Sample Category Title

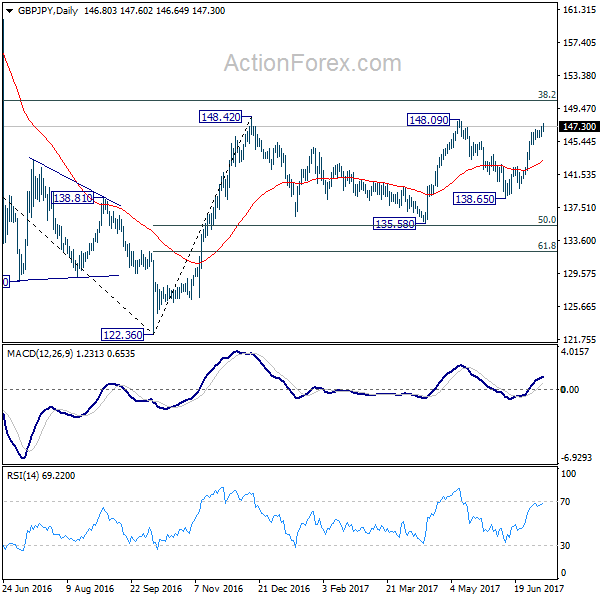

GBP/JPY Daily Outlook

Daily Pivots: (S1) 146.15; (P) 146.71; (R1) 147.39; More....

GBP/JPY's rally continues to as high as 147.60 and intraday bias stays on the upside for 148.09/42 resistance zone. Decisive break there will extend whole rally from 122.36 to long term fibonacci level at 150.43 next. On the downside, break of 146.03 support is needed to indicate short term topping. Otherwise, outlook will remains bullish in case of retreat.

In the bigger picture, rise from medium term bottom at 122.36 is expected to continue to 38.2% retracement of 196.85 to 122.36 at 150.43. Decisive break there will carry long term bullish implications and pave the way to 61.8% retracement at 167.78. In case the sideway pattern from 148.42 extends, we'd be looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside.

Australia’s Construction Sector Activity Slightly Slowed In June

For the 24 hours to 23:00 GMT, the AUD declined 0.32% against the USD and closed at 0.7583.

LME Copper prices rose 0.2% or $10.5/MT to $5828.5/MT. Aluminium prices rose 0.7% or $12.5/MT to $1925.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7585, with the AUD trading a tad higher against the USD from yesterday's close.

Earlier today, data showed that Australia's AiG performance of construction index declined to a level of 56.0 in June, following a level of 56.7 in the previous month.

The pair is expected to find support at 0.7566, and a fall through could take it to the next support level of 0.7548. The pair is expected to find its first resistance at 0.7609, and a rise through could take it to the next resistance level of 0.7634.

Moving ahead, investors will look forward to Australia's NAB business confidence and Westpac consumer confidence data, slated to release next week.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

ECB Minutes Show Discussion Of An Exit From Monetary Stimulus

For the 24 hours to 23:00 GMT, the EUR rose 0.62% against the USD and closed at 1.1421, after minutes of the European Central Bank (ECB) June meeting indicated that policymakers are tilting towards tapering the central bank's quantitative easing programme.

According to minutes, board members mulled over the possibility of tapering the ECB's asset purchases in coming months if confidence in the region's inflation outlook improves further. However, officials decided against it for now as recovery in the Euro-bloc's economic activity had yet to result in higher inflation. Moreover, the ECB stressed on the need to maintain caution in communication as it could trigger unwarranted movements in financial markets.

In other economic news, data showed that Germany's seasonally adjusted factory orders rebounded 1.0% on a monthly basis in May, undershooting market expectations for a rise of 1.9%. In the prior month, factory orders had registered a revised drop of 2.2%. Meanwhile, the nation's Markit construction PMI fell to a level of 55.1 in June, compared to a reading of 55.3 in the previous month.

The greenback lost ground against its major counterparts, on the back of softer than expected jobs data in the US that pointed to some loss of momentum in the nation's job growth.

Data revealed that the ADP private sector employment in the US climbed less-than-expected by 158.0K in June, compared to market consensus for a rise of 188.0K. The private sector employment had recorded a revised increase of 230.0K in the previous month. Further, the nation's initial jobless claims registered an unexpected rise to a level of 248.0K in the week ended 01 July 2017, rising for the third straight week and confounding market expectations of a drop to a level of 243.0K. Initial jobless claims had registered a level of 244.0K in the previous week. Also, the nation's trade deficit narrowed less-than-anticipated to a level of $46.5 billion in May, after registering a deficit of $47.6 billion in the prior month.

