Sample Category Title

EUR/JPY Daily Outlook

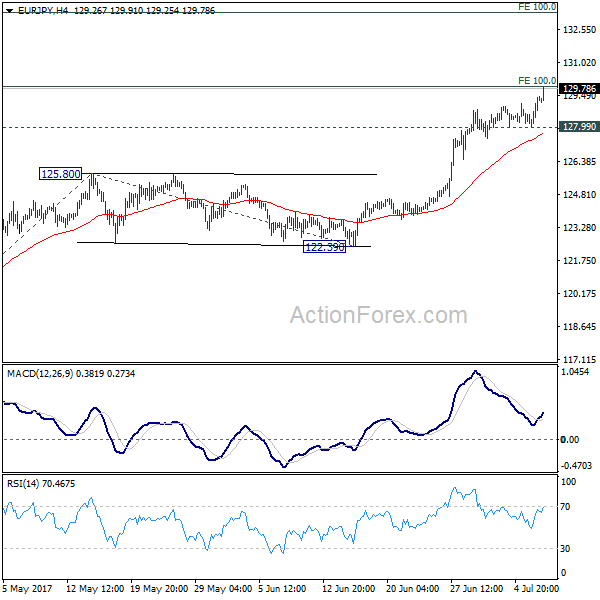

Daily Pivots: (S1) 128.40; (P) 128.90; (R1) 129.82; More...

EUR/JPY's rally extends and reaches as high as 129.91 and there is no sign of topping yet. Firm break of medium term projection level at 128.89 will pave the way to next near term projection level at 100% projection of 114.84 to 125.80 from 122.39 at 133.35. On the downside, break of 127.99 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

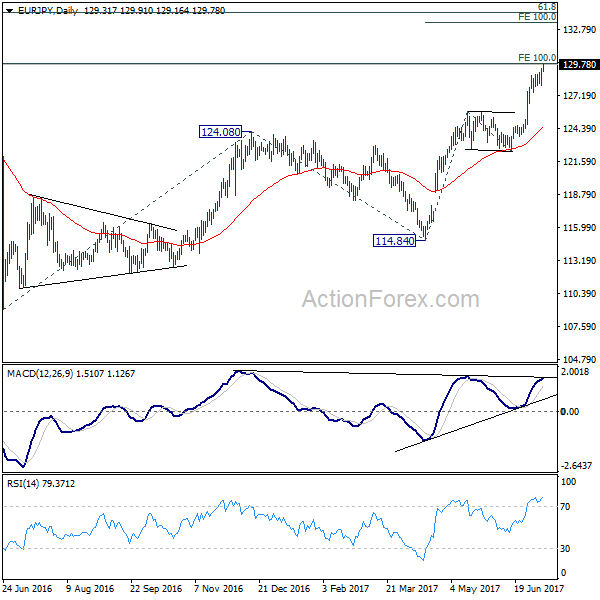

In the bigger picture, the break of 126.09 support turned resistance should have confirmed completion of down trend form 149.76 (2014 high), at 109.03 (2016 low). Current rise from 109.03 has already met target of 100% projection of 109.03 to 124.08 from 114.84 at 129.89. Sustained break there will pave the way to 61.8% retracement of 149.76 to 109.03 at 134.20 and above. Medium term outlook will now remain bullish as long as 122.39 support holds.

BoJ Announced Emergency Bond Buying as Global Yields Surges, USD/JPY Strengthens ahead of NFP

Yen tumbles broadly as global bond rout continued and pushed yields higher again. German 10 year bund yields broke 0.5% level for the first time since January 2016. Meanwhile, US 10 year yield jumped to a near two month high and closed firmly at 2.37, up 0.036. The resumed selling in bonds were believed to be triggered by the hawkish ECB minutes which indicated the discussion of removing easing bias. Also, some believed that weak results of French 30 year bond-auction was another trigger. UD/JPY reaches as high as 113.83 as recent rise resumed. GBP/JPY also hits as high as 147.60. Meanwhile, EUR/JPY is even stronger and hits 129.91, set to take on 130 handle.

