Sample Category Title

Trade Idea: USD/CAD – Sell at 1.3115

USD/CAD - 1.2948

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway with wave iii ended at 1.4690, wave v of C may bring one more marginal rise probably in 2018

Trend: Near term down

Original strategy :

Sell at 1.3115, Target: 1.2915, Stop: 1.3175

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.3115, Target: 1.2915, Stop: 1.3175

Position: -

Target: -

Stop:-

As the greenback has remained under pressure, suggesting recent selloff from 1.3794 top would resume after consolidation and although recovery to 1.3000, then 1.3015 cannot be ruled out, reckon upside would be limited to 1.3075-80 and 1.3115-20 should attract renewed selling interest, bring another decline later, below support at 1.2912 would extend the fall from 1.3794 top (wave c of larger degree wave b top) to 1.2895-00 but loss of momentum should limit downside to 1.2870 and reckon 1.2850 would hold from here.

In view of this, would not chase this fall here and would be prudent to sell the pair again on recovery as 1.3115-20 should limit upside. Above 1.3160-70 would defer and suggest low is formed, bring a stronger rebound to 1.3215-20 and possibly towards 1.3260-65 but only break there would abort and signal a temporary low is formed instead, then test of resistance at 1.3308 would follow.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

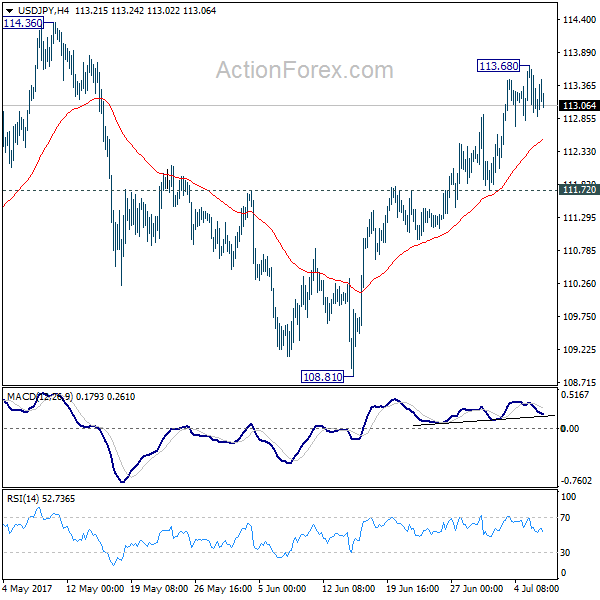

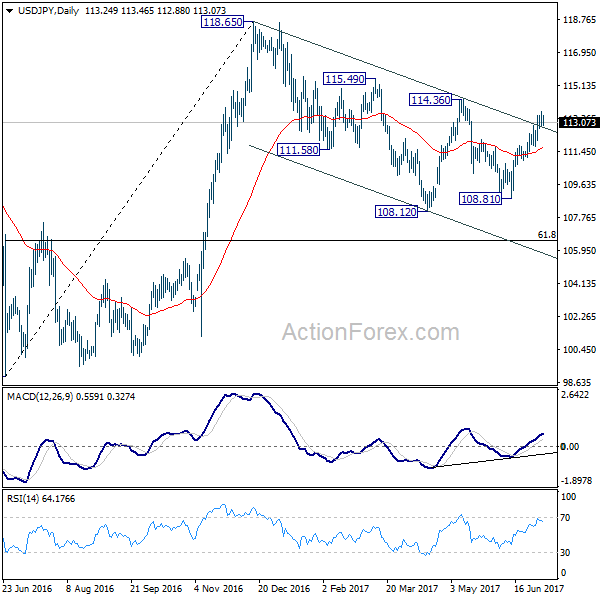

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.85; (P) 113.14; (R1) 113.57; More...

Intraday bias in USD/JPY remains neutral for consolidation below 113.68 temporary low. Downside of retreat should be contained by 111.72 support to bring another rally. Above 113.68 will target 114.36 resistance next. Decisive break there will confirm our bullish view that corrective pull back from 118.65 has completed at 108.12. In that case, further rally would be seen to retest 118.65.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

