Sample Category Title

Forex: Risk-On Or Risk-Off?

The rhetoric continues between North Korea and the United States with North Korea's Foreign Minister, Ri Yong Ho, describing President Trump's recent comments as 'tantamount to a declaration of war' and even stating that Pyongyang reserved the right to take countermeasures that could include shooting down US bombers that are not inside Korea's air space. The White House was quick to deny such claims and Trump's Security Advisor has commented that the US has 4 or 5 different scenarios as to a resolution, stating that 'some are uglier than others'. Meanwhile, China's Ambassador to the United Nations has stated that the situation is 'getting too dangerous'. As the 'war of words' continues the markets will be evaluating risk and will act accordingly.

ECB President Mario Draghi addressed the European Parliament's committee on economic affairs on Monday and commented that 'Overall, we are becoming more confident that inflation will eventually head to levels in line with our inflation aim, but we also know that a very substantial degree of monetary accommodation is still needed for the upward inflation path to materialize'. The speech held no surprises as it remained consistent with the ECB's Policy Statement it made in September. EUR did suffer, falling 1% on Monday over fears of the German right wing political party's recent impressive showing in the German elections and the fact that Chancellor Merkel will need time to form a new coalition government.

In the United States, New York Fed President William Dudley commented to students and professors at a Community College in NY State that 'With a firmer import price trend and the fading of effects from a number of temporary, idiosyncratic factors, I expect inflation will rise and stabilize around the (Fed‘s) 2% objective over the medium term'. He also added 'In response, the Federal Reserve will likely continue to remove monetary policy accommodation gradually'. Dudley's comment mirrored the comments he made earlier in September and reinforced the expectation of a rate hike in December.

EURUSD, after dropping 1% on Monday to a 4-week low of 1.1831, recovered slightly in early trading to currently trade around 1.1860.

USDJPY dropped over 0.3% on Monday and appears to remain under pressure in early Tuesday trading. Currently, USDJPY is trading around 111.60.

GBPUSD has improved 0.2% overnight to currently trade around 1.3490.

Gold gained over 1% on Monday, as risk-off sentiment gathered pace with the latest 'exchange' of words between the US and North Korea. Currently, Gold is trading around $1,310.

WTI saw its most dramatic one-day gain for several months, as it improved by over 3% on Tuesday. With Turkey threatening to cut crude oil flows from Iraq's Kurdistan region to the outside world, London Brent hit a 26-month high of $58.40 overnight. Currently, Brent is trading around $58.40 with WTI trading around $59.20 in early Tuesday trading.

Major economic data releases for today:

At 13:00 BST, Chairing of Jean Monnet Lecture 'Good Pension Design' by ECB Praet at the Second ECB Annual Research Conference organized by the ECB in Frankfurt, Germany.

At 14:30 BST, FOMC Member, and President and CEO of the Federal Reserve Bank of Cleveland, Loretta Mester is scheduled to speak in Ohio, USA.

At 15:00 BST, the US Census Bureau will release New Home Sales and New Home Sales Change (MoM) for August. The forecast is for a slight increase in New Home Sales to 0.585M (prev. 0.571M) and New Home Sales Change to come in at 3.3% (prev. -9.4%)

At 15:30 BST, FOMC Member Lael Brainard is speaking in Washington D.C. at the Federal Reserve Board Conference: Disparities in the Labor Market: What are we missing?

At 17:45 BST, Fed Chair Janet Yellen is scheduled to speak at the 59th NABE Annual Meeting in Cleveland, Ohio on: Inflation, Uncertainty, and Monetary Policy.

