Sample Category Title

Calm on the Macro Front

In focus today

From the US, December durable goods orders and January consumer confidence index from Conference Board are due for release. We will follow the latter for gauging how consumers feel about the economy and inflation as Trump begins his second term in the White House.

In the euro area, the bank lending survey from the ECB is scheduled for release.

In Hungary, the central bank will announce its policy rate - we and markets expect the central bank to leave the policy rate unchanged at 6.5%.

Economic and market news

What happened overnight

In the US, President Trump described DeepSeek, the Chinese AI start-up, as a "wake-up call" for US industries. He emphasised that US tech companies should focus intently on competing to win - and his desire to "unleash" US tech companies and "dominate the future like never before". Concerns over DeepSeek's AI model caused US stocks, particularly AI stocks such as Nvidia and Broadcom, to tumble yesterday. The emergence of DeepSeek, which develops AI models with lower development costs and without using the most advanced chips for training, raises questions about the US's ability to maintain its lead over China in this field. It also challenges US AI bellwethers to continue developing competitive AI models without relying on the most advanced chips.

In politics, Scott Bessent won Senate confirmation as Treasury secretary with a 68-29 vote. Bessent has previously reiterated his support for extending the Tax Cuts and Jobs Act, while also declining to commit to raising taxes on the highest-earning individuals.

What happened yesterday

In Germany, the Ifo index recorded a small increase in January due to a better assessment of the current economy situation while expectations declined. The assessment of the current business situation rose to 86.1, which is the highest level in five months. This signals a possible bottoming out of activity following the previous years' declining trend like the PMIs that exceeded 50 last week. However, with Ifo expectations declining to the lowest level in a year we continue to expect the German economy to stagnate in the first half of this year and then start growing in the second half due to lower monetary policy rates and rising real incomes.

