Sample Category Title

USD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Marubozu

• Time of formation: 14 Nov 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 15 Feb 2017

• Trend bias: Down

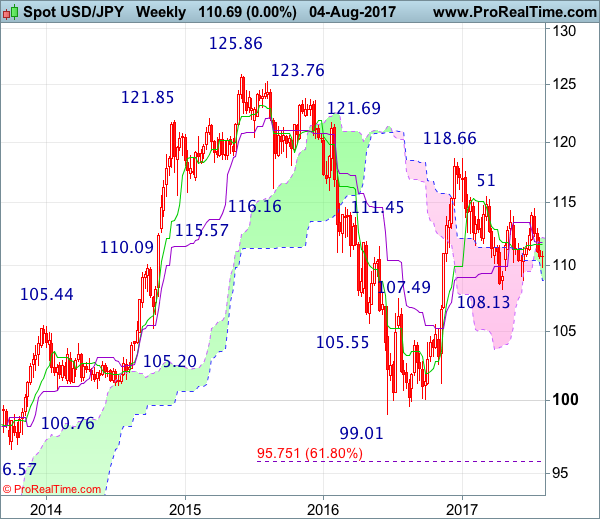

USD/JPY – 110.65

The greenback resumed recent decline after brief bounce to 110.98 and our short position entered at 112.00 met indicated downside target at 110.00 (with 200 points profit) as the pair fell to as low as 109.85 on Friday, having said that, as dollar found good support there and has rebounded in part due the broad-based strength in the greenback, suggesting minor low has been formed and consolidation above this level is in store, hence initial upside risk is for test of 111.03-05 (current level of the Tenkan-Sen and Friday’s high), however, a daily close above there is needed to bring retracement of recent decline to 111.70-75 but the Kijun-Sen (now at 112.18) should hold and bring another decline later.

On the downside, expect pullback to be limited to 110.30-40 and bring such a rebound. Below said support at 109.85 would signal the decline from 114.50 is still in progress and may extend weakness to 109.40, having said that, as broad outlook remains consolidative, reckon downside would be limited to previous support at 108.82 and the part shall stay above previous chart support at 108.13, bring another rebound later.

Recommendation : Short entered at 112.00 met indicated downside target at 110.00 with 200 points profit and would sell again at 112.00 for 110.00 with stop above 113.00.

On the weekly chart, despite last week’s anticipated fall to 109.85, the subsequent rebound from there formed a doji star and if this week ends with a white candlestick, this would signal the retreat from 114.50 has ended, then test of the Kijun-Sen (now at 111.82) and the upper Kumo (now at 112.11) would be seen, however, still reckon upside would be limited to 112.90-00 and 113.55-60 should hold, price should falter well below resistance at 114.50, bring another decline later.

On the downside, below said support at 109.85 would signal the fall from 114.50 is still in progress, then further weakness to 109.40 would follow, however, reckon 108.82-84 (previous support as well as current level of the lower Kumo) would limit downside and price should stay well above support at 108.13, bring recovery later. In the event dollar drops below support at 108.13, this would signal early fall from 118.66 top has resumed and may extend weakness to 117.40-50, then 117.00 but downside should be limited to 106.50-55 (61.8% Fibonacci retracement of 99.01-118.66), bring rebound later.

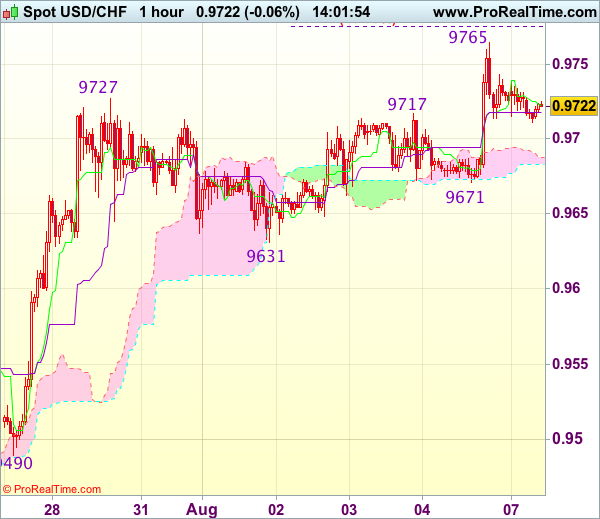

Trade Idea : USD/CHF – Buy at 0.9700

USD/CHF - 0.9722

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9723

Kijun-Sen level : 0.9718

Ichimoku cloud top : 0.9688

Ichimoku cloud bottom : 0.9683

Original strategy :