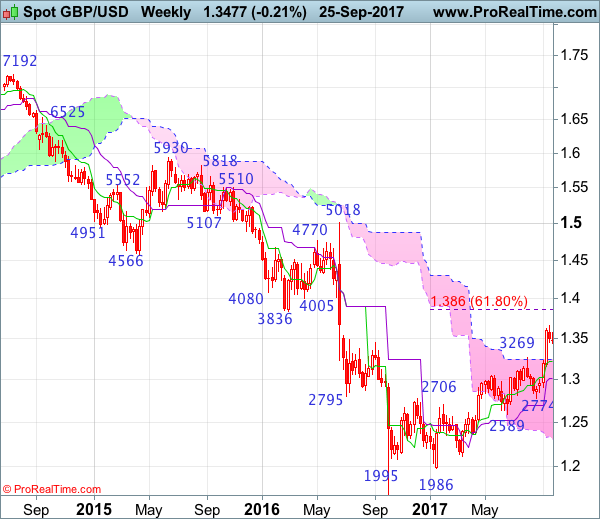

Currencies: EUR/USD And EUR/GBP Are Nearing Significant Support Levels

Sunrise Market Commentary

- Rates: Will risk sentiment continue to support core bonds?

Core bonds profited yesterday of renewed sabre rattling between North Korea and the US, giving the profit taking on shorts more impetus. Today's data will be largely ignored at the expense of the risk sentiment. There might be some more correction, but we still are in a sell-on-uptick modus, also as oil prices are moving higher. - Currencies: EUR/USD and EUR/GBP are nearing significant support levels

Yesterday, sentiment on the euro obviously turned less positive after the German election even as the impact on other markets was modest. A risk-off correction also weighed more on the euro than on the dollar. Eco data probably won't be decisive for FX trading today. If EUR/USD drops below 1.1823, the recent correction might have further to go.

The Sunrise Headlines

- US equities were hard hit by North Korean threats, but recovered quite well limiting daily losses. NASDAQ lost more ground. Asian equities trade marginally lower.

- Brent crude oil has risen above $59 a barrel to its highest in more than two years, lifted by fast-growing demand and a threat to Iraqi Kurdistan's crude exports as the autonomous region holds a referendum on independence

- The U.S. has gamed out four or five scenarios on how the crisis with North Korea will be resolved, and "some are uglier than others," McMaster said. U.S. officials dismissed as "absurd" N-K Ri Yong Ho's comment that Trump's UN speech amounted to a declaration of war.

- NY Fed Dudley signalled one more hike this year, calling factors holding down prices temporary, while Chicago's Fed Evans and Minneapolis Fed Kashkari said tightening before seeing signs of wage and price pressure would be a mistake.

- The ECB is not scared of tapering QE, ECB Coeure said. The board member said any exit will be careful and "in light of the price stability mandate.”

- Iraq's parliament voted to ban Kurdish crude exports, take back control of disputed oil fields and demanded troops be sent to Kurdistan-controlled territory after Monday's non-binding independence referendum. Turkish President Erdogan hinted at shutting off oil exports and at a military response.

- Today's calendar contains US New Home sales, consumer confidence and the Richmond Fed survey. Focus will though be on geopolitical issues, and on the manifold Fed and ECB speakers.

Currencies: EUR/USD And EUR/GBP Are Nearing Significant Support Levels

Will EUR/USD drop below 1.1823 support?

Yesterday, the focus for FX trading turned from the dollar to the euro. The German election outcome might complicate intra-EMU cooperation. EUR/USD settled in a gradual intraday downtrend. The pair dropped below 1.19. ECB Draghi mentioned the recent rise of the euro as a source of volatility/uncertainty. Later on a new exchange of hostile comments between North Korea and the US made investors look for safe havens. The risk-off triggered a simultaneous decline of USD/JPY, EUR/USD and EUR/JPY. USD/JPY finished the session at 111.73. EUR/USD close the day at 1.1848. A real test of the 1.1823 support didn't occur.

Yesterday's risk-off trade in the US also leaves its traces in Asian overnight. Major Asian equity indices show minor losses. USD/JPY hovers in the mid 111 area, near yesterday's low. However, yesterday's motive, additional fiscal spending ahead of the snap elections, doesn't support the yen anymore. EUR/USD stabilizes in the mid 1.18 area. Oil jumped sharply higher yesterday and maintains its gains this morning (Brent 59.40 $/p), but there is no obvious (invers) link with the dollar.

