Sample Category Title

Euro Unchanged As Eurozone Flash GDP Matches Estimate

EUR/USD is unchanged in the Wednesday session. Currently, the pair is trading at 1.1715, down 0.20% on the day. On the release front, euro zone Flash GDP edged up to 0.6% in the second quarter, matching the forecast. In the US, the focus will be on housing data, with the release of Building Permits and Housing Starts. Both indicators are expected to remain unchanged from their previous readings. As well, the FOMC will release the minutes of its July policy meeting. On Thursday, the euro zone releases Final CPI and the ECB publishes the minutes of its July meeting. In the US, the key events are unemployment claims and the Philly Fed Manufacturing Index.

The euro zone economy has now picked up speed over three straight quarters. In the second quarter, euro zone Flash GDP posted a gain of 0.6%, slightly stronger than the 0.5% reading in Q1. Much of the credit for improved growth in the euro zone must be given to Germany, the largest economy in the bloc and the star performer. Germany's GDP expanded 0.6% in the second quarter. Consumer spending, a key driver of economic growth, continues to propel economic growth, and Germany has now posted 12 straight quarters of growth. Higher wages and increased government spending have also boosted the economy. The export sector remains strong, despite the stronger euro, as global demand for German products, especially automobiles, remains firm. Positive economic conditions in Germany have translated into a stronger euro zone economy, which has experienced higher growth and lower unemployment.

The euro has taken a pause in August, but the currency has posted impressive gains in recent months, with EUR/USD jumping 3.5% in July. The euro has received a boost from a stronger euro zone economy, as well as growing political risk in the United States, as the Trump administration has lurched from crisis to crisis, and hasn't managed to pass a single major bill through Congress. The latest fiasco for Trump was the alt-right protest in Charlottesville, where one protester was killed by a suspected white supremacist. Trump initially refused to condemn white supremacists for the violence, and faced a strong backlash of criticism from both Democrat and Republican lawmakers. Trump finally came out with a statement on Monday which condemned hate groups, including white supremacists. However, the brash president followed up on Tuesday by again blaming both sides in Charlottesville, raising questions about Trump's reluctance to unequivocally condemn hate group such as white supremacists.

European Futures Higher | FOMC Minutes May Reveal New Details | Sterling Needs Help | Crude Inventory Data Under...

Sceptical About Dollar Rally

Hawkish FOMC Minutes Could Push Gold Lower

UK Earning Data Could Save Sterling

API Data Tumbled While Focus on Crude Inventory

European markets are keeping their attention on the upcoming FOMC minutes. The saggy inflation data could have an influence on the Fed minutes. The Fed see a valid reason to keep the interest rates at their current if the inflation does not create much rifts in the market. What the market would be looking at is the wind-up timing in relation to the Fed's balance sheet. The market is expecting the Fed to announce the winding down of the size of their balance sheet to begin in September

Sceptical About Dollar Rally

The king dollar is trading lower despite the fact that US retail sales data confirmed that the consumers are supporting the economy. The growth in the US wages is making consumers spend more. The US Empire State index also showed some solid reading and printed the highest level since September 2014. The index plays a fair share in the GDP growth and this confirms that we could be looking at a much better GDP growth for 2017.

The dollar rally picked up more fuel on the back of the hawkish comments by a top Federal Reserve official. Traders pay close attention to Bill Dudley, the New York Fed Chief, because of his influential position in the committee. He clearly wants the market to acknowledge that it would be a mistake to consider that the Fed cannot trigger the button for another interest rate hike this year.

However, we are sceptical about the current momentum in the dollar. The CFTC data is still showing that speculators are still piling into the second most crowded trade.

The retail sales number does provide a reasonable picture of the consumer health, however, the Fed considers inflation dearer. We do know that the inflation data was saggy and the fed could acknowledge this in their minutes. Therefore, we do think that the prospects of another rate hike are still remote for this year.

Hawkish FOMC Minutes Could Push Gold Lower

The bullish dollar is shifting the focus away from the safe havens. The yellow metal, the Japanese yen and the Swiss Franc, all are out of fuel. The Increasing odds of the US interest rate hike could push the gold price below the 1250 and this could happen if the upcoming FOMC minutes deliver some hawkish tone.

UK Earning Data Could Save Sterling

Sterling took the beating and the punishment could continue if the economic numbers do not provide support. The UK average earnings in the three months may rise to 2 percent. Even if this number is printed, there would not be a moment of celebration because inflation would still easily be outpacing it and creating more pressure for consumers. The inflation data was the only element which was supporting the argument that the Bank of England should tighten the monetary policy. However, the latest inflation number has eased off those concerns for the BOE. The unemployment rate is expected to remain at 4.5 percent, the lowest number since 1975 despite Brexit.

