Sample Category Title

UK Manufacturing PMI At Three-Month Low Of 54.3 In June

'While growth slowed in June, the average of the past three surveys pointed to the fastest rate of quarterly growth in the sector for three years.' — George Nikolaidis, EEF

Manufacturing activity in Britain slowed unexpectedly last month, a private survey showed on Monday. Markit report showed that its PMI for the UK manufacturing sector came in at 54.3 points in June, falling to a three-month low from a downwardly-revised figure of 56.3 in the preceding month. However, analysts expected a smaller decline to 56.4 for the month from May's originally reported 56.7. Growth of the country's manufacturing output slowed as businesses showed smaller increases in demand for new domestic orders, while export orders marked the weakest pace of growth in five months. Though, some economists expect the UK economy to show stronger growth in the Q2 with stronger competitiveness boosted by the weak Sterling. However, export orders are set to put downward pressures on further economic expansion. Meanwhile, overall confidence weakened to a seven-month low amid the beginning of the Brexit talks and more uncertainties surrounding the UK outlook. Opposite to Britain's faltering manufacturing sector, manufacturing activity in other EU countries rose to its highest level in six years in June.

Dairy Product Prices Drop For Second Straight Time

'Prices for nearer-dated contracts lifted more than prices for later dated ones, suggesting some buyers need whole milk powder more urgently than others.' — Susan Kilsby, AgriHQ

Dairy product prices fell for the second consecutive time at the latest auction held on Tuesday in New Zealand, official data showed. The GDT Price Index dropped 0.4%, following a 0.8% decrease registered at the preceding auction, with an average selling price of $3,303 per tonne. During the Tuesday auction, some 28,574 tonnes of dairy products were sold, compared with 21,171 sold previously. The price of skimmed milk powder fell 4.5% to $2,090 per tonne, the price of anhydrous milk fat dropped 3.5% to $6,596 per tonne. On the other hand, lactose gave up 3.3%, falling to $839 per tonne, while prices of cheddar retreated 3.2% to $4,051 per tonne. Moreover, the price of rennet casein fell 2.7% to $6,133, whereas butter prices showed a slight decline of 0.1% to $5,775. Though, the price of butter was still more than two times higher since June 2016. Some experts suggested that it was too early to expect dairy product prices to resume the downside trend. Some 127 out of 165 bidders won, with the majority of buyers coming from the Middle East and North Asia.

Elliott Wave Analysis: AUDUSD Undergoing A Three Wave Reversal Lower

AUDUSD made a sharp and strong recently, which we now see it as a start of a three wave reversal lower. This sharp reversal also suggests that a bigger correction within black wave IV is completed and that more weakness may follow. At the moment we see black wave A/1 in action, that can search for support around 0.7537 level.

AUDUSD, 4H

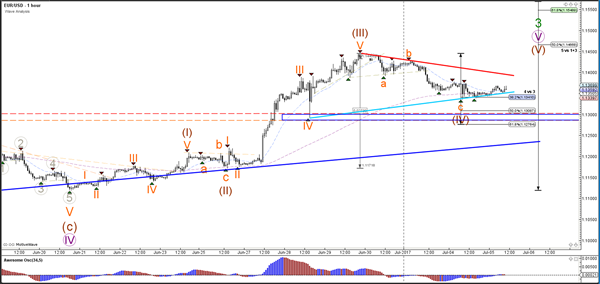

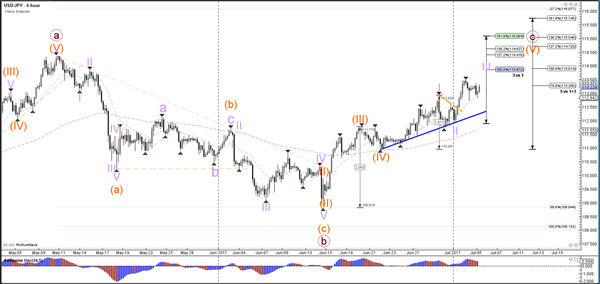

Daily Technical Analysis: EUR/USD, USD/JPY Setup Contracting Triangle Chart Patterns

Currency pair EUR/USD

The EUR/USD pullback is creating a contracting triangle chart pattern via the trend lines (blue/red). A bullish break above resistance (red) could see price approach the Fibonacci targets of wave 5 (purple) which could complete wave 3 (green). A bearish break could see price retest the broken resistance levels.