Today, the eco calendar is well filled with US economic data, Fed speakers including Yellen and ECB speakers Praet and Liikanen. US New Home sales declined sharply in July (-9,4% M/M). They are notoriously volatile and we expect a significant rebound in August. Consumer confidence (Conference board) was near a cyclical high in August (122.9). However, the hurricanes and higher gasoline prices suggest a decline in September. The market reaction on a weaker figure (consensus 119.5) should be modest. CB speakers are a wildcard. However, Yellen probably will hold the line of last week's press conference. We don't expected ECB's Praet to bring key new elements on the ECB policy debate at this stage.

Yesterday, the uncertain political consequences of the German election outcome for Germany and for Europe weighed slightly on the euro. Contrary to what was the case of late, a flaring up of risk-off sentiment this time weighed more on the euro than on the dollar. So, there are tentative signs that market sentiment turned less euro friendly. Today's eco data probably won't be a big help for the dollar. However, question remains whether global sentiment (cautious risk-off) and/or CB talk will sustain a further euro correction. We have the impression that yesterday's trends (simultaneous decline of USD/JPY, EUR/USD and EUR/JPY) might go somewhat further. A break of EUR/USD below 1.1823 could inspire a further technical repositioning.

From a technical point of view EUR/USD hovers in a consolidation pattern between 1.1823 and 1.2070. It was disappointing for EUR/USD bears that the recent correction didn't reach the range bottom. More confirmation is needed that the bottoming out process in US yields and in the dollar might be the start of more sustained USD gains (against the euro). In case of a break, next support in EUR/USD comes in at 1.1774 and 1.1662 The day-to-day momentum in USD/JPY was constructive recently, but it was in the first place due to yen weakness. USD/JPY regained the 110.67/95 previous resistance, a short-term positive. The 114. 49 correction top is the next important reference. However, yesterday's price action suggests that this cross rate remains sensitive to changes in overall risk sentiment.

German election and global risk-off push EUR/USD close to 1.1823 support

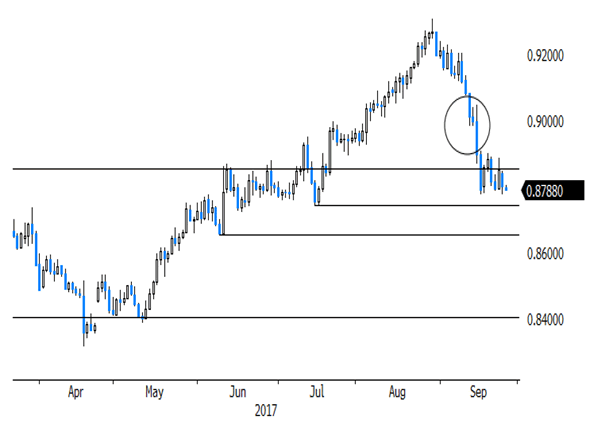

EUR/GBP

EUR/GBP: euro softness to inspire further losses?

Sterling trading was driven by global markets reaction to the German election results. The euro remained under pressure in early European dealings. EUR/GBP declined to the 0.8785 area. The rise of sterling temporary propelled cable, but finally the dollar outperformed the euro and sterling. The German election outcome might complicate the Brexit negotiations. It hasn't become easier for Merkel to make concessions. The risk-off correction (North-Korea) later in the session affected EUR/USD and cable in a similar way. Cable closed at 1.3466. EUR/GBP hovered with reach of the recent lows and close the session at 0.8798

Today, UK loans for housing are only of intraday significance. The formal Brexit negotiations restarted yesterday evening. There is no indication that a break-through on the stalemate is imminent. The EU wants progress on the conditions of the divorce, before considering talking on a new trade relationship. In theory this is negative for sterling, but the market focus isn't on the Brexit negotiations. In line with the assessment on EUR/USD, we think that the euro sentiment has worsened after the German election. If so, the EUR/GBP correction might have some further to go.