Buy at 0.9700, Target: 0.9800, Stop: 0.9665

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9685, Target: 0.9785, Stop: 0.9650

Position : -

Target : -

Stop : -

Although the greenback has retreated after rising to 0.9765 on Friday and consolidation below this level would be seen, reckon downside would be limited to support at 0.9671 and bring another rise later, above said resistance at 0.9765 would signal recent upmove is still in progress, then further gain to 0.9775 (50% projection of 0.9438-0.9727 measuring from 0.9631) and later 0.9800-10 (61.8% projection) would follow but reckon 0.9830-40 would hold from here, bring another retreat later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as 0.9680-85 should limit downside. Below 0.9671 support would defer and suggest top is possibly formed, risk test of support at 0.9631 but break there is needed to add credence to this view, bring retracement of recent rise to 0.9596 (previous resistance turned support).

Market Update – Asian Session: Markets Gain On US Payrolls

Asia Summary

Asian markets opened mostly higher after strong US employment data on Friday. Commodity names especially seeing strength in Australia. Quotes on China rebar reach a 4-yr high after a report said that Hebei Province will curb steel production during the winter (Hebei province is China largest iron and steel producer). According to Citi, winter steel curbs could cut daily production by 8%.

NZD fell slightly to 0.7397 after Q3 New Zealand inflation expectation survey generally showed a decline in expectations. The only rise in the survey was 2-yr GDP, which rose to 2.64% from 4.89% seen in Q2. Korean won and equities moved a bit higher after UN approved fresh sanctions against North Korea that was also supported by China and Russia.

Key economic data

(NZ) NEW ZEALAND Q3 INFLATION EXPECTATION SURVEY: 2-YEAR INFLATION EXPECTATION 2.09% V 2.17% PRIOR

(JP) JAPAN JULY OFFICIAL RESERVE ASSETS: $1.260T V $1.249T PRIOR

(AU) AUSTRALIA JULY CONSTRUCTION INDEX: 60.5 V 56.0 PRIOR (highest since 2005)

(AU) AUSTRALIA JUL ANZ JOB ADVERTISEMENTS M/M: 1.5% V 2.7% PRIOR

Speakers and Press

China

(CN) China Banking Regulatory Commission (CBRC) said to have extended June deadline for banks to submit risk assessments until mid-August

(CN) China Foreign Min Wang Yi: China and the US are reluctant to fight trade war

(US) US Army to no longer use drones made by China based SZ DJI Technology Co, citing 'cyber vulnerabilities' – financial press

(CN) Shanghai Stock Exchange to increase scrutiny of M&A, transfer of control deals and other corporate actions that could lead to financial risk in the market –Xinhua

(CN) PBOC to include internet finance into macro prudential assessment (MPA) - China Daily

New Zealand

(NZ) New Zealand Treasury: Economic growth may lift slightly over the next year

Korea

(KR) UN Security Council voted unanimously to impose new sanctions on North Korea, includes cutting $1B in exports related to North Korea

Europe

(UK) Said that is prepared to pay up to €40B to the EU to settle its Brexit bill - Telegraph

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.6%, Hang Seng +0.3%, Shanghai Composite -0.2%, ASX200 +1.1%, Kospi +0.4%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.4%, Dax +0.2%, FTSE100 +0.2%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1802-1.1766; JPY 110.85-110.60; AUD 0.7949-0.7912; NZD 0.7417-0.7397

Dec Gold -0.1% at 1,263/oz; Sept Crude Oil -0.3% at $49.42/brl; Sept Copper -0.4% at $2.88/lb

(CN) China PBOC OMO injects CNY250B in 7 and 14-day reverse repos v CNY120B prior

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT: 6.7228 V 6.7132 PRIOR

(KR) South Korea Treasury sells 5-yr pre-issuance Govt bonds at 1.98%

(KR) South Korea sells KRW700B v KRW700B offered in 6-month monetary stabilization bonds; avg yield 1.33% v 1.32% prior

(TH) Thailand sells THB5B in 3-month bills; avg yield 1.05074%; bid-to-cover ratio 3.65x

Equities notable movers

Hong Kong/China

China Resources Cement, 1313.HK Reports 1H net HK$1.64B v HK$0.26B y/y, Rev HK$13.2B v HK$11.3B y/y; +3.4%

Japan

Square Enix, 9684.JP Reports Q1 Net ¥8.4B v ¥5.3B y/y; Op ¥12.9B v ¥8.9B y/y; Rev ¥57B v ¥51.1B y/y; +7.4%

Toshiba, 6502.JP Auditor is said to be considering endorsing FY16 securities or financial report - Japanese Press; +6.5%