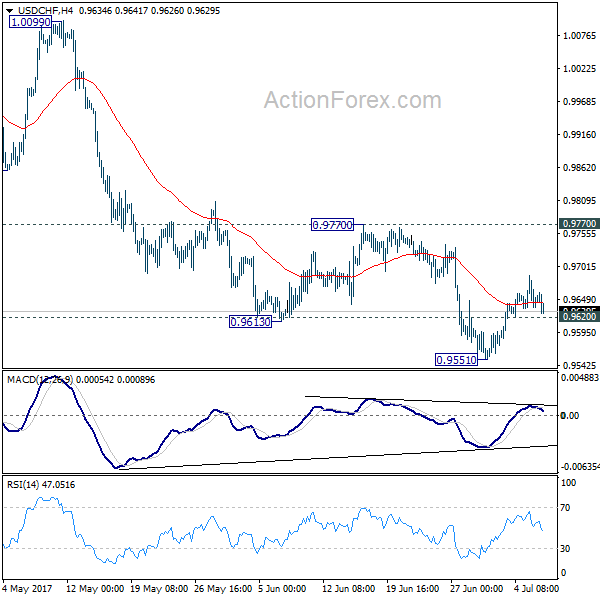

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9617; (P) 0.9652; (R1) 0.9675; More......

USD/CHF is still bounded in consolidation pattern from 0.9551 and intraday bias remains neutral for the moment. Outlook also stays bearish as long as 0.9777 resistance holds. Below 0.9620 minor support will turn bias back to the downside first. Further break of 0.9551 will extend the decline from 1.0342 to 0.94443 key support level. At this point, we'd expect strong support from there to bring rebound. Meanwhile, break of 0.9777 will now indicate short term reversal, on bullish convergence condition in 4 hour MACD.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

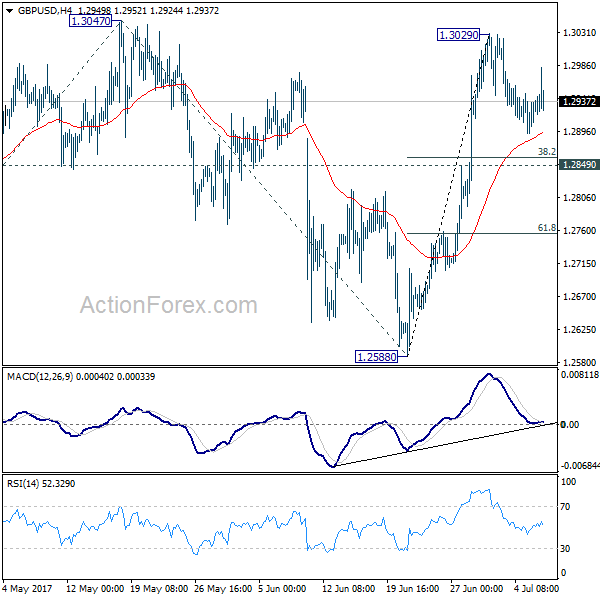

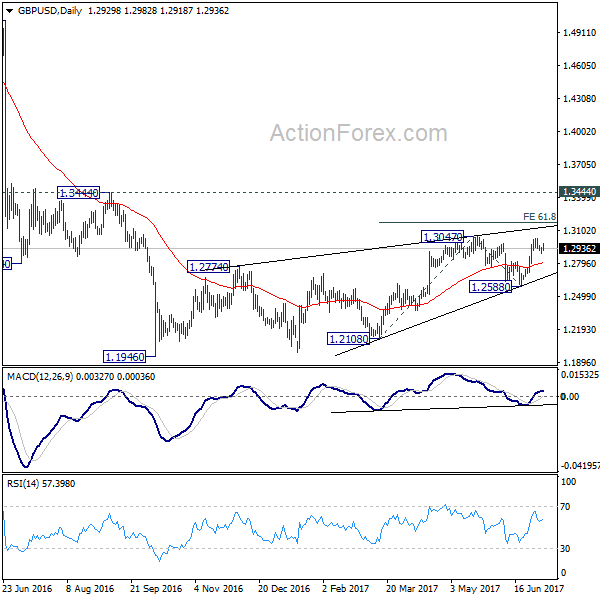

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2900; (P) 1.2924; (R1) 1.2955; More...

GBP/USD is still bounded in consolidation from 1.3029 and intraday bias stays neutral. Another fall cannot be ruled out. But downside should be contained above 1.2849 support to bring rise resumption. Break of 1.3029 should then send GBP/USD through 1.3047 to 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 next.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is now in favor, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

U.S. Trade Deficit Narrows in May

The U.S. international trade deficit narrowed in May by $1.1 billion (bn) to $46.5 bn from the April figure of $47.6 bn (revisions to April were negligible). Consensus expectation was for the trade balance to narrow a bit more to -$46.2 billion.

