Sample Category Title

USD/JPY Still Sideways

Price continues to move sideways on the Daily chart as the Nikkei failed to resume the corrective phase. The rebound invalidated the breakdown from the symmetrical triangle and now is expected to reach and retest the 38.2% retracement level and the third warning line (WL3). A valid breakout above the WL3 will confirm a further increase in the upcoming weeks, while only a valid breakdown below the wl1 will signal a major drop.

AUD/USD Throwback

Price increased significantly today and now is retesting the median line (ML) of the major ascending pitchfork. It has erased the yesterday's losses, even if the USDX stays higher. Could drop again if the US data will come in better later and the FOMC Meeting Minutes will signal a rate hike in the upcoming period.

Has found support at the lower median line (lml) of the minor descending pitchfork and now could climb to retest the median line (ml) as well. Only a valid breakdown from the minor ascending pitchfork will confirm a major drop.

Pound Trying to Hold Steady after Steep Decline

The British Pound is trying to steady its stance at 1.28, after stronger than expected UK wage growth figures spared it from further losses, following a heavy decline noted in the latest inflation figures that were released yesterday.

Once the results of the UK jobs report are absorbed by the headlines, these are unlikely to remain a key driver behind British Pound price action. The UK inflation data has crumbled optimism over the Bank of England (BoE) raising interest rates any time soon. I think that even the most cautious optimist must be realizing that the case for the BoE to raise UK rates over the coming months is very slim. The Sterling is more sensitive to monetary policy speculation than anything else at present. This means that with interest rate rise talk fading into the background, this will result in many buyers losing interest in the Pound. I don't think there are any chances that the BoE will be raising UK interest rates over the upcoming months.

Let's also not forget that Governor Carney famously flirted with the prospects of higher UK interest rates just a few years ago, before backtracking. While the BoE has previously flirted with increasing interest rates, there is no reason for the Monetary Policy Committee (MPC) to vote for higher rates any time soon.

The only reason for the interest rate talk in the first place are UK inflationary pressures, but the British Pound, rebounding from its milestone 30+ year low below 1.20 in late 2016, should ease inflationary pressures later this year. This, coupled with the ongoing EU uncertainty and falling growth, will ultimately encourage the BoE to at least maintain rates at the current record low.

There is no real incentive for investors to be long on Pound as it stands. Unless there is another round of excessive USD weakness, traders are likely to jump on future opportunities to enter selling positions, when the Pound/Dollar is trading above 1.30.

EURUSD continues dipping lower

The Eurodollar is continuing to gradually ease away from its two-year high above 1.19, which was seen earlier this month, with the EURUSD at risk to dipping below 1.169 at time of writing. Reports that ECB President, Mario Draghi, will downplay any policy shift announcement at next week's Jackson Hole conference, seems to have been used as a catalyst to sell the Euro. I also wouldn't rule out the possibility that investors might be starting to price some German election premiums, into their portfolios.

With this in mind, the Euro has rallied significantly in recent months and it is possible that the EURUSD will remain under pressure in the near-term. My view is that Euro buyers will consider entering more buying positions on EURUSD, as it heads towards 1.15.

Investors need to remain alert ahead of FOMC minutes

I don't think US interest rate expectations are as dead in the water, as the markets have suggested in recent weeks. If the FOMC minutes release, due this evening, provides a hint to investors that the Federal Reserve could pull the trigger on another US interest rate rise late in 2017, the USD is in line to receive another bid.

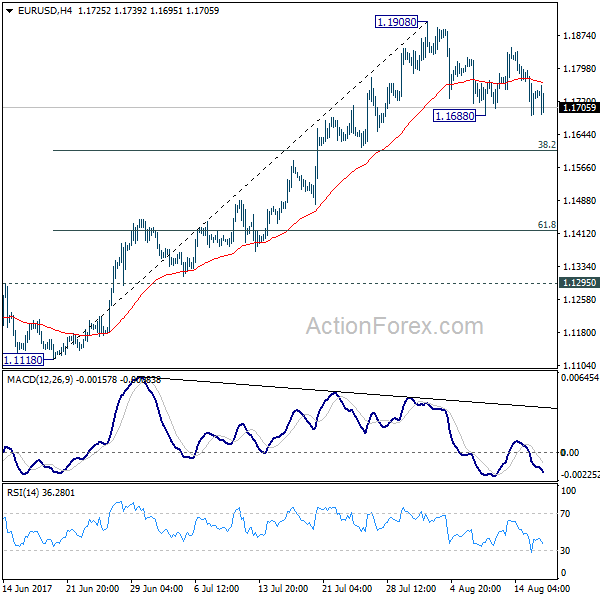

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1753; (P) 1.1796 (R1) 1.1822; More...

