Sample Category Title

Dollar Reverses Losses after Chicago PMI Beat; Pound Slips as GDP Growth Disappoints

In a relatively busy data session, investors turned their attention back to the economic calendar, while concerns over Trump's tax proposals continued to weigh on the markets. Disappointing US inflation readings had a moderate impact on the dollar as markets were optimistic that the Fed would deliver another rate hike in December after Fed Chair, Janet Yellen, supported on Tuesday a gradual rate hike despite the weakness in inflation. The pound was the worst performer following weaker GDP growth readings.

The core PCE price index which is the Fed's preferred inflation measure added losses to the dollar on Friday after September's estimates appeared weaker than anticipated. While forecasts for the annual rate stood at August's mark of 1.4%, the index edged down by 0.1 percentage points to 1.3%, a level last seen in November 2015.

On the other hand, the Chicago PMI for the aforementioned month shot up to 65.2, approaching the 3-year highs reached in June and surpassing sharply the forecast of 58.5. This offset the dollar's earlier losses, pushing its index up to 93.21.

Dollar/yen pared half of yesterday's losses, jumping 0.22% on the day to 112.56.

According to the Office for National Statistics the final annual GDP growth for the UK missed the expectations of 1.7%, falling by 0.5 percentage points to 1.5% in the second quarter and touching the lowest growth since 2013 due to a weaker service sector in July. However, the quarterly basis figure remained unrevised at 0.3%, slightly up from the 0.2% reported in the first quarter.

Household savings ratio stuck at historically low levels in the second quarter at 5.4% despite the agency upwardly revising the previous mark of 1.7% to 3.8% due to errors in calculations.

Despite the fifth-largest economy growing slowly, the data might not change the BOE's intentions to raise rates soon. The Bank of England's Governor, Mark Carney, speaking on BBC radio on Friday reiterated that interest rates are likely to move upwards in "the relatively near term" but to a "limited extend" if the economy maintains its current performance. Yet, he did not confirm whether this would emerge at the November's MPC meeting.

The pound, however, failed to gain on Carney's remarks, falling to $1.3354 before rebounding to $1.3408. Euro/pound changed hands at a one-week high of 0.8841.

Initial Eurozone CPI readings for the month of September were just a shy lower than the forecast, hinting for a gradual removal of monetary stimulus. Headline inflation stood flat at 1.5% y/y, while analysts anticipated prices to pick up by 1.6%. Excluding food and energy items, the core equivalent was unchanged at 1.3%, whereas analysts projected for prices to grow at August's rate of 1.2%. A day earlier, ECB chief economist Peter Praet argued that the ECB will discuss recalibration and not termination of the asset purchase program.

In other data out of the Eurozone, German unemployment fell surprisingly to a record low of 5.6% in September in contrast to retail sales which came in disappointing.

Euro/dollar breached above 1.1800 key level, trading higher by 0.25% on the day at 1.1810.

After four months of increases, the monthly Canadian GDP growth numbers in July indicated that the economy neither expanded or contracted, driving dollar/loonie up by 0.30% to 1. 2463.This was below the 0.1% expected and the 0.3% reported in June.

EUR/USD On The Run

The currency pair increased significantly today and resumed the yesterday's bullish candle. The today's increase will invalidate the Wednesday's breakdown, that's why we may have another bullish momentum in the upcoming days. Price is trading in the green and tries to climb much higher as the dollar index dropped further today.

The USDX is trading in the red and is under selling pressure on the short term again. The index has found strong resistance and 93.68, much below the 93.81 static resistance and now goes down and could retest the 92.49 horizontal support before will try to climb higher again.

The Euro increased despite some poor Euro-zone data, the German Retail Sales dropped by 0.4%, even if the traders have expected to see a 0.5% growth. Moreover, the Euro-zone CPI Flash Estimate increased only by 1.5%, less versus the 1.6% estimate, while the Core CPI Flash Estimate surged only by 1.1%, less versus the 1.2% estimate.

Price failed to stabilize below the median line (ML) of the minor black ascending pitchfork and below the median line (ml) of the minor descending pitchfork. A retest of the ML will confirm a further increase in the upcoming period, the next target will be at the upper median line (uml) of the descending pitchfork.

The pair is trapped within the 1.2041 horizontal resistance and the 1.1711 static support, could move in range between these levels in the upcoming period after the failure to approach and reach the median line (ML) of the major ascending pitchfork.

