Sample Category Title

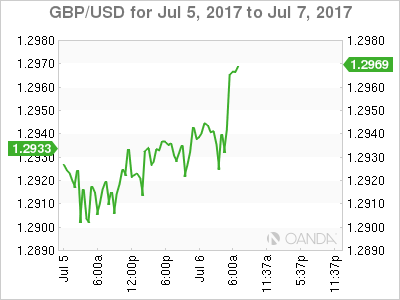

Trade Idea Update: GBP/USD – Buy at 1.2865

GBP/USD - 1.2950

Original strategy :

Buy at 1.2865, Target: 1.3000, Stop: 1.2830

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2865, Target: 1.3000, Stop: 1.2830

Position : -

Target : -

Stop : -

Although the British pound has recovered after falling to 1.2893, reckon upside would be limited to 1.2980-85 and near term downside risk remains for the corrective fall from 1.3030 (last week’s high) to bring retracement of recent upmove to 1.2880-85 (38.2% Fibonacci retracement of 1.2640-1.3030), however, downside should be limited to 1.2865-70 and bring another upmove later, above 1.2980-85 would signal low is formed, bring rebound to 1.3000 but break of said resistance at 1.3030 is needed to signal recent upmove has resumed and extend further gain towards recent high 1.3048.

In view of this, we are looking to buy cable again on further corrective fall as previous resistance at 1.2861 should turn into support and contain downside, bring another rise. Below 1.2830-35 (50% Fibonacci retracement of 1.2640-1.3030) would abort and signal top is formed, bring further fall towards support at 1.2794.

USDCAD Forecast and BOC Meeting Next Week

Bank of Canada will have a meeting on July 12 to decide the interest rate. USDCAD has declined due to recent comments made by top Bank of Canada officials which seem to suggest that interest rates could be raised soon. The market in fact is pricing in an 82 percent chance of a rate hike next week. In a CNBC interview last week, Bank of Canada Governor Stephen Poloz said that the two interest rate cuts by Bank of Canada in 2015 have done their jobs in shielding Canadian economy from the steep fall in the price of oil. He also added that the central bank needs to consider its options as excess capacity in the economy is used up.

Mr. Poloz reiterated his hawkish stance in a recent interview with German newspaper Handelsblatt. He said that monetary policymakers must "anticipate where the economy will be 18 or 24 months from now". He also said inflation in Canada should be well into an uptrend by the first half of 2018. Thus normalization must begin before the price growth hits its target.

The Canadian dollar strengthened against the U.S dollar on Tuesday after his comments. The loonie touched its strongest intraday level in nine months at 1.2908. The strength in loonie is not only based on rate hike expectation alone. Recent economic data also shows Canada's economy grew for sixth consecutive month in April. Meanwhile, business sentiment suggest companies feel more optimistic. Prices of oil, one of Canada's major exports, also started to recover. This further adds support for the Canadian dollar.

Data from CFTC (U.S Commodity Futures Trading Commission) shows a record pace of short covering in the Canadian dollar for a fifth straight week. The June 27 COT (Commitment of Traders) report below shows non commercial's net short positions in Canadian dollar dropped to 49,495 contracts from 82,881 a week earlier. With the net short position remains elevated at 50K, CAD remains vulnerable to short squeeze and position adjustment.

USDCAD Long Term Analysis

Daily USDCAD chart above shows pair declined sharply after reaching the peak on January 20, 2016. Pair declined from 1.4693 to 1.2461 (approximately 2200 pips) within a span of less than 4 months. The decline finally bottomed on May 3, 2016. The pair then took 1 year time from May 3, 2016 to May 5, 2017 to correct the decline in overlapping fashion, characteristic of a correction. This correction looks to be forming a bearish flag and recently pair has broken below the channel which may suggest that the correction is complete on May 5, 2017. A break below May 3, 2016 low (1.2461) will give the final confirmation that pair has started the next leg lower.

USDCAD 4 hour Elliott Wave Sequence Chart

USDCAD 4 Hour chart above shows a 5 swing bearish sequence from May 4, 2017 high. Please note that this is not the same as 5 waves impulse, but rather the number of swing count. The 5 swing sequence suggests that while the sixth swing bounce fails below swing #4 high at 1.3328, more downside can be seen in the pair.