Goods exports rose 0.2% m/m in May, driven higher by a surge in consumer goods (+5.6%) and automotive vehicles and parts (+4.9%). Although there were large declines recorded in foods, feed and beverage exports (-6%), and smaller declines in capital goods and industrial supplies, they were not material enough to offset strong gains in consumer and automotive exports. Exports of services rose 1.0% m/m in the month, the fastest pace yet for 2017.

Imports declined 0.1%m/m in May, driven down by declines in consumer goods (-2.9%) and automotive vehicles and parts (-2.4%). These declines were largely offset by gains in capital goods (+2.4%) and industrial supplies (+0.2%).

Adjusting for price changes, merchandise exports rose 1.0% m/m in May, ending the streak of consecutive monthly declines at three. Import volumes rose 0.1% m/m, similar in magnitude but the opposite direction of the nominal change.

As the headline figure suggests, the U.S. trade balance with its major trading partners narrowed on net in May. The trade deficit with the European Union widened a touch in May, as did deficits with China and Mexico. However, given the monthly volatility of trade data, more telling is the year-to-date balance relative to last year. This metric suggests that trade deficits with NAFTA members Canada and Mexico have widened considerably thus far in 2017; the trade deficit with Canada has widened by $7.7 bn, and by $3.8 bn with Mexico. Similarly the trade deficit with Europe widened by $2.9 bn, and with China by $6.9 bn. Lastly, the trade deficit with OPEC nations widened by $15.3 bn YTD compared with last year, consistent with much stronger oil imports.

Key Implications

The gain in export volumes was a welcome surprise after months of decline, but net-trade is unlikely to be a major source of growth for the U.S. economy. The weaker trade-weighted dollar and improved foreign demand environment should act to support U.S. exporters for the remainder of this year, but strong domestic demand should boost imports further, resulting in net trade exerting a small drag on 2017 economic activity.

Looking ahead, the uncertain global environment could still exert a material headwind to U.S. exporters. From domestic and global policy uncertainty to geopolitical events, risks to net trade will remain skewed toward the downside for some time.

Canada’s Larger Trade Deficit in May Masks a Decent Month for Exporters

Highlights:

- Canada's merchandise trade deficit roughly doubled to $1.1 billion in May from $0.55 billion in April as a jump in imports more than offset higher exports.

- The 1.3% nominal increase in exports was fairly broad-based with 8 of 11 major subsectors posting gains.

- Special factors were also at play with an 11% jump in exports of metal and non-metallic mineral products attributed to a transfer of gold assets within the banking sector. That increase was offset by a price-driven drop in crude oil exports.

- Forestry product export volumes fell 5% in May following imposition of duties on Canadian softwood lumber in late-April.

- Nominal imports were up 2.4% in May with half of the increase coming from aircraft imports.

Our Take:

There is a lot of noise to filter through in today's trade report but we think the message on exports is ultimately positive. Non-energy export volumes, even excluding a transitory jump in gold exports, posted a solid increase in May and are now up relative to a year ago. A price-related decline in oil exports belies what has been a fairly strong increase in energy export volumes year-to-date. That supports the Bank of Canada's view that adjustment to lower oil prices is now largely complete. May's trade data is consistent with our expectation that net exports will add about 1 1/2 percentage points to GDP growth in Q2.

There are reasons to expect an upward trend in Canadian exports will continue. Global trade growth is picking up alongside stronger economic activity and other drivers such as US industrial production and business investment have improved year-to-date. Recent surveys from the Bank of Canada and Export Development Canada showed improving sentiment among exporters as strong orders make up for uncertainty regarding US trade policy. The Bank of Canada's latest view seems to be that, while uncertainty is clouding the outlook, monetary policy decisions can't be held off in the face of concerns that could linger for some time. As such, we don't see the threat of trade policy changes, including upcoming NAFTA renegotiation, preventing the bank from raising the overnight rate next Wednesday.

CAC Slips on Hawkish ECB Minutes

The CAC index is showing considerable losses in the Thursday session. Currently, the index is currently trading at 5132.50 and is down 0.93% on the day. On the release front, the ECB released its minutes from the June policy meeting. France's 10-year bond yield rose to 0.82% and Eurozone Retail PMI improved to 53.2, up from 52.0. On Friday, the US releases Nonfarm Payrolls, which is expected to improve to 175 thousand.

European stock markets are lower on Thursday, following the release of the ECB minutes. The minutes indicated that policymakers discussed removing its "easing bias" at the June meeting, but ultimately decided not to make a move, since stronger economic conditions had not resulted in higher inflation. ECB chief economist Peter Praet reiterated the bank's stance at a conference in Paris on Thursday. Praet noted that eurozone economic growth is accelerating, but said that the ECB still needs to provide a "steady hand" in order to spur stubbornly low inflation levels.

