Sample Category Title

Aussie Tumbles as S&P Downgraded China, Dollar Paring Some Gains

Dollar is maintaining most of the post-FOMC gains against other major currencies. But it's turning softer against Euro and Sterling today. Better than expected job data provides no inspiration to the greenback. While developments in USD/CHF and USD/JPY are bullish, GBP/USD shows the Pound is still having an upper hand against Dollar. EUR/USD is staying well above 1.1822 support zone and maintaining near term bullishness too. Nonetheless, it's the selloff in Aussie and Kiwi that catches most eyes. RBA Governor Philip Lowe's comments suggest that he's in no hurry to follow other central banks in tightening. But the main driver is S&P's downgrade of China's sovereign credit rating.

S&P lowered China rating to A+

S&P Global Ratings lowered China's sovereign credit rating by one step to A+, down from AA-. That's the first rating cut since 1999. S&P warned that "China's prolonged period of strong credit growth has increased its economic and financial risks." And, "although this credit growth had contributed to strong real gross domestic product growth and higher asset prices, we believe it has also diminished financial stability to some extent." That's the second downgrade by major rating agencies this year. Moody's downgraded China from Aa3 to A1 earlier in May. The Finance Minister has yet to respond yet. Some economists noted that time impact of the downgrade on China will be limited. That's due to the low reliance on external funding, due to huge domestic savings and tight capital account control.

RBA Lowe in no hurry to hike

RBA Governor Philip Lowe said today that "some normalization of monetary conditions globally should be seen as a positive development, although it does carry risks. It is a sign that economic growth in advanced economies has become self-sustaining, rather than just being dependent on monetary stimulus." However, he emphasized that "a rise in global interest rates has no automatic implications for us here in Australia." Though, "an increase in global interest rates would, over time, be expected to flow through to us, just as the lower interest rates have." But, "our flexible exchange rate though gives us considerable independence regarding the timing as to when this might happen." The comments suggest that RBA is in no hurry to follow other central banks to raise interest rates.

ECB growth yet to translate into inflation

ECB monthly bulletin noted that "ongoing economic expansion provides confidence that inflation will gradually head to levels in line with its inflation aim". However, it has yet to "translate sufficiently into stronger inflation dynamics." And therefore, "a very substantial degree of monetary accommodation is still needed for underlying inflation pressures to gradually build up and support headline inflation." Nonetheless, ECB sounded upbeat on employment as "the swift decline in euro area unemployment is particularly encouraging against a background of increasing labour supply." ECB is widely expected to announce some sort of recalibration of monetary policy in October. There will be a number of occasions in the coming data for officials to express their stance and arguments. President Mario Draghi will speak today. Executive Board members will Vitor Constancio, Peter Praet, Benoit Coeure, Sabine Lautenschlaeger and Yves Mersch will all speak at multiple events around Europe.

BoJ Kuroda left door open for further easing

BoJ Governor Haruhiko Kuroda said in the post meeting press conference that the central bank will "patiently continue accommodative monetary policy to achieve 2 percent inflation." And he pledged to "adjust policy as needed looking at economic, price and financial developments. He also kept the door open for "further monetary easing steps if necessary." On some recent topics, Kuroda said that "it's inappropriate to alter or abandon our 2 percent inflation target." Meanwhile, BOJ policymakers are "carefully watching progress on fiscal discipline as it would affect not just fiscal policy but monetary policy." It's reported earlier this week that Japan Prime Minister Shinzo Abe will dissolve the parliament later this month and call for a snap election in October. And Abe will push back the timing of primary budget surplus by a few years, from fiscal 2020 to later in the decade.

BoJ left monetary policy unchanged today as widely expected. Short term policy interest is kept at -0.1%. And the central bank will continue to dive 10 year JGB rate at around 0%. Annual pace of monetary base expansion is kept at JPY 80T under the yield curve control framework. The biggest surprise for the decision is that new comer Goushi Kataoka dissented as he believed that "monetary easing effects gained from the current yield curve were not enough for 2 percent inflation to be achieved around fiscal 2019". And Kataoka also "opposed the description on the outlook for the CPI" as " possibility of the rate of change increasing toward 2 percent from 2018 onward was low at this point."