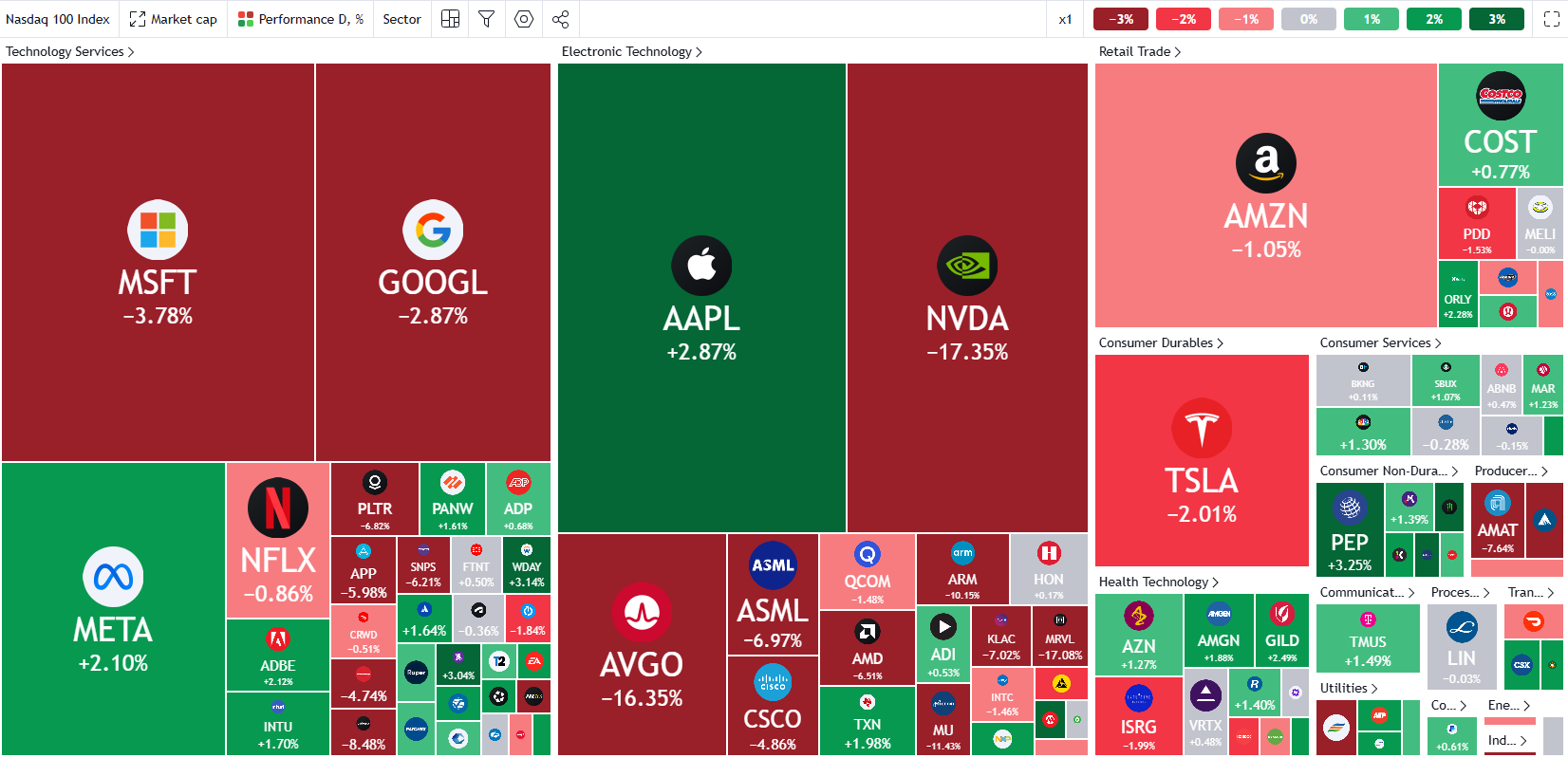

Equities: Global equities declined yesterday with significant dispersion. The Far East markets were higher, European markets remained largely unchanged, while the US markets suffered a substantial downturn. A closer look at US performance reveals notable differences, with the Dow rising by 0.7% and the Nasdaq falling by 3.1%. This highlights a micro-level narrative we mentioned yesterday, centred around DeepSeek. The Chinese AI maker's popular LLM model, R1, is potentially disrupting the AI world as we know it.

At company level, the biggest loser among the MAG 7 was Nvidia, which fell by 17%, while Meta, on the other hand, rose by 2%. Unsurprisingly, this is due to the initial analysis of which companies will potentially benefit from or be adversely affected by this development.

The next question that may gain attention in the coming days is whether this should be perceived as good or bad for equities overall. Yesterday, equities reacted negatively, but we argue that this development is incredibly positive from both an economic and inflation perspective and should therefore be seen as beneficial. Admittedly, many unknowns remain, and while we are not technical AI experts, based on the analysis we have seen so far, we confidently conclude that this will be net positive.

In the US yesterday, the Dow rose by 0.7%, the S&P 500 fell by 1.5%, the Nasdaq dropped by 3.1%, and the Russell 2000 decreased by 1.0%. Asian markets are mixed this morning, with Japan declining, while mainland markets in China are closed for the Lunar New Year. European futures are marginally higher this morning, while US futures are mixed, with the Nasdaq being slightly higher.

FI: Global bond markets took its cue from the equity market and the DeepSeek introduction as a catalyst for the global risk-off sentiment yesterday. The front end and the belly of the curve outperformed the long end with the 5y point down about 5bp in Europe and 9bp in the US. 10y Bund ASW widened 1.5bp to turn positive again for the first time in two weeks.

FX: EUR/USD was off to a strong start during yesterday's session breaching the 1.0500 mark, as easing tariff risk premia fuelled broad-based USD weakness. The recent risk-off sentiment, triggered by the tech sector sell-off, has favoured JPY and CHF over the USD, as declining US yields, narrowing rate differentials between the US and the rest of the G10, and equity outflows from the US weighed on the USD. Overnight, however, more broad-based universal tariffs were flagged by the Trump administration, pushing EUR/USD firmly back towards the 1.0400 mark, highlighting the cross' sensitivity to tariffs news. GBP was in for another day of gains as the fiscal induced risk premium slowly continues to fade. Oil prices fell sharply yesterday and have dropped firmly from recent highs putting additional pressure on oil-FX.