At the June meeting, the bank removed an easing bias regarding interest rates, effectively closing the door to further rate cuts. However, policymakers may now be wary about any more signals of tightening policy, to avoid another run on the euro, such as last week's "Draghi rally" during the ECB forum. The ECB meets for a policy meeting on July 20, and we could see a bland rate statement, to the effect that the economy is headed in the right direction, but QE will remain in place until inflation levels move higher. However, Draghi has surprised the markets before, so the meeting could prove to be a market-mover.

The dollar shrugged off the release of the Fed's June policy meeting, which failed to shed much light on the Fed's plans. The minutes revealed a divided Fed over the key issues of inflation and the Fed's bloated balance sheet. Some members expressed unease at the Fed's current forecast of rate hikes, given the persistently low levels of inflation. According to the current "dot plot", the Fed expects to raise rates in December, and three times in 2018. There was also division over the timing of reducing the $4.2 trillion balance sheet – some policymakers were in favor of starting in September, while others preferred later in the year. At the June meeting, the Fed stated that it would begin reducing the balance sheet this year, but provided no details. Analysts expect the Fed to start winding down the balance sheet in September, prior to a rate hike in December. The markets are lukewarm about a rate hike in December, with the odds at just 50%, according to the CME Group.

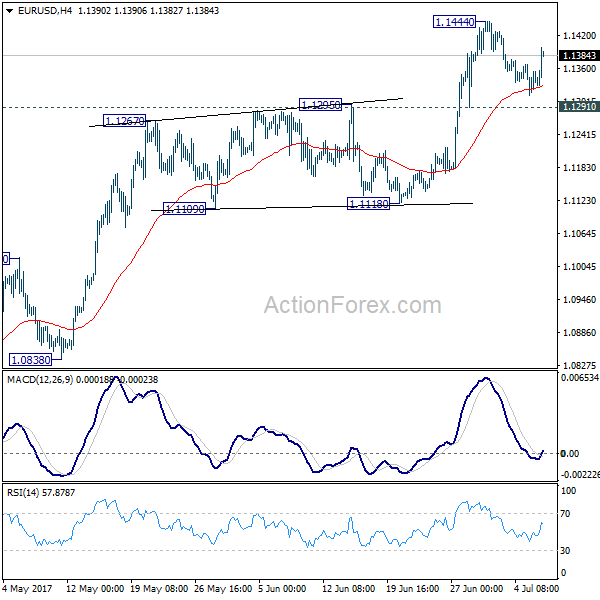

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1319; (P) 1.1344 (R1) 1.1375; More.....

EUR/USD rebounds strongly after drawing support from 4 hour 55 EMA. But it's staying in range below 1.1444 and intraday bias remains neutral first. In case of another fall, we'd expect downside to be contained by 1.1291 resistance turned support to bring rally resumption. Break of 1.1444 will extend the rise from 1.0339 low to 1.1615 resistance next. Meanwhile, break of 1.1291 will turn focus back to 1.1118 support.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1776). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

Dollar Under Pressure after ADP Employment Miss, Euro Jumps on Hawkish ECB Account

Dollar is under some pressure in early US session after disappointing job data. On the other hand, Euro surged broadly as market perceived the ECB monetary policy account as a hawkish one. US ADP employment report showed 158k growth in private sector jobs in June, below expectation of 180k. Prior month's figure was revised down to 230k, from 253k. Initial jobless claims rose 4k to 248k in the week ended July 1, versus consensus of 243k. The number, nonetheless, remain historically low and stayed below 300k handle for the 122 straight weeks. Continuing claims rose 11k to 1.96m in the week ended June 24, staying below 2m for 12 straight weeks. Also released in early US session, US trade deficit narrowed to USD -46.5b in May. Canada trade deficit widened to CAD -1.1b in May. Canada building permits rose 8.9% mom in May.

Quick update: Dollar stays soft despite upside surprise in ISM services

FOMC minutes for June meeting released yesterday showed that policy makers were divided over the timing of balance sheet reduction while there was also discussion over the recent inflation weakness."Several participants indicated that the reduction in policy accommodation arising from the commencement of balance sheet normalization was one basis for believing that, if economic conditions evolved broadly as anticipated, the target range for the federal funds rate would follow a less steep path than it otherwise would". Yet, "some other participants suggested that they did not see the balance sheet normalization program as a factor likely to figure heavily in decisions about the target range for the federal funds rate". More in FOMC Members Divided over Balance Sheet Reduction Schedule.