Another set of economic data showed that the US ISM non-manufacturing PMI surprisingly rose to a level of 57.4 in June, while investors had envisaged for a drop to a level of 56.5. In the previous month, the PMI had registered a reading of 56.9. Additionally, the nation's final Markit Markit services PMI unexpectedly advanced to a level of 54.2 in June, expanding at its fastest pace since January 2017 and compared to a reading of 53.6 in the previous month. The preliminary figures had recorded a drop to a level of 53.0. Moreover, the nation's MBA mortgage applications rebounded 1.4% in the week ended 30 June 2017, following a decline of 6.2% in the prior week.

In the Asian session, at GMT0300, the pair is trading at 1.1414, with the EUR trading 0.06% lower against the USD from yesterday's close.

The pair is expected to find support at 1.1354, and a fall through could take it to the next support level of 1.1294. The pair is expected to find its first resistance at 1.145, and a rise through could take it to the next resistance level of 1.1486.

Going ahead, investors will focus on Germany's industrial production data for May, slated to release in a few hours. Additionally, in the US, the crucial non-farm payrolls, unemployment rate and average hourly earnings data, all for June, slated to release later today, will attract significant amount of market attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Pound Trading A Tad Higher, Ahead Of A Slew Of Economic Data In The UK

For the 24 hours to 23:00 GMT, the GBP rose 0.26% against the USD and closed at 1.2969.

In the Asian session, at GMT0300, the pair is trading at 1.2970, with the GBP trading slightly higher against the USD from yesterday’s close.

The pair is expected to find support at 1.2933, and a fall through could take it to the next support level of 1.2895. The pair is expected to find its first resistance at 1.2996, and a rise through could take it to the next resistance level of 1.3021.

Trading trends in the GBP today is expected to be determined by the release of Britain’s industrial, manufacturing and construction output data along with total trade balance figures, all for May, slated to release in a few hours. Also, the NIESR GDP estimate for the three months to June, will also be on investors’ radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the USD slightly declined against the JPY and closed at 113.13.

In the Asian session, at GMT0300, the pair is trading at 113.70, with the USD trading 0.5% higher against the JPY from yesterday's close.

The pair is expected to find support at 113.11, and a fall through could take it to the next support level of 112.53. The pair is expected to find its first resistance at 114.06, and a rise through could take it to the next resistance level of 114.43.

Next week, investors will keep a close watch on Japan's (BOP basis) trade balance, Eco-Watchers survey, tertiary industry index and final industrial production data.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Annual Inflation Growth Weakest In 7 Months In June

For the 24 hours to 23:00 GMT, the USD declined 0.36% against the CHF and closed at 0.9606.

On the macro front, Switzerland's consumer price index (CPI) advanced less-than-expected by 0.2% on an annual basis in June, rising at its weakest pace in seven months. In the prior month, the CPI had risen 0.5%, while lower market participants expected for a rise of 0.3%. Meanwhile, on a monthly basis, the nation's consumer prices unexpectedly eased 0.1% in June, compared to an advance of 0.2% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 0.9611, with the USD trading slightly higher against the CHF from yesterday's close.

The pair is expected to find support at 0.9587, and a fall through could take it to the next support level of 0.9564. The pair is expected to find its first resistance at 0.9647, and a rise through could take it to the next resistance level of 0.9684.

Ahead in the day, traders will await the release of Switzerland's unemployment rate data for June.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canada’s Building Permits Surged In May

For the 24 hours to 23:00 GMT, the USD rose 0.16% against the CAD and closed at 1.2978.

Macroeconomic data indicated that Canada's building permits jumped 8.9% on a monthly basis in May, higher than market expectations for a gain of 1.0% and after recording a revised advance of 0.5% in the previous month. On the contrary, the nation's international merchandise trade deficit expanded to a level of C$1.09 billion in May, following a revised deficit of C$0.55 billion in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.2985, with the USD trading a tad higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2941, and a fall through could take it to the next support level of 1.2896. The pair is expected to find its first resistance at 1.3012, and a rise through could take it to the next resistance level of 1.3038.

Looking forward, Canada's unemployment rate data for June, due to release later in the day, will keep investors on their toes.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

A Potential Break Down Looms For The USDCHF

Key Points:

- Price action fails to breach trend line and turns negative.

- Key support level at 0.9585 nearing.

- Watch for a breakdown towards the 0.9550 mark in the coming week.

The USDCHF has been under some significant selling pressure of late as the pair continues to decline under the auspices of a bearish trend line. However, there has been some short term resurgence for the pair which saw a concerted move, which ultimately failed, back towards the falling trend line. Subsequently, the ill-fated, short term rally has set the wheels of a breakdown in motion that could yield some significant short side moves in the week ahead.