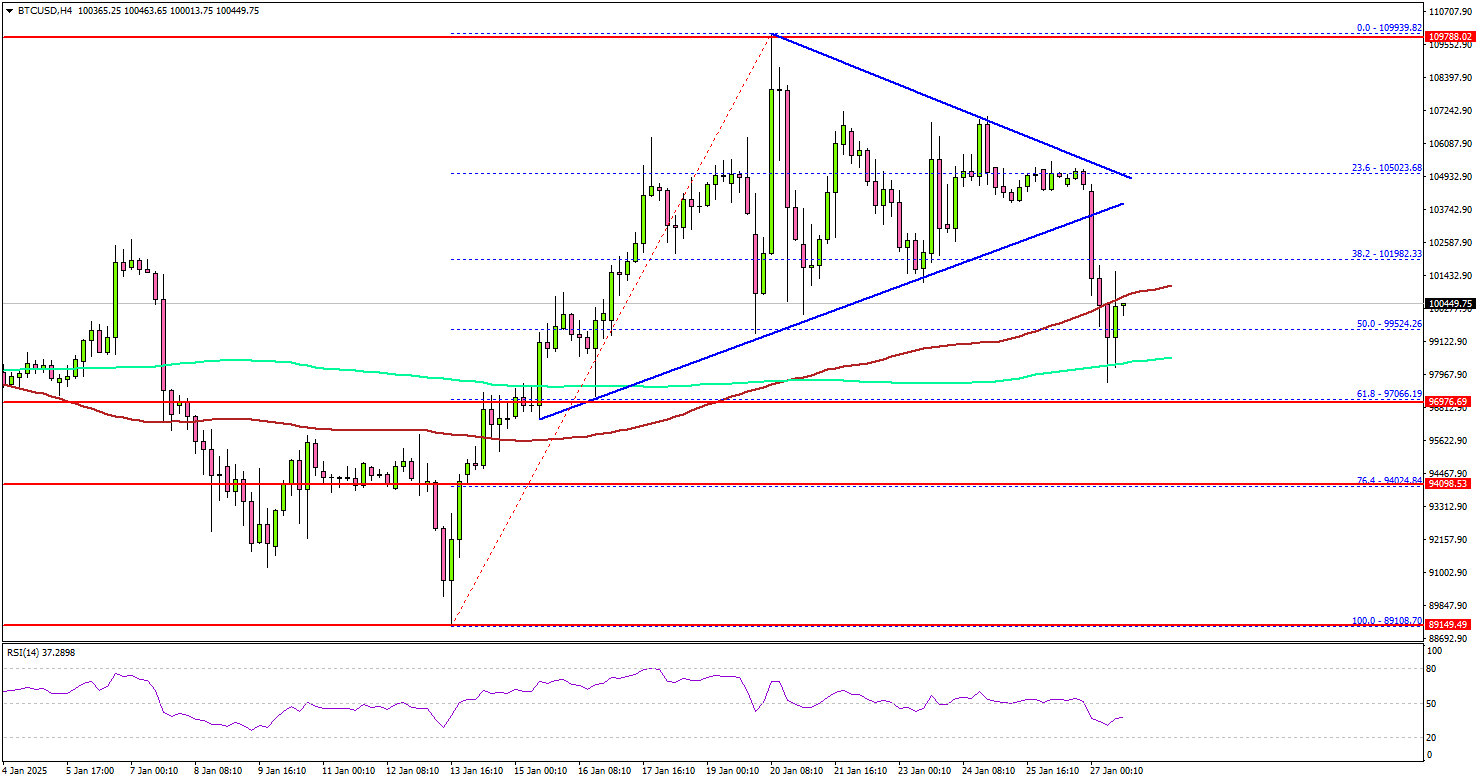

Bitcoin Takes a Dive: Will This Support Level Trigger a Rebound?

Key Highlights

- Bitcoin price started a fresh decline from the $109,939 high.

- BTC traded below a key contracting triangle with support at $103,750 on the 4-hour chart.

- Ethereum price also declined after the bears were active near the $3,500 zone.

- Gold rallied toward $2,785 before the bears appeared.

Bitcoin Price Technical Analysis

Bitcoin price failed to remain in a positive zone above $105,000 against the US Dollar. BTC started a fresh decline below $104,000 and $103,500.

Looking at the 4-hour chart, the price traded below a key contracting triangle with support at $103,750. There was a move below the 50% Fib retracement level of the upward move from the $89,108 swing low to the $109,939 high.

The price even spiked below the 100 simple moving average (red, 4-hour) and tested the 200 simple moving average (green, 4-hour). It is now consolidating losses above the 61.8% Fib retracement level of the upward move from the $89,108 swing low to the $109,939 high.

On the upside, the price could face resistance near the $102,000 level. The next key resistance is $103,500. A successful close above $103,500 might start another steady increase. In the stated case, the price may perhaps rise toward the $105,000 level.

Immediate support is near the $98,500 level. The next key support sits at $97,000. A downside break below $97,000 might send Bitcoin toward the $94,000 support. Any more losses might send the price toward the $92,000 support zone.

Looking at Ethereum, the bears remained active below the $3,500 resistance zone, resulting in a fresh decline.

Today’s Economic Releases

- US Housing Price Index for Nov 2024 (MoM) - Forecast +0.2%, versus +0.4% previous.

- US Durable Goods Orders for Dec 2024 – Forecast +0.2% versus -1.2% previous.