The EUR/USD is still completing its ABC zigzag correction (orange) within wave 4 (brown). The Fibonacci levels of wave 4 vs 3 (brown) plus the broken resistance levels (blue box) are a key support zone. A bullish bounce confirms the wave 4 whereas a bearish beak invalidates it.

Currency pair USD/JPY

The USD/JPY uptrend is still intact as long as price stays above the support trend line (blue). A new higher high could indicate a bullish continuation towards the Fibonacci targets of wave 3 (purple) and wave 5 (orange).

The USD/JPY is in a contracting triangle chart pattern (blue/red lines) after completing an ABC correction (pink). A break below the 61.8% invalidates the wave 4 (grey) whereas a bullish break confirms the wave 5 (grey).

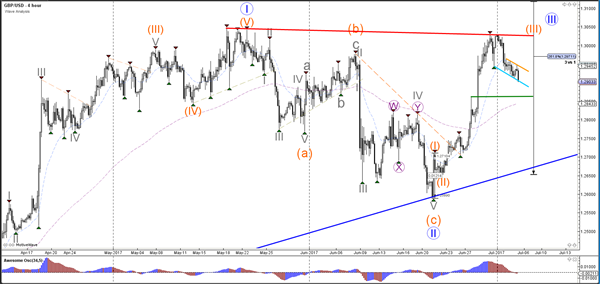

Currency pair GBP/USD

The GBP/USD bullish momentum is losing steam as price is falling lower. The resistance level (red) could be proving to be too tough to break. The support trend lines however could still provide a potential turn around (green/blue).

The GBP/USD is attempting to break below the support levels (blue) and 61.8% Fibonacci of wave 4 vs 3, which would invalidate the retracement.

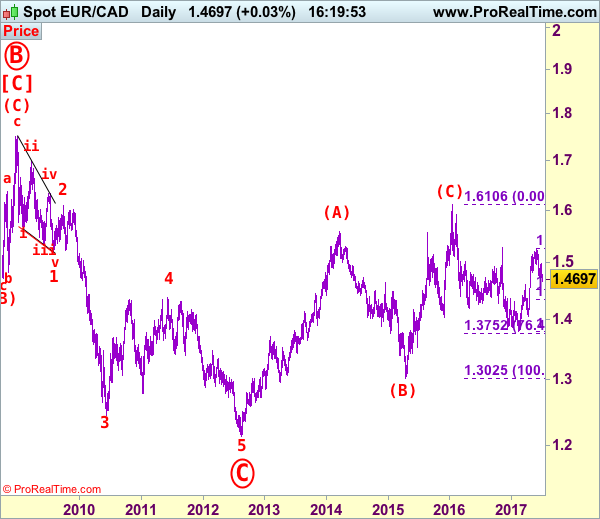

EUR/CAD Elliott Wave Analysis

EUR/CAD – 1.4693

EUR/CAD: Wave 4 ended at 1.4380 and wave 5 as well as circle wave C has possibly ended at 1.2129, major (A)-(B)-(C) correction has commenced and indicated target at 1.6000 had been met.

The single currency only recovered to 1.4980 (we recommended to sell at 1.5000 in our previous update and missed the entry) before dropping again, adding credence to our view that top has been formed at 1.5259 last month, hence downside bias remains for this fall from there to extend weakness to 1.4600, then 1.4520-25 (50% Fibonacci retracement of entire rise from 1.3784-1.5259), however, near term oversold condition should limit downside to 1.4480-85 and reckon support at 1.4397 would hold from here, risk from there is seen for a strong rebound to take place later.

Our latest preferred count is that larger degree wave [C] from 1.3289 as well as circle wave B ended at 1.7509 in Dec 2008 with (A): 1.6325, (B): 1.4719 followed by wave (C) at 1.7509, hence circle wave C is unfolding with wave 1 ended at 1.5186 (diagonal wave 1), wave 2 at 1.6096, impulsive wave 3 has ended at 1.2451, followed by wave 4 at 1.4380, in view of recent strong rebound, we are now treating the wave 5 as well as larger degree circle wave C has ended at 1.2129, hence (A)-(B)-(C) correction has commenced from there with impulsive wave (C) now unfolding and indicated initial upside target at 1.6000 had been met and reckon 1.6500 would hold.

