Sample Category Title

Dollar Falls ahead of Friday’s Employment Report as Euro Gains on ECB Minutes

The US dollar lost significant ground against the euro in today's forex action while it was also under pressure against the yen as sentiment towards the greenback turned negative ahead of Friday's employment numbers.

In Europe, German factory orders for May grew by 1% month-on-month, while analysts had been expecting a 2% increase. During April, factory orders had fallen by 2.2%. In the monetary policy meeting accounts of the European Central Bank, there was a discussion whether the pledge to accelerate the bank's bond buying should be dropped in order to reflect an improving economic background. However, inflation was still weak and this called for stable policy.

Euro/dollar briefly crossed above the 1.14 level to make a high for the day at 1.1401 and continued to hover slightly below that level at 1.1395 at the time of writing despite a beat in the ISM non-manufacturing PMI.

It was a relatively busy day for US economic releases. Starting with the ADP private sector payroll numbers for June, they came in at 158 thousand; a little off from the 185K expected by analysts and down from the previous month's downwardly revised figure of 230K. Initial weekly jobless claims were also a little negative as they climbed slightly to 248K from 244K the previous week. The nation's trade balance was more or less in line with expectations with a deficit of 46.50 billion dollars during May. The respective deficit during April was 47.6 billion.

The day's most important economic news came with the release of the ISM non-manufacturing index for June. The index rose to 57.4 compared with 56.9 in May. Analysts had forecast a print of 56.5. While the new orders component climbed sharply to 60.5, the employment sub-index fell a couple of points to 55.8. Prices paid also rose to 52.1 form 49.2, which could have some implications for services inflation going forward.

Against the yen the dollar was in a narrow range as an effort to break above 113.46 failed after stock markets turned south and some risk aversion set in. Dollar/yen was last at 113.20.

In commodities, gold was holding around $1223 an ounce whereas oil extended its rebound from the previous day's deep losses to $46.33. In today's crude oil inventory report, there was a significantly larger-than-expected draw of 6.29 million barrels. Analysts were expecting only a 2.28 million barrels draw and this substantial encouraged further gains for oil prices

Looking ahead, Friday's agenda will be dominated by June's employment report in the United States. Nonfarm payrolls are expected to come in at 179 thousand, the unemployment rate to hold at 4.3% and average hourly earnings to rise by 0.3%. Following that number, during the weekend, traders could follow the G20 summit in Germany for clues about the economic policy of the world's major economies. Geopolitics are also an issue to watch after this week's North Korean missile test.

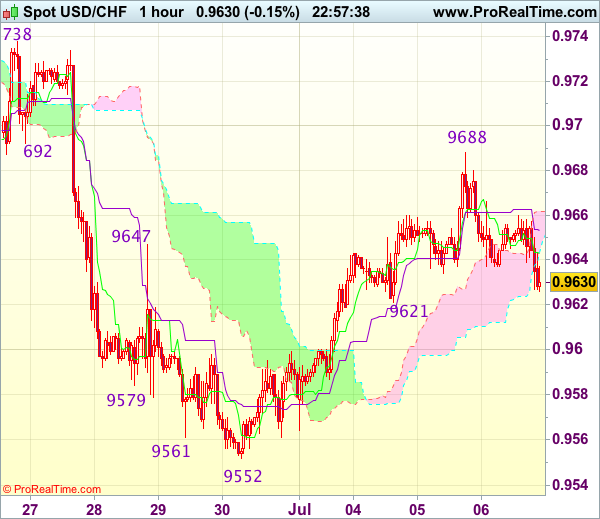

Trade Idea Wrap-up: USD/CHF – Buy at 0.9585

USD/CHF - 0.9630

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9642

Kijun-Sen level : 0.9651

Ichimoku cloud top : 0.9662

Ichimoku cloud bottom : 0.9648

Original strategy :