In response to the developments, BoJ announced to carry out an emergency fixed-rate bond buying operation to curb long term yields under the so called "Yield Curve Control" framework. The central bank said it will buy unlimited amount of JGB with maturities of 5 to 10 years. This is the third time BoJ carries out such operations since the announcement of YCC last year. The first offer in November drew no bids. Under the second operation in February, JPY 723.9b in bonds were purchased.

Yen follows yield, not stocks

We've pointed out before that Yen is decoupling from risk aversion and its now more correlated to yields. This is clearly seen again as global equities tumbled overnight. DOW lost -158.13 pts, or -0.74% to 21320.04. S&P 500 dropped -22.79 pts, or -0.94% to 2409.75. NASDAQ closed down -61.40 pts, or -1.0% at 6089.46. NASDAQ stays the more vulnerable one as last week's low was breached. Weakness carries on in Asia with Nikkei trading down -0.3% and broke 20000 handle at the time of writing. FTSE and DAX might set to take on last week's low at 7302.7 and 12319 respectively.

Euro boosted by hawkish ECB accounts

For the week so far, Euro is the second strongest major currency, behind Dollar by a thin margin. And yesterday's rebound in EUR/USD could actually be setting up for a break through 1.1444 resistance today. The minutes for the June ECB meeting turned out more hawkish than expected. The minutes unveiled that policymakers had discussed removing the guidance on the bond asset purchase program (QE), if necessary. Policymakers just shrugged off recent weakness in headline inflation as core inflation continued to climb higher. This came in line with President Mario Draghi's comments last week that "deflationary forces have been replaced by reflationary ones", pointing to a "strengthening and broadening recovery" in the Eurozone. More in June's Minutes Revealed ECB Discussed over Removing Asset Purchases Guidance, Euro Soars

NFP expectations setting up for downside surprise

Non-farm payroll report from US will be the main focus today. Economists expect 173k growth in the job market in June, with unemployment rate unchanged at 4.3%. Average hourly earnings are expected to show 0.3% mom growth. Looking at other related data, ADP private payroll was a disappointment with only 158k growth. Employment component of ISM services dropped from 57.8 to 55.8. But employment component of ISM manufacturing jumped sharply from 53.5 to 57.2. Four week moving average of initial jobless claims was relatively unchanged at 243k while continuing claims stayed below 2m level. Conference board consumer confidence improved slightly to 118.9. The data point to a solid NFP report today, which on the other hand, could be seen as a setup for a downside surprise.

Also on the data front, Japan labor cash earnings rose 0.7% yoy in May, while real cash earnings rose 0.1% yoy. UK production data will be the main focus in European session, where trade balance will also be released. Germany will release industrial production too. Swiss will release unemployment and foreign currency reserves. Later in the day, in additional to US NFP, Canada will also release employment data and Ivey PMI.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 128.40; (P) 128.90; (R1) 129.82; More...

EUR/JPY's rally extends and reaches as high as 129.91 and there is no sign of topping yet. Firm break of medium term projection level at 128.89 will pave the way to next near term projection level at 100% projection of 114.84 to 125.80 from 122.39 at 133.35. On the downside, break of 127.99 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the break of 126.09 support turned resistance should have confirmed completion of down trend form 149.76 (2014 high), at 109.03 (2016 low). Current rise from 109.03 has already met target of 100% projection of 109.03 to 124.08 from 114.84 at 129.89. Sustained break there will pave the way to 61.8% retracement of 149.76 to 109.03 at 134.20 and above. Medium term outlook will now remain bullish as long as 122.39 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | JPY | Labor Cash Earnings Y/Y May | 0.70% | 0.40% | 0.50% | |

