Sample Category Title

EURUSD Intraday Analysis

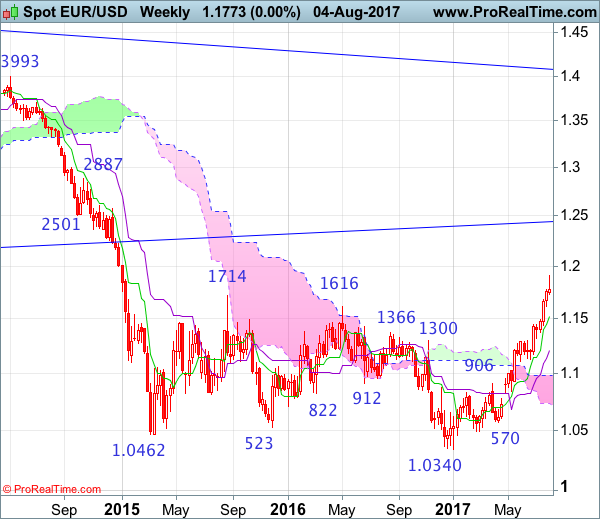

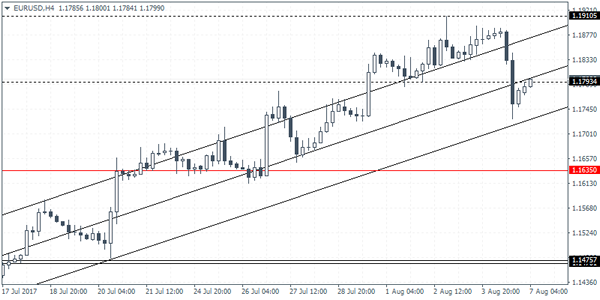

EURUSD (1.1799): The euro lost ground to the US dollar on Friday as price initially posted a 5-day low. However, the EURUSD managed to pull back to close the day at 1.1777. In the near term, EURUSD could be seen attempting to regain the 1.7934 handle which marks a minor support level. A breakout above this level could keep EURUSD range bound. However, price action suggests that any upside gains will be limited in the near term. Support at 1.6350 is quite likely to be the next destination for the EURUSD.

US Dollar Rebounds On Better Than Expected NFP

Friday's payrolls report from the US Labor department showed an overall positive outlook on the jobs market. The US economy added 209k jobs in July. This was higher than the median estimates of 182k. June's payrolls were also revised higher to 231k. Wage growth also increased 0.3%, in line with expectations while the US unemployment rate fell to 4.3%.

The US dollar posted strong gains on the back of the payrolls report helping the currency to recover some of the losses.

Looking ahead, it is likely to be a slow day for the markets. The German industrial production data is due today and is forecast to rise 0.2% on the month. The Swiss inflation data is also due later today and is expected to fall 0.3% on the month.

In the US trading session, Minneapolis Fed President, Neel Kashkari, an FOMC voting member will be starting the Fed speak this week.

Trade Idea: GBP/JPY – Sell at 145.50

GBP/JPY - 144.57

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term up

New strategy :

Sell at 145.50, Target: 143.50, Stop: 146.10

Position: -

Target: -

Stop:-

Sterling ran into heavy offers at 146.80 late last week and dropped sharply from there, suggesting the rebound from 144.05 has ended there, hence consolidation with downside bias is seen for another fall towards said support, however, break there is needed to retain bearishness and signal another leg of corrective decline from 147.75 top is underway, then further fall to 143.50 and later test of support at 143.30 would follow.