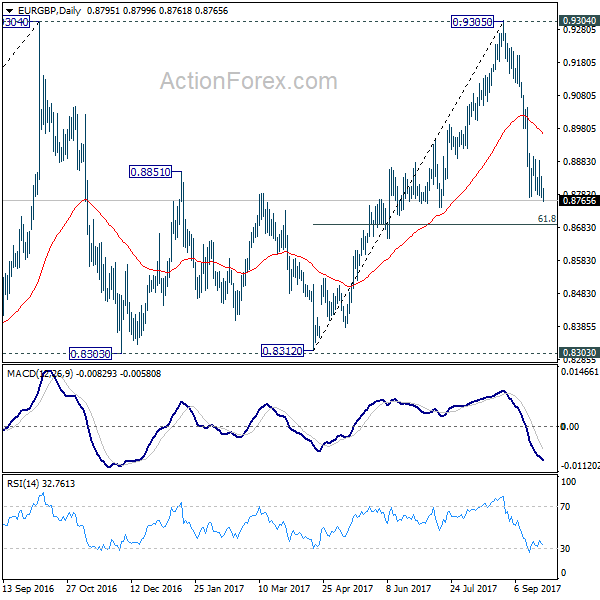

EUR/GBP made an impressive uptrend since April and set a MT top at 0.9307 late August. Recent UK price data amended the dynamics and the reversal of sterling was reinforced by hawkish BoE comments. Medium term, we maintain a EUR/GBP buy-on-dips approach as we expect the mix of relative euro strength and sterling softness to persist. However, the prospect of (limited) withdrawal of BOE stimulus put a solid floor for sterling ST term. We look how far the current correction has to go. EUR/GBP is nearing support at 0.8743 and 0.8652, which we consider difficult to break

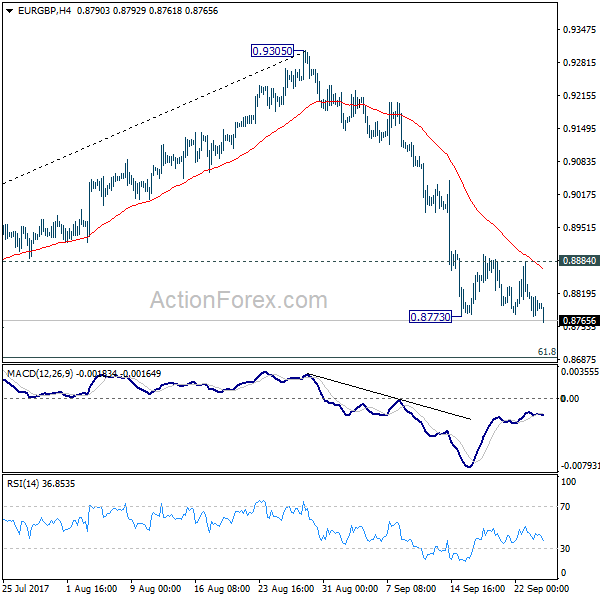

EUR/GBP: near recent lows

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8767; (P) 0.8803; (R1) 0.8830; More

EUR/GBP's break of 0.8773 suggests resumption of fall from 0.9305. Intraday bias is back on the downside for 61.8% retracement of 0.8312 to 0.9305 at 0.8691 and below. Such decline is seen as the third leg of consolidation pattern from 0.9304. We'll look for bottoming signal again at it approaches 0.8303 support. However, break of 0.8884 minor resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's still in progress with fall from 0.9305 as the third leg. Break of 0.8303 could be seen. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

Euro Soft But Holding on to Support, Dollar Losing Ground to Yen

While Euro is staying soft, after post German election selloff, it's still holding above near term support against Dollar and Yen. Weakness is mainly seen against Sterling as 0.8773 support is taken out. Also, the common currency has not yet shown any sign of a rebound. Meanwhile, Dollar is turning slightly softer against others while Yen is picking up some strength. Mixed comments from Fed officials provided little support the the greenback. While are still pricing in more than 70% chance of a December Fed hike, the decision will remain very much data dependent. Tensions between US and North Korea remain tight as verbal exchanges between leaders continued to escalate.