But after all, Kataoka's dovish voice is indeed not much of a surprise. He has been considered a vocal, firm advocate of aggressive monetary easing. And he's believed to be brought in by Prime Minister Shinzo Abe to replace the relatively hawkish voice of former policymaker Takahide Kiuchi and Takehiro Sato. One could even argue that it's actually a surprise that Kataoka is not dovish enough to push for rate cut of expanding the QQE program.

Fed still on course for a December hike

Yesterday, Fed finally made formal announcement that it would begin normalizing the balance sheet in October. As indicated in June, the process does not involve active selling of securities, but a passive run-off of its holdings. The policy rate also stayed unchanged at 1-1.25%. The overall tone of the statement and the press conference came in more hawkish than expected. Despite downward revision in the core CPI for this year, the staff upgraded the economic growth outlook and downgraded the unemployment rate forecast.

The median dot plot continued to project one more rate hike this year, followed by three more increases in 2018. As CME's 30-day Fed funds futures suggested, bets for a December hike markedly jumped to 73.4% from 57.7% in the prior day. The overall tone signaled that the Fed is committed to carry on the rate hike schedule (three increases for 2017) as indicated earlier this year. Barring a 'material' change in the economic outlook, the Fed should implement its rate hike and balance sheet normalization policies any planned. More in Fed To Reduce Balance Sheet From October, Committed To One More Rate Hike This Year.

More on FOMC:

- FOMC Review: Unchanged Hiking Signals As QT Is Set To Begin Next Month

- FOMC: Gauging Normality For Investors: Real Rates Positive

- Fed Announces Tapering But No Rate Hike; Unchanged Dots Seen as Hawkish

- FOMC Leaves Rates Unchanged and Sticks to its Plans to Gradually Unwind Balance Sheet

On the data front

US Initial jobless claims dropped -23k to 259k in the week ended September 16, much lower than expectation of 302k. That's the 133 straight weeks of sub-300k reading. Continuing claims rose 44k to 1.98m in the week ended September 9. Philly Fed business outlook improved strongly to 23.8, up from 18.9 and beat expectation of 17.5. House price index rose 0.2% mom in July. Canada wholesales rose 1.5% mom in July. UK public sector borrowing rose to GBP 5.1b in August. Swiss trade surplus narrowed to CHF 3.17b in August. New Zealand GDP grew 0.8% qoq in Q2, in line with expectation. Japan all industry index dropped -0.1% mom in July.

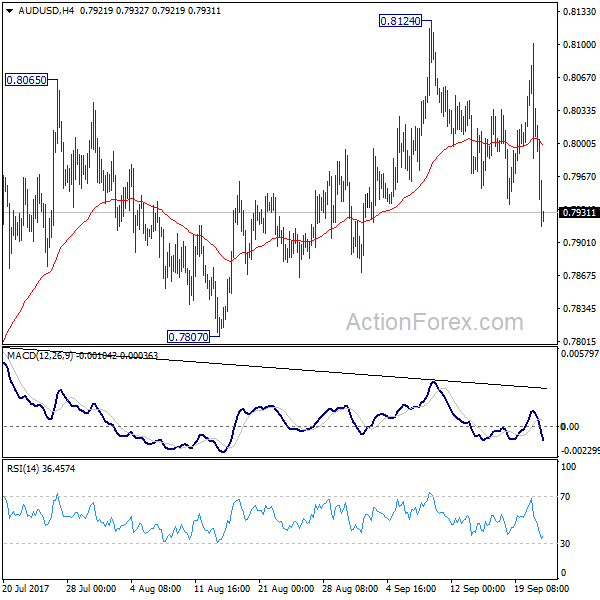

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7976; (P) 0.8039; (R1) 0.8093; More...

AUD/USD drops sharply to as low as 0.7917 so far today. But it's still staying in range of 0.7807/8124. Intraday bias remains neutral first. Deeper fall cannot be ruled out. But still, with 0.7807 support intact, near term outlook stays bearish and another rise is expected. Break of 0.8124 will turn bias to the upside and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335 next. However, considering bearish divergence condition in 4 hour MACD, firm break of 0.7807 will indicate near term reversal and turn bias back to the downside for 0.7328 key support.