In view of this, would not chase this fall here and would be prudent to sell cable on subsequent recovery as 145.60-70 should limit upside. Above 146.00-10 would dampen this bearish scenario and risk a strong rebound to 146.50 but only break of said resistance at 146.80 would revive bullishness and signal correction from 147.75 has ended instead, bring further gain to 147.30-35 later.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

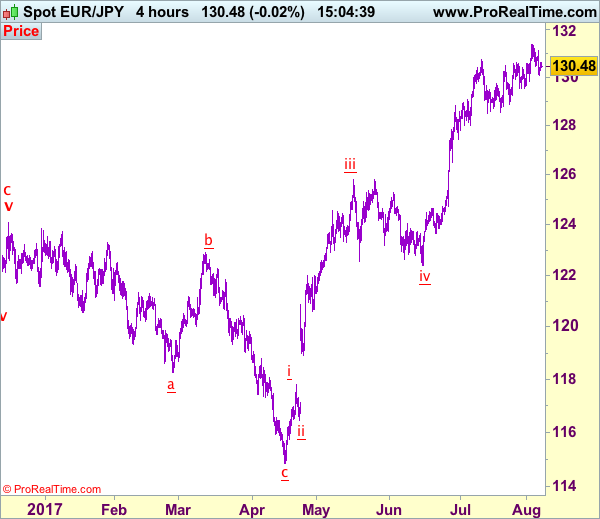

Trade Idea: EUR/JPY – Stand aside

EUR/JPY - 130.48

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term up

Original strategy:

Bought at 130.70, stopped at 130.40

Position: - Long at 130.70

Target: -

Stop: - 130.40

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Despite rebounding to 131.12 on Friday, the single currency ran into renewed selling interest there and has dropped sharply, dampening our bullishness and suggesting a temporary top has possibly been formed at 131.40 last week, hence downside risk remains for the retreat from there bring weakness to 130.00, then support at 129.84, break there would add credence to this view, bring retracement of recent rise to 129.54 and later towards 129.00.

In view of this, would be prudent to stand aside in the meantime. Above 130.90 would bring another test of 131.12 but only break of latter level would signal the retreat from 131.40 has ended, bring retest o this level later. Once this resistance is penetrated, this would confirm recent upmove has resumed and extend gain to 131.60, then 132.00-10, however, loss of upward momentum should prevent sharp move beyond 132.50-60 and reckon 132.90-00 would hold from here.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Week Ahead: After NFP Beat, U.S. Inflation Under The Spotlight

After three weeks of back-to-back losses, the dollar index received a boost following the robust U.S. jobs report. Not only did Non-Farm Payrolls beat expectations last month rising by 209,000 jobs versus earlier expectations of 183,000, but June's figures were also revised higher, to 231,000 from 222,000. The unemployment rate also declined to 4.3% from 4.4% and most importantly, average earning growth accelerated by 0.3% for the first time since February. Friday's strong jobs report will pave the way for the Fed to start reducing the balance sheet for September, but markets are still not confident that a third rate hike will occur this year. According to CME's FedWatch, markets still believe that chances of a rate hike in December is below 50% and for this perception to change, it requires inflation to accelerate after declining for five straight months. This is what we are going to know the week ahead.

The Producer Price index and the Consumer Price index are due to be released on Thursday and Friday, respectively. The CPI is what matters most to traders, and after declining from 2.7% in February to 1.6% in June, economists expect prices to edge up 1.8%. If inflation data suggests that prices are back on the rise, this will lead to revaluating the rate hike path and strengthens the case for a December rate hike.

The U.S. dollar, which suffered from steep losses over the past five months looks extremely oversold, despite Friday's rally. The Euro, Aussie, Swedish Krona and Danish Krone are all up by more than 10% against the Greenback in 2017. While much of the repricing occurred in response to a hawkish tilt in global central banks' rhetoric, I think the move was too fast, and we are likely to see some consolidation in the weeks to come. However, if U.S. inflation makes a U-turn and fiscal policy developments move on the right track, the dollar could have already found a short-term bottom.

I believe central banks such as the ECB and RBA will become more worried about the strength of their currencies. The Eurozone's economic health is much better than most have anticipated in 2017, and no doubt the central bank wants to prepare markets for tightening policy. However, if the Euro continued to appreciate from current levels, there will be many negative implications on the recovery, and that is why I believe the ECB will indirectly intervene in talking down the Euro. This is another reason why the dollar might have bottomed out on the short run.