North Korea boosting defense in its east coast

South Korea news agency Yonhap reported that North Korean has been boosting defense in its east coast as tensions between US and the North escalated. North Korea Foreign Minister Ri Yong Ho complained yesterday that US President Donald Trump's tweet that Ri and leader Kim Jong Un "won't be around much longer" was a declaration of war. And, North Korea has every right on counter measures including shooting down US bombers "even when they are not inside the airspace border of our country". And Ri warned that "the whole world should clearly remember it was the U.S. who first declared war on our country." White House Press Secretary denied that and said "we've not declared war on North Korea. And frankly, the suggestion of that is absurd."

Chicago Fed Evans a little nervous that inflation weakness is structural

Chicago Fed President Charles Evans, a dove, repeated his call for cautious and gradual approach to rate hike. Even though he is "broadly comfortable" with Fed's projections, his emphasized that "this path are not set in stone". And, "as the FOMC comes to decision points over the coming months, I think we need to see clear signs of building wage and price pressures before taking the next step in removing accommodation." Also, it would take "a couple more months of data" before confirming that the slow down in inflation was temporary. And he is " a little nervous that some of the recent weakness might be a little more structural."

On the other hand, New York Fed President William Dudley said that "With a firmer import price trend and the fading of effects from a number of temporary, idiosyncratic factors, I expect inflation will rise and stabilize around the 2 percent objective over the medium term". And, "in response, the Federal Reserve will likely continue to remove monetary policy accommodation gradually."

ECB Draghi: We can't afford hasty moves

ECB President Mario Draghi spoke to the European Parliament's comment on economic affairs in Brussels yesterday. Draghi emphasized the need to be "sensitive to the danger of not halting a recovery through hasty monetary-policy decision making." And he warned that "we can't afford hasty moves." And any change, or so called re-calibration of monetary policies will maintain "the degree of monetary support that the euro-area economy still needs to complete its transition to a new balanced growth trajectory characterized by sustained conditions of price stability." Nonetheless, Draghi still sounded upbeat and noted that "economic expansion is now firm and broad-based across euro area countries and sectors." And, policymakers "are becoming more confident that inflation will eventually head to levels in line with our inflation aim".

Separately, ECB Executive Board member Yves Mersch said that the central bank will continue to "prudently adjust our toolbox of monetary policy instruments" once there is "a sufficiently sustained adjustment in the path of inflation." Regarding the stimulus program, Mersch noted that "while the temporary collateral framework has successfully eased potential collateral shortages, it could be argued that it should not become part of the regular framework". That is, collateral rules could now be tightened up as ECB can also start shifting back to "a more conventional environment for the conduct of monetary policy.

French Macron to deliver Euro reform speech

French President Emmanuel Macron will deliver a speech in Paris today, outlining his proposals on reforms in Europe. And it's seen as an appropriate step to voice our his ideas before German Chancellor Angela Merkel has formed the coalition after Sunday's election. The key elements of Macron's reform include reinforcing the Euro against future shocks, a European agency for innovation and a system on start-up funding. However, the untested coalition of CDU, FDP and Greens in Germany could prove to be intrinsically unstable. And negations could take months that might delay Macron's plan.

EU and UK still at odds over key Brexit issues

As the fourth round of Brexit negotiations started, the EU and UK are clearly staying at odds over the key issues. EU's chief negotiator Michel Barnier emphasized that "we cannot discuss a transition period without reaching a preliminary agreement on an orderly withdrawal." And he reiterated that "real progress on the three main issues is essential to move to a discussion on the transition as well as the future, these are separate issues." Also, Barnier pointed out that a future trade agreement and so called transition or implementation period are not foregone conclusions. And "without exception", UK will remain subject to EU budge, jurisdiction if it choose to stay in the single market after Brexit.