EUR/USD dips mildly today but it's staying above 1.1688 support and intraday bias stays neutral. Consolidation from 1.1908 is still in progress and deeper pull back might be seen. But downside should be contained by 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring rebound. On the upside, break of 1.1908 will extend recent up trend to 1.2042 long term support turned resistance next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

Euro Mildly Lower as ECB Draghi Won’t Deliver Big Monetary Policy Speech at Jackson Hole

Commodity currencies are the strongest performers today as lifted by firm risk appetite. European indices are trading in black while US futures point to higher open. Sterling is staging a relief recovery after solid job data. Euro, on the other hand, trades softer on report that ECB President Mario Draghi will not sign policy changes in the upcoming Jackson Hole conference. Yen and Swiss are also weak in risk seeking markets. Nonetheless, the greenback remains the strongest one for the week as markets await FOMC minutes.

ECB Draghi won't deliver a big monetary policy speech at Jackson Hole

Euro trades generally lower today in response to a Reuters report that ECB president Mario Draghi will not deliver new messages regarding monetary policy in the Jackson Hole symposium in US on August 25. A spokesman of ECB said that Draghi will focus on the theme of symposium instead, that is, fostering a dynamic global economy. Reuters also quoted an unnamed source saying that "expectations that this will be a big monetary policy speech are wrong".

While the Euro trades softer, it's staying well above key near term support levels against Dollar, Yen and Sterling, and maintain bullishness against these currencies. It's understandable that the September ECB meeting is an important one regarding tapering the asset purchase program. And Draghi would like to keep his cards close to his chest.

Separately, ECB governing council member Ardo Hansson said that "as the exit from the asset buying program is in line with the recovery of economic activity, everything is calm." And, "after the completion of the purchase of bonds, the reinvestment of bonds already bought will continue for some time; that is, when the earlier purchased bonds expire, new ones will be bought instead."

Released from Eurozone, Q2 GDP grew 0.6% qoq, unchanged from Q1's figure and met expectations. Italian GDP rose 0.2% qoq in Q2, same as in Q1, and met expectations.

Sterling relief recovery as unemployment dropped to lowest since 1975

Sterling recovers against other major currencies, but not commodity currencies today, after solid job data. Claimant counts dropped -4.2k in July, much better than expectation of 3.7k rise. Unemployment rate dropped to 4.4% in the three months to June. Unemployment rate also hit the lowest level since 1975. Average weekly earnings rose by 2.1% 3moy in June, above expectation of 1.8% 3moy. However, some economists point out that real wage growth was at -0.5% yoy after adjustment for inflation.

The recovery is in the Pound is more of a relief rally as at least the set of job data is overall positive. But there is no change in the view that BoE is still distant from raising interest rate. Lower than expected inflation, which some talks that CPI won't hit 3% this year, would not prompt BoE for an early hike. And the central bank would at least wait for the result of Brexit negotiation before acting.

FOMC minutes watched for views on inflation

Regarding minutes of July FOMC meeting, the markets will be particularly interested in knowing policy-makers' views on inflation outlook. In the accompanying statement of the meeting, policymakers acknowledged that the overall inflation and the measure excluding food and energy prices (core inflation) have "declined" and are "running below 2%". The removal of the word "somewhat" signaled the weakness in inflation is more than the Fed had anticipated. We would look to see if the Fed maintained the view that weak inflation is "transitory".

So far, Fed officials have been rather cautious regarding the chance of another rate hike by the end of the year. The main exception is New York Fed President William Dudley while remained "favor of doing another rate hike later this year". After his comments earlier this week, market pricing of Fed rate path returned to normal. For now, Fed fund futures are pricing in 98.6% chance for Fed to stand pat in September. Chance of a rate hike in December is roughly 50%.

In US, housing starts dropped -4.8% mom to 1.15m annualized rate in July, below expectation of 1.22m. Building permits dropped -4.1% mom to 1.22m, below expectation of 1.25m. Canada International securities transactions dropped -0.92b in June.