Korea

Samsung Engineering,028050.KR Awarded KRW1.13T order; +9.1%

Australia

Starpharma, SPL.AU Two phase 3 trials related to VIVAGEL met primary objective; +8%

AirXpanders, AXP.AU Received A$15M under a debt financing transaction with Oxford Finance; +5.7%

Other

TMUS Sprint said to be resuming prelim talks on merger with T-Mobile - financial press

Trade Idea : GBP/USD – Sell at 1.3110

GBP/USD - 1.3057

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3050

Kijun-Sen level : 1.3095

Ichimoku cloud top : 1.3191

Ichimoku cloud bottom : 1.3164

Original strategy :

Sell at 1.3110, Target: 1.3010, Stop: 1.3145

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3110, Target: 1.3010, Stop: 1.3145

Position : -

Target : -

Stop : -

As cable has recovered after Friday’s selloff to 1.3024, suggesting minor consolidation would be seen and recovery to the Kijun-Sen (now at 1.3095) cannot be ruled out, however, reckon previous support at 1.3112 would turn into resistance and limit upside, bring another decline later, below said support at 1.3024 would signal the fall from 1.3269 top is still in progress and may extend weakness to 1.3005-10 (100% projection of 1.3269-1.3112 measuring from 1.3165) but a break below support at 1.2999 is needed to retain bearishness, then decline to 1.2986 (61.8% Fibonacci retracement of 1.2812-1.3269) and possibly 1.2955-60 would follow.

In view of this, we are looking to sell cable on recovery as previous support at 1.3112 should limit upside. Only break of 1.3165 is needed to signal low is formed instead, bring a stronger rebound to 1.3200 but upside should be limited to 1.3240-50 and price should falter below said resistance at 1.3269.

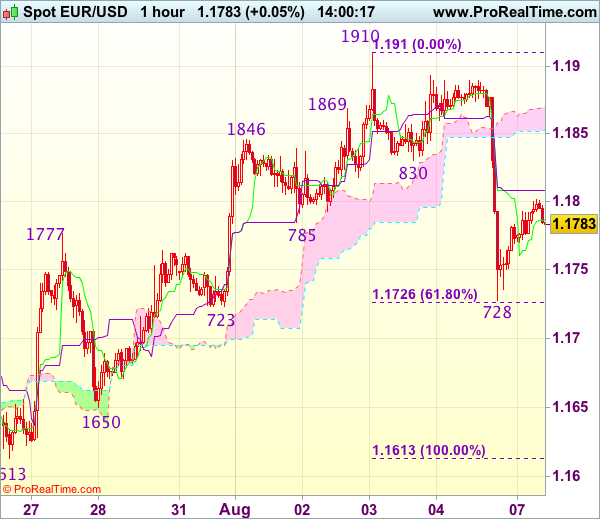

Trade Idea : EUR/USD – Sell at 1.1830

EUR/USD - 1.1789

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1787

Kijun-Sen level : 1.1809

Ichimoku cloud top : 1.1870

Ichimoku cloud bottom : 1.1854

Original strategy :

Sell at 1.1810, Target: 1.1710, Stop: 1.1845

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1830, Target: 1.1730, Stop: 1.1865

Position : -

Target : -

Stop : -

As the single currency found support at 1.1728 after dropping sharply on Friday, suggesting consolidation above this level would be seen and recovery to the Kijun-Sen (now t 1.1809) cannot be ruled out, however, reckon previous support at 1.1830 would limit upside and bring another decline later, below 1.1750 would bring test of 1.1723-28 (previous support as well as 61.8% Fibonacci retracement of 1.1613-1.1910), break there would add credence to our view that top has been formed at 1.1910 last week, bring further fall to 1.1700 but reckon support at 1.1650 would hold.

In view of this, we are looking to sell euro again on recovery as 1.1830 previous support should limit upside. Above the lower Kumo (now at 1.1854) would defer and risk a stronger rebound to 1.1870 but price should falter below said last week’s high at 1.1910, bring another decline later.

Trade Idea : USD/JPY – Buy at 110.45

USD/JPY - 110.73

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 110.75

Kijun-Sen level : 110.53

Ichimoku cloud top : 110.42

Ichimoku cloud bottom : 110.16

Original strategy :

Buy at 110.50, Target: 111.50, Stop: 110.15

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.45, Target: 111.45, Stop: 110.10

Position : -

Target : -

Stop : -

Friday’s rally above 110.98 resistance signals a temporary low has been formed at 109.85 last week and consolidation above this level would be seen with mild upside bias for this rebound to bring retracement of recent decline, hence gain to 111.29-30 (previous resistance and 61.8% Fibonacci retracement of 112.20-109.85) is likely, however, break there is needed to add credence to this view, bring retracement of recent decline to 111.50 but price should falter below another previous resistance at 111.71.