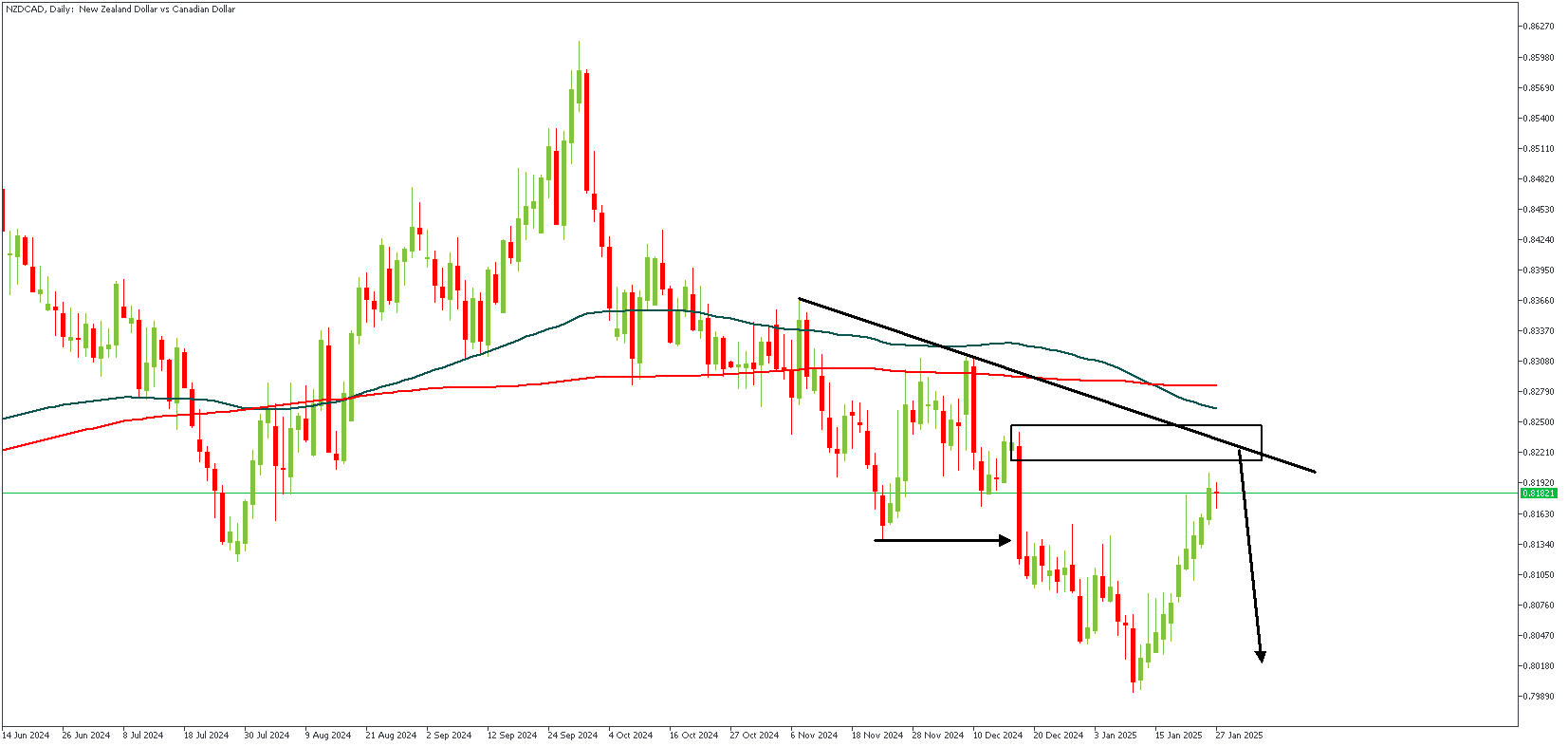

NZDCAD Price Action Breakdown

The NZDUSD pair has lost its recent gains and is trading near 0.5680 on Monday as market sentiment turns cautious. This pressure comes from reports that former US President Trump's advisers are pushing for 25% tariffs on Mexico and Canada starting February 1, with no plans for negotiations. Meanwhile, tensions with Colombia eased after the country agreed to US terms regarding deportation flights.

The US Dollar Index (DXY) has recovered from its monthly low and is trading near 107.70, adding to the Kiwi's struggles. Additionally, weaker-than-expected Chinese manufacturing data and the limited impact of China's new economic stimulus measures have further weighed on the New Zealand Dollar, given New Zealand's reliance on trade with China.

NZDCAD – D1 Timeframe

Crossing the 100-day moving average below the 200-day moving average is the initial factor leaning towards a bearish sentiment. In addition to that, however, we see the trendline resistance aligning well within the range of the rally-base-drop supply zone highlighted on the daily timeframe chart of NZDCAD. Since the price has already mitigated the Fair Value Gap (FVG) area, retesting the supply zone would be necessary to complete the puzzle.