The economic calendar is light in the week ahead, as many big traders and fund managers are off to enjoy the summer season. During such times markets become quiet and trading volumes fall. This does not necessarily mean that we shouldn't expect significant price fluctuations. That is why a close eye should remain on Washington as political drama might take center stage anytime.

German Industrial Production For June Is Also Due For Release Today

Market movers today

There is a relatively quiet week ahead in terms of data releases, including today.

In the euro area, we get numbers for the Sentixinvestor confidence today, which we expect to decline slightly to 27.6 in August from 28.3 in July. While business activity and economic confidence remain high, euro area PMIs did decline last week. Together with recent months without gains in the major stock indices, it poses the question of whether we have reached the top. A robust argument is the stronger EUR, which we expect to drag on the euro area growth out look and become a headwind to inflation in the coming years.

German industrial product ion for June is also due for release today. The previous five months showed consecutive monthly growth in industrial production, with the figure for May showing 1.2%. We expect the June figure to be 0.5%. We expect industrial production to continue showing strong figures for Q3, as in Q1 and Q2. German business confidence is high and we continue to see strong activity levels for companies, which supports growth in indust rial production.

In Denmark and Norway, we get industrial product ion data today. For more see the Scandi section on page 2.

Selected market news

On Friday, the US jobs report came out better than expected with a fall in the unemployment rate and unchanged wage growth (against expectat ions of a drop). In our view, the jobs report supports our view that the Fed will announce " quantitative tightening" in September and hike again in December, given that the Fed tends to put most weight on the unemployment rate. However, we think risk is skewed towards the Fed pausing its hiking cycle, as wage growth and inflation are low. See also Flash Comment US: Fed likely to continue tightening on strong jobs report, 7 August .

On Saturday, the UN Security Council passed a resolution imposing new economic sanctions on North Korea, which aims at reducing North Korean exports by USD1bn (a third of its total exports) by targeting North Korea's primary exports, including coal, iron, iron ore, lead, lead ore and seafood. See also CNN.

In the UK, The Telegraph reported that the UK is ready to pay a divorce bill of EUR40bn (against the EU's estimates in the range of EUR60-100bn) but only if the EU starts negotiations about the future relationship. A Downing Street source later denied the story, see The Guardian. In our view, the divorce bill remains the biggest obstacle to the Brexit negotiations, not least given the weak minority government in the UK. Previously, the EU's chief negotiator Michel Barnier had said the negotia ions were proceeding too slowly, meaning that negotiations in phase 1 (divorce bill, citizens' right s and Irish border) may not be concluded in October as hoped for.

Flash Comment US: Fed Likely To Continue Tightening On Strong Jobs Report

Market still eager to buy EUR/USD despite strong report. In terms of employment growth, we have now had two strong reports in a row, as employment rose by 209,000 in July and June was revised up to 231,000. Some of the strength in recent months is likely catch-up from the weakness earlier this year, as US growth seems stable slightly above trend growth.

As employment has risen for 82 consecutive months and the labour market recovery is expected to continue, focus was on the unemployment rate and wage growth, as these are more important for the Fed's decision whether to continue tightening monetary policy or not. The unemployment rate fell from 4.4% to 4.3%, while wage growth was unchanged at 2.5% against expectations of a fall to 2.4%. The combination of lower unemployment and better wage data sent EUR/USD slightly lower on the announcement, as it supports the Fed's case for announcing ‘quantitative tightening' (shrinking the balance sheet) in September and raising rates again in December.

However, we still think the jobs report underpins the Fed's dilemma: unemployment and (wage) inflation are low at the same time (the opposite situation of the 1970s), just as we wrote in Flash Comment US: Fed's dilemma, 7 July. Also, the Fed was slightly more dovish at the latest meeting (see FOMC Review: Smidgen dovish but it does not alter the overall picture, 26 July). The reason the Fed continues hiking is Janet Yellen and co's strong belief in the Phillips curve. The tight labour market should be sufficient to push wage growth and inflation higher eventually.