In view of this, we are looking to buy dollar on dips as 110.40-50 should limit downside and bring another rise later. Below 110.15-20 would defer but only break of 110.00 would signal the rebound from 109.85 has ended, bring retest of this level, below there would extend recent decline to 109.70 and later towards 109.50.

Australia’s Construction Sector Expanded At Its Fastest Pace In 12 Years In July

For the 24 hours to 23:00 GMT, the AUD declined 0.31% against the USD and closed at 0.7932 on Friday.

LME Copper prices rose 0.6% or $40.0/MT to $6330.0/MT. Aluminium prices declined 0.1% or $1.5/MT to $1890.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7939, with the AUD trading 0.09% higher against the USD from Friday's close, after recent data showed that Australia construction sector activity surged in July.

Overnight data revealed that Australia's AiG performance of construction index rose to a level of 60.5 in July, notching its highest level since 2005. In the previous month, the index had registered a reading of 56.0.

The pair is expected to find support at 0.7893, and a fall through could take it to the next support level of 0.7848. The pair is expected to find its first resistance at 0.7982, and a rise through could take it to the next resistance level of 0.8026.

Looking forward, Australia's NAB business confidence index for July, scheduled for release in the early hours tomorrow, will attract significant amount of market attention.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Germany’s Factory Orders Sharply Advanced In June

For the 24 hours to 23:00 GMT, the EUR declined 0.8% against the USD and closed at 1.1783 on Friday.

In economic news, data showed that Germany's seasonally adjusted factory orders rose more-than-expected by 1.0% on a monthly basis in June, highlighting a pickup in momentum in the nation's industrial sector. Factory orders had registered a revised rise of 1.1% in the previous month, while markets were expecting for a gain of 0.5%.

The greenback gained ground against its key counterparts on Friday, after an upbeat US jobs report reinvigorated hopes of another Federal Reserve (Fed) interest rate hike before the end of the year.

Data indicated that non-farm payrolls in the US climbed more-than-expected by 209.0K in July, pointing to further tightening in the nation's labour market. Non-farm payrolls had registered a revised rise of 231.0K in the prior month, while market participants had anticipated for an advance of 180.0K. Additionally, the nation's unemployment rate touched a sixteen-year low in July, after it eased to 4.3%, meeting market expectations. Unemployment rate had recorded a level of 4.4% in the prior month.

Moreover, the nation's average hourly earnings of all employees climbed 0.3% on a monthly basis in July, in line with market expectations, rising by the most in five months. Average hourly earnings of all employees had risen 0.2% in the prior month. Also, the nation's trade deficit narrowed more-than-anticipated to $43.6 billion in June, as exports surged to a nearly three-year high. Investors had envisaged the nation's trade deficit to narrow to $44.5 billion, after recording a revised deficit of $46.4 billion in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.1794, with the EUR trading 0.09% higher against the USD from Friday's close.

The pair is expected to find support at 1.1718, and a fall through could take it to the next support level of 1.1643. The pair is expected to find its first resistance at 1.1879, and a rise through could take it to the next resistance level of 1.1965.

Ahead in the day, traders will keep a close watch on Germany's industrial production data for June and the Euro-zone's Sentix investor confidence data for August. Moreover, the US labour market conditions index for July and consumer credit data for June, slated to release later in the day, will be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Pound Trading A Tad Higher In The Asian Session

For the 24 hours to 23:00 GMT, the GBP declined 0.72% against the USD and closed at 1.3047 on Friday. The US gained ground against the Pound following better than expected US jobs data for July.

In the Asian session, at GMT0300, the pair is trading at 1.3053, with the GBP trading marginally higher against the USD from Friday’s close.

The pair is expected to find support at 1.2997, and a fall through could take it to the next support level of 1.2940. The pair is expected to find its first resistance at 1.3137, and a rise through could take it to the next resistance level of 1.3220.

Moving ahead, market participants will look forward to the UK’s Halifax house prices data for July, scheduled to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Marginally Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.66% against the JPY and closed at 110.68 on Friday.

In the Asian session, at GMT0300, the pair is trading at 110.72, with the USD trading a tad higher against the JPY from Friday’s close.

The pair is expected to find support at 110.14, and a fall through could take it to the next support level of 109.55. The pair is expected to find its first resistance at 111.18, and a rise through could take it to the next resistance level of 111.63.

Going ahead, investors will closely monitor Japan’s trade balance figures for June, slated to release overnight, followed by the Eco-Watchers survey data for July.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.