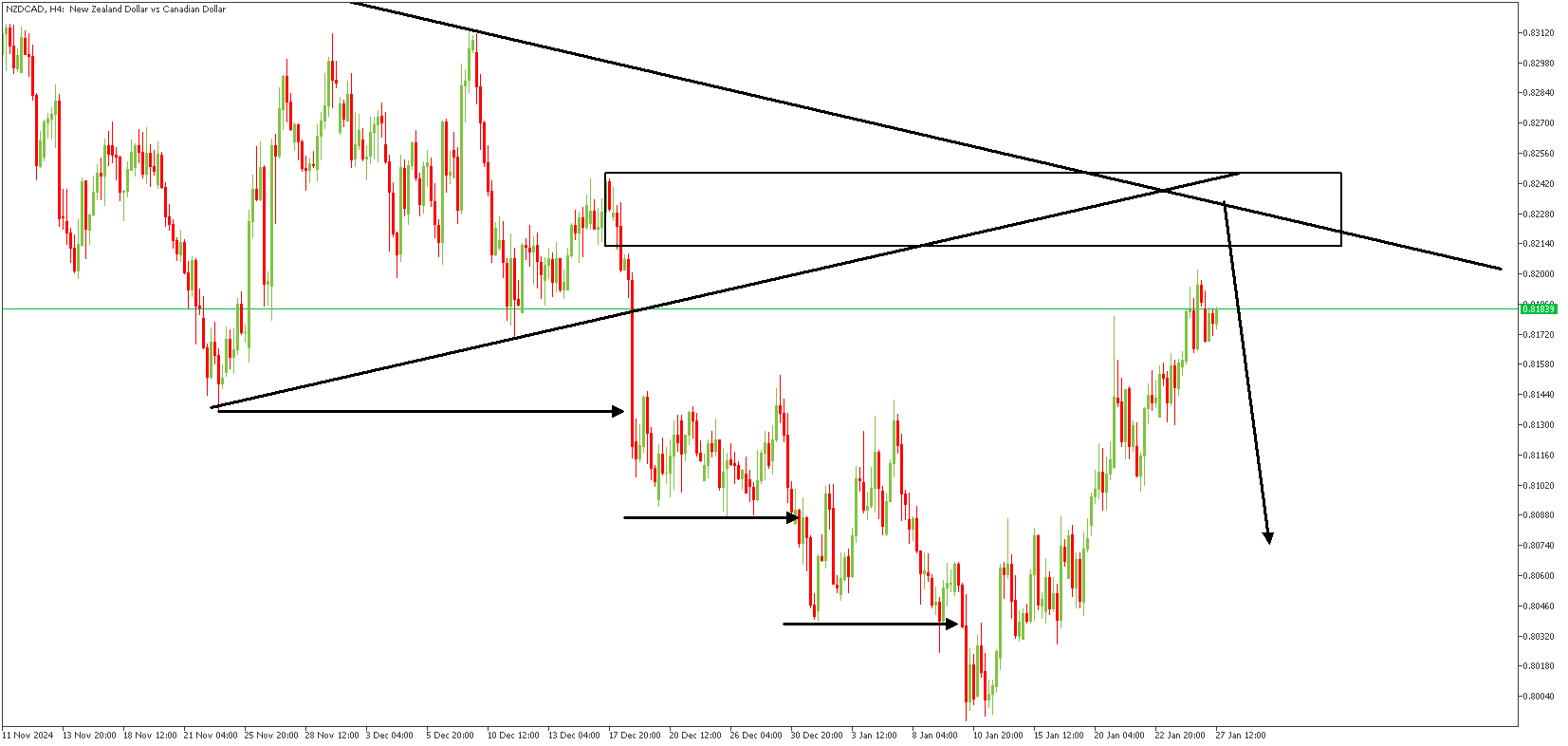

NZDCAD – H4 Timeframe

On the 4-hour timeframe chart, we discover that there are two resistance trendlines – not just one – and both intersect right within the region of the supply zone. The multiple bearish breaks of structure and the price's expected reaction from the supply zone would confirm a bearish entry.

Analyst's Expectations:

- Direction: Bearish

- Target: 0.80706

- Invalidation: 0.82582

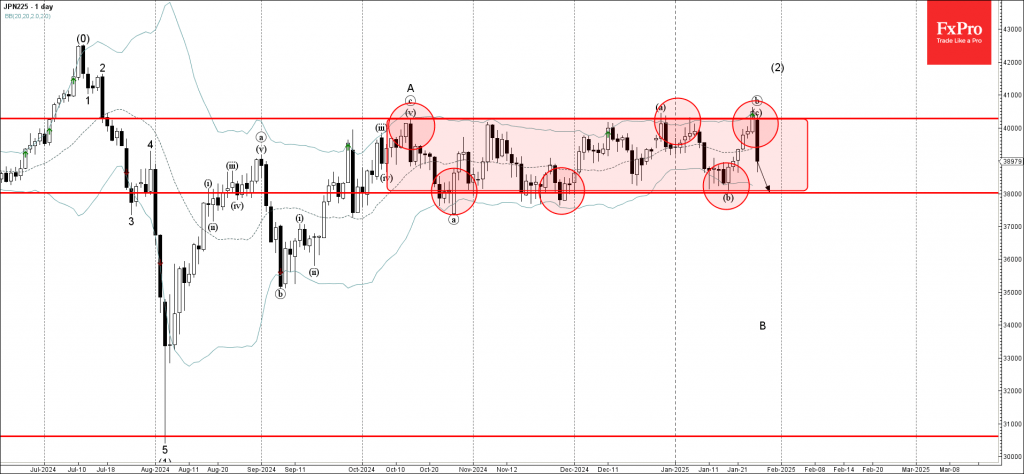

Nikkei 225 Wave Analysis

- Nikkei 225 fall inside sideways price range

- Likely to fall to support level 38025.00

Nikkei 225 index recently reversed down from the strong resistance level 40285.00 (upper border of the tight sideways price range inside which the pair has been moving since October) standing close to the upper daily Bollinger Band.

The downward reversal from the resistance level 40285.00 stopped the previous minor wave c, which started earlier from the lower border of this price range 38025.00.

Nikkei 225 index can be expected to fall to the next support level 38025.00 – from where the index is likely to correct up.