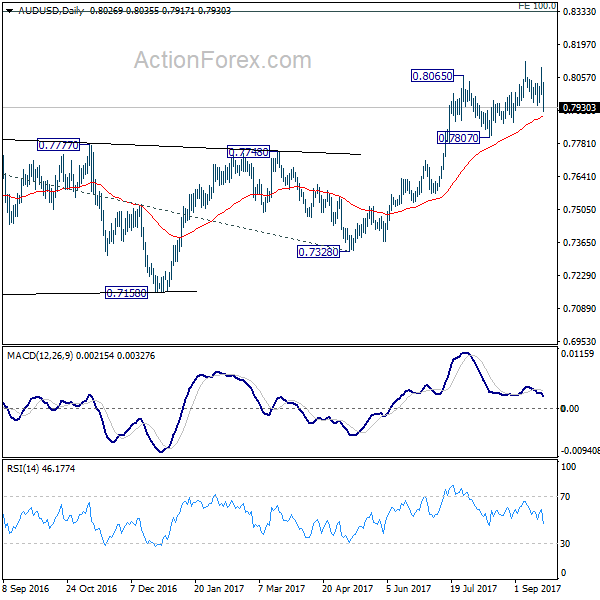

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8090) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7807 support is needed to to be the first sign of completion of the rebound. Otherwise, further rise is now in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| JPY | BoJ Monetary Policy Statement | |||||

| 22:45 | NZD | GDP Q/Q Q2 | 0.80% | 0.80% | 0.50% | 0.60% |

| 04:30 | JPY | All Industry Activity Index M/M Jul | -0.10% | -0.10% | 0.40% | 0.20% |

| 05:45 | CHF | SECO Economic Forecasts | ||||

| 06:00 | CHF | Trade Balance (CHF) Aug | 3.17B | 2.41B | 3.51B | 3.49B |

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 08:30 | GBP | Public Sector Net Borrowing (GBP) Aug | 5.1B | 6.5B | -0.8B | |

| 12:30 | CAD | Wholesale Sales M/M Jul | 1.50% | -0.90% | -0.50% | -0.60% |

| 12:30 | USD | Initial Jobless Claims (SEP 16) | 259K | 302K | 284K | 282K |

| 12:30 | USD | Philadelphia Fed Business Outlook Sep | 23.8 | 17.5 | 18.9 | |

| 13:00 | USD | House Price Index M/M Jul | 0.20% | 0.40% | 0.10% | |

| 14:00 | EUR | Eurozone Consumer Confidence Sep A | -1.5 | -1.5 | ||

| 14:00 | USD | Leading Indicators Aug | 0.20% | 0.30% | ||

| 14:30 | USD | Natural Gas Storage | 91B |

GBP/USD Retreat Favored

The currency pair seems too exhausted to climb much higher at this moment, so it could come down to retest a support level before will reach and retest a support level. It looks undecided right now also because the USDX has decreased a little again. The greenback needs a bullish spark from the United States economy, will receive one if the Unemployment Claims will come in better than expected. The Initial Claims are expected to increase from 284K to 302K in the previous week and could reach the highest level since March 5 2015. The Philly Fed Manufacturing Index is expected to decrease from 18.9 to 17.3 points, while the HPI could increase by 0.4%, more versus the 0.1% estimate. The Consumer Confidence is expected to remain steady at -2 points, while the CB Leading Index may increase by 0.3%, matching the 0.3% growth in the former reading period.

Price failed to stay above the 150% Fibonacci line and now could drop towards the first warning line (wl1) of the ascending pitchfork and towards the upside line of the ascending channel. Technically, it should drop after the failure to reach and retest the lower median line (lml) of the ascending pitchfork. The perspective remains bullish despite a minor decrease, the price is still located in the green territory.

A minor decrease is natural after the impressive rally, but we'll see how will react after the US data will be sent to the public.

USD/CHF Crucial Breakout In Play

USD/CHF resumes the upside momentum and seems poised to reach fresh new highs in the upcoming period. Has finally managed to make an aggressive breakout, which will lead the rate at least till the upper median line (uml) of the ascending pitchfork.

Has climbed also above the second warning line (WL2) of the former ascending pitchfork. I want to remind you that the rate continues to move in range on the short term, so only a valid breakout above the 0.9787 static resistance and above the upper median line (wl1) will confirm a major increase.

EUR/CHF Likely To Climb Higher

Price is trading in the green after the yesterday's minor decrease. A valid breakout above the 150% Fibonacci line (ascending dotted line) will confirm a further increase. The next upside target will be at the sliding line (sl) of the black ascending pitchfork, while the major resistance level will be at the first warning line (WL1) of the major ascending pitchfork.