Fundamentally, there has been a significant swing around the greenback sentiment due to a range of confusing and mixed economic data emanating from the U.S. In particular, retail sales, consumer spending, and a lack of wage inflation appears to be clouding the current economic outlook for the U.S. and this is adding to slipping greenback sentiment. In addition, this is largely overshadowing some of the recent relatively poor data from Switzerland, including a slip in the monthly CPI figures.

In particular, a quick review of the major technical factors provides some illuminating hints as to what is coming for the embattled pair. Presently, the RSI Oscillator is demonstrating a definite downtrend but is yet to reach neutral territory which suggests that there is still room to move on the downside. Also, price action is currently well below the 100 hour moving average and there looks to be little prospect of an upside move towards that level any time soon.

Subsequently, the view is that the pair's recent decline from the 0.9688 mark towards support around the 0.9600 handle suggests that the longer term decline is not yet completed. The most likely scenario is then likely to be a challenge to support at 0.9585 before a sharp move towards our initial target of 0.9552, representing the recent low, and ultimately towards the 0.9500 handle.

Ultimately, the next week will likely be relatively critical for the pair with an impending breakdown and challenge to support at 0.9585. Subsequently, be on guard for a breach of this level because it will cause a fairly rapid Dollar depreciation.

The Silver Flash Crash: What Might Have Been At Work

Key Points:

- A flash crash has hit silver markets leaving many traders scratching their heads.

- Numerous explanations have been put forward, including the less reliable ones.

- Prices seem to have stabilised now.

Silver prices have been the subject of significant debate of the past few hours as a result of a flash crash that saw the metal plummet to the $14.27 handle before roaring higher within moments. Of course, this has brought out the usual speculations and accusations about exactly what was driving the movement so we have collected a few honourable mentions that might help to explain the crash.

Firstly, the classic 'fat finger' argument has been put forward by numerous analysts as a contributing factor to the tumble. To elaborate,a fat finger is when human input error generates a substantially erroneous trade – typically via an extra zero here or there. As entertaining as the notion is, such mistakes are typically safeguarded against by various fail safes. What’s more, a spike of this size in such a heavily followed market would almost certainly have been picked up prior to execution.

One slightly more plausible suggestion has been a sudden liquidity drain that sparked a bout of panic selling. Indeed, markets have been fairly thin over the 4th of July holiday period which could have compounded fears that silver was becoming illiquid in the wake of JP Morgan’s recent acquisitions. This being said, the extent to which JP Morgan has ‘rigged’ silver markets is constantly challenged and courts seem to be unable to agree on whether or not the institution is breaking antitrust legislation.

Stop loss orders have also been fingered as a cause for the sudden rout for all the usual reasons. Specifically, the hitting of numerous stop loss orders in rapid succession could have easily amplified the effects of a sell-off – even if they probably didn’t trigger the downtrend in the first place. Moreover, given that many traders may have been out of action due to the holiday’s in the US, it’s quite reasonable to expect more ‘set and forget’ trades to have been placed than is typical. This would have left the metal more exposed to this type of risk than we would usually expect.

Ultimately, there are many other potential explanations for what was hammering silver prices but we may never get to the bottom of it. These include, but are not limited to, algorithmic traders, glitches, stub quotes, and so on. Indeed, it was probably a mix of some, if not all, of the above. Nevertheless, it at least looks as though the metal has stabilised now and it could meander higher now that we are out of the woods. This should see the metal make a beeline for the $16 handle in the coming days, especially as political tensions from the G20 Summit begin to be felt.

Elliott Wave View: USDX Downside Resumes

Short term USDX (USD Index) Elliott Wave view suggests the rally to 97.88 high on 6/20 ended Intermediate wave (X). Decline from there is unfolding as an impulse Elliott Wave structure with extension and ended at 95.47 low on 6/29. This 5 wave move could be Minor wave A of an Elliott wave zigzag structure structure, where Minute wave ((i)) ended at 97.17 and Minute wave ((ii)) ended at 97.47. Minute wave ((iii)) ended at 96.15, Minute wave ((iv)) at 96.61 and Minute wave ((v)) of A ended at 95.47.

Revised view calls for Minor wave B bounce completed at 96.52. For this view, a break below Minor wave A at 95.47 will add more validity. Until then, a double correction in Minor wave B can’t be completely ruled out. The subdivision of Minor wave B is unfolding as an Elliott wave double three structure. Minute wave ((w)) ended at 96.24, Minute wave ((x)) ended at 96.04 and Minute wave ((y)) of B ended at 96.52. Near term, while bounces stay below Minor wave B at 96.52, expect the Index to resume lower. We don’t like buying the Index.

USDX 1 Hour Elliott Wave Chart