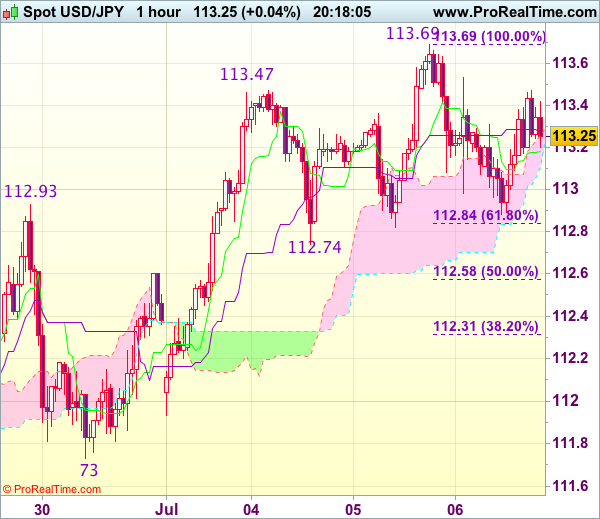

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 113.26

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback resumed recent rise and rose to as high as 113.69 yesterday, lack of follow through buying and the subsequent retreat suggest consolidation below this level would be seen and weakness to 112.80-85 (38.2% Fibonacci retracement of 111.46-113.69) is likely, however, break of support at 112.74 is needed to signal top has been formed there, bring retracement of recent rise to 112.40-45, then 112.20 but reckon 111.95-00 would hold from here.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Above said resistance at 113.69 would signal recent upmove is still in progress and may extend further gain to 114.00 but loss of momentum should prevent sharp move beyond 114.25-30.

Dollar Pressured ahead of ADP NFP Report

Financial markets offered a muted response towards June's hawkish FOMC meeting minutes, with the Dollar rally easing as investors re-evaluated the mixed messages that policy makers dished out. It was interesting how the minutes illustrated a visible divide between officials over the timings of the balance sheet reduction, with an increasing split on the outlook for inflation compounding to the confusion. While Fed hawks felt that the economy could handle higher interest rates and that this period of low inflation in the States was 'transitory', doves expressed concerns over the recent softness in inflation continuing. There were also discussions over the uncertainty regarding the possible implementation and changes to fiscal and other government policies.

All in all, Dollar bullish investors who were seeking some form of inspiration and further clarity from June's FOMC meeting minutes, were left empty handed and this was reflected in price action. Will the Federal Reserve have the ability to reduce their balance sheet and increase interest rates this year? Time will tell as such may depend on whether economic data from the States stabilizes, with this period of softness proving to be 'transitory'.

Speaking of economic data, investors may direct their attention to the influx of releases from the States today, which could support or deflate rate hike expectations. The ADP Non-Farm payroll will be the first course, followed by unemployment claims and topped up with the ISM Non-Manufacturing PMI report. In this period, where markets need more conviction over the Federal Reserve moving forward, with raising US interest rates and unwinding its balance sheet, economic data is likely to be closely scrutinized.

From a technical standpoint, the Dollar Index remains under pressure on the daily charts. A breakdown below 96.00 may encourage a further depreciation lower towards 95.50.

ECB meeting minutes in focus

The main risk event for the Euro during Thursday's trading session, will be the release of June's ECB meeting minutes which investors may deeply analyze for any discussions of a possible QE exit strategy. Although the Euro could find itself pressured if the minutes strike a dovish tone and emphasize the tepid inflation levels, the downside could be limited as markets digest this as old news.

It should be kept in mind that there has been a multitude of comments from various ECB members since June's meeting, with the recent upbeat remarks on the Eurozone economy from Draghi last week supporting the Euro. The EURUSD remains bullish on the daily charts as there have been consistently higher highs and higher lows. The formation of a new higher low above 1.1300 may open a path back towards 1.1450.

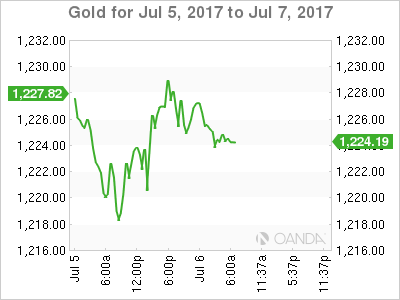

Gold in a tight spot

Gold prices appreciated during Wednesday's trading session, after June's hawkish FOMC meeting minutes failed to support the Greenback and even created a sense of confusion. The mixed thoughts on inflation and the divide over the timings of the balance sheet reductions raised questions on the central bank's ability to move forward with actually raising rates. Heightening tensions surrounding North Korea have also supported the flight to safety, with Gold trading around $1225 at the time of writing. While uncertainty in the longer term has the ability to ensure the yellow metal remains buoyant, bulls are fighting against the tide in the short term. Gold remains vulnerable to further downside as long as prices remain below $1240. Weakness below $1220 may open a path towards $1214.