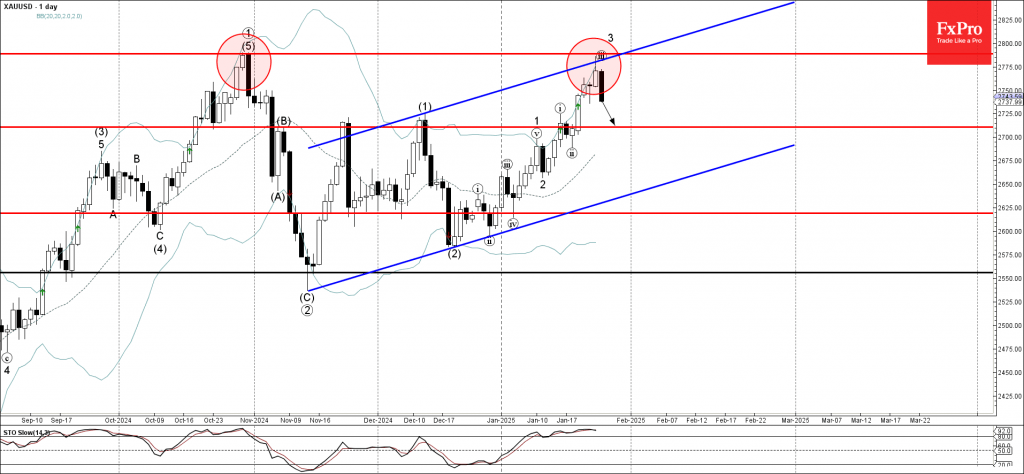

Gold Wave Analysis

- Gold reversed from resistance zone

- Likely to fall to support level 2711.00

Gold recently reversed down from the resistance zone between the key resistance level 2789.00 (former multi-month high from October), resistance trendline of the daily up channel from November and the upper daily Bollinger Band.

The downward reversal from this resistance zone will likely form the daily Japanese candlesticks reversal pattern Bearish Engulfing (strong sell signal for Gold), if the price closes today near the current levels.

Given the strength of the resistance level 2789.00 and the overbought daily Stochastic, Gold can be expected to fall to the next support level 2711.00.

DeepSeek vs. US Tech Giants: The Battle for AI Supremacy and Its Market Impact

- DeepSeek, a Chinese AI startup, has launched a new open-source AI model that is reportedly as good as top chatbots but significantly cheaper.

- This news triggered a selloff in US tech stocks, with Nvidia and other chipmakers experiencing significant drops.

- Despite the market reaction, it’s too early to determine if DeepSeek will be the new AI leader.

- Nasdaq 100 has rebounded, maintaining its bullish structure.

Global markets have started a busy week with a lot of volatility as the little-known Chinese artificial intelligence model called ‘DeepSeek’ sparked a selloff in AI-related shares, with megacap stocks including Nvidia the worst hit.

Chinese startup DeepSeek has launched a free assistant that uses cheaper chips and less data. This move seems to challenge the common belief in financial markets that AI will boost demand for everything from chipmakers to data centers. A bubble waiting to burst or is that a premature assumption? Let us take a look.

What is DeepSeek?

DeepSeek Artificial Intelligence Co., Ltd., started in 2023, is quickly becoming important in the world of AI. Based in China, DeepSeek focuses on pushing AI research forward. Their big goal is to create Artificial General Intelligence (AGI), which is AI that can understand, learn, and do tasks like a human in many different areas. Even though they’re just starting out, DeepSeek’s fast progress shows they’re serious about influencing the future of smart systems.

Origins and Mission

DeepSeek was founded during a pivotal time for AI, as breakthroughs in generative AI models like ChatGPT sparked global interest in advanced machine learning. Although the founders are not widely named, they reportedly include experienced professionals from China’s tech industry and academia, bringing together skills in AI research, software engineering, and strategic innovation. Their goal for DeepSeek is to move beyond the limits of narrow AI systems, which are great at specific tasks, by creating AGI that can generalize knowledge and adapt to new challenges.

The name “DeepSeek” means “deep exploration” or “in-depth pursuit,” highlighting its focus on foundational research and innovative applications. This mission aligns with China’s national strategy to lead in AI innovation, as outlined in initiatives like the Next Generation Artificial Intelligence Development Plan.

Technological Focus and Early Developments

DeepSeek focuses on several key areas in AI development:

AGI Research: DeepSeek works on technologies like large language models, reinforcement learning, and multimodal AI to create models that can think, be creative, and understand context.

Industry Applications: Besides AGI, DeepSeek makes useful AI tools for healthcare, finance, education, and self-driving systems. Their tools are being tested for things like medical diagnosis and personalized learning.

Ethical AI: DeepSeek focuses on ethical rules and safety measures to make sure AI is developed responsibly, following global standards.

Leadership and Shareholders

DeepSeek’s leadership team includes AI researchers, engineers, and executives with backgrounds in top Chinese tech companies and universities. The company hasn’t revealed its shareholders, but it’s probably supported by private investors, venture capital, and partners who share China’s AI goals. It’s possible, though not confirmed, that state-affiliated groups are involved, given the importance of AGI.