Buy at 0.9600, Target: 0.9700, Stop: 0.9565

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9585, Target: 0.9685, Stop: 0.9550

Position : -

Target : -

Stop : -

As the greenback retreated after rising to 0.9688, suggesting consolidation below this level would be seen and pullback to 0.9621 support cannot be ruled out, however, if our view that low has been formed at 0.9552 is correct, downside would be limited to 0.9585-90 and bring another rebound later, above said resistance would extend the rise from 0.9552 low for retracement of recent decline to 0.9700 but reckon upside would be limited and price should falter below resistance area at 0.9738-43.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback as 0.9585-90 should limit downside and bring another rise later. Below 0.9560-65 would abort and signal intra-day top is formed, risk retest of 0.9552, then towards 0.9525-30.

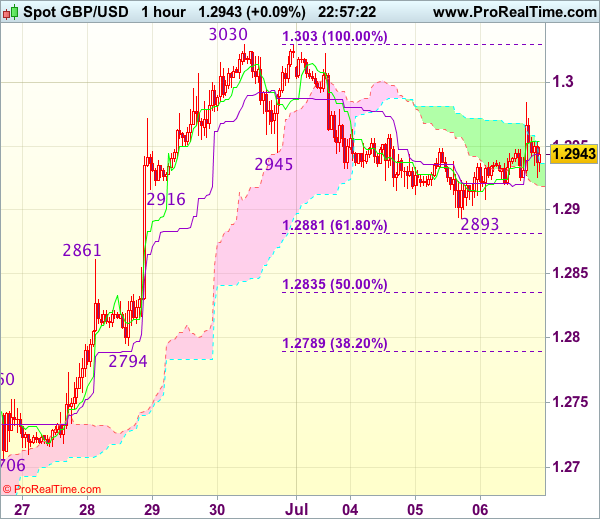

Trade Idea Wrap-up: GBP/USD – Buy at 1.2865

GBP/USD - 1.2948

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2954

Kijun-Sen level : 1.2946

Ichimoku cloud top : 1.2936

Ichimoku cloud bottom : 1.2918

Original strategy :

Buy at 1.2865, Target: 1.3000, Stop: 1.2830

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2865, Target: 1.3000, Stop: 1.2830

Position : -

Target : -

Stop : -

Although the British pound has recovered after falling to 1.2893, reckon upside would be limited to 1.2980-85 and near term downside risk remains for the corrective fall from 1.3030 (last week’s high) to bring retracement of recent upmove to 1.2880-85 (38.2% Fibonacci retracement of 1.2640-1.3030), however, downside should be limited to 1.2865-70 and bring another upmove later, above 1.2980-85 would signal low is formed, bring rebound to 1.3000 but break of said resistance at 1.3030 is needed to signal recent upmove has resumed and extend further gain towards recent high 1.3048.

In view of this, we are looking to buy cable again on further corrective fall as previous resistance at 1.2861 should turn into support and contain downside, bring another rise. Below 1.2830-35 (50% Fibonacci retracement of 1.2640-1.3030) would abort and signal top is formed, bring further fall towards support at 1.2794.

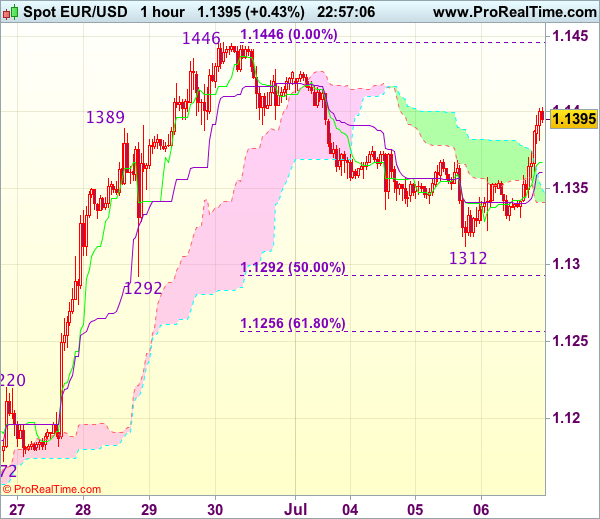

Trade Idea Wrap-up: EUR/USD – Buy at 1.1355

EUR/USD - 1.1399

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1374

Kijun-Sen level : 1.1365

Ichimoku cloud top : 1.1346

Ichimoku cloud bottom : 1.1340

Original strategy :