Commodity spotlight – WTI Crude

WTI Crude edged higher during early trading on Thursday, after API data showed an unexpected decline in US crude inventories which encouraged investors to profit-take. With the unyielding oversupply dynamics weighing heavily on the minds of investors and it becoming clearer that OPEC no longer has the overwhelming say over the industry, oversupply will continue to be the name of the game when it comes to oil. This also means that the valiant efforts being made by OPEC to regain market share, are at threat of being offset from producers outside of their agreement pact. Investors may direct their attention towards the pending weekly oil inventory report from the EIA, which could pressure WTI further if there is a build.

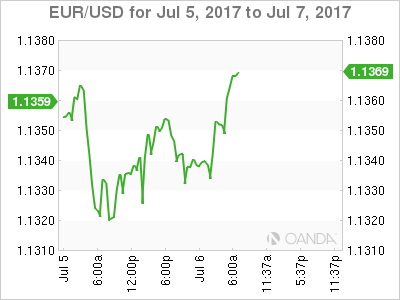

Trade Idea Update: EUR/USD – Buy at 1.1355

EUR/USD - 1.1381

Original strategy :

Buy at 1.1290, Target: 1.1390, Stop: 1.1255

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1355, Target: 1.1455, Stop: 1.1320

Position : -

Target : -

Stop : -

Current rebound suggests low has been formed at 1.1312 yesterday and consolidation with upside bias is seen for gain to 1.1400-10, however, break there is needed to signal the pullback from 1.1446 (last week’s high) has ended and bring subsequent retest of this level, break there would confirm recent upmove has resumed for headway to 1.1475-80 but price should falter below 1.1500.

In view of this, we are looking to buy euro on dips but one should exit on subsequent rally. Below 1.1325-30 would abort and signal an intra-day top is formed, risk test of said support at 1.1312, then 1.1292 (previous support as well as 50% Fibonacci retracement of 1.1139-1.1446).

US Data Eyed Ahead of Friday’s Jobs Report

As we enter the business end of the week, the US will be in focus with a large number of data scheduled to be released including some important labour market numbers and surveys on the services sector.

ADP, PMIs and Fed Speakers Scheduled for Thursday

The Independence Day bank holiday earlier in the week caused a delay in a number of figures being released. It means that ahead of tomorrow's jobs report, we'll get the ADP release for June which is expected to show 185,000 jobs being created, roughly in line with the NFP 12-month average. This would suggest the labour market is continuing to tighten, giving further ammunition to the hawks on the Fed that argue that inflation will ramp up.

We'll also get the final services PMI number for June, alongside the composite PMI and the ISM non-manufacturing PMI. The services sector is hugely important to the US economy and both of these numbers continue to point to decent, albeit uninspiring, levels of growth. Jobless claims and trade balance numbers will also be released alongside these figures. We'll also hear from three Federal Reserve policy makers, with vice Chair Stanley Fischer, Jerome Powell and John Williams all scheduled to appear.

USD Edges Lower After FOMC Minutes

The dollar is trading a little lower on the day as the US open approaches. The minutes from the last FOMC meeting did little to support the greenback, with the lack of inflationary pressures appearing to be taking its toll on the appetite for more rate hikes, among some policy makers. That suggests to me that, while one more rate hike may come this year - perhaps in December - the pace beyond then may slow, with the focus then turning to the balance sheet. Of course, should inflation move towards 2%, as remains the assumption of the committee, the pace of tightening may increase with it.

Oil Higher as API Reports Large Drawdown

Oil is up more than 1% on the day so far, paring Wednesday's losses which came on reports that Russia is not willing to deepen the production cuts that could be necessary to bring the market back into balance and support prices. The rebound off the lows was aided by the inventory data from API which reported a substantial drawdown last week of 5.76 million barrels. Prices may be further supported today if this number is confirmed by EIA, with only around half that currently expected.

