (CAD): -2.7Be v -3.0B prior

08:30 (US) Weekly USDA Net Export Sales

09:00 (MX) Mexico Sept Consumer Confidence: 86.0e v 88.5 prior

09:00 (RU) Russia Gold and Forex Reserve w/e Sept 29th: No est v $427.1B prior

09:00 (RU) Russia Sept CPI data

09:10 (US) Fed’s Powell (voter, neutral)

09:15 (US) Fed’s Williams (non-voter)

10:00 (US) Fed’s Harker (voter, hawk) at conference

10:00 (US) Aug Final Durable Goods Orders: 1.7%e v 1.7% prelim; Durables Ex Transportation: 0.2%e v 0.2% prelim

10:00 (US) Aug Factory Orders: +1.0%e v -3.3% prior; Factory Orders (Ex Transportation): No est v 0.5% prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (US) Treasury announcement for upcoming issuance during week of Oct 9th (3-year, 10-year and 30-year bonds)

12:00 (UK) BOE’s McCafferty

13:30 (UK) BOE’s Haldane (chief economist)

15:00 (MX) Mexico Citibanamex Survey of Economists

16:30 (US) Fed’s George (non-voter, hawk) at conference

CRUDE OIL Declining Towards $50

Crude oil is pushing lower towards $50 level. Key support is given at 45.40 (17/08/2017 high). Strong resistance found at 52.43 (26/09/2017) has been broken. Expected to show continued weakness.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Selling Pressures

Silver is weighing down. Hourly resistance is given at 16.89 (04/10/2017 high) while hourly support can be found at 16.54 (04/10/2017 high). Expected to show further bearish move.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Bouncing Higher On Strong Support

Gold is monitoring hourly support given at 1267 (15/08/2017 low). Hourly resistance is located at 1357 (08/09/2016). Stronger support lies at 1204 (10/07/2017 high). Expected to show further monitoring of support at 1267.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).