Buy at 1.1355, Target: 1.1455, Stop: 1.1320

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1355, Target: 1.1455, Stop: 1.1320

Position : -

Target : -

Stop : -

Current rebound suggests low has been formed at 1.1312 yesterday and consolidation with upside bias is seen for gain to 1.1415-20, however, break there is needed to signal the pullback from 1.1446 (last week’s high) has ended and bring subsequent retest of this level, break there would confirm recent upmove has resumed for headway to 1.1475-80 but price should falter below 1.1500.

In view of this, we are looking to buy euro on dips but one should exit on subsequent rally. Below 1.1325-30 would abort and signal an intra-day top is formed, risk test of said support at 1.1312, then 1.1292 (previous support as well as 50% Fibonacci retracement of 1.1139-1.1446).

Trade Idea Wrap-up: USD/JPY – Stand aside

USD/JPY - 113.14

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.25

Kijun-Sen level : 113.26

Ichimoku cloud top : 113.31

Ichimoku cloud bottom : 113.22

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback resumed recent rise and rose to as high as 113.69 yesterday, lack of follow through buying and the subsequent retreat suggest consolidation below this level would be seen and weakness to 112.80-85 (38.2% Fibonacci retracement of 111.46-113.69) is likely, however, break of support at 112.74 is needed to signal top has been formed there, bring retracement of recent rise to 112.40-45, then 112.20 but reckon 111.95-00 would hold from here.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Above said resistance at 113.69 would signal recent upmove is still in progress and may extend further gain to 114.00 but loss of momentum should prevent sharp move beyond 114.25-30.

Pound Edges Lower, Markets Eye US Nonfarm Payrolls

GBP/USD climbed close to the symbolic 1.30 level on Thursday, but has retracted. In North American trade, the pair is trading at 1.2940. On the release front, US employment numbers were softer than expected. ADP Nonfarm Payrolls plunged to 154 thousand, well below the estimate of 184 thousand. Unemployment claims rose to 248 thousand, above the estimate of 243 thousand. On Friday, there are three key employment events – Average Hourly Earnings, Non-Farm Employment Change and the unemployment rate. As well, the Federal Reserve will release its semi-annual Monetary Policy Report.

British PMIs in June continued to point to expansion, but there are concerns, as all three PMIs pointed to slower growth in June. The PMIs, which gauge the strength in the manufacturing, construction and services sectors, were all down compared to the May readings. The double whammy of the British election and the start of Brexit talks with Europe have increased uncertainty and resulted in a decrease in new orders across the economy, as underscored by the softer PMI readings. Weaker economic conditions and fears of a bite from Brexit have put the BoE in a difficult position regarding interest rate policy – the economy may not be ready for a rate hike, but inflation is at 3%, well above the BoE's inflation target of 2%. A rate hike would likely push inflation to lower levels.

BoE policymakers have not hesitated to publicly air their differences over rate policy, which clearly will not add to investor confidence. BoE Governor Mark Carney is at odds with MPC member Ande Haldane and other members regarding raising rates. Just a few weeks ago, Carney went on record, adamantly opposed to a rate hike. However, he has since softened his approach, and his comments at the ECB forum last week triggered a strong pound rally, as the currency punched above the 1.30 level for the first time since late May.