| 0:00 | JPY | Real Cash Earnings Y/Y May | 0.10% | -0.10% | 0.00% | |

| 5:00 | JPY | Leading Index May P | 104.6 | 104.2 | ||

| 5:45 | CHF | Unemployment Rate Jun | 3.20% | 3.20% | ||

| 6:00 | EUR | German Industrial Production M/M May | 0.20% | 0.80% | ||

| 7:00 | CHF | Foreign Currency Reserves Jun | 695.0B | 693.7B | ||

| 8:30 | GBP | Industrial Production M/M May | 0.40% | 0.20% | ||

| 8:30 | GBP | Industrial Production Y/Y May | 0.20% | -0.80% | ||

| 8:30 | GBP | Manufacturing Production M/M May | 0.40% | 0.20% | ||

| 8:30 | GBP | Manufacturing Production Y/Y May | 0.90% | 0.00% | ||

| 8:30 | GBP | Construction Output M/M May | 0.60% | -1.60% | ||

| 8:30 | GBP | Visible Trade Balance (GBP) May | -10.9B | -10.4B | ||

| 12:00 | GBP | NIESR GDP Estimate Jun | 0.20% | |||

| 12:30 | CAD | Net Change in Employment Jun | 54.5k | |||

| 12:30 | CAD | Unemployment Rate Jun | 6.60% | |||

| 12:30 | USD | Change in Non-farm Payrolls Jun | 173K | 138K | ||

| 12:30 | USD | Unemployment Rate Jun | 4.30% | 4.30% | ||

| 12:30 | USD | Average Hourly Earnings M/M Jun | 0.30% | 0.20% | ||

| 14:00 | CAD | Ivey PMI Jun | 53.8 | |||

| 14:30 | USD | Natural Gas Storage | 46B |

Let Me See Your Fingers: Silver Flash Crash

Uh oh. It happened again.

Speaking to people around the traps this morning, it actually doesn’t even sound like it was a fat finger as such. It is a break of a daily trend line that has been in play since 2015 and it just happened to line up with the previous swing low from 2016.

There would have been a tonne of stops sitting just below this level and in illiquid Asian session trading, we know things can get out of hand quite quickly when sell orders all start triggering with nobody in sight to buy.

Take a look at what I’m talking about on the XAG/USD daily chart below:

Silver Daily:

Market Morning Briefing: Dow Broke Below 21400

STOCKS

Dow (21320.04, -0.74%) broke below 21400, indicating that the downward correction might not be over yet. Note that 21500 is a crucial long term resistance which could bring in sharp rejection towards 21200 or maybe even lower. Medium term looks bearish.

Dax (12381.25, -0.58%) has been trading exactly between 12500 and 12300 levels and as mentioned yesterday, while 12500 holds we could see some more downside in the near term possibly extending towards 12200 levels. Near term looks sideways to bearish.

Shanghai (3196.23, -0.50%) is in an uptrend and could see eventual rise towards 3220-3240 with some interim dips. We could see a bounce from 3190 back to higher levels next week.

Nikkei (19965.78, -0.14%) came down to test 19856 contrary to our expectation of a rise. There could be some chances of testing 19750 on the downside in the near term but overall medium term looks potentially bullish.

Nifty (9674.55, +0.38%) made an intra-day high of 9700 yesterday, testing our initial target. 9700 is an important level just now and if it breaks, we could see a sharp 100points rally towards 9800 soon. Else there could be some scope of consolidation within 9600-9700 region.

COMMODITIES

In the smaller time frame, Gold (1219) is oversold and needs a pause before attempting sub 1190 levels. It is hovering around 1120 levels which is a near term area of support and a pause in the range of 12320-1245 can provide the necessary bearish momentum.

Silver (15.74) is trading below its support of 15.80. The scrip is oversold too thus weekend profit taking could pull the price towards 16.20 levels. Markets are now awaiting U.S. non-farm payrolls for June, due on today at 6:00 pm IST, for more insight into Fed policy and the future path of U.S Dollar.

No directional movement had been seen in Copper (2.66) also as it is trading within the range of 2.66-2.78.If 2.66 holds then we might see 2.82 within few days of time otherwise it might come back towards 2.55 levels. We will remain bullish on copper while it is trading above 2.55 levels.