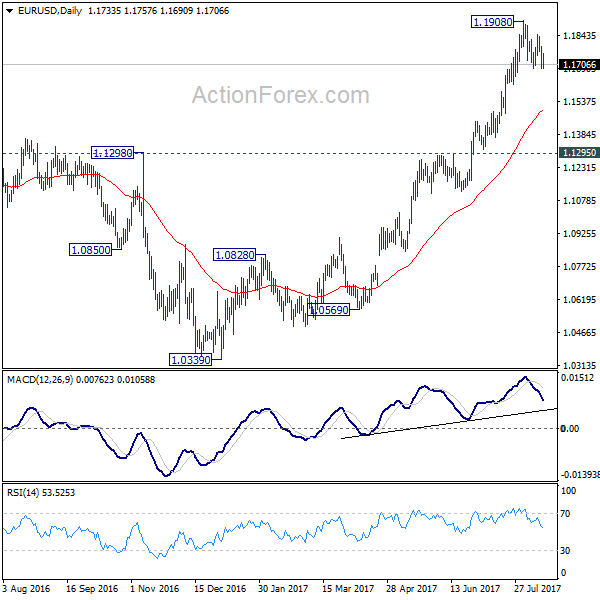

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1753; (P) 1.1796 (R1) 1.1822; More...

EUR/USD dips mildly today but it's staying above 1.1688 support and intraday bias stays neutral. Consolidation from 1.1908 is still in progress and deeper pull back might be seen. But downside should be contained by 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring rebound. On the upside, break of 1.1908 will extend recent up trend to 1.2042 long term support turned resistance next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Jul | 0.10% | -0.10% | -0.20% | |

| 01:30 | AUD | Wage Cost Index Q/Q Q2 | 0.50% | 0.50% | 0.50% | 0.60% |

| 08:00 | EUR | Italian GDP Q/Q Q2 P | 0.40% | 0.40% | 0.40% | |

| 08:30 | GBP | Jobless Claims Change Jul | -4.2K | 3.7K | 6.0K | 3.5K |

| 08:30 | GBP | Claimant Count Rate Jul | 2.30% | 2.30% | ||

| 08:30 | GBP | Average Weekly Earnings 3M/Y Jun | 2.10% | 1.80% | 1.80% | 1.90% |

| 08:30 | GBP | ILO Unemployment Rate 3M Jun | 4.40% | 4.50% | 4.50% | |

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | 0.60% | 0.60% | 0.60% | |

| 12:30 | CAD | International Securities Transactions (CAD) Jun | -0.92B | 23.45B | 29.46B | |

| 12:30 | USD | Housing Starts Jul | 1.16M | 1.22M | 1.22M | |

| 12:30 | USD | Building Permits Jul | 1.22M | 1.25M | 1.25M | 1.28M |

| 14:30 | USD | Crude Oil Inventories | -3.0M | -6.5M | ||

| 18:00 | USD | FOMC Meeting Minutes Jul |

CAC Gains Ground as Eurozone GDP Improves

The CAC index has posted strong gains in the Wednesday session. Currently, the index is at 5,195.75, up 1.07% on the day. On the release front, euro zone Flash GDP edged up to 0.6% in the second quarter, matching the estimate. In the US, the Federal Reserve will release the minutes of its July policy meeting. On Thursday, the euro zone releases Final CPI and the ECB publishes the minutes of its July policy meeting.

The euro zone economy continues to improve in 2017, so there were no surprises as euro zone Flash GDP posted a strong gain of 0.6% in the second quarter, edging above the 0.5% gain in Q1. The euro zone economy has now picked up speed over three consecutive quarters. Much of the credit for improved growth in the euro zone goes to Germany, whose economy continues to fire on all four cylinders. Germany has been the locomotive of the euro zone. France, the second largest economy in the bloc, reported economic growth of 0.5% in the second quarter, with a strong export sector boosting economic growth. Despite the positive GDP numbers, inflation remains well below the ECB target of 2%. In July, French Final CPI declined 0.3%, after two readings of 0.0%. Euro zone Final CPI slowed to 1.3% in July, its weakest gain this year. Weak inflation levels have hampered ECB plans to wind down its asset purchases program, although the markets are prepared for a statement from the ECB concerning the scheme in September or October.

Global stock markets have been on a roller coaster, as tensions between the US and North Korea reached a fever pitch last week, only to recede this week. The CAC declined 2.9% last week, but has rebounded, recording gains of 2.0% so far this week. At the same time, although a military conflict remains unlikely in the Korean peninsula, tensions remain high, and if the war of words ratchets higher, investors could head for safer pastures and dump shares in favor of the Japanese yen and gold, which was the case last week.