UK's Brexit Secretary David Davis, on the other hand, emphasized that "we do not want our EU partners to worry they will pay more or receive less over the remainder of the current budget plan as a result of our decision to leave." And, "the UK will honour commitments we've made during the period of our membership." However, Davis also emphasized that "it's obvious that reaching a conclusion on this issue can only be done in the context of, and in accordance with, our new deep and special partnership with the EU."

While the talks of the Brexit teams carry on in Brussels, UK Prime Minister Theresa May will meet with European Council President Donald Tusk in London today.

New Zealand business confidence tumbled

New Zealand NBNZ business confidence sank to 0 in September, down sharply from 18.3. That's the third straight month of decline and the lowest reading since September 2015. Nonetheless, ANZ chief economist Cameron Bagrie noted today that news economic drivers are emerging and growth would remain "respectable". The drivers are appearing in form of "higher commodity prices, rising household incomes and expansionary fiscal policy". Nonetheless, Bagrie also pointed out, after the election over the weekend, "policy uncertainty will rise over the coming months as political horse trading takes place" and that can be "unsettling". Also from New Zealand, trade deficit came in much higher than expected at NZD -1235m in August.

Oil prices surged on supply disruption concern

Oil prices jumped on concerns over potential supply disruption after Turkey threatened to "close the valves" on Kurdistan's oil exports. This was due to Turkey's objections over an independence referendum held in the Kurdistan region of Iraq. While the Iraqi government has condemned the act, Turkish and Iranian worried that the controversial referendum would be contagious, causing the huge Kurdish population in their countries to do the same. Western powers, including US and UK have also warned that the referendum would exacerbate the instability in the MENA region. However, these powers have not considered their indifference towards the suppression on the people in Kurdish region. Indeed, their concerns probably only lie on the oil. Kurdistan is home to 40% of Iraq's oil reserves. It is estimated that Kurdistan has oil reserve of at least 45B barrel with exports of around 600K bpd. Most of the oil leaves the region via a pipeline from Kirkuk to the Turkish city of Ceyhan, to export markets in Russia and Europe. Oil facilities in the regions were relatively undamaged despite US' invasion in Iraq in 2003. It would create another conflict, in case of a Kurdistan independence, on the ownership of the region's oil revenue and the lucrative oil reserve.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8767; (P) 0.8803; (R1) 0.8830; More

EUR/GBP's break of 0.8773 suggests resumption of fall from 0.9305. Intraday bias is back on the downside for 61.8% retracement of 0.8312 to 0.9305 at 0.8691 and below. Such decline is seen as the third leg of consolidation pattern from 0.9304. We'll look for bottoming signal again at it approaches 0.8303 support. However, break of 0.8884 minor resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's still in progress with fall from 0.9305 as the third leg. Break of 0.8303 could be seen. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Aug | -1235M | -825M | 85M | 98M |

| 23:50 | JPY | BOJ Minutes July 19-20 Meeting | ||||

| 23:50 | JPY | Corporate Service Price Y/Y Aug | 0.80% | 0.70% | 0.60% | |

| 0:00 | NZD | NBNZ Business Confidence Sep | 0 | 18.3 | ||

| 6:00 | EUR | German Import Price Index M/M Aug | 0.00% | 0.10% | -0.40% | |

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Jul | 5.80% | 5.70% | ||

| 14:00 | USD | New Home Sales Aug | 591K | 571K | ||

| 14:00 | USD | Consumer Confidence Sep | 120 | 122.9 |

XAUUSD Intraday Analysis

XAUUSD (1310.74): Gold prices rebounded strongly in the day yesterday as price action closed above the support zone of 1300.86 yesterday. We expect this continuation to push prices higher in the near term. Gold prices will need to test the resistance level at 1324.72 - 1320.39 region. A reversal here could push gold prices back lower to the support level. A rebound off this level could keep the bullish bias intact as gold prices could eventually break past 1324.72 and target the next main level at 1345.87.