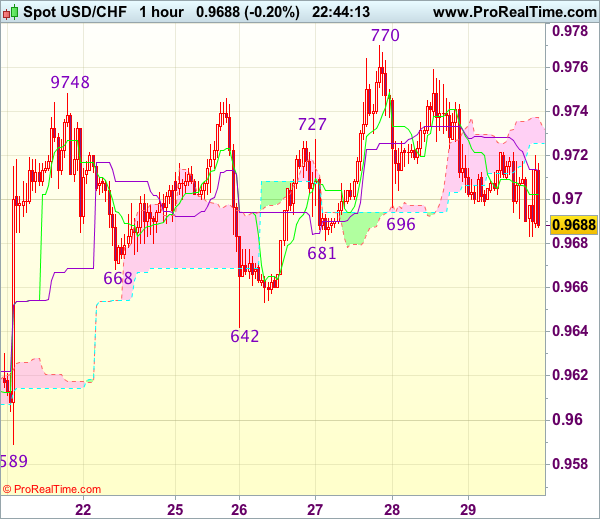

USD/CHF Another False Breakout

Price failed to stay above the second warning line and now could drop deeper in the upcoming days. USD/CHF is somehow expected to drop in the upcoming days after the failure to make new highs and to jump above the 0.9771 previous high. The failure to reach and retest the upper median line (uml) of the descending pitchfork could send the rate very fast towards the median line (ml) of the descending pitchfork.

GBP/JPY Further Drop In The Cards

The GBP/JPY is trading in the red on the short term, could drop further after the false breakout above the 151.66 horizontal resistance. You can see that has come back to retest the mentioned resistance and now goes down. The first downside target will be at the 150% Fibonacci line, a breakdown below it will open the door for more declines.

Trade Idea Wrap-Up: USD/CHF – Sell at 0.9705

Due to holidays, next update will be posted on Oct 9.

USD/CHF - 0.9677

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9696

Kijun-Sen level : 0.9707

Ichimoku cloud top : 0.9737

Ichimoku cloud bottom : 0.9726

New strategy :

Sell at 0.9705, Target: 0.9605, Stop: 0.9740

Position : -

Target : -

Stop : -

The greenback continued meeting resistance around 0.9720 and has slipped again in NY morning, suggesting top has possibly been formed at 0.9770 earlier this week and downside bias is seen for test of support at 0.9642, however, break there is needed to add credence to this view and extend fall to 0.9620, then towards previous support at 0.9589 which is likely to hold from here.

In view of this, we are looking to sell dollar on recovery as 0.9700-05 should limit upside and bring another decline later. Above 0.9720-25 would suggest an intra-day low is formed, bring rebound to 0.9750 but still reckon strong resistance at 0.9770-73 would hold from here.

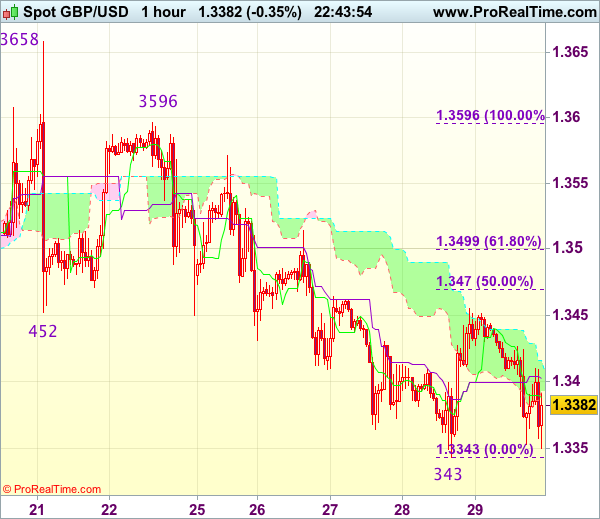

Trade Idea Wrap-up: GBP/USD – Hold long entered at 1.3375

Due to holidays, next update will be posted on Oct 9.