The markets will be all ears as the Federal Reserve releases its July minutes. At that policy meeting, the Fed outlined plans to reduce its bloated balance sheet of $4.2 trillion. The Fed hasn't given any details about when it will commence trimming the balance sheet. Analysts expect September will be the start date, and the Fed could start the process by slowing its asset purchases by modest amount, such as $10 billion/mth.

Draghi Said to Wait Until Autumn Before Giving Clues on QE Exit Plans

Notes/Observations

- UK Jun Wage and unemployment data bucked tepid economic growth

- European Q2 GDP data continues to show broadening expansion in region

- Draghi said to wait until autumn before giving clues on QE exit plans; Jackson Hole event risk possibly diminished

Overnight

Asia:

- PBOC Adviser Sheng Songcheng: Cut of RRR is not in line with China's policy, more likely to use SLF, MLF and PSL. China unlikely to tighten monetary policy in H2

Europe:

- UK Govt paper said to reject the idea of a customs border in the Irish sea. UK wants to maintain a common travel area, which would allow UK and Irish citizens to move freely.

- Germany Fin Min Schaeuble believed ECB observes its mandate; did not agree with German constitutional court

Americas:

- Fed's Kaplan (moderate, voter) reiterates call to start balance sheet unwind soon. Appropriate to be patient on timing on next rate hike.

- Fed Vice Chair Fischer: Efforts to loosen bank rules are 'dangerous' and extremely short sighted

- Congressional Budget office (CBO): If Trump ends key Obamacare funds premiums estimated to increase 20% in 2018 for Silver plans; removing cost-sharing payments would increase federal deficit by $194B from 2017 to 2018

Energy:

- Weekly API Oil Inventories: Crude: -9.2M v -7.84M prior

Economic Calendar

- (RO) Romania Q2 Advance GDP Q/Q: 1.6% v 1.2%e; Y/Y: 5.9% v 5.1%e

- (HU) Hungary Q2 Preliminary GDP Q/Q: 0.9% v 1.1%e; Y/Y: 3.2% v 3.6%e

- (CZ) Czech Q2 Advance GDP Q/Q: 2.3% v 0.8%e; Y/Y: 4.5% v 3.0%e

- (TH) Thailand Central Bank (BoT) left its Benchmark Interest Rate unchanged at 1.50% (as expected) for its 17th straight pause in the current easing cycle

- (NL) Netherlands Q2 Preliminary GDP Q/Q: 1.5% v 0.6%e; Y/Y: 3.3% v 2.3%e

- (IT) Italy Q2 Preliminary GDP Q/Q: 0.4% v 0.4%e; Y/Y: 1.5% v 1.4%e

- (PL) Poland Q2 Preliminary GDP Q/Q: 1.1% v 0.8%e; Y/Y: 3.9% v 3.8%e

- (UK) July Jobless Claims Change: -4.2K v +3.5K prior; Claimant Count Rate: 2.3% v 2.3% prior

- (UK) Jun Average Weekly Earnings 3M/Y: 2.1% v 1.8%e; Weekly Earnings ex Bonus 3M/Y: 2.1% v 2.0%e

- (UK) Jun ILO Unemployment Rate: 4.4% v 4.5%e; Employment Change 3M/3M: _125K v +97Ke

- Sells € in 6-month Bills; Avg Yield: % v -0.410% prior; Bid-to-cover: x v 2.80x prior

- Sells € in 12-month Bills; Avg Yield: % v -0.374% prior; Bid-to-cover: x v 1.94x prior

- (EU) Euro Zone Q2 Preliminary GDP (2nd reading) Q/Q: 0.6% v 0.6%e; Y/Y: 2.2% v 2.1%e

**Fixed Income Issuance:

- (IN) India sold total INR160B vs. INR160B indicated indicated in 3-month and 12-month Bills

- (DK) Denmark sold DKK600M in 3-month Bills; Yield: -0.660% v -0.680% prior; bid-to-cover: 5.0x v x 1.0x prior

- (ES) Spain Debt Agency (Tesoro) sold total €4.47B vs. €4.0-5.0B indicated range in 6-month and 12-month bills

- (EU) ECB allotted $35M in 7-day USD Liquidity Tender at fixed 1.66% vs $35M prior

- (SE) Sweden sold SEK10B vs. SEK10B indicated in 3-month bills; Avg Yield: -0.7615% v -0.7525% prior; Bid-to-cover: 1.65x v 1.45x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

**Equities**

Indices [Stoxx600 +0.7% at 379, FTSE +0.6% at 7429, DAX +0.9% at 12280, CAC-40 +1.0% at 5193, IBEX-35 +0.7% at 10549, FTSE MIB +1.1% at 21962, SMI +0.5% at 9056, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes:

European Indices continue the positive sentiment seen this week with further strong rises today, led by the CAC which trades higher by over 1%, as well as the Dax. Press reports that ECB's Draghi will make no new announcements at the Jackson hole meeting also helped boost Equities. In corporate news, Balfour Beatty outperforms after strong results, while Admiral trades lower after in line results. Evotec trades at 16 year highs after raising guidance following the completion of Aptuit acquisition, whilst Akza Nobel trades higher after reaching an agreement with Elliot after months of dispute.