On the upside, whilst initial recovery to 1.4730-35 and possibly 1.4780 cannot be ruled out, reckon upside would be limited to 1.4830-35 and bring another decline later. Above 1.4900 would risk another test of said resistance at 1.4980, break there would signal first leg of decline from 1.5259 top has ended, risk a stronger rebound to 1.5050 and possibly towards 1.5100-10 but price should alter well below said resistance at 1.5259 and bring another decline later this month.

Recommendation: Sell at 1.4770 for 1.4570 with stop above 1.4870.

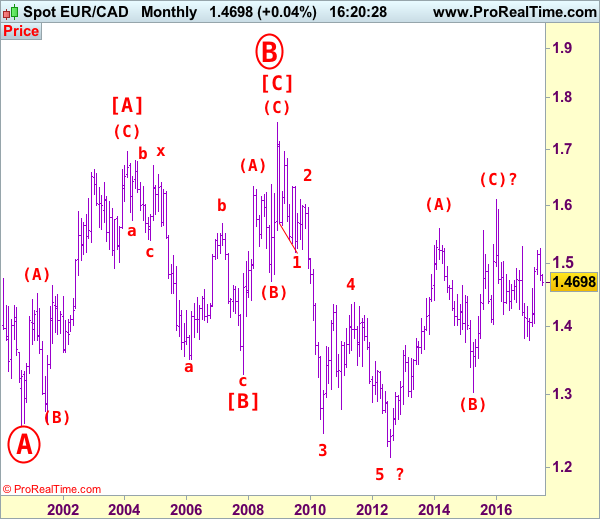

On the bigger picture, our long-term count on the monthly chart is that a big sideways consolidation from 2000 low of 1.2557 has possibly ended at 1.7509 as circle wave B with [A]: 1.6976 ( (A): 1.4513, (B): 1.2612, (C): 1.6976), wave [B]: 1.3289 is a double three with 1st a-b-c: 1.5384, x: 1.6709 and 2nd a-b-c: 1.3289. As indicated above, the wave [C] has ended at 1.7509. The selloff from there is now unfolding which itself should be labeled as an impulsive wave with wave 1: 1.5186 (diagonal wave 1), followed by wave 2: 1.6096 and wave 3: 1.2451, wave 4: 1.4380, wave 5 as well as larger degree circle wave C has possibly ended at 1.2129 and major correction has possibly commenced for retracement of recent decline towards 1.4000, then 1.4180-90 (38.2% Fibonacci retracement of 1.7509-1.2129). Below said support at 1.2129 would risk weakness to psychological support at 1.2000 and then 1.1851 (50% projection of 1.7509-1.2451 measuring from 1.4380) but reckon 1.1500 would remain intact, bring reversal later.

AUD/USD Elliott Wave Analysis

AUD/USD – 0.7615

AUD/USD – Wave 5 of C and (B) has possibly ended at 1.1081

Although aussie rose to as high as 0.7717 late last week, the subsequent sharp retreat from there suggests a temporary top has been formed and consolidation with initial downside bias is seen for weakness towards support at 0.7535, however, still reckon downside would be limited to 0.7490-00 and bring another rise later, above 0.7680-85 would bring retest of 0.7717, however, loss of upward momentum should prevent sharp move beyond previous chart resistance at 0.7750, bring another retreat later.

We are keeping our count that top has been formed at 1.1081 (wave 5 of V) and major correction (A-B-C-X-A-B-C) has commenced, indicated downside targets at 0.7945 (61.8% Fibonacci retracement of entire rise from 0.6007-1.1081) and 0.7750 had been met and downside bias is seen for further weakness to 0.6800, then 0.6700 but reckon 0.6500 would hold from here.

Our preferred count is that the rally from 0.6007 to 0.7270 (7 Jan 2009) is marked as wave A, the retreat to 0.6248 (2 Feb 2009) is wave B and the subsequent upmove is labeled as wave C with wave (iii) and wave (iv) ended at 0.8265 and 0.7700 respectively and wave (v) as well as 3 ended at 0.9407, then wave 4 ended at 0.8066 (instead of 0.8578). The wave 5 has met our indicated projection target of 1.1060 and could ended at 1.1081, this level is now treated as the peak of wave (C) as well as larger degree wave B, hence major fall in wave C has commenced, our initial downside target at psychological support at 0.7000 has just been met and further weakness to 0.6500 would be seen later.