The Federal Reserve minutes were released on Wednesday, but the markets reacted with little more than a shrug. The minutes revealed divisions in the Fed over inflation and the bloated balance sheet, but failed to provide any clarity about future monetary policy. Some FOMC members expressed unease at the Fed's current forecast of rate hikes, given the persistently low levels of inflation. According to the current "dot plot", the Fed expects to raise rates in December, and three times in 2018. There was also dissension over the timing of reducing the $4.2 trillion balance sheet – some policymakers were in favor of starting in September, while others preferred later in the year. At the June meeting, the Fed stated that it would begin reducing the balance sheet this year, but provided no details. Analysts expect the Fed to start winding down the balance sheet in September, prior to a rate hike in December. The markets are lukewarm about a rate hike in December, with the odds at just 50%, according to the CME Group.

Yen Shrugs off Weak US Employment Numbers

USD/JPY has inched lower in Thursday trading. In the North American session, the pair slightly above the 113 level. On the release front, US job data was a disappointment. ADP Nonfarm Payrolls plunged to 154 thousand, well below the estimate of 184 thousand. Unemployment claims rose to 248 thousand, above the estimate of 243 thousand. On Friday, there are three key employment events – Average Hourly Earnings, Non-Farm Employment Change and the unemployment rate. As well, the Federal Reserve will release its semi-annual Monetary Policy Report.

A rebound in global economic growth has been a godsend for the Japanese economy, which has enjoyed a strong 2017. The export and manufacturing sectors are strong, consumers and businesses are spending more, and GDP expanded at an annualized rate of 1.0% in the first quarter. However, despite years of radical accommodative policy, the Bank of Japan has failed to raise inflation levels, which remain well below the bank's target of 2 percent. BoJ Governor Haruhiko Kuroda is on record in declaring that the bank would not lower its inflation forecast, but this stance apparently has changed. The BoJ appears ready to raise a white flag (of sorts) and lower its inflation target when policymakers gather for a rate meeting on July 20. However, traders should not expect the move to shake up the markets – any downgrade in the inflation target will likely be of a minor nature.

The Federal Reserve minutes were released on Wednesday, but the markets reacted with little more than a shrug. The minutes revealed divisions in the Fed over inflation and the bloated balance sheet, but failed to provide any clarity about future monetary policy. Some FOMC members expressed unease at the Fed's current forecast of rate hikes, given the persistently low levels of inflation. According to the current "dot plot", the Fed expects to raise rates in December, and three times in 2018. There was also dissension over the timing of reducing the $4.2 trillion balance sheet – some policymakers were in favor of starting in September, while others preferred later in the year. At the June meeting, the Fed stated that it would begin reducing the balance sheet this year, but provided no details. Analysts expect the Fed to start winding down the balance sheet in September, prior to a rate hike in December. The markets are lukewarm about a rate hike in December, with the odds at just 50%, according to the CME Group.

June’s Minutes Revealed ECB Discussed over Removing Asset Purchases Guidance, Euro Soars

The minutes for the June ECB meeting turned out more hawkish than expected, sending EURUSD to a 3-day high of 1.1397 and Europe's Stoxx 600 stock index to a 11-week low 378.45. The minutes unveiled that policymakers had discussed removing the guidance on the bond asset purchase program (QE), if necessary. Policymakers just shrugged off recent weakness in headline inflation as core inflation continued to climb higher. This came in line with President Mario Draghi's comments last week that "deflationary forces have been replaced by reflationary ones", pointing to a "strengthening and broadening recovery" in the Eurozone. German 2-year yield breached the March high after the comments and has rallied to a level not seen since January 2016 since then.

The minutes contained several flavors that were surprising to the market. It suggested that, as the tail risks to the recovery outlook have been vanishing, policymakers had considered dropping the "easing bias" in the forward guidance. The refrained from doing so as the region's economic recovery has not yet achieved higher inflation. The minutes also revealed, while the Council reiterated the promise to in the "size and/or duration" of the QE program, it believed that, "as the economic expansion proceeded and if confidence in the inflation outlook improved further, the case for retaining this bias could be reviewed".