Looking ahead notable earners out of the US include Target and Performance Food Group.

Equities

- Consumer discretionary [Lookers [LOOK.UK] -4.6% (Earnings)]

- - Consumer Staples [ ICA Gruppen [ICA.SE] -5% (Earnings)]

- Materials: [ Akza Nobel [AKZA.NL] +1% (Earnings), BHP [BLT.UK] +2.2% (Elliot announces 5% holding)]

- Industrials: [Maersk [MAERSKB.DK] +2% (Earnings) ]

- Financials: [Admiral [ADM.UK] -6.8% (Earnings), Swiss Life [SLHN.CH] -1.3% (Earnings)]

- Healthcare: [Evotec [EVT.DE] +3.3% (Completes acquisition of Aptuit, Raises outlook)]

- Real Estate: [Balfour Beatty [BBY.UK] +5.1% (Earnings)]

Speakers

- ECB's Draghi reportedly will not deliver a fresh policy message at Jackson Hole and hold off on policy discussion until the autumn. Would focus on the theme of the symposium, fostering a dynamic global economy

- - ECB's Hansson (Estonia): Wage pressures are beginning to emerge despite low inflation but are very uneven

- ECB'S Lautenschlaeger (Germany): Banks not as far advanced as we would like to see them in Brexit preparations

- Turkey Econ Min Zeybekci: Expected Q3 GDP growth over 7%

- Moody's: Political tensions in the ruling African National Congress will weigh on South Africa's growth

- Thailand Central Bank policy statement noted that today's decision to keep policy steady was unanimous and reiterated that monetary policy remained accommodative. Strong THB currency (Baht) was affecting business and would monitor currency closely; Baht rising on external position . Inflation seen returning to target band later than expected as headline inflation to slowly rise in H2. No need to cut rates further

- - Indonesia President Widodo: 2018 GDP growth seen at 5.4% and inflation at 3.5%

- China govt said to take measures to increase foreign investment

Currencies

- EUR/USD stayed within recent ranges but saw some whippy price action after reports circulated that ECB chief Draghi would not deliver any fresh policy message at the upcoming Jackson Hole symposium next week. There was some speculation that Draghi might provide some groundwork on how the ECB would exits its unconventional policy. Draghi has not been at the Jackson Hole conference for the past 3 years and his last appearance foreshadowed the launch of QE. EUR/USD hovering around 1.1730 area ahead of the NY morning.

- The GBP currency was firmer following better wage data out of the UK. The BOE noted that they were watching wage growth closely as it gauged whether the increase in inflation was creating longer-lasting pressure on prices. GBP/USD probing the 1.29 level after testing fresh 5-week lows earlier in the session below 1.2850.

- The easing of tension on the Korean Peninsula continued to help weaken the JPY currency. USD/JPY approaching the 111 neighborhood.

Fixed Income

- Bund futures trades at 163.80 up 3 ticks after ECB's Draghi is reportedly not planning on delivering a fresh policy message at Jackson Hole next week. Downside targets 163.50 followed by 162.56. To the upside the 164.50 to 165.20 remains key resistance.

- Gilt futures trades at 127.39 down 31 ticks as UK Unemployment Rate hits lowest level since 1975. A resumption to the upside could eye 128.25 then 128.75. A move back below 126.51 targets 125.97

- Wednesday's liquidity report showed Tuesday's excess liquidity in the Euro Zone rose to €1.742T from €1.741T and use of the marginal lending facility fell to €94M from €427M prior.

- Corporate issuance saw $19B come to market via 5 issuers headlined by Amazon's $16B (fourth-largest high grade deal of 2017 ) 7 part offering, and Etrade's $1B 2-part offering.