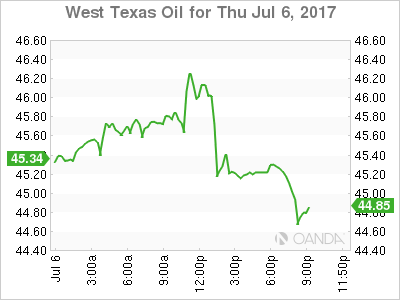

A shortage in U.S crude inventory by more than 6 million barrels could not generate enough buying momentum to keep the prices of Brent (47.46) and WTI (44.92) above their respective resistances. Prices had fallen as OPEC June exports were up 450k bpd from May, and up 1.9 million barrel a day from a year ago due to the supply from Libya and Nigeria, which are not bound by the OPEC/NOPEC production cut agreements. If the key resistances of 48 (Brent) 46.50 (WTI) will hold for the week then gradual selling for the target of 44.70 and 42 can ’t be ruled as seller will take every bounce as a further opportunity for selling.

FOREX

The currency markets are preparing for the shift to a more hawkish stance of the central banks from the decade long accommodative stance, pushing the yields higher everywhere and strengthening majors against Dollar. US NFP data tonight remains the main focus now.

It was stated repeatedly earlier in the week that most of the majors have been in a normal correction and further break of major supports are required before the downtrend can be confirmed. The correction of Euro (1.1415) has probably ended as it bounced back near to the year high of 1.1445 and Dollar Index (95.92) slipped below 96.00. If the US NFP data comes weak tonight, Dollar may test the major support of 95.50-40 while Euro may rise further to the long term resistance area near 1.15-1.16.

Dollar Yen (113.69) is rallying towards our targets of 114.30-115.00 as expected with the immediate support coming higher at 113.00-112.75.

Pound (1.2970) responded well to the requirement of an immediate rally but still requires a break above the major resistance area of 1.3030-50 to negate downside risks and confirm further rise towards 1.3200.

Aussie (0.7585) remains weak despite the global Dollar weakness and may test the lower support levels of 0.7530-15.

Dollar Rupee (64.78) closed flat despite the activity in the global forex and may end the week in the range of 64.60-90 without much movement.

INTEREST RATES

The US yields have risen sharply, the 30YR (2.92%) breaking above the immediate resistance. The 5YR (1.94%) and the 10Yr (2.37%) are also trading higher and looks bullish for the next few sessions.

The US 10-5Yr differential (0.43%) has risen sharply and could test resistance near 0.4375% in the next few sessions from where a rejection towards 0.4125% is possible.

The German-US 10Yr (-1.81%) has risen above important resistance and while that holds, the yield spread could move up in the near term. In that case, it could be an indication of further strength in Euro.

The US-Japan 10Yr (2.28%) has been rising sharply in the last few sessions and while it continues to rise, we may see a weaker Yen going forward. The yield spread could rise towards 2.33% in the coming sessions.

The German-Japan 10Yr yield spread (0.47%) has broken a long 1-year sideways channel and moved up sharply. The spread could move up further in the near term and take up EUR/JPY to much higher levels in the near term. A rise in EUR/JPY (129.84) towards 132 and higher is possible soon.

A World Of Confusion

Another stellar volume day in the Forex world with clear and distinct market drivers leading the way. After 24 hours to digest the FOMC minutes smart money suggest one more rate hike in 2017 but the tail risk given the markets disparate US economic view is a softer outlook as the market continues to lean against the Federal Reserve Hawkish convictions given the downcast inflation outlook.

As for the Greenback, the key to any sustainable USD recovery is down to the yield curve and more precisely a faster and steeper tightening cycle.

The first Friday of the month brings in the granddaddy of all economic indicators, US Non-Farm payrolls. The markets will look past the headline print and focus on the wage growth component given the Feds” It’s all about inflation mandate.“

The ECB minutes were viewed minimally hawkish, but the EUR resurgence was driven off the back of fixed income moves with the market seeing the Feds to hike just one more time in 2017 while l the ECB looks to taper and perhaps even more aggressively than the current view.With that in mind, German bund yields broke 0.50% for the first time since January 2016

Although US payrolls will be the primary focus, the G-20 summit should not be ignored given the US Presidents Trumps controvertible view of the brave new world. Expect the president’s tone to be bombastically pugnacious toward the developments in North Korea which move from the spotlight to under the microscope.

There is such an unpalatable level of uncertainty that suggests investor appetite for risk remains low.