GBP/USD - 1.3399

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3388

Kijun-Sen level : 1.3403

Ichimoku cloud top : 1.3416

Ichimoku cloud bottom : 1.3393

Original strategy :

Bought at 1.3375, Target: 1.3475, Stop: 1.3340

Position : - Long at 1.3375

Target : - 1.3475

Stop : - 1.3340

New strategy :

Hold long entered at 1.3375, Target: 1.3475, Stop: 1.3340

Position : - Long at 1.3375

Target : - 1.3475

Stop : - 1.3340

Although cable retreated after meeting resistance at 1.3455 and initial downside risk is seen, as long as support at 1.3343 holds, mild upside bias remains for another rebound, above said resistance would extend the rebound from 1.3343 to 1.3470 (50% Fibonacci retracement of 1.3596-1.3345), however, reckon resistance at 1.3514 would limit upside and price should falter well below resistance at 1.3571, bring another decline later.

In view of this, we are holding on to our long position entered at 1.3375. Only below said support at 1.3343 would abort and signal the selloff from 1.3658 top has resumed and extend weakness to previous resistance at 1.3329, then towards 1.3300.

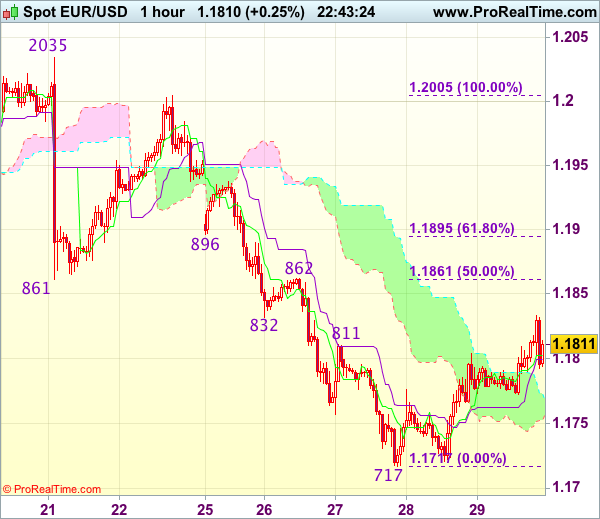

Trade Idea Wrap-up: EUR/USD – Sell at 1.1855

Due to holidays, next update will be posted on Oct 9.

EUR/USD - 1.1818

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.1803

Kijun-Sen level : 1.1800

Ichimoku cloud top : 1.1773

Ichimoku cloud bottom : 1.1752

Original strategy :

Sell at 1.1855, Target: 1.1735, Stop: 1.1890

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1855, Target: 1.1735, Stop: 1.1890

Position : -

Target : -

Stop : -

Euro’s rebound after holding above support at 1.1717 has retained our view that consolidation above this level would be seen and marginal gain from here cannot be ruled out, however, reckon upside would be limited to 1.1850 and renewed selling interest would emerge below 1.1861-62 (50% Fibonacci retracement of 1.2005-1.1717 and previous resistance), bring another decline later, below 1.1770-75 would bring weakness to 1.1740-45, break there would bring retest of said support at 1.1717, below there would signal the decline from 1.2093 top has resumed and extend weakness to 1.1700 but loss of downward momentum should prevent sharp fall below previous support at 1.1662 and reckon 1.1625-30 would hold.

In view of this, we are looking to sell euro on recovery as 1.1850-55 should limit upside and bring another decline. A firm break above previous support at 1.1832-38 (now resistance) should hold and bring another decline later. Above resistance at 1.1862 would abort and signal low is formed instead, bring a stronger rebound to 1.1896 (another previous support).

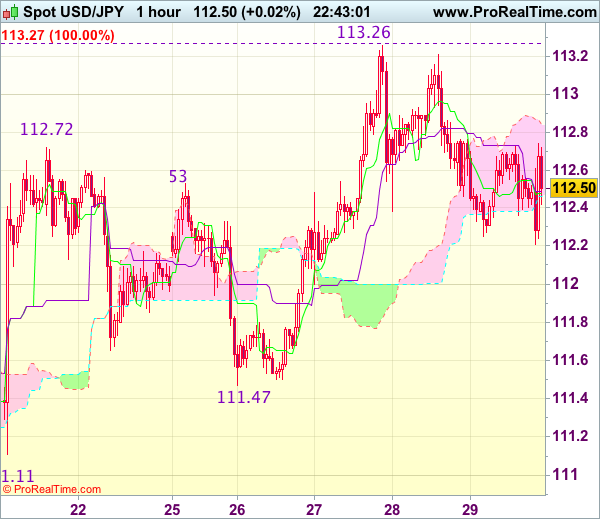

Trade Idea Wrap-up: USD/JPY – Stand aside

Due to holidays, next update will be posted on Oct 9.