EURUSD Awaits Draghi Speech

Price-action has reclaimed the 1.1900 handle on the EURUSD pair, ahead of today's key note speech by European Central Bank President Mario Draghi, at the second ESRB annual conference in Frankfurt, Germany.

Earlier, sellers failed to close price beneath the pairs monthly pivot point, provoking a strong intraday bounce towards the 1.1919 level, which is four pips above Monday's swing-low and ten pips away from the daily pivot point.

Going forward, if the euro fails to close price back above the 1.1915 level on a higher time-frame basis, sellers may push price-action back towards the monthly pivot point, located at 1.1884.

Key intraday technical resistance above the 1.1919 level, is found at 1.1928, 1.1938 and 1.1957.

Below the 1.1900 handle, intraday EURUSD support is found at 1.1884, 1.1870 and the pairs key 50-day moving average, located at 1.1855.

Below 1.1855, traders will look to the former weekly low, at 1.1838 and the pairs crucial 200-week moving average, at 1.1725.

GBPUSD Turning Lower

Sterling is turning lower, after failing to move above the pairs key 50-hour moving average, at 1.3515. The British pound is also coming in-line with the broader intraday theme of overall U.S dollar index strength.

Yesterday, the pair printed an explosive 1-hour price-candle immediately after the Federal Reserve interest decision, with price-action spiking to a new yearly high, at 1.3657, and then falling to a new weekly low, at 1.3552.

A higher time frame price-close below the 1.3473 level should accelerate technical selling, whilst a higher time-frame price close above 1.3515 should encourage buying interest.

Key intraday GBPUSD support is found at 1.3452 and 1.3420, with key intraday support from the pairs key 100-week moving average, at 1.3382.

To the upside, key intraday GBPUSD resistance is found 1.3496 and 1.3515. Once closing above 1.3515, further resistance is seen at the daily pivot, at 1.3538, and the 50 percent Fibonacci retracement of yesterday's daily range, at 1.3557.

GBPUSD – Sets Up To Weaken Further On Loss Of Upside Steam

GBPUSD - The pair saw price rejection on Wednesday leaving risk of more weakness on the cards in the days ahead. Support lies at the 1.3450 level where a break will turn attention to the 1.3400 level. Further down, support lies at the 1.3350 level. Below here will set the stage for more weakness towards the 1.3300 level. Conversely, resistance stands at the 1.3550 levels with a turn above here allowing more strength to build up towards the 1.3600 level. Further out, resistance resides at the 1.3650 level followed by the 1.3700 level. On the whole, GBPUSD continues to face further downside threats on higher price rejection.

U.S Dollar Hanging Tough For Now

September 21: Five things the markets are talking about

The Fed's decision to leave the benchmark interest rate unchanged was entirely anticipated yesterday, but their ‘hawkish' forecast for where rates will be at the end of the year caught some of the market by surprise.

As expected, the Fed announced its balance sheet runoff plan would start next month, while keeping its options open on a potential December rate hike. After the announcement the U.S Treasury curve flattened as short-end backed up faster than long rates.

Note: With the Fed biting the bullet over quantitative easing (QE), investors are now expected to turn their attention to several appearances by ECB officials for clues on the future of Europe's stimulus.

Elsewhere, the Bank of Japan (BoJ) also left policy unchanged, as expected. The one dissenter, by new BOJ policy board member Goushi Kataoka, said that the 'yield curve control is not enough to meet inflation target,' and 'sees low chance of consumer prices increasing from 2018 on.'

In the U.K, Brexit strategy continues to top the agenda as PM Theresa May prepares to outline her revised approach tomorrow, while in Germany campaigning continues before Sunday's (Sept. 24) general election. Down-under, New Zealand prepares to go to the polls Saturday.

1. Stocks mixed results

In Japan, the Nikkei share average edged up overnight (+0.2%), helped by gains on Wall Street and a weaker yen (¥112.40) after the Fed signalled it still expects to raise interest rates one more time this year. The BoJ kept monetary policy steady, while maintaining its upbeat view of the economy. The broader Topix index rallied less than +0.05% to its highest print in two-years, before giving up some of its gains after the BoJ's decision.

Note: Investors remain weary of headlines related to a snap Japanese election that are rumoured to be called by PM Abe as early as next Monday.