Looking Ahead

- (NG) Nigeria July CPI Y/Y: No est v 16.1% prior

- (CO) Colombia July Consumer Confidence Index: No est v -11.7 prior

- 05:30 (PT) Portugal Debt Agency (IGCP) to sell €0.75-1.0B in 3-month and 12-month bills

- 06:00 (IL) Israel Q2 Advance GDP Y/Y: 3.1%e v 1.4% prior

- 06:00 (RU) Russia to sell combined RUB40B in 2022 and 2027 OFZ bonds

- 06:45 (US) Daily Libor Fixing

- 07:00 (US) MBA Mortgage Applications w/e Aug 11th: No est v +3.0% prior

- 07:00 (ZA) South Africa Jun Retail Sales M/M: 0.1%e v 0.9% prior; Y/Y: 2.3%e v 1.7% prior

- 07:00 (BR) Brazil Aug FGV Inflation IGP-10 M/M: -0.1%e v -0.8% prior

- 08:00 (BR) Brazil IBGE Services Sector Volume Y/Y: -4.0%e v -1.9% prior

- 08:00 (UK) Baltic Dry Bulk Index

- 08:30 (US) July Housing Starts: 1.22Me v 1.215M prior; Building Permits: 1.25Me v 1.275M prior (revised from 1.254M)

- 08:30 (CA) Canada Jun Int'l Securities Transactions: No est v C$29.5B prior

- 10:30 (US) Weekly DOE Crude Oil Inventories

- 11:30 (BR) Brazil weekly Currency Flow data

- 12:00 (CA) Canada to sell 30-year bonds

- 14:00 (US) FOMC Minutes from July 26th decision

Daily Technical Analysis: GBP/USD Flat/Range Zone Has Been Broken

The GBP/USD has broken, the range/flat zone to the downside, going below W L5 camarilla pivot. At this point we see a retracement towards 1.2900 zone. The retracement happened after the good UK data namely wages and jobs. However the trend is still in place and the spike towards the POC (D H4, Trend line, ATR high, W L4, order block) 1.2930-40 could possibly be sold towards 1.2830 and 1.2815. Breakout below 1.2795 could further weaken the price to 1.2750.

Technical Outlook: EURGBP Pulls Back From Fresh High, Overall Bulls Remain Intact

The pair hit fresh high at 0.9142 today (the highest since early Oct 2016) but was unable to hold gains and dipped below 0.9100 handle after upbeat UK jobs data boosted pound.

Overall bulls remain firmly in play for now, underpinned by rising 10SMA at 0.9063 (initial support) and ascending 4-hr cloud (spanned between 0.9041 and 0.9000, with lower boundary being reinforced by rising 20SMA) which is expected to contain dips before larger bulls from higher base at 0.8300 zone resume.

However, deeper pullback cannot be ruled out as daily RSI emerges from overbought territory and shows a plenty of space at the downside.

Violation of 0.9000 handle would risk extension towards 0.8942 (rising daily Kijun-sen) and 0.8890 (27 July trough).

Res: 0.9100, 0.9142, 0.9207, 0.9244

Sup: 0.9082, 0.9063, 0.9041, 0.9000

DAX Higher As Eurozone GDP Improves In Q2

The DAX index has posted considerable gains in the Wednesday session, continuing the upward movement seen on Monday. The DAX is trading at 12,280.75, up 0.82% on the day. On the release front, euro zone Flash GDP edged up to 0.6% in the second quarter, matching the forecast. In the US, the Federal Reserve will release the minutes of its July policy meeting. On Thursday, the euro zone releases Final CPI and the ECB publishes the minutes of its July policy meeting.

It was report card day for the euro zone economy, with the release of Flash GDP for the second quarter. The reading was positive, posting a gain of 0.6%, edging above the 0.5% gain in Q1. The euro zone economy has now picked up speed over three consecutive quarters. Much of the credit for improved growth in the euro zone goes to Germany, whose robust economy continues to impress. Germany’s GDP expanded 0.6% in the second quarter. Consumer spending, a key driver of economic growth, continues to propel economic growth, and the country has now posted 12 straight quarters of growth. Higher wages and increased government spending have also boosted the economy. The export sector remains strong, despite the stronger euro, as global demand for German products, especially automobiles, remains firm.

Geopolitical tensions in the Korean peninsula have abated, and this has helped boost global stock markets. The DAX has rebounded after sharp losses last week, following some saber-rattling between Washington and Pyongyang. The two countries engaged in an escalating war of words, with North Korea threatening to attack Guam, which hosts a major US military base. Although a military conflict remains unlikely, tensions remain high, and if tensions again rise, investors could head for safer pastures, and dump shares in favor of the Japanese yen and gold, which was the case last week.