Meanwhile, policymakers stressed that "continued caution in communication" is critical. It is particularly important to avoid sending signals that "could trigger a premature tightening of financial conditions, which in turn could put the progress made towards a sustained convergence towards the Governing Council's inflation aim at risk, thereby prolonging the need for extraordinarily accommodative monetary policy".

Recall that the ECB staff upgraded it GDP forecasts but downgraded the inflation outlook. The staff projected that GDP would expand +1.9% this year, up +0.1 percentage point +1.8% projected in March, before easing to +1.8% and then to +1.7% in 2018 and 2019, respectively. Note that growth forecasts for 2018 and 2019 were also revised higher +0.1 percentage point from previously. On inflation, the staff revised lower the forecasts to +1.5% for 2017, +1.3% for 2018 and +1.6% for 2019. The corresponding estimates in March were +1.7%, +1.6% and +1.7%. The Council members noted that they found it "puzzling" as the core inflation was revised lower despite stronger economic growth and falling unemployment rate.

Trade Idea: EUR/GBP – Sell at 0.8845

EUR/GBP - 0.8804

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

New strategy :

Sell at 0.8845, Target: 0.8745, Stop: 0.8885

Position : -

Target : -

Stop : -

Although the single currency recovered after finding support at 0.8756 and initial upside risk is for recovery to 0.8845-50, as long as indicated resistance at 0.8882 (last week’s high) holds, further consolidation would be seen and prospect of another retreat remains, below said support at 0.8756 would add credence to our view that a temporary top is possibly formed at 0.8882, bring retracement of recent upmove to 0.8730-35, however, still reckon downside would be limited to 0.8719 support.

In view of this, would be prudent to sell euro on recovery as 0.8845-50 should limit upside. Above 0.8882 would revive bullishness and extend recent upmove from 0.8304 low to 0.8900-10, having said that, as broad outlook remains consolidative, reckon current c leg of larger degree wave b should be limited to 0.8950 and price should falter well below 0.9000 psychological level.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Euro Price Action Dominates

- German bunds broke through the 0.5% yield resistance level in the morning and jumped (temporarily) on the ECB minutes. Sentiment spilled over to US Treasuries yields too, be it more modestly. The nervous mood is also apparent in equity markets, with losses in European stocks running around -0.90% and spilling over into the American S&P which moves around losses of -0.50%. EUR/USD is up around 0.35%.

- The ECB minutes revealed the Council considered removing the pledge to increase the bond-buying program if needed in their last meeting. It also thought "it was necessary to avoid signals that could trigger a premature tightening of financial conditions" that might undo the progress on inflation (mission failed).

- Private US employers added 158K jobs in June, according to the ADP payroll report. The consensus expected 188K and the figure is also lower than the 230K in May. A separate report showed that initial jobless claims edged slightly higher by 4K, while markets expected it to drop.

- Trump affirmed the American commitment to Nato's mutual defence clause and called on European nations to invest more in defence, in a hotly-anticipated speech on the transatlantic relationship in Warsaw. Trump also called Poland an exemplary ally against Russian "destabilising" behaviour.

- The EU and Japan have backed US calls for new UN sanctions on North Korea, after the country's test of an intercontinental ballistic missile earlier this week stoked diplomatic tensions in the region.

- European and Japanese leaders confirmed that they have reached a political agreement on a free-trade deal to liberalise markets from dairy products to car parts. Japanese PM Abe states the deal "is the birth of the world's largest, free industrialised economic zone".

- France plans to end the sale of petrol and diesel cars in the country by 2040, according to the new French environment minister's climate plan.