On the downside, whilst initial pullback to 0.7535 support cannot be ruled out, reckon downside would be limited to 0.7490-00 and bring another upmove later. Below 0.7455-60 would abort and suggest the rebound from 0.7329 has ended instead, bring further fall to 0.7415 support, however, as broad outlook remains consolidative, indicated strong support at 0.7372 should remain intact.

Recommendation: Buy at 0.7500 for 0.7700 with stop below 0.7400.

Our alternate count on the daily chart treated the top formed in 2008 at 0.9851 could be a larger degree wave I and was followed by a deep and sharp correction in wave II to 0.6007 and wave III is unfolding from there.

The long-term uptrend started from 0.4775 (2 Apr 2001) with an impulsive structure. Wave I is labeled as 0.4775 to 0.9851 (15 Jul 2008), wave II has ended at 0.6007 (Oct 2008) and wave III is still in progress which may extend further gain to 1.1265.

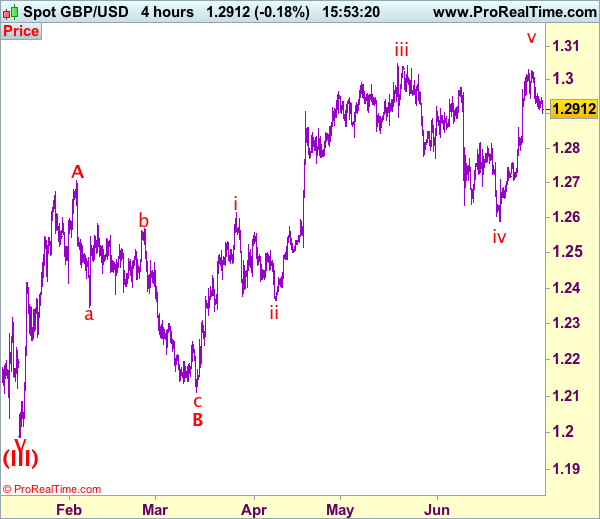

Trade Idea: GBP/USD – Buy at 1.2835

GBP/USD – 1.2906

Recent wave: Wave V of larger degree wave (III) has ended at 1.1986 and major correction has commenced from there for gain to 1.3000 and 1.3140-50

Trend: Near term up

Original strategy :

Buy at 1.2870, Target: 1.3020, Stop: 1.2810

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.2835, Target: 1.3000, Stop: 1.2800

Position: -

Target: -

Stop:-

As sterling has slipped again today, suggesting near term downside risk remains for the corrective fall from 1.3030 temporary top to bring retracement of recent upmove, hence weakness to previous resistance at 1.2861 (now support) cannot be ruled out, however, reckon 1.2830-35 (50% Fibonacci retracement of 1.2640-1.3030) would limit downside and bring another rise later, above 1.3000 would bring test of said resistance at 1.3030, break there would extend the rise from 1.2589 low towards recent high at 1.3048 but break there is needed to retain bullishness and bring subsequent headway towards 1.3090-00.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

On the downside, whilst initial pullback to 1.2900 is likely, reckon 1.2861 (previous resistance turned support) would limi downside and 1.2830-35 should hold, bring such a rise. Below support at 1.2794 would abort and signal top is formed instead, risk further fall to 1.2750, then towards 1.2706 support.

US Dollar Steady Ahead Of Fed Minutes, Euro, Sterling Modestly Up

Following yesterday's low trading activity during the US session amid the 4th of July holiday in the US, not much data has been released during today's Asian session either. Both, the euro and sterling modestly gained against the dollar. Looking at commodities, both oil prices and gold were up.

The Australian dollar retraced some of yesterday's losses, last trading at $0.7614, after tumbling on Tuesday as a result of the Reserve Bank of Australia's decision to maintain a neutral policy stance. It seems that traders dismissed a mixed bi-weekly global dairy auction report that showed average dairy prices edged lower from the prior period, but whole milk powder, a key New Zealand export, rose.