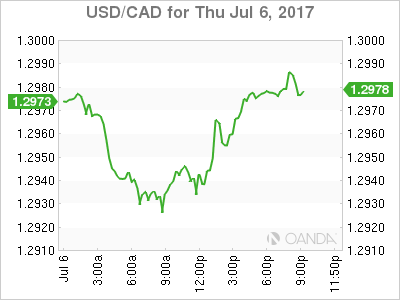

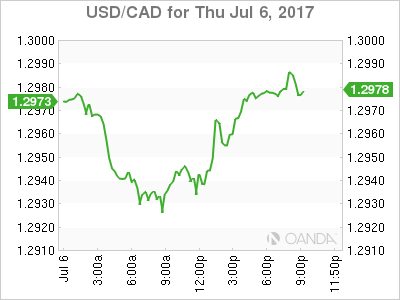

USD/CAD Canadian Dollar Higher On Surprise Oil Inventories Drawdown

The Canadian dollar appreciated against the US dollar on Thursday after the release of underperforming US economic indicators and a bigger drawdown of weekly crude inventories boosted the loonie. The Canadian currency has gained ever since Bank of Canada (BoC) senior policy makers have hinted at an upcoming rate hike. The market is pricing in a rising probability of a higher benchmark rate when the central bank meets on July 12.

Political risk has impaired the US dollar as the Trump administration has struggled to persuade republican senators to pass the healthcare reforms under consideration. The divisive proposal has reduced the political capital available to the Trump administration with the pro-growth policies still to see the light of day. The Trump trade got underway in December as infrastructure spending and fiscal stimulus was thought to be the first policies to be pushed through a Republican majority.

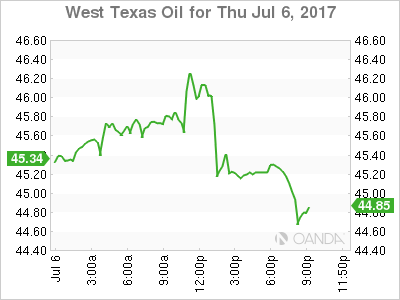

Oil prices rose as crude inventories in the US had a bigger drawdown than expected. Crude has been caught in a battle between Organization of the Petroleum Exporting Countries (OPEC) and other producers who signed a production cut agreement and Brazil, Canada and the United States who are part of the deal and have ramped up production.

The Canadian trade balance showed a rise in export and imports in May that marked records for both. The balanced showed a larger than expected $845 million it was explained by a one-time import of five airliners. Eight of the eleven export sectors have grown for three consecutive months. The trade data validates the optimism shown by the comments of BoC Governor about the Canadian economy.

The USD/CAD lost 0.239 in the last 24 hours. The currency pair is trading at 1.2953 after a mixed bag of economic indicators for the US dollar. The private payrolls ADP report disappointed with a 158,000 positions added, after a forecast of 184,000 and a downward revision that reduced by 23,000 last months massive gain. US unemployment claims came in higher than anticipated by a small margin but added to the pessimism about US employment. The ISM non-manufacturing PMI exceeded the forecast by reaching 57.4 in June. Both ISM surveys showed an overall strength in the manufacturing and services sectors.

The rise of oil prices after the lower than expected inventories boosted the CAD but the currency pair remains range bound ahead of the U.S. non farm payrolls (NFP) due on Friday, July 7 at 8:30 am EDT. The forecast for US jobs is for a gain of 175,000 new positions added in June. Last month’s report was 23,000 jobs lower than forecast and the slowdown in the private sector has raised concerns that it could come under forecasts. Given the focus of the Fed on inflation the market will be focusing on the average hourly earnings as a measure of inflation. Wages are forecasted to have grown 0.3 percent from last month.

Canadian employment data will also be released at the same time with a gain of 11,000 expected after the monster 54,500 gain last month. The CAD has appreciated since June 11 when the Bank of Canada (BoC) turned hawkish saying the rate cuts from 2015 have done their job. The central bank is widely anticipated to hike rates this year with the July 12 meeting at more than 50 percent probability.