In Hong Kong, shares ended little changed, as strength in financial and consumer stocks offset a slump in the resources sector triggered by a stronger dollar. The Hang Seng index fell -0.1%, while the China Enterprises Index rose +0.2%.

In China, the major indexes slipped, as developers and the materials sector weakened, offsetting gains in financial firms buoyed by the potential of another Fed rate increase. The blue-chip CSI300 index fell -0.1%, while the Shanghai Composite Index lost -0.2%.

In Europe, regional indices trade mostly higher across the board with the weaker EUR (€1.1916) helping push indices higher following the Fed and BoJ rate decision.

U.S stocks are set to open in the ‘red' (-0.1%).

Indices: Stoxx600 +0.2% at 382.7, FTSE flat 7271.5, DAX +0.2% at 12598, CAC-40 +0.5% at 5267, IBEX-35 +0.2% at 10311, FTSE MIB +0.5% at 22470, SMI +0.4% at 9133, S&P 500 Futures -0.1%

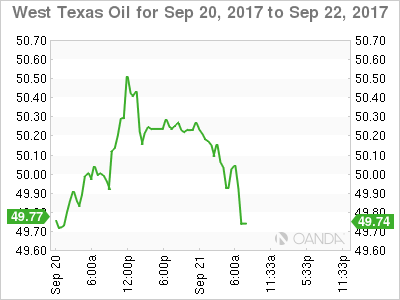

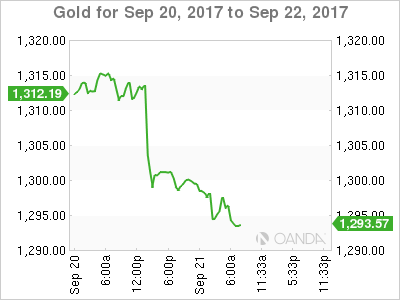

2. Oil prices steady ahead of key OPEC meeting, gold lower

Oil prices were steady overnight, holding most of this week's gains ahead of today's OPEC meeting in Vienna that could extend production limits aimed at clearing a glut that has depressed the market for more than three years.

In January, OPEC and its allies agreed to reduce output by about -1.8m bpd until March 2018 in an attempt to empty inventories. The market is now anticipating an extension to that deal, possibly to the end of next year.

Brent crude oil is down -5c at +$56.24 a barrel, while U.S light crude is -15c lower at +$50.54.

Note: Both contracts have risen more than +15% over the last three-months as global oil supply has tightened.

Ahead of the U.S open, gold prices have slipped to its lowest print in over three-weeks overnight. A stronger U.S dollar and increasing prospects of a December Fed rate hike is curbing appetite for the ‘yellow' metal. Spot gold is down -0.2% at +$1,298.06 an ounce.

3. Sovereign yields on the rise

With the Fed considered a tad more ‘hawkish' after yesterday's Federal Open Market Committee (FOMC) meeting – suggesting it is open to one more rate hike in 2017, data depended and three hikes next year – took the market by surprise.

FI dealers scrambled to price in a Dec. hike, pushing front-end U.S yields much higher (U.S 2's backed up to +1.43% for the first time since 2008) and flattening the curve.

According to the CME, Fed fund future odds moved from pre-meet +50% to +73% possibility for a Dec. Fed rate hike.

Market fears that the Fed will continue to raise rates despite lackluster inflation could keep pressure on the bond market in the near term. Also, the Fed indicated yesterday that it reduced its longer-term projection for its federal-funds rate. Officials now see a rate target of +2.8%, rather than +3%.

The yield on U.S 10-year rallied less than +1 bps to +2.27%, reaching its highest yield print in more than seven-weeks on its fifth consecutive advance. In Germany, the 10-year Bund yield climbed +3 bps to +0.47%, the highest in more than six-weeks.

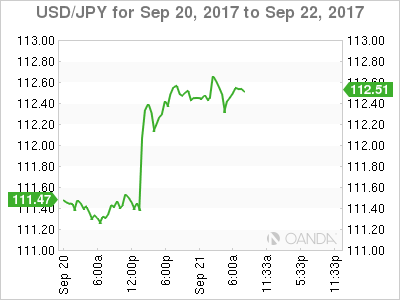

4. Dollar still holding tough for now

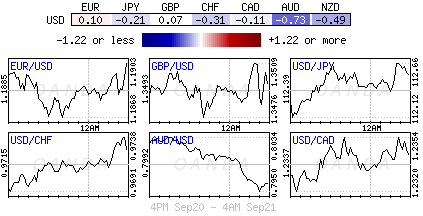

The U.S dollar has posted a powerful rebound in the past 24-hours as the market was caught off guard by the Fed's projection of one more rate hike within the year.