The Sterling drop against the euro is more prominent and a lot of this is just purely insane. This is because investors are hanging their hopes that the euro-Sterling rally could push the pair to parity. The UK is heading to leave the EU bloc and investors do not believe that the U.K. has any firm plan to save the economy from a catastrophe.

API Data Tumbled While Focus on Crude Inventory

Crude oil moved higher as the API inventory data tumbled. However, the data which matters the most is your crude inventory number and this is what investors will be looking at more closely. The forecast is that the downtrend would confirm a drop of 3.4 million barrels. Remember the oil curve is already in backwardation. It implies that the contracts approaching their expiration are trading at a higher price in comparison to the forward contract. In simple words, it shows that the supply concerns are fading fast and the market could be looking at a situation when demand would exceed supply.

FOMC Minutes Eyed As Fed Prepares First Balance Sheet Reduction

- FOMC minutes could offer interest rate and balance sheet clues;

- EIA expected to report seventh consecutive decline in inventories;

- GBP bounces on stronger labour market data;

- Eurozone growth momentum accelerates in July.

US futures are pointing to a higher open on Wall Street on Wednesday, as risk appetite continues its recovery ahead of the release of the FOMC minutes from the July meeting.

The Federal Reserve has become noticeably less hawkish in recent months as inflation has failed to pick up as much as policy makers had anticipated, causing some to question whether the current pace of tightening is appropriate. I expect the minutes will reflect this growing unease within the Fed which could once again weigh on interest rate expectations. Markets are currently pricing in only a 49% chance of another rate hike this year and even that has only been achieved in the last couple of days following some hawkish remarks from William Dudley.

The balance sheet is something else that traders will likely be looking for further clarity, with the central bank strongly hinting that it will start reducing it from September. The minutes may offer insight into how it plans to do so, although until now the market reaction to this has been very muted.

Other notable data points today including building permits and housing starts for the US, as well as crude inventory data from EIA. API reported a 9.2 million barrel draw down on Tuesday which didn’t provoke much of a reaction in the markets, despite the fact that a repeat of this today would represent the biggest drop since September last year and the seventh consecutive week of declines. Should EIA report a similar number then we may see a more significant reaction in Brent and WTI.

Sterling has rebounded slightly on Wednesday after the latest labour market data showed unemployment fell to 4.4% in the three months to June while average earnings rose by 2.1%. Both of these numbers exceeded market expectations offering some reprieve for the pound which suffered losses on Tuesday on the back of softer than expected inflation data.

While the numbers were generally good, the key takeaway from the release remains the fact that real wages are falling as wage growth lags behind inflation. While the gap between the two has narrowed and is likely to shorten again over the course of the next year or so, it is likely to continue to weigh on growth in the meantime. Even an apparently tight labour market isn’t easing the situation, with the Bank of England saying earlier this month that Brexit uncertainty is likely holding down wages.

There was also good news for the eurozone this morning, with GDP data for the second quarter exceeding expectations at 2.2% and indicating that the recovery is becoming more broad based. The eurozone may be a little late to the party but we’ve seen significant improvement in the region over the last year and the latest figures are extremely encouraging. There is obviously still a long way to go but there is certainly reason for optimism.

Technical Outlook: AUDUSD – Near-Term Bears Are Taking A Breather, Thick 4-Hr Cloud Expected To Cap Recovery

The Aussie bounced on Wednesday after repeated failure to clear support at 0.7818 (50% retracement of 0.7571/0.8065 upleg), as near-term bears off 0.8065 peak are taking a breather.

Recovery is so far holding below initial resistance at 0.7877 (Tuesday's high / broken Fibo 38.2%) with thickening 4-hr cloud (spanned between 0.7900 and 0.7949) weighing on near-term action and seen capping extended upticks.

Renewed attempts lower require close below 0.7818 handle to open way for extension towards 0.7760 (Fibo 61.8% of 0.7572/0.8065).

Conversely, sustained break above 4-hr cloud will generate initial signal of higher low at 0.7807 (Tuesday's low) and would trigger further retracement of pullback from 0.8065.

Res: 0.7877, 0.7893, 0.7900, 0.7948

Sup: 0.7832, 0.7818, 0.7807, 0.7760

Elliott Wave Analysis: USDJPY Intra-Day View

USDJPY accelerated higher during Asian trading hours, into wave five of three after a triangle formation in red wave four. As such, this can be final trust up before we get a new deeper pullback into wave four. Ideally, pair will come back down to 110.20/40 area from where we will expect a new continuation higher.

USDJPY, 1H

EUR/USD Analysis: Bounces Off Dominant Support

The EUR/USD currency exchange remains predictable, as another target was reached during Tuesday's trading session. As it can be observed on the chart, the Euro reached the support line of the medium term descending channel pattern against the US Dollar.