Oil prices rose 0.5 percent on Thursday. The West Texas Intermediate is trading at $45.24 after the Energy Information Administration (EIA) weekly crude inventories report showed a bigger than expected drawdown. US crude stocks fell by 6.3 million barrels last week and let the total inventories at a six month low. The black stuff could not hold to most of the drawdown related gains as it backtracked as there are still concerns about oversupply. American output has increased and it has all but offset the efforts from the Organization of the Petroleum Exporting Countries (OPEC) who signed a production cut agreement with other major producers to limit the global supply.

The production cut agreement has enjoyed from full compliance in the first six months and was extended for another 9 after its effects have only managed to stabilize oil prices. Demand remains soft even as energy importing nations are running out of storage as they take advantage of current low prices.

Investment banks have reduced their price forecasts into the $50 to $55 price range for the end of the year. The battle between OPEC deal agreement producers and the US will continue to dictate the price of energy.

Market events to watch this week:

Friday, July 7

4:30 am GBP Manufacturing Production m/m

8:30 am CAD Employment Change

8:30 am CAD Unemployment Rate

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

Dollar Stumbles Ahead of US Jobs Report

Central Banks and Geopolitics Pressure Dollar

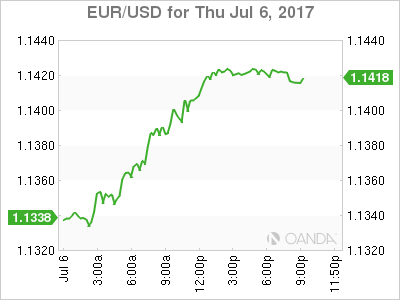

The US dollar is lower against most of the majors as a host of central banks have joined the Fed’s hawkish club in words if not in actions. The minutes from the European Central Bank (ECB) released on Thursday and disappointing private payrolls in the US had the dollar losing ground ahead of the U.S. non farm payrolls (NFP) to be published on Friday, July 7 at 8:30 am EDT.

Job gains have been steady in the US with employment the most reliable pillar of the economic recovery. Wage growth has been slow and with low inflation a concern for the U.S. Federal Reserve it will be one of the most discussed indicators. The US is expected to have gained 175,000 positions with hourly earnings rising 0.3 percent on a monthly basis.

Geopolitics will also be front and center as the G20 meeting is underway in Hamburg, Germany. Highlights will include the first face-to-face meeting with Vladimir Putin as well as several trade talks as American protectionism has been criticized.

The EUR/USD gained 0.849 percent in the last 24 hours. The single currency is trading at 1.1423 and was boosted by the release of the European Central Bank (ECB) meeting notes. The EUR has appreciated versus the USD as more central banks have been optimistic about economic growth despite low inflation. The ECB has a long way to go before it can start a tightening monetary policy, but so far the rhetoric has hinted at tapering of its quantitive easing program.

The ADP report was lower than expected but still points to a solid job market, the same story as the unemployment claims that also underwhelmed this week. The pressure is on the NFP jobs report to dispel the doubts surrounding wage growth and its implications on inflation that could reduce the tightening of monetary policy by the Fed. The central bank is expected to start reducing its balance sheet and hike rates one more time before the year ends.

Oil prices rose 0.5 percent on Thursday. The West Texas Intermediate is trading at $45.24 after the Energy Information Administration (EIA) weekly crude inventories report showed a bigger than expected drawdown. US crude stocks fell by 6.3 million barrels last week and let the total inventories at a six month low. The black stuff could not hold to most of the drawdown related gains as it backtracked as there are still concerns about oversupply. American output has increased and it has all but offset the efforts from the Organization of the Petroleum Exporting Countries (OPEC) who signed a production cut agreement with other major producers to limit the global supply.

The production cut agreement has enjoyed from full compliance in the first six months and was extended for another 9 after its effects have only managed to stabilize oil prices. Demand remains soft even as energy importing nations are running out of storage as they take advantage of current low prices.

Investment banks have reduced their price forecasts into the $50 to $55 price range for the end of the year. The battle between OPEC deal agreement producers and the US will continue to dictate the price of energy.