GBPUSD Intraday Analysis

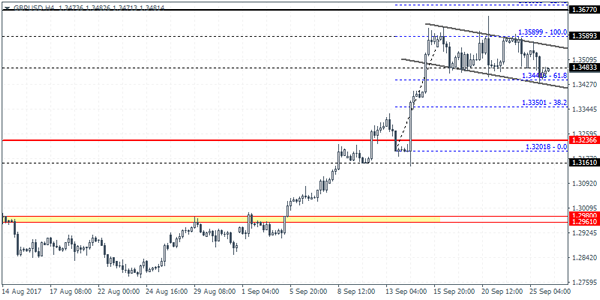

GBPUSD (1.3483): The British pound also continues with its consolidation with price action briefly slipping below 1.3488 support. Th re-adjusted bullish flag pattern remains in play although price will need to breakout from this bullish pattern to signal continuation. Continued consolidation within 1.3558 - 1.3488 could potentially weaken the bullish chart pattern and increase the risk of a downside breakout. A daily close below 1.3441 could validate this bearish bias as GBPUSD could be seen pushing lower towards 1.3236.

EURUSD Intraday Analysis

EURUSD (1.1857): The EURUSD turned bearish, but the price action continues to remain range bound within 1.2080 and 1.1822 levels of support and resistance. This sideways price action could potentially signal to a breakout in the near to medium term. On the 4-hour chart, however, there are some bearish signs with the descending triangle formation. Support is seen at 1.1843 - 1.1822 level. A breakout below this level could signal further declines that could send the common currency towards the support level at 1.1688 which is pending retest.

Euro Weakens As Investors Assess German Elections

Despite attempting to fill the gap at the open, the euro currency was seen turning bearish. Investors digested the German elections outcome which turned out as expected. However, with the AfD making inroads into the Bundestag, the markets were a bit cautious. The rise of the populist and right leaning political parties this year has been a major concern among the leaders in the EU.

Politics was the main theme on Monday with the New Zealand election results expected to be announced over the week. In Japan, PM Abe called for snap elections in a bid to consolidate his position amid threats from North Korea. Speaking in a televised speech on Monday, Abe said the elections would be a verdict of his performance in handling the spending plans and also his handling of the North Korea crisis. Abe also said that he would resign as the prime minister if his party failed to win a majority.

Looking ahead, the economic calendar is light today which makes the Fed Chair Janet Yellen's speech the main event of the day. Ms. Yellen will be speaking at an event in Cleveland.

Data, FOMC Drive Headlines Tuesday

A steady stream of market-moving events is expected Tuesday, with North America seeing the bulk of the releases. However, several European reports will also make headlines ahead of the New York session.

The European data wire begins at 06:00 GMT with German import prices, which are a key inflation metric. Forty-five minutes later, France's INSEE will release its monthly business climate survey for September.

Action continues at 08:00 GMT with the Italian trade balance, followed by the British Bankers Association (BBA) monthly report on mortgage approvals at 08:30 GMT.

European Central Bank (ECB) official Peter Praet will deliver a speech at 12:00 GMT. Praet has been a member of the Executive Board since 2011.

Shifting gears to the United States, the S&P/Case-Shiller Home Price Index is scheduled for release at 13:00 GMT.

The Commerce Department's new home sales report is due one hour later. The sale of new homes is forecast to rise 3.3% to a seasonally adjusted annual rate of 585,000 in August.

Later in the session, the Federal Reserve Bank of Richmond will unveil its September manufacturing index.

On the policy circuit, a parade of Fed speakers will deliver speeches on Tuesday, including Chairwoman Janet Yellen. Her speech follows public remarks by Federal Open Market Committee (FOMC) members Loretta Mester and Lael Brainard.

The FOMC voted last week to hold interest rates at 1.25%, but signaled that one more upward adjustment is likely this year. The Fed also penciled in October as the start of its balance sheet reduction program.

The US dollar will be highly sensitive to monetary policy on Tuesday. The greenback shot up half a percent at the start of the week after New York Fed President William Dudley said interest rates are on track to rise gradually.