On Wednesday various events can be expected. First of all, a new short term ascending pattern should be spotted. Secondly, as the pair has reached above the resistance of the weekly S1, the rate will set out to test the resistance of the various hourly SMAs, which are located near the 1.1770 mark. However, it is most likely that the resistance of the simple moving averages will be passed.

GBP/USD Analysis: Recovers Slightly

Weak UK and strong US fundamentals on Tuesday resulted in a 108-pip fall of the GBP/USD exchange rate within six hours. As a result, the Pound fell down to the 1.2852 mark, but subsequently remained relatively stable slightly above 1.2860.

Strongly bearish technical indicators suggest that a rebound should occur in this session. The nearest resistance is the weekly S2 at 1.2887; this level, however, should be breached without any hindrance.

It is expected that the rate will trade in the 1.2900/40 area by Thursday morning if no surprising fundamentals or events shake the market tremendously. In case the Pound is pressured to the downside, losses should be limited circa 1.2840.

USD/JPY Analysis: Moves Above Weekly R1

Following a breach of the upper line of the junior channel, the US Dollar continued to appreciate against the Yen near the weekly R1. Further potential upwards was strengthened by solid data mid-session that resulted in a surge up to the 110.80 mark.

Subsequently, the rate resumed its up-trend until early morning when the lack of market volatility guided the Greenback sideways.

This change in sentiment together with worsening technical indicators demonstrate that the rate is likely to fall today, possibly seeking to retrace from the upper channel line circa 110.00. The 55– and 200-hour SMAs are located near this area.

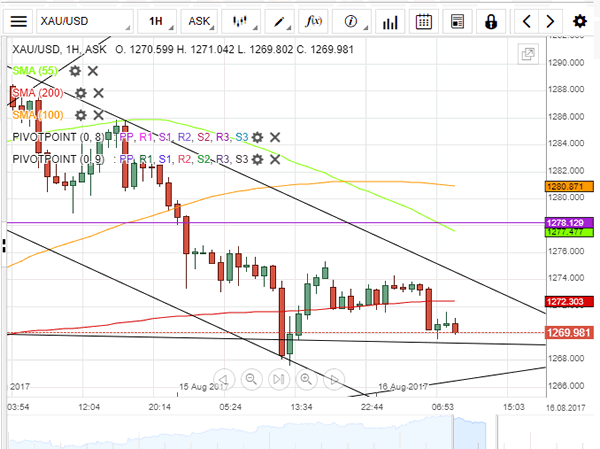

XAU/USD Analysis: Reaches 1,270 Mark

The bullion reached the targeted 1,270 mark, as the better than expected fundamental data was released during the middle of Tuesday's trading session. In addition, the fall that occurred due to the release of the data stopped exactly at the support of the junior descending channel pattern.

As a result on Wednesday it can be expected that the commodity price will reach higher and touch the upper trend line of the channel. However, by looking at the various level of significance and taking into account already broken lines, it can be assumed that the movement of the metal could be rather flat until it reaches the support of the active dominant pattern just below the 1,270 mark

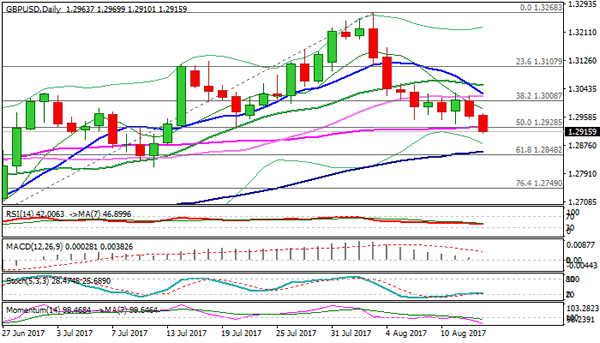

Technical Outlook: Cable Bounces On Upbeat Jobs Data But Limited Upside Is Seen For Now

Cable bounced to 1.2900 zone after better than expected UK jobs data. Jobless claims fell by 4.2K in July, beating forecast for increase in claims by 3.7K while Unemployment rate fell to 4.4% in June from 4.5% forecast / previous month.

The most significant release was average earnings, with headline earnings coming at 2.1% in June vs 1.8% forecast, while ex-bonus earnings rose to 2.1% from 2.0% previous month/ forecast.

Strong jobs sector numbers are bullish signal, but pound remains under pressure and is in downtrend since the beginning of August. Long bearish candle that was left on Tuesday continues to weigh on near-term action, seeing limited upside action before bears resume for renewed attack at daily cloud (spanned between 1.2869 and 1.2818) which contained downside attempts for now.

Broken 55SMA marks solid barrier at 1.2930, followed by Tuesday’s high at 1.2970 and key barrier at 1.3000 (psychological resistance, reinforced by falling daily Tenkan-sen) which is expected to cap extended upticks.

Res: 1.2902, 1.2930, 1.2970, 1.3000

Sup: 1.2840, 1.2811, 1.2749, 1.2715