Rates

Law of gravity pulls Bund through major support

In past sessions, the Bund reached the key 161.68/58 support (neckline double top/38% retracement), but couldn't rebound sustainably. Every attempt to move away was aborted, suggesting buyers' fatigue. Today, that was no longer the case. In a morning session devoid of key economic releases, the Bund future dropped below the key support, immediately attracting more selling. There is no obvious trigger available to explain the break. News agencies attribute it to a "weak" French (and Spanish) auction of long papers. However, we saw no sign of that in the bidding (good bids/covers) nor in the pricing. ECB Villeroy said that "ECB's non-standard monetary stimulus will not last indefinitely" and added that "nominal interest rates, which are still particularly low today, have started to rise since autumn 2016 and are set to increase further, in line with the pace of economic recovery and inflation growth". However, these remarks were in the market well ahead of the break at 11h. We think that the Draghi's speech last week and the BIS warning on too accommodative monetary policy fertilized the soil for today's move. As the market goes our direction, we applaud the price action, but are fully aware that the break needs to be confirmed after tomorrow's payrolls release and in the weekly close. Peripheral yield spreads were barely affected with Ireland, Portugal and Greece even showing some (very) modest narrowing.

US Treasuries (and gilts) followed Bunds lower. The ADP report was weaker than expected and the initial claims marginally higher than expected, but it couldn't give US Treasuries the power to fight back. The trade deficit was in line with expectations. Just after the release of our report, the US non-manufacturing ISM will still be published.

At the time of writing, German yields increase by 1.5 (2-yr) to 8.1 bps (10-yr), the belly underperforming the wings. The key 0.50% yield resistance for the 10-year Bund was also broken and similarly, the 5-yr Bund yield confirmed the break of the -0.26% and is now closing in (helped by benchmark change) on the psycho 0% yield resistance. The US yield curve bear steepened with yields up between 0.8 bp and 5.7 bps (30-yr)

Currencies

Jump in European yields propels euro rebound

This morning, it was 'logical' to assume US data would drive USD trading. However, it turned out different. The German 10-year yields cleared the important 0.50% mark and interest rate differentials narrowed in favour of the euro. US data were softer than expected, but only of second tier importance. EUR/USD rebounded to the high 1.13 area. USD/JPY showed no clear trend as the rise in core yields was counterbalanced by a setback in global equities. USD/JPY hovers just north of 113.

Overnight, most Asian equity indices showed modest losses. Signs of division within the Fed, yesterday's setback of the oil price and ongoing geopolitical uncertainty on North-Korea caused some investor caution. USD/JPY drifted back to the 113 area. EUR/USD also ceded a few ticks and traded at around the 1.1340 area going into the European open.

There were no important eco data in Europe. Still, there was an interesting move in the European bond market and this move spilled over into the currency market. The Bund future contracts dropped below an important technical support pushing the 10-year German yield north of 0.50%. US yields lagged the rise in Europe, narrowing the interest rate differential in favour of the euro. EUR/USD extended its intraday rebound in the 1.13 big figure. Interestingly, the rise in core bond yields this time hardly supported USD/JPY, probably as equities suffered too. ECB's Praet tried to convince markets that the ECB had every reason to remain cautious but this didn't help to soften the rise of EMU yields and the euro.

In the US, ADP job growth was reported at 158 000, missing the consensus estimate of 188 000. The May figure was also revised downward. The claims and the trade balance were marginally worse than expected. The dollar recorded some additional losses. EUR/USD filled offers just below 1.14. USD/JPY lost a few ticks but is holding north of 113. Lower equities and weaker US data are keeping each other in balance for now. A good non-manufacturing ISM might help to prevent further USD losses. More than ever, we assume that the dollar.

Euro price action dominates

There were no eco data in the UK today. So, sterling trading was driven by the overall rebound of the euro. That said the intraday gains of EUR/GBP remained rather modest. The pair trades currently in the 0.8800 area. Cable showed no clear trend today. The pair still hovers in the mid 1.29 area. One shouldn't draw firm conclusions from today's EUR/GBP price action. If anything, the modest rise of EUR/GBP suggests that underlying sentiment on sterling remains constructive short-term.