EUR/USD

The euro nosedived on Monday alongside other dollar rivals. The EUR/USD touched a session low of 1.1841 on Monday, which would have been enough for a more than one-month low. The pair was last up 0.1% at 1.1860. The pair faces a key trend channel support around 1.1825.

GBP/USD

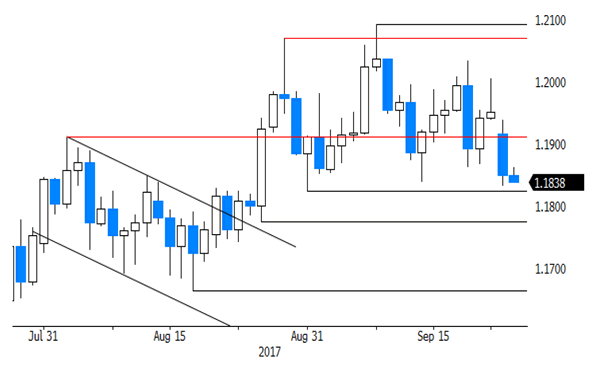

Cable has declined roughly 100 pips from Friday's close as part of a broad retracement following fresh multiyear highs. The GBP/USD rebounded in early Tuesday trading to reach 1.3482. From a technical perspective, the 1.3443 region remains a strong support level for cable. On the opposite side of the ledger, strong resistance is seen at 1.3580.

GOLD

Gold prices rebounded sharply on Monday, rising in lockstep with the US dollar. Spot prices are back above $1,300.00 a troy ounce after a multi-week retracement sent the bulls packing. Bullion faces a major support zone at around $1,287.00. Below that level, the metal is likely supported until $1,267.00. Traders should carefully monitor risk sentiment in the financial markets for a directional play on gold.

GBP/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 31 Jul 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Morning star

• Time of formation: 25 Aug 2017

• Trend bias: Near term up

GBP/USD – 1.3475

Although cable edged higher to 1.3659 last week, the subsequent retreat suggest consolidation below this level would be seen and pullback to the Tenkan-Sen (now at 1.3406) cannot be ruled out, however, reckon 1.3380-82 would limit downside and bring another rise later. A daily close below 1.3325-30 would suggest top is possibly formed, bring weakness to the Kijun-Sen (now at 1.3217) but a sustained breach below there is needed to add credence to this view, bring further fall to support at 1.3153 which is likely to hold from here.

On the upside, expect recovery to be limited to 1.3590-00 and bring another retreat. Above 1.3600 would bring retest of 1.3659 but break there is needed to extend recent rise to 1.3700-10, however, near term overbought condition should limit upside to 1.3800 and reckon 1.3860 (61.8% Fibonacci retracement of 1.5018-1.1986) would remain intact, risk from there is seen for a strong retreat to take place later.

Recommendation: Buy again at 1.3250 for 1.3550 with stop below 1.3150.

On the weekly chart, despite rising to 1.3659 last week, lack of follow through buying and the subsequent retreat suggest consolidation would take place and pullback to 1.3400-05 is likely, however, reckon downside would be limited to 1.3300-10 and renewed buying interest should emerge around the upper Kumo (now at 1.3247) and bring another rise later. Above said resistance at 1.3659 would extend recent erratic rise form 1.1986 low to 1.3750-60 and 1.3800 but near term overbought condition should prevent sharp move beyond 1.3860 (61.8% Fibonacci retracement of 1.5018-1.1986) and 1.3900-10 should hold, bring retreat later.

On the downside, although initial pullback to 1.3400-05, then 1.3350 cannot be ruled out, reckon downside would be limited to the upper Kumo (now at 1.3247) and bring another rise later. Below the Tenkan-Sen (now at 1.3217) would defer and suggest a temporary top is formed, bring retracement of recent rise to 1.3140-50, then towards 1.3100, however, still reckon downside would be limited to the Kijun-Sen (now at 1.3012) and support at 1.2909 should remain intact, bring another rally later.