In yesterday's session, the EUR slumped -0.8% to €1.1860 intraday, giving back most of its gains made in the prior four-sessions. USD/JPY has managed to surge up to ¥112.52, its highest intraday level in nearly two-months, extending its winning streak to a fourth-session.

USD/CHF is up for a fourth day as it gains +0.2% to $0.9724, and USD/CAD has regained the psychological C$1.2300 level by rising +0.3% to C$1.2324. The pound swung up to £1.3656 Wednesday, its highest intraday level since the Brexit vote, before retreating to trade atop of £1.3492.

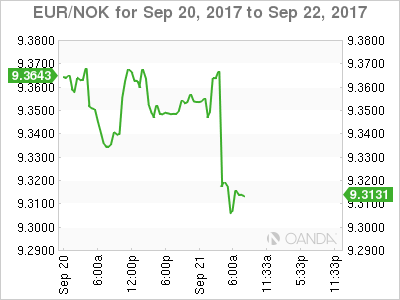

Elsewhere, NOK ($7.8066) has rallied against the U.S dollar after Norges Bank suggested rates might rise sooner than anticipated, even as it left its key policy rate at a record low of +0.5% earlier this morning. EUR/NOK has dropped to its lowest level in a week and a half at around €9.3057.

5. S&P cuts China's credit rating

S&P Global Ratings cut China's sovereign credit rating for the first time in 18-years earlier this morning, citing the risks from soaring debt, and revised its outlook to stable from negative.

The sovereign rating was cut by one step, to A+ from AA-.

'China's prolonged period of strong credit growth has increased its economic and financial risks,' S&P said. 'Although this credit growth had contributed to strong real GDP growth and higher asset prices, we believe it has also diminished financial stability to some extent.'

Note: Moody's Investors Service cut China's rating last May to A1 from Aa3, citing similar concerns over economy-wide debt and effects on state finances.

Daily Technical Analysis: EUR/USD Main Channel Could Break To The Downside

The EUR/USD has formed the main channel (light green) that could break soon if the price gets below 1.1890. The price will be trapped in the downtrend channel (violet) and might drop to 1.1800. the POC zone (D H3,EMA89, 50.0,order block, ATR high) 1.1930-50 could reject the price on a retracement. If we don’t see any retracement, pay attention to break of 1.1890. Targets are 1.1850, 1.1835 and 1.1800.

Market Update – European Session: Euro Indices Rise As Markets Digest Latest Rate Decisions From The FED And BoJ

Notes/Observations

European Indices higher following FOMC rate decision, unwind lifts dollar

Norway keeps rates on hold, reiterates will likely remain on hold til 2019

Overnight

Asia:

BoJ left rates on hold as expected with a vote of 8-1 with newcomer Kataoka dissenting

China PBOC sets yuan reference rate-0.3% at 6.5867, the weakest level since Sept 1st.

New Zealand Q2 GDP comes in line with expectations

Taiwan and Philippines leave rates on hold as expected

HTC Confirms $1.1B cooperation agreement with Google, where Google will acquire part of HTC engineering team related to Pixel phone

Australia's CBA to sell Life Insurance unit to AIA Group for $3B

Europe:

Norway keeps deposit rates on hold as expected; Notes Capacity Utilization is on the rise, higher than previously assumed, labor mkt improvement has occurred somewhat faster pace than assumed in June

Sweden Central bank (Riksbank) Sept Minutes showed there are some temporary factors behind the most recent upturn in inflation and the krona has strengthened more rapidly than in the forecast in July

ECB SEPT ECONOMIC BULLETIN: Short term indicators confirm the outlook for robust growth momentum in the near term

Americas:

FOMC kept rates on hold as expected, confirms start of balance sheet reduction in Oct; hurricanes could temporarily boost inflation