In our view, the problem is that the tightness of the labour market is not the only factor determining wage growth, as second-round effects following many years with low inflation have hit wage growth. When employees expect inflation to remain low, they can live with low wage growth, as real wage growth may still be solid, making it less likely inflation will reach the target.

EUR/USD fell slightly on the NFP announcement. However, the very modest price action shows the market's eagerness to buy EUR/USD. In our view, we could see a push towards 1.20 over the coming one to two weeks, as momentum is very strong. However, the move is likely to fade ahead of the Jackson Hole symposium on 24-26 August and the ECB meeting on 8 September, with the pressure building on the ECB to raise concerns about the strength of the EUR. The effective EUR is now back to September 2014 levels. Fundamentally, we expect EUR/USD to rise further over the coming 12 months on relative growth and valuations. We forecast EUR/USD at 1.22 in 12M.

Trade Idea: AUD/USD – Hold short entered at 0.8030

AUD/USD – 0.7925

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term up

Original strategy :

Sold at 0.8030, Target: 0.7880, Stop: 0.8000

Position: - Short at 0.8030

Target: - 0.7880

Stop: - 0.8000

New strategy :

Hold short entered at 0.8030, Target: 0.7880, Stop: 0.7985

Position: - Short at 0.8030

Target: - 0.7880

Stop:- 0.7985

Although aussie has recovered after falling to 0.7891 and consolidation above this level would be seen, as long as resistance at 0.7980 holds, mild downside bias remains for another retreat, below said support at 0.7891 would add credence to our view that wave iii top is possibly formed at 0.8066, bring correction in wave iv to 0.7875-80 (previous support) but break there is needed to retain bearishness, bring retracement of recent upmove to 0.7839 (previous resistance tuned support), however, downside should be limited to 0.7786 and price should stay well above wave i top at 0.7712.

In view of this, we are holding on to our short position entered at 0.8030. A sustained breach above said resistance at 0.7980 would abort and suggest low is possibly formed, bring a stronger rebound to 0.8000, then towards 0.8043 resistance, break there would signal the pullback from 0.8066 top has ended instead, bring retest of this level first, then 0.8100 and possibly 0.8140-50. We are keeping our latest bullish count that recent impulsive waves is unfolding as (1 2, (i)(ii), i ii) and may extend headway to aforesaid upside targets.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

US Data Surprises The Markets

On Friday, the US Department of Labour released Nonfarm Payrolls for July of 209K that beat the markets' expectation of 183K. Additionally, US Unemployment improved from 4.4% to 4.3% and average hourly earnings crept up by 0.3%, from 0.2% the year before, underlining a relatively strong labour market. Such a healthy set of data, which helped USD recover from 15-month lows against many currencies on Friday, should bolster labour market resiliency and, the slight increase in hourly earnings, may suggest that there is momentum in the economy to generate some inflation. The data may further help support the Federal Reserve's plans to hike rates before year end although any inflationary pressure is likely to be very small.

Markets also remain cautious as the political tension in the US is likely to increase with the news that President Trump's 'inner circle' is in focus, as a grand jury has been convened in Washington DC that is investigating the June 2016 meeting between Donald Trump Jr and Russian Nationals – which may further hamper USD strength. Following the data release, USD made 1% gains against EUR, GBP, JPY & Gold attracting broad short USD covering.

EURUSD backed off from highs on Friday, dropping over 175 pips before retracing higher to currently trade around 1.1790.

USDJPY remains in a relatively narrow trading range, currently trading around 110.75, after dropping to a 7-week low last week below 110.

GBPUSD gave up some of its recent gains on Friday, dropping over 100 pips following US employment data. Currently, GBPUSD is trading around 1.3055.