The USD/CAD lost 0.239 in the last 24 hours. The currency pair is trading at 1.2953 after a mixed bag of economic indicators for the US dollar. The private payrolls ADP report disappointed with a 158,000 positions added, after a forecast of 184,000 and a downward revision that reduced by 23,000 last months massive gain. US unemployment claims came in higher than anticipated by a small margin but added to the pessimism about US employment. The ISM non-manufacturing PMI exceeded the forecast by reaching 57.4 in June. Both ISM surveys showed an overall strength in the manufacturing and services sectors.

The rise of oil prices after the lower than expected inventories boosted the CAD but the currency pair remains range bound ahead of the U.S. non farm payrolls (NFP) due on Friday, July 7 at 8:30 am EDT. The forecast for US jobs is for a gain of 175,000 new positions added in June. Last month’s report was 23,000 jobs lower than forecast and the slowdown in the private sector has raised concerns that it could come under forecasts. Given the focus of the Fed on inflation the market will be focusing on the average hourly earnings as a measure of inflation. Wages are forecasted to have grown 0.3 percent from last month.

Canadian employment data will also be released at the same time with a gain of 11,000 expected after the monster 54,500 gain last month. The CAD has appreciated since June 11 when the Bank of Canada (BoC) turned hawkish saying the rate cuts from 2015 have done their job. The central bank is widely anticipated to hike rates this year with the July 12 meeting at more than 50 percent probability.

Market events to watch this week:

Friday, July 7

4:30 am GBP Manufacturing Production m/m

8:30 am CAD Employment Change

8:30 am CAD Unemployment Rate

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

Bunds Breakout In Telltale EUR Sign

Talk of removing the easing bias in the ECB minutes helped to push German 10-year yields above a key level. The euro was the top performer while the New Zealand dollar lagged. Japanese earnings data and comments from the Fed's Fischer are due later. Yesterday's EURUSD long was issued @ 1.1325 when the price was at 1.1340s but when it subsequently fell to as low as 1.1330, only those who manually entered higher have pariticipated in the 100-pip rally.

Bund yields rose 9 basis points on Thursday as borrowing costs jumped across the eurozone. The rise to 0.56% in German benchmark 10s continues a climb that started from 0.26% on June 27 when Draghi alluded to temporary factors holding down inflation. German-US 10yr spread hit a fresh 8 mth high, a pattern that Ashraf widely discussed in the Premiun videos of the last 2 weeks.

Since then, ECB officials have tried to put the genie back in the bottle. A series of 'ECB sources' stories have said officials are growing worried about a European-style taper tantrum and are unhappy about the rise in the euro.

They had more to be unhappy about with German 10-year yields breaking a double top at 0.5% and hitting the highest since January 2016. The euro was slow to react to the bond move initially but it gained momentum throughout the day in an eventual climb to 1.1420 from 1.1340. It highlights the buy-the-dip approach that's increasingly popular in EUR/USD and EUR/JPY.

The minutes of the ECB meetings on June 7-8 warned prophetically that small changes in communication could be misperceived. They also revealed that Draghi & Co had discussed removing the easing bias at the time but decided it was prudent that it remained.

What the ECB likely wasn't counting on at the time was the rise in the euro and yields. So the question becomes: Is that a gamechanger? It might be. The ECB knows that the recovery is at a delicate stage and they won't want to be accused of snuffing out the flames before the fire takes hold. What's tougher to say if that's a major worry at EUR/USD 1.14 or at 1.20?

What could help the ECB is that if the US economy regains some momentum along with signs of inflation. Non-farm payrolls expectations edged lower after June ADP employment at 158K compared to 185K expected. That puts a downside bias in non-farm payrolls but the market will be much more focused on wages signals.

The Fed also has an opportunity to send direct signals with Fischer due to speak at 2330 GMT. The topic of the speech is government policy and labor productivity so it may steer clear of comments on rates. The other event to watch is at 0000 GMT when Japanese labor cash earnings are due. A rise of 0.4% is expected but real earnings are forecast to fall 0.1% y/y in a reminder that the BOJ still has a long ways to go before even thinking about raising rates.