Economic data

(UK) AUG PUBLIC FINANCES (PSNCR): £0.0B V -£3.9B PRIOR; PUBLIC SECTOR NET BORROWING: +£5.1B V +£6.4BE

(CH) SWISS AUG TRADE BALANCE (CHF): 2.17B V 3.5B PRIOR

(CH) SWISS AUG M3 MONEY SUPPLY Y/Y: 4.0% V 4.0% PRIOR

(NL) Netherlands Aug Unemployment Rate: 4.7% v 4.8%e

(NL) Netherlands Sept Consumer Confidence Index: 23 v 26 prior

Fixed Income Issuance:

(ES) SPAIN DEBT AGENCY (TESORO) SELLS TOTAL €4.68B VS. €4.0-5.0B INDICATED RANGE IN 2021, 2026, 2028 AND 2044 BONDS

(FR) FRANCE DEBT AGENCY (AFT) SELLS TOTAL €6.99B VS. €6.0-7.0B INDICATED RANGE IN 2020, 2023 AND 2024 OATS

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.2% at 382.7, FTSE flat 7271.5, DAX +0.2% at 12598, CAC-40 +0.5% at 5267, IBEX-35 +0.2% at 10311, FTSE MIB +0.5% at 22470, SMI +0.4% at 9133, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes:

European Indices trade mostly higher across the board with the weaker Euro helping push Indices higher following the FOMC rate decision yesterday.

Corporate activity was light this morning, with notable movers including Capita trading sharply lower after missing estimates while Kier Group trades higher after Full year results. Else where Ryanair remains on focus after press reports that the Pilots have rejected a cash bonus offer to work overtime, while CRH trades higher after acquiring Ash Grove.

On the US front Calgon Carbon called sharply higher after being acquired.

Equities

Consumer discretionary [ Capita [CPI.UK)] -10% (Earnings), Mitchells & Butlers [MAB.UK] -5.1% (Trading update), Ryanair [RYA.UK] -2.2% (Reprtedly pilots turn down £12K cash bonus offer to work overtime]

Industrials: [Kier [KIE.UK] +8.6% (Earnings)]

Material: [CRH [CRH.UK] +2.8% (To acquire Ash Grove for enterprise value of $3.5B)]

Healthcare:[Nicox [COX.FR] +2.6% (Announces licensing agreement with Eyevance for commercialization of ZERVIATETM in the United States; To receive upfront payment of $6M)]

Speakers

BOJ Gov Kuroda: To adjust policy as appropriate and to maintain momentum towards 2% price target- post rate decision press conference

Currencies

The dollar continues hold ground after gaining sharply yesterday, while the Yen weakens following the BoJ rate decision. Then USD/JPY rallied over 100 pips following the rate decision.

Fixed Income

Thursday's liquidity report showed Wednesday's excess liquidity fell to €1.729T from €1.747T and use of the marginal lending facility rose to €137M from €86M.

Corporate issuance saw $0.6B come to market in quieter session, bringing Week to date issuance to just above $13B and Monthly issuance at ~ $102B

Looking Ahead

07:30 (BR) Brazil Central Bank (BCB) Quarterly Inflation Report (QIR)

08:00 (PL) Poland Central Bank (NBP) Sept Minutes

08:00 BR) Brazil Mid-Sept IBGE Inflation M/M: 0.1%e v 0.4% prior; Y/Y: 2.6%e v 2.7% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Sept Philadelphia Fed Business Outlook: 17.2e v 18.9 prior

08:30 (US) Initial Jobless Claims: 300Ke v 284K prior; Continuing Claims: 1.98Me v 1.944M prior

08:30 (CA) Canada July Wholesale Trade Sales M/M: -0.7%e v -0.5% prior

08:30 (US) Weekly USDA Net Export Sales

09:00 (US) July FHFA House Price Index M/M: 0.4%e v 0.1% prior

09:00 (MX) Mexico July Retail Sales M/M: +0.1%e v -1.1% prior; Y/Y: 1.0%e v 0.4% prior

09:00 (RU) Russia Gold and Forex Reserve w/e Sept 15th: No est v $427.3B prior

09:00 (ZA) South Africa Central Bank (SARB) Interest Rate Decision: Expected to cut Interest Rate by 25bps to 6.75%

10:00 (US) Aug Leading Index: No est v 0.3% prior

10:00 (EU) Euro Zone Sept Advance Consumer Confidence: -1.5e v -1.5 prior

10:30 (US) Weekly EIA Natural Gas Inventories

12:00 (US) Fed reports Q2 Financial Accounts: Household Change in Net Worth: No est v $2.347T prior