Gold suffered with USD strength, dropping over $10 on Friday. Gold is currently trading around $1,258.

WTI is still trading near to $50 pb, as representatives of OPEC meet for a 2-day gathering on Monday in Abu Dhabi to discuss why some of them are falling behind in pledges to reduce production. WTI is currently trading around $49.52.

At 08:30 BST, the markets get the latest look at the UK housing market, with the release of the Halifax House Price Index for July. Market consensus suggests a 0.2% rise in the month on month figure, bettering the previous reading of -0.1%, which is likely to be regarded as inflationary.

At 16:45 BST, Federal Reserve Bank of St. Louis President James Bullard gives a presentation on the U.S. economy and monetary policy in Nashville.

At 18:25 BST, Minneapolis Federal Reserve President Kaskari (FOMC voting member) is scheduled to speak at a moderated question and answer session in South Dakota.

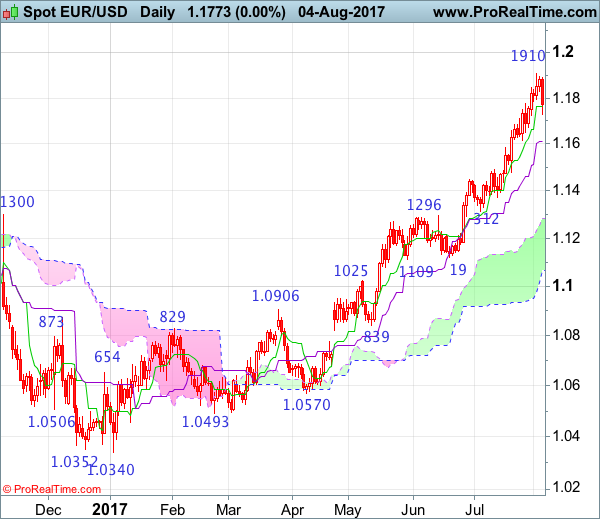

EUR/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 03 May 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 3 May 2016

• Trend bias: Sideways

EUR/USD – 1.1788

Despite rising to 1.1910 last week, the subsequent retreat suggests a temporary top has possibly been formed there and consolidation below this level is in store, however, a daily close below support at 1.1723-28 is needed to add credence to this view, bring retracement of recent upmove to 1.1670-75, then towards support at 1.1613 but only a sustained breach below the Kijun-Sen (now at 1.1611) would provide confirmation, then further fall to 1.1530-35 and then 1.1500 would follow.

On the upside, although initial recovery to 1.1830 cannot be ruled out, reckon upside would be limited and price should falter below said resistance at 1.1910, bring another retreat later. A break of 1.1910 would signal recent upmove from 1.0340 is still in progress and may extend headway to 1.1950, then psychological level at 1.2000, however, loss of upward momentum should prevent sharp move beyond 1.2165 and price should falter below 1.2220-30, bring retreat later.

Recommendation: Buy at 1.1590 for 1.1790 with stop below 1.1490.

On the weekly chart, although the single currency rose to 1.1910 last week, the quick retreat from there formed a shooting star and if this week ends with a black candlestick, this would add credence to this bearish reversal pattern and suggest a temporary top is possibly formed, bring weakness to 1.1613 support, break there would signal correction of recent upmove has commenced for test of the Tenkan-Sen (now at 1.1515) and later towards 1.1435, however, ,downside should be limited to 1.1370 and support at 1.1312 should remain intact, bring rebound later.

On the upside, expect recovery to be limited to 1.1840-50 and price should falter below said resistance at 1.1910, bring retreat later. A break above said last week’s high at 1.1910 would signal the major rise from 1.0340 low is still in progress and may extend gain to 1.1950, then 1.1200, however, weakening of near term upward momentum would prevent sharp move beyond 1.2160-70 and reckon 1.2220-30 would hold, price should falter below 1.2300-10, bring another retreat later.

‘