DeepSeek and its Open Source Model

Like its Western competitors Chat-GPT, Meta’s Llama, and Claude, DeepSeek uses a large-language model, which means it trains on huge amounts of text to understand everyday language.

However, unlike Silicon Valley companies that keep their models private, DeepSeek is open source. This means anyone can access its code, see how it works, and even change it.

Jim Fan, a senior research manager at Nvidia, said on X that DeepSeek is keeping the original mission of OpenAI alive by being truly open and empowering everyone.

DeepSeek claims it is the best among open-source models and competes with the most advanced closed-source models worldwide.

What Impact has DeepSeek Had on US Equities and Indices?

Over the weekend, DeepSeek created a buzz as tech analysts said the company’s AI model is better than the world’s top chatbots and costs only a tenth as much.

This saw the app surpass ChatGPT to become the No.1 app on the US app store. Released on January 20, 2025, DeepSeek gained popularity quickly thanks to countless threads on social media as well as its quality and price point.

All of these factors set DeepSeek apart from its peers.

Big Tech Rattled by DeepSeek as the Nasdaq fell 5% pre-market trading. Markets are concerned that a cheaper Chinese model could have a massive impact on US tech dominance.

According to DeepSeek, the company only spent around $5.6 million in developing their model, which is a pittance when compared to what US tech giants have poured into AI development and infrastructure.

This was reflected in companies such as NVIDIA which was down as much as 12% in pre-market trading stretching to 17% at the time of writing (four-month low). Other chipmakers such as Broadcom were down as much as 11%.

Source: TradingView (click to enlarge)

Another company that felt the sting was Japanese firm SoftBank, which is part of President Donald Trump’s AI investment drive. It was also down around 8% on Monday.

As much as we are seeing blood in the water today, this may be a knee-jerk reaction. It is still too early to declare DeepSeek as the new leader in the AI race but as one analyst put it, it certainly is a wake up call to America.

Technical Analysis – Nasdaq 100

From a technical standpoint, the Nasdaq 100 has recovered some of its pre-market losses having traded at a low of around 20660.

The Index also gapped down, so if you are taking the gap into account from Friday’s close, The Nasdaq 100 was down by as much as +- 7.5% at its lowest point.

The index appears to have found support of the 100-day MA and up about 500 points since. The bullish structure still remains intact without a daily candle close below the 20756 handle.

This does not mean that a daily candle close above this level means bulls will take charge once more but does leave the door open for a more sustained recovery and a push on toward fresh highs.

This week will bring US earnings as well, with Microsoft, Meta, Tesla and Apple due to announce their fourth-quarter earnings this week. Could this prove to be the catalyst to arrest this early week slump?

Nasdaq 100 Daily Chart, January 27, 2025

Source: TradingView (click to enlarge)

Support

- 21000

- 20795

- 20664 (100-day MA)

Resistance

- 21255

- 21637

- 22000

USDJPY: Fresh Acceleration Lower Cracks Important Supports

USDJPY edged higher after fresh acceleration lower in European session on Monday, hit new multi-week low.

Bears found footstep at 50% retracement of 148.64/158.87 upleg, but upside is likely to be limited, as broken supports at 154.96/76 (Fibo 38.2% / 55DMA) and 154.80 (bull-trendline) reverted to strong resistances.

Daily close below these levels to verify fresh bearish signal (also generated on break of the base of multi-day range.

Weaker technical picture on daily chart (14-d momentum falling deeper into negative territory / Tenkan/Kijun-sen bear cross) support bearish near-term outlook.

Close below trendline is seen as minimum requirement to keep bears in play for renewed attack at 151.71 (session low / Fibo 50%), violation of which to expose targets at 152.81/55 (200DMA / Fibo 61.8%).

Alternatively, bounce and close above 155.00 zone would sideline immediate bears and signal possible false break lower (formation of bear-trap).

Res: 154.96; 155.98; 156.46; 156.79

Sup: 153.71; 153.16; 152.81; 152.55

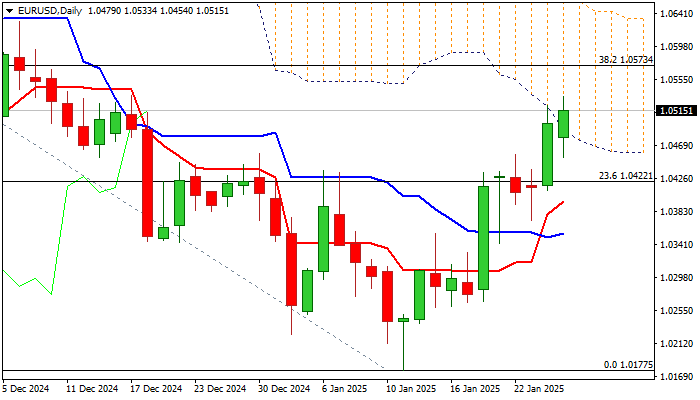

EUR/USD: Recovery Holds Grip, But Fed/ECB Policy Divergence May Obstruct Bulls

EUR/USD regained traction after overnight’s drop and rose above 1.05 handle, penetrating falling daily cloud (spanned between 1.0490 and 1.0664), after better than expected German January Ifo report boosted the sentiment.