Non-Manufacturing Sector Expansion Unexpectedly Accelerates in June

Institute for Supply Management's (ISM) non-manufacturing index rose 0.5 points to 57.4 in June. The headline print came in firmly above market consensus which called for a modest decline to 56.5.

Gains were broad-based with the majority of the survey components accelerating in June. All of the subcomponents are now in expansionary territory, including prices and imports that had previously been in contractionary territory.

Among the main sub-indicators, new orders rose 2.8 points to 60.5, prices paid rose 2.9 points to 52.1, while business activity also recorded a small uptick (+0.1 to 60.8). On the other hand, the employment sub-index pulled back 2 points to 55.8, following a healthy 6.4 point increase in the month prior.

Comments from survey contacts remained largely positive. Nearly all non-manufacturing industries surveyed reported growth in June, with 'Other Services' being the only exception.

Key Implications

Similar to its manufacturing equivalent, the ISM non-manufacturing index surpassed market expectations and accelerated in June. What is more, the index remains firmly in expansionary territory and comments from contacts remain largely positive with most industries reporting growth last month. Improvements among most of the main subcomponents including new orders and business activity, both of which have continued to outperform the overall index for most of the post-recession period, added to the encouraging headline print.

While the employment component pulled back slightly, this followed a large gain in the month prior. Overall, the sub-index remains on a decent footing relative to the experience of the last two years, boding well for a respectable print for June's payrolls report tomorrow.

The improvement in the prices paid sub-index was encouraging at first glance, with the component moving back to expansionary territory in June. Nonetheless, the index failed to recoup the significant ground lost in the month prior, with the prices sub-index remaining lower on a year-over-year basis for a second consecutive month – mirroring the same trend in the manufacturing survey. All told, this implies some additional softness for overall price pressures. While yesterday's minutes from June's FOMC decision suggest that most Fed officials see the recent price weakness largely as transitory, slowing inflation remains the main risk to the pace of policy rate normalization.

Gold Shrugs off Bland Federal Reserve Minutes, Soft Job Numbers

Gold has posted small losses in Thursday trading. In the North American session, spot gold is trading at $1224.01 per ounce. On the release front, US employment numbers were softer than expected. ADP Nonfarm Payrolls dropped to 154 thousand, well below the estimate of 184 thousand. Unemployment claims rose to 248 thousand, above the estimate of 243 thousand. On Friday, there are three key employment events – Average Hourly Earnings, Non-Farm Employment Change and the unemployment rate. As well, the Federal Reserve will release its semi-annual Monetary Policy Report. If there are some surprises from these key employment events, we could see some volatility from gold.

Gold prices started the week with sharp losses, falling to 7-week lows on Monday. Since then, the metal has been subdued. The Federal Reserve minutes were on the dull side, as policymakers appear to have retreated from their upbeat view of the US economy in the June rate statement. The minutes revealed divisions in the Fed over inflation and the bloated balance sheet, but failed to provide any clarity about future monetary policy. Some FOMC members expressed unease at the Fed's current forecast of rate hikes, given the persistently low levels of inflation. According to the current "dot plot", the Fed expects to raise rates in December, and three times in 2018. There was also dissension over the timing of reducing the $4.2 trillion balance sheet – some policymakers were in favor of starting in September, while others preferred later in the year. At the June meeting, the Fed stated that it would begin reducing the balance sheet this year, but provided no details. Analysts expect the Fed to start winding down the balance sheet in September, prior to a rate hike in December.

The Fed has consistently said that it plans to raise interest rates for a third and final time in December. Last month, Fed Chair Janet Yellen shrugged off inflation worries, saying that she expected inflation was mired at lows levels due to temporary factors. However, the markets don't seem to be buying in, as the odds of a December hike are only 50%, according to the CME Group. The US economy slowed down in the first quarter, and there are signs that Q2 will also be soft. Consumer spending, which comprises two-thirds of US economic growth, remains soft. Another sore point in the economy is inflation, which remains below the Fed's target of 2%. If the economy doesn't show signs of stronger growth and higher inflation, the Fed might change its tune about a December rate, which would likely send the US dollar lower.