Dollar Steady After FOMC Minutes Leave A Hawkish Message Amid Signs Of Split

Late on Wednesday, the Federal Reserve (Fed) published the minutes of its meeting held in June 13-14, providing the reasoning behind its decision to raise the fed funds rate for the second time this year to a target range of 1.00-1.25% and its intention to reduce the size of the balance sheet. However, the release of the minutes did not provide a strong support to the dollar, with major currency pairs remaining flat in the forex markets.

The Fed minutes revealed that bank officials are in a hawkish mood as several policymakers in June’s meeting were positive and, therefore, agreed to unwind the stimulus monetary programme within months. The decision came after the Committee judged that current economic conditions give an incentive to tighten monetary policy further, while they also projected that future economic developments will warrant gradual rate hikes.

Regarding the present economic progress, the members said that the labour market is stronger as unemployment rate fell to 4.3% in May and was below the longer-run target, despite disappointing wage growth and slower employment growth. The latter, they explained, was attributed, as expected, to a narrowing labour capacity. Moreover, inflation over the last 12 months rose slightly but remained below the 2% target according to the core PCE price index, which was 1.5% in April. Household spending together with fixed investment continued growing in recent months as well.

In the medium-term, the members anticipate that economic activity will increase moderately and the labour market will strengthen further, whereas inflation is expected to stabilize around 2%. Nevertheless, Fed officials claimed that uncertainty around fiscal policies remain significant as they are likely to adjust, but short-term risks are considered balanced as risks arising from foreign economic developments are less severe now.

Taking the above into account, most of the Fed policymakers decided to raise rates gradually and shrink the balance sheet despite weak inflation. However, a disagreement was found regarding the timing the Fed will start reducing its asset holdings. Some members wanted to initiate the process within months – favouring the upcoming July meeting or August – whereas others preferred to wait longer and assess economic conditions first before taking any action.

There was also a split regarding the pace of future rate increases, with some Committee members voicing concern about the downside risks to inflation, while other participants saw a bigger risk from the low unemployment level that could potentially lead to the economy overheating.

In terms of reaction in the forex markets, dollar pairs showed little response to the Fed’s minutes. The dollar index, which gauges the dollar strength against its major counterparts, moved sideways, last trading at 95.93. Dollar/yen reversed its overnight losses before steadying at 113.41 in early European trading today. Euro/dollar was also steady at $1.1362, while the pound/dollar stood at $1.2940.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD had another indecisive movement yesterday. Price attempted to push lower, bottomed at 1.1312 but closed a little bit higher at 1.1350. The bias is neutral in nearest term probably with a little bullish bias testing 1.1425 resistance area. A clear break and daily close above that area would continue the bullish scenario targeting 1.1500 – 1.1530 region. Immediate support is seen around 1.1285. A clear break and daily close below that area could trigger further bearish pressure testing 1.1180 region but overall I remains bullish and any downside pullback should be seen as a good opportunity to buy. Fundamental focus will be on the US NFP number tomorrow.

GBPUSD

The GBPUSD had another indecisive movement yesterday. The bias is neutral in nearest term probably with a little bullish bias testing 1.3000 region but key resistance remains at 1.3050 which remains a good place to sell with a tight stop loss. Immediate support is seen around 1.2890/75. A clear break below that area could trigger further bearish pressure testing 1.2815/00 region. On the upside, a clear break and daily close above 1.3050 would activate my bullish mode. Fundamental focus will be on the US NFP number tomorrow.

USDJPY

The USDJPY was indecisive yesterday formed a Doji on daily chart. There are no changes in my technical outlook. The bias remains bullish in nearest term testing 114.30 resistance area. Immediate support remains around 112.75/60 area. A clear break below that area could lead price to neutral zone in nearest term testing 112.00 region or lower but overall I remain bullish and any downside pullback should be seen as a good opportunity to buy. On the upside, a clear break and daily close above 114.30 would expose 115.50 region. Fundamental focus will be on the US NFP number tomorrow.

USDCHF

The USDCHF attempted to push higher yesterday, slipped above 0.9675 resistance but closed lower at 0.9640, formed a bearish pin bar as you can see on my daily chart below. This fact could end the bullish correction phase but note that 0.9550 – 0.9450 area remains a key support and good place to buy with a tight stop loss below 0.9450. Immediate resistance is seen around 0.9688 (yesterday’s high). A clear break above that area would expose 0.9765 region. Fundamental focus will be on the US NFP number tomorrow.