The greenback held steady against the yen during the Asian trading session, following some weakness yesterday. The dollar was trading at 113.26 yen, ahead of the European trading session. Looking ahead, the release of the Fed's meeting minutes will be the focus of the day that could induce significant moves in the US dollar. Ahead of Friday's key jobs report, investors want to gauge how committed the Fed was to hiking rates again this year, as well as any details on plans to wind back its balance sheet.

The euro gained against the US dollar during the Asian session, retracing yesterday's losses on a more cautious tone regarding the monetary policy outlook by the ECB's Chief Economist, Peter Praet. Upside in the Spanish services PMI provided a boost to the euro. At 58.3, June services PMI came in above the expectations of 56.5 and the prior month's 57.3. Euro/dollar was last trading at 1.1364. Looking ahead, the pair could be driven by services PMI data that are scheduled to be released for the eurozone and a number of its member countries, including Germany, France and Italy.

The pound also gained modestly against the greenback during the Asian session, with pound/dollar last trading at 1.2922. Similar to the eurozone, focus in the UK will be on services PMI for June. At 53.5, the forecast is just slightly below May's reading of 53.8.

In the commodities markets, gold rose for the second consecutive day, last trading above the $1,225 an ounce handle. The precious metal has been gaining as it is perceived as a safe-haven in the wake of another long-range missile test by North Korea.

Oil prices across have been rising as the European session was starting. WTI inched higher, reaching $47.13 a barrel, following several days of gains. Brent crude has been also gaining, up 0.26%, last trading at $49.76 a barrel.

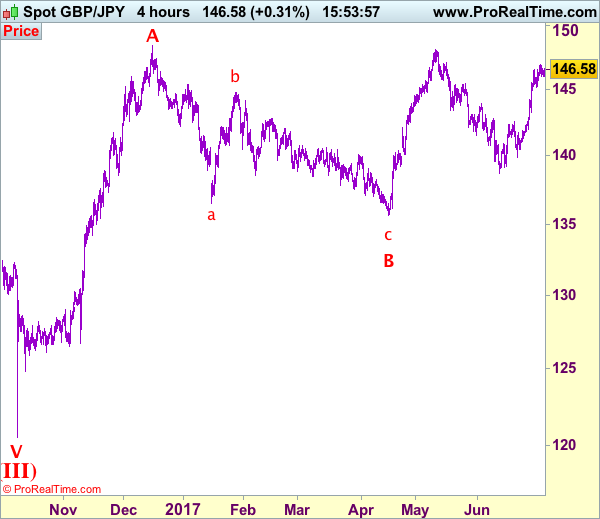

Trade Idea: GBP/JPY – Buy at 145.15

GBP/JPY - 146.55

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term up

Original strategy:

Buy at 145.15, Target: 147.15, Stop: 144.55

Position: -

Target: -

Stop: -

New strategy :

Buy at 145.15, Target: 147.15, Stop: 144.55

Position: -

Target: -

Stop:-

As sterling has maintained a firm bias after recent rally, suggesting bullishness remains for further gain to 147.10 (previous resistance), having said that, loss of near term upward momentum should prevent sharp move beyond 147.50-60 and price should falter below recent high at 148.10, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and we are looking to buy sterling on subsequent pullback as support at 145.15 should limit downside. Below 144.60-70 would defer and risk test of previous resistance at 144.20, break there would abort and signal a temporary top is formed, bring correction of recent rise to 143.90-00 but support at 143.30 should remain intact.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

Trade Idea: EUR/JPY – Buy at 127.00

EUR/JPY - 128.90

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term up

Original strategy:

Buy at 127.00, Target: 129.00, Stop: 126.40

Position: -

Target: -

Stop: -

New strategy :

Buy at 127.00, Target: 129.00, Stop: 126.40

Position: -

Target: -

Stop:-

Although the single currency has continued edging higher after resuming recent upmove and further gain to 129.50-60 cannot be ruled out, loss of near term upward momentum should prevent sharp move beyond psychological resistance at 130.00, risk from there has increased for a retreat to take place later. Below 128.00-05 would suggest a minor top is formed, bring correction to 127.40-50 but renewed buying interest should emerge around 127.00, bring another rise later.

In view of this, we are looking to reinstate long on pullback as 127.00 should limit downside. Below support at 126.49 would defer and suggest top is possibly formed, risk correction to 126.00 and later towards 125.40-50.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).