USD/JPY - 112.48

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 112.48

Kijun-Sen level : 112.49

Ichimoku cloud top : 112.84

Ichimoku cloud bottom : 112.46

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling to 112.21, lack of follow through selling suggests further consolidation would take place and recovery to 112.75-80 cannot be ruled out, however, price should falter below indicated resistance at 113.26, bring another retreat later, below 112.20 would signal top has been formed at 113.26, bring retracement of recent rise to 112.00, then 111.75-80 but previous support at 111.47 should remain intact.

On the upside, whilst recovery to 112.75-80 cannot be ruled out, reckon said resistance at 113.26 would hold and bring further consolidation. Only a break of said this week’s high at 113.26 would revive bullishness and signal recent upmove has resumed, then further gain to previous resistance at 113.58 would follow but loss of upward momentum should prevent sharp move beyond 113.75-80 and reckon 114.00-10 would remain intact. As near term outlook is mixed, would be prudent to stand aside for now.

Trade Idea: EUR/GBP – Sell at 0.8930 or buy at 0.8670

Due to holidays, next update will be posted on Oct 9.

EUR/GBP - 0.8832

Original strategy :

Sell at 0.8890, Target: 0.8740, Stop: 0.8930

O.C.O.

Buy at 0.8670, Target: 0.8820, Stop: 0.8610

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.8930, Target: 0.8750, Stop: 0.8970

O.C.O.

Buy at 0.8670, Target: 0.8820, Stop: 0.8610

Position : -

Target : -

Stop : -

As the single currency recovered after holding above support at 0.8746, suggesting consolidation above this level would be seen and corrective bounce to 0.8870 cannot be ruled out, however, reckon upside would be limited to 0.8899 and 0.8930-35 should hold, bring another decline later, below said support at 0.8746 would extend recent decline from 0.9307 top to extend weakness to 0.8690-95 (61.8% Fibonacci retracement of 0.8312-0.9307), having said that, loss of downward momentum should prevent sharp fall below 0.8670-75 (50% projection of 0.9226-0.8774 measuring form 0.8899) and bring rebound later.

In view of this, whilst we are looking to sell euro on recovery, we are inclined to turn long on subsequent decline as 0.8670-75 should limit downside. Below 0.8640-50 would risk weakness to 0.8600-10 but sharp fall below there should not be repeated and risk remains for another rebound to take place soon.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

USD Returns Part of this Week’s Gains

- European equities eked out modest to moderate gains, with the exception of Madrid that trades flat ahead of the referendum. US equities open little changed.

- Eurozone inflation rose by 1.5% Y/Y in September, unchanged from August and slightly below expectations. Core inflation surprised on the downside slowing to 1.1% Y/Y from 1.2% Y/Y. The outcome makes it slightly harder for the ECB to wind down its bond buying programme, but we don't expect a further delay.

- German unemployment slid to a record low in September in a sign that Europe's largest economy will continue to expand on the back of domestic spending. The jobless rate dropped to 5.6%, down from 5.7% in August. Number of jobless fell by a SA 23,000 to 2.506 million, beating the median estimate for a drop of 5,000.

- The UK economy expanded at a weaker 1.5% Y/Y pace in Q2 than the 1.7% Y/Y estimated before. The figures highlight the "notable slowdown" in growth in H1. It was the slowest growth pace since 2013.

- EC president Juncker has ruled out any chance that EU leaders will decide next month to unlock the next stage in Brexit talks. "By the end of October we will not have sufficient progress," he said, adding that "miracles" would need to happen to change this. However, he admitted that negotiations are making progress.

- BOE president Mark Carney confirmed that the BOE is close to raising interest rates at its November meeting, saying that they would rise so long as there was not a sudden and unexpected deterioration in economic data.