DAX Loses Ground As German Manufacturing Report Misses Expectations

The DAX index has dropped in the Thursday session, as the index is down 0.74%. Currently, the DAX is at 12,361.50. On the release front, German Factory Orders gained 1.0%, well short of the forecast of 1.9%. Eurozone Retail PMI improved to 53.2, up from 52.0. Today's highlight is the minutes from the ECB's policy meeting in June.

The German manufacturing sector continues to expand, as stronger global demand for German products has boosted the manufacturing and exports sector. Earlier in the week, German Manufacturing PMI came in at 59.6, pointing to expansion. Factory Orders were up 1.0% in May, rebounding after a sharp decline of 2.1% in April. We'll get a look at Industrial Production on Friday, which is expected to show a weak gain of o.2%.

All eyes will be on the ECB later on Thursday, with the release of the minutes from the July policy meeting. Investors will be monitoring closely, looking for hints that the ECB is moving close to exiting the QE scheme. There was plenty of excitement last week, as the “Draghi rally” saw the euro soar by 2.0%. Draghi spoke at the ECB forum, a gathering of central bankers. His upbeat comments about growth and inflation in the eurozone economy triggered a rush to buy euros, much to the surprise of the ECB. In June, the bank removed an easing bias regarding interest rates, effectively closing the door to further rate cuts. However, policymakers may now be wary about any more signals of tightening policy, to avoid another run on the euro. The ECB meets for a policy meeting on July 20, and we could see a bland rate statement, to the effect that the economy is headed in the right direction, but QE will remain in place until inflation levels move higher. However, Draghi has surprised the markets before, so the meeting could prove to be a market-mover.

The dollar shrugged off the release of the Fed's June policy meeting, which failed to shed much light on the Fed's plans. The minutes revealed a divided Fed over the key issues of inflation and the Fed's bloated balance sheet. Some members expressed unease at the Fed's current forecast of rate hikes, given the persistently low levels of inflation. According to the current “dot plot”, the Fed expects to raise rates in December, and three times in 2018. There was also division over the timing of reducing the $4.2 trillion balance sheet – some policymakers were in favor of starting in September, while others preferred later in the year. At the June meeting, the Fed stated that it would begin reducing the balance sheet this year, but provided no details. Analysts expect the Fed to start winding down the balance sheet in September, prior to a rate hike in December. The markets are lukewarm about a rate hike in December, with the odds at just 50%, according to the CME Group.

ECB Minutes Key For Next EUR Move

Yesterday's Fed minutes has done little to aid dealers in mapping out their U.S yield cure. It's tomorrow's U.S jobs report (08:30 am EST), including a wage inflation reading, which is the key data point for capital markets this week to effect market expectations on the Fed's policy outlook.

At their meeting last month, Fed officials debated when to start shrinking the central bank's balance sheet, according to meeting minutes released yesterday, with some favoring starting “within a couple of months” and others suggesting it would be better to wait. The main sticking point was uncertainty over whether the recent drop in inflation is temporary, or a real problem.

The Fed's lack of consensus has global equities trading mixed, yen giving up some of its recent gains and ‘big' dollar little changed.

Similarly, the European Central Bank's (ECB) account of their June 8 monetary policy meeting (07:30 am EST) will be watched for any discussion on the decision to drop the reference to future interest rate cuts – by removing the words “or lower” from their introductory statement. Dealers will also be looking for clues on “tapering.”

To date, many expect the ECB to make some kind of announcement regarding tapering of bond buying at the September or October monetary policy meeting, with a reduction in monthly purchases starting in January.

Note: Friday's non-farm payroll (NFP) report is expected to add around +175k workers last month and wage growth probably strengthened.

1. Stocks show a mixed reaction to FOMC minutes

In Japan, the Nikkei (-0.4%) dropped to three-week lows overnight as ongoing tensions around North Korea continued to sap risk appetite. The broader Topix dropped -0.2%.

In Singapore, the Straits Times Index declined -0.5% while Indonesia's benchmark gauge climbed +0.3% and India's Sensex advanced +0.5%.

In Hong Kong, the Hang Seng Index fell -0.2%, while the Hang Seng China Enterprises Index retreated -0.4%.

In China, the Shanghai Composite Index increased +0.2%.