ECB considered dropping pledge of expanding QE

ECB's monetary policy accounts showed that during the meeting on June 7-8, policy makers discussed dropping the pledge to expand its quantitative easing program if necessary as "the economic expansion proceeded and if confidence in the inflation outlook improved further." And, "gradual adjustments in the governing council's communication...would be in line with the evolving risk assessment." But for the moment, "there was broad agreement among members that the current monetary policy stance remained appropriate" given the subdued inflation.

ECB chief economist Peter Praet repeated his urge that the central bank needs "patience and persistence" as "our mission is not yet accomplished." Praet acknowledged broadening economy recovery but underlying inflation remained too low. And he emphasized that "maintaining a steady hand continues to be critical to fostering a durable convergence of inflation toward our monetary policy aim."

Released in Europe today, Eurozone retail PMI rose to 53.2 in June. German factory orders rose 1.0% mom in May. Swiss CPI slowed deeply to 0.2% yoy in June, down from 0.5% yoy.

Australia trade surplus widened

From Australia, trade surplus widened to AUD 2.47b in May, up from AUD 0.09b and beat expectation of AUD 1.11b. That was driven by the 9% growth in exports over the month while imports rose 1%. However, it should be noted that coal exports jumped 62% over the month, for supply was disrupted back in April after Queensland was hit by cyclone in late March. Aussie remains the weakest major currency for the week as markets were dissatisfied that RBA didn't turn hawkish, following other major central banks.

IMF Lagarde: Financial vulnerabilities present an immediate concern

IMF Managing Director Christine Lagarde warned in a blog post that "financial vulnerabilities present an immediate concern." And, "after a long period of favorable financial conditions, including low-interest rates and easier access to credit, corporate leverage in many emerging economies is too high." In Europe, she noted that "bank balance sheets still need repair following the crisis." In China, "a faster-than-projected expansion - if it continues to be fueled by rapid credit and increased spending - would potentially lead to unsustainable public and private debt in the future".

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1319; (P) 1.1344 (R1) 1.1375; More.....

EUR/USD rebounds strongly after drawing support from 4 hour 55 EMA. But it's staying in range below 1.1444 and intraday bias remains neutral first. In case of another fall, we'd expect downside to be contained by 1.1291 resistance turned support to bring rally resumption. Break of 1.1444 will extend the rise from 1.0339 low to 1.1615 resistance next. Meanwhile, break of 1.1291 will turn focus back to 1.1118 support.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1776). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) May | 2.47B | 1.11B | 0.56B | 0.09B |

| 06:00 | EUR | German Factory Orders M/M May | 1.00% | 1.80% | -2.10% | -2.20% |

| 07:15 | CHF | CPI M/M Jun | -0.10% | 0.00% | 0.20% | |

| 07:15 | CHF | CPI Y/Y Jun | 0.20% | 0.30% | 0.50% | |

| 08:10 | EUR | Eurozone Retail PMI Jun | 53.2 | 52 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Jun | -19.30% | 9.70% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:15 | USD | ADP Employment Change Jun | 158K | 180K | 253K | 230K |

| 12:30 | CAD | Building Permits M/M May | 8.90% | 2.60% | -0.20% | |

| 12:30 | CAD | International Merchandise Trade (CAD) May | -1.1B | -0.5B | -0.4B | |

| 12:30 | USD | Trade Balance May | -46.5B | -46.3B | -47.6B | |

| 12:30 | USD | Initial Jobless Claims (JUL 01) | 248K | 243K | 244K | |

| 14:00 | USD | ISM Services/Non-Manufacturing Composite Jun | 57.4 | 56.5 | 56.9 | |

| 15:00 | USD | Crude Oil Inventories | 0.1M |

Trade Idea Update: USD/CHF – Buy at 0.9600

USD/CHF - 0.9635

Original strategy :

Buy at 0.9600, Target: 0.9700, Stop: 0.9565

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9600, Target: 0.9700, Stop: 0.9565

Position : -

Target : -

Stop : -

As the greenback retreated after rising to 0.9688, suggesting consolidation below this level would be seen and pullback to 0.9621 support cannot be ruled out, however, if our view that low has been formed at 0.9552 is correct, downside would be limited to 0.9600 and bring another rebound later, above said resistance would extend the rise from 0.9552 low for retracement of recent decline to 0.9700 but reckon upside would be limited and price should falter below resistance area at 0.9738-43.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback as 0.9600 should limit downside and bring another rise later. Below 0.9565-70 would abort and signal intra-day top is formed, risk retest of 0.9552 first.