Bulls look to resume recovery from Jan 13 low (1.0177) after reversal pattern has been completed on weekly chart (the pair was up 2.1% last week, in the biggest weekly advance since the second week of July 2023).

The action is underpinned by positive daily studies (daily Tenkan/Kijun-sen are converging after formation of bull-cross / strong positive momentum) with extension above Fibo barrier at 1.0573 (38.2% of 1.1214/1.0177) needed to verify signal and open way towards upper triggers at 1.0629/56 (Dec 6 lower top / cloud top).

However, recovery may face increased headwinds and risk of stall due to divergence of Fed and ECB monetary policies, as the US central bank is widely expected to stay on hold on policy meeting on Wednesday, while the ECB’s rate cut on Thursday is fully priced.

Also, dynamics of policy easing remains in favor on the ECB which is expected to cut by 75 basis points until June while Fed is seen easing policy by 50 basis points in 2025, although the first cut might be delayed and occur after June.

Res: 1.0534; 1.0573; 1.0629; 1.0656.

Sup: 1.0490; 1.0454; 1.0422; 1.0396.

Sunset Market Commentary

Markets

Not the start and the first measures from the Trump 2.0 administration nor a big eco data surprise and the anticipated central bank reaction, but a Chinese artificial intelligence start-up (DeepSeek) triggered the first big volatility moment of 2025. The AI language learning model of the Chinese company is said to provide high profile results comparable to its American competitors at a much lower price. It also questions the viability of massive capital investments in high-end chips and extensive computing power. This also questions elevated valuations for multiple companies working in the IT supply chain. European equities and US equity futures nosedived this morning.

The Nasdaq future at some point lost > 5.0%, but pressure eased slightly as US investors entered the fray. Even so, volatility remains elevated. The Nasdaq and the S&P 500 currently lose 3.0% and 1.75% respectively. The EuroStoxx 50 currently declines 0.75 %. For indices of several EU member states, declines remain limited (e.g. MIB +/- unchanged). The (predominantly US driven) equity sell-off also spilled over the other markets. US Treasuries serve as a preferred safe haven. US yields are off the intraday lows, but are still ceding between 7.0 bps (2-y) and 9 bps (5-y) in volatile trading. Declines in EMU yields are less pronounced with German yields ceding about 3-4 bps across the curve. German IFO business climate showed a mixed picture. The headline index improved (85.1 from 84.7) on an improvement in the current assessment, but German companies even gain turn more pessimistic on future expectations. The tone of the report after feels a bit disappointing after Friday’s PMIs. Despite the overall market turmoil, oil hardly declines further after a substantial correction since mid this month. Brent holds near $78 p/b).

On FX markets, the risk-off narrative is a bit less straightforward as is the case in equity and FI markets. With potential impact of the DeepSeek developments mainly questioning US AI/tech dominance, the dollar isn’t able to take up its traditional safe haven function. The yen outperforms among the majors with USD/JPY falling from an 156 close on Friday to currently trade near 154.2. In Europe, the Swiss franc stages a comeback after last week’s setback (EUR/CHF 0.945 from 0.951). Even the single currency reversed earlier intraday losses with EUR/USD rebounding from the 1.046 area to currently trade near 1.052 on broader USD selling. The impact of the US-instigated risk-off on smaller currencies also remains rather modest. EUR/GBP trades little changed in the 0.841 area. The Aussie dollar underperforms, both against the dollar (0.63) and the euro (EUR/AUD 1.672). The likes of the NOK and the SEK also incur modest losses against the euro, but are holding with recent ranges. A similar pattern also develops from CE currencies even as the damage remains fairly limited (EUR/CZK 25.10, EUR/HUF 409.0, EUR/PLN 4.22).

News & Views

More members of the National Bank of Poland’s monetary committee break with governor Glapinski’s (solo?) view that rate cuts will only be something for 2026. MPC Duda referred to room to cut the policy rate by the end of the year with Janczyk putting the option on the table as well. That makes at least 5 out of 9 members not ruling out a H2 2025 move. The July inflation report, coming after presidential elections and by that time presenting a more precise impact on fiscal policy (energy subsidies) on the path of inflation, seems to be the one to start readying a discussion on the topic. Rate cuts, if any, should remain small in size according to Duda (25 bps steps). EUR/PLN rebounds in today’s tough risk climate but preserves last week’s technical break below EUR/PLN 4.25 support.

EU foreign ministers agreed to extend again the sanctions on Russia. They have to do so every six months. EU foreign policy chief Kallas said that this way it will continue to deprive Moscow from revenues to finance its war. The deal came after Hungarian prime minister Orban lifted his opposition in place since December. He wanted to wait the inauguration (and reaction function) of Donald Trump together with getting several energy assurances. The EC will continue discussions with Ukraine on the supply to Europe through the gas pipeline system and is willing to associate Hungary and Slovakia in the process.