In Europe, regional bourses had opened mixed, but are now drifting lower. With crude oil moving higher it's providing some support to energy stocks on the FTSE 100, while materials stocks are under pressure following drop in precious metals. Markets attention has switched to the ECB minutes and tomorrow's non-farm payroll (NFP) report.

Indices: Stoxx50 -0.5% at 3,462, FTSE -0.5% at 7,358, DAX -0.3% at 12,418, CAC-40 -0.5% at 5,154, IBEX-35 -0.7% at 10,453, FTSE MIB -0.5% at 21,042, SMI -0.5% at 8,913, S&P futures -0.1%.

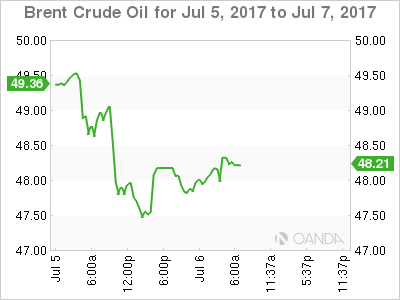

2. Oil rallies after U.S inventory drop, gold prices steady

Ahead of the U.S open, crude oil is trading better bid, recovering some ground after a surprisingly upbeat picture of U.S demand.

However, the prospect of oversupply in 2018 continues to provide a headwind, which is causing many analysts to cut next year's price forecasts.

Brent crude futures are up +71c at +$48.50 a barrel. The price fell as much as -4.6% intraday yesterday, before closing down -3.7%, its biggest one-day drop in a month. U.S West Texas Intermediate (WTI) crude futures are also up +71c, at +$45.84 a barrel.

Yesterday after the close, API data showed U.S. crude inventories fell more sharply than expected, down -5.8m barrels in the week to June 30, against expectations for a draw of -2.3m barrels.

Note: OECD total oil inventories are still above +3B barrels and the recovery in Libyan and Nigerian supplies, coupled with a return of U.S shale, is expected to prevent steep stock draws ahead.

For now, rising geopolitical risks is providing some support for gold. The precious metal is little changed (-0.1% to +$1,223.97 an ounce) overnight as tensions on the Korean peninsula stoked safe-haven demand for the metal. Nevertheless, the dollars strength is expected to provide weight for some metal prices.

3. European Bond auctions back up yield

Heavy government bond supply from the U.K, Spain and France is putting some downward price pressure on the bond prices ahead of the U.S open.

Note: Today's supply is tilted to the long- end of both the Spanish and French yield curves. Spain is offering €5B in 2022-, 2040- and 2046-dated, while France auctions €8.5B May 2027-, October 2027- and May 2048-dated OATs. While in the U.K, £2.5B 10-Gilts is on offer (+1.25% 2027).

The collective Euro supply has U.S 10's backing up +3 bps to +2.35%, after falling -3 bps points yesterday and Gilts, OAT's and Bunds climbing +2 bps.

Elsewhere, down-under, Australia's benchmark yield has gained +1 bps to +2.64%. The Reserve Bank of Australia's (RBA) Harper said that Aussie policy makers are “comfortable holding interest rates for now and see no reason to scare the horses at the moment” by signaling coming interest rate increases.

4. Dollar's mixed fortunes

Sterling is marginally higher outright (£1.2935), but continues to trade in “no man's land.”

Some of the pounds gains in the past weeks have been on the back of expectations that the BoE may raise interest rates given higher-than-expected inflation. Sterling bears are hoping that the “lower highs and lower lows” is putting the currency pair at risk of a steeper decline towards £1.28 again.

Note: GBP/USD rallied well above £1.30 after Carney spoke last week, but has since failed to hold above this key level.

The EUR (€1.1362) is steady outright after booking gains in the week on upward revisions to German manufacturing and service sector activity, similar changes to the broader eurozone purchasing managers' indices, and a rebound in retail sales (see below). Market is waiting for the ECB minutes for conviction on the single units next move.

Note: The reduction in the ECB's bond-buying program is not fully priced in yet by the markets.

5. Eurozone sales rise to greatest extent in almost two years

Data this morning showed that Eurozone retailers recorded an uptick in sales during June (53.2 vs. 52 m/m).

Growth was driven by sharp expansions in France (74-month high) and Germany, although another decline in Italy continued weigh on overall growth.

Digging deeper, there was a broad-based drop in ‘gross margins' for retails, which suggests a continued challenging business climate, while a strong increase in employment provides stronger evidence of a recovery in the eurozone retail sector.