Rates

Bund corrects further up, but US Treasuries stall

Core bonds' upward correction resumed in early European dealings and bonds managed to hold on to marginal, (US), respectively modest (German) gains. We think that after the sharp sell-off for the best part of September, core bonds were ripe for an upward correction and that started in fact yesterday. Early EMU data releases were mixed with strong German labour market data on the one hand and weak German retail sales and weak French consumer spending on the other hand. The rise of Bunds coincided with falling equities and a rising EUR/USD, but when equities turned north, it didn't affect Bunds. The Bund made a last minor move higher on the weaker-than-expected EMU headline and core inflation. We don't expect it to have much impact on the ECB decision on asset purchases when they meet at the end of October. Bunds moved sideways shortly after the initial reaction and continued to go so till the closing of our report. The US Treasuries lagged Bunds on their way higher (effectively moving sideways throughout the session), but rose sluggishly to new minor intra-day highs after the release of slightly lower-than-expected US PCE deflators. However, US Treasuries traded soon lower again, little changed on the day. The US personal spending and income data were weak, but as expected.

At the time of writing, the German curve bull flattens with yields down 0.2 bp (2-yr) to 3 bps (30-yr). US yields are flat (2-yr) to 0.9 bp (10-yr) lower. The outperformance of German bonds is partly explained by catching up after strength of US Treasuries yesterday eve. In the intra-EMU bond market, 10-year yield spreads were little changed (between -1 and +2 bps). Spanish bonds only marginally underperformed despite Sunday's disputed Catalonian referendum and the increased tensions surrounding it. The risks of a Catalonian secession are small, but we would have expected some spread widening as it should be considered as a non-negligible tail risk. Markets are maybe a bit too sanguine.

Currencies

USD returns part of this week's gains.

Yesterday, the recent rise in core yields and in the dollar ran into resistance. Additional profit taking occurred today. Soft price data (in the US and the EMU) weighted more on the dollar than on the euro. EUR/USD tries to regain the previous range bottom at 1.1823. The loss of USD/JPY remains modest (112.30 area).

Asian equity markets ex-Japan traded in positive territory. Activity slowed as several markets including China prepared for holidays next week. Japan hovered around yesterday's closing level. Japanese eco data were mixed (see headlines). They gave the BOJ every reason to maintain its very loose monetary policy. The yen lost a few ticks after the data. USD/JPY traded in the 112.60 going into the start of European dealings. EUR/USD stabilized in the 1.1775 area.

Yesterday, the rise in US yields and in the dollar stalled and a modest countermove started as the was 'no strong enough' US news to extend the uptrend. This pattern continued today. From the start in Europe, the dollar lost gradually further ground. One might call it end of week profit taking even as the profit recent dollar profits still aren't that spectacular. Whatever, EUR/USD returned north of 1.18. USD/JPY drifted lower in the 112 big figure. EMU inflation (headline and core) both printed slightly softer than expected. The CPI release caused a temporary pause in the EUR/USD rebound, but the intraday trend resumed soon. Interest rates declined slightly more in Europe than in the US but differentials were too small to be significant for EUR/USD trading.

US spending and income data were weak as signalled by the retail sales data earlier this month. The PCE deflators were even a touch softer than expected at 1.4% Y/Y for the headline figure and 1.3% for the core. This is well off the Fed's 2% target. US yields and the dollar lost a few more ticks after the publication. EUR/USD is again testing the 1.1823 previous range bottom. A close above this level would be a disappointing for USD bulls. The losses in USD/JPY are modest. The pair is trading in the 112.40 area.

Is EUR/GBP bottoming out?

There were plenty of eco data in the UK today. Indicators showed a mixed picture but markets focused on two negative topics. UK Q2 growth was confirmed at 0.3% Q/Q but the Y/Y figure was reduced from 1.7% Y/Y to 1.5% Y/Y due to downward revision in Q3 and Q4 of 2016. The good post-Brexit performance of the UK economy was a bit good than assumed until now. At same time, output growth in the key UK services sector even declined 0.2% M/M in July. Sterling already felt some headwinds in the run-up to the data and the move accelerated afterwards. EUR/GBP extended its rebound north of 0.88. Admittedly, part of this move mirrored an overall rise of the euro. BoE's Carney in an interview indicated the BoE still intends a rate hike in the coming months. However, the rate hike talk was of little help for sterling anymore. EUR/GBP trades currently in the 0.8835 area. The pair is moving further away from the recent lows and from the 0.8742 support. A bottoming out process is developing. Cable dropped (temporary?) below the 1.34 mark, but the decline was retarded by a generally softer dollar. The pair trades again near the big figure.