Sample Category Title

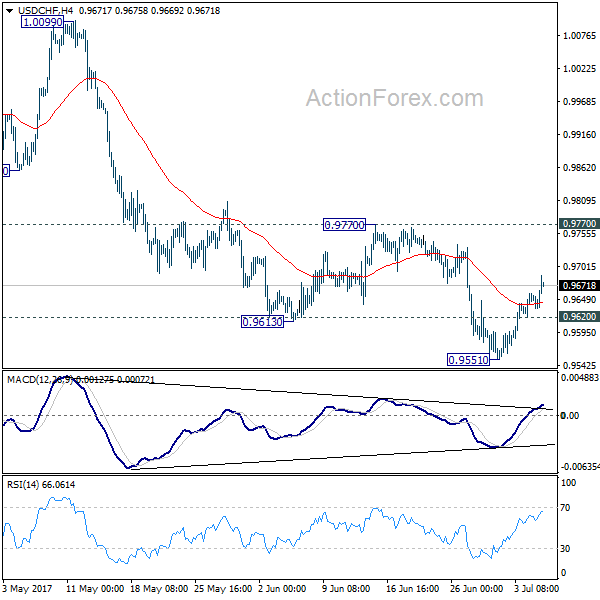

Trade Idea Update: USD/CHF – Buy at 0.9600

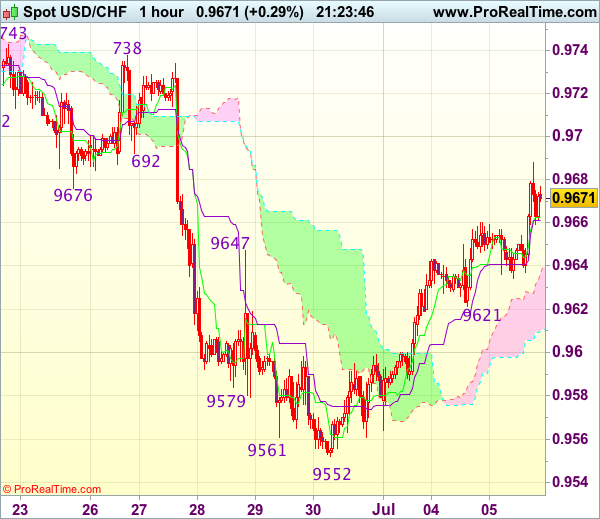

USD/CHF - 0.9673

Original strategy :

Buy at 0.9600, Target: 0.9700, Stop: 0.9565

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9600, Target: 0.9700, Stop: 0.9565

Position : -

Target : -

Stop : -

As the greenback has maintained a firm undertone after staging a strong rebound from 0.9552 (last week’s low), retaining our view that a temporary low has been formed there and consolidation with mild upside bias is seen for this move to bring retracement of recent decline, hence gain to 0.9690-00 is likely, however, reckon upside would be limited and price should falter below resistance area at 0.9738-43, bring retreat later.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback as 0.9600 should limit downside and bring another rise later. Below 0.9565-70 would abort and signal intra-day top is formed, risk retest of 0.9552 first.

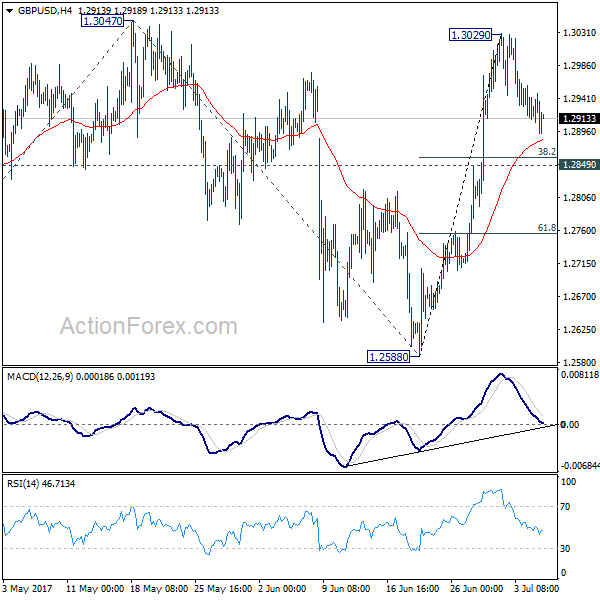

Trade Idea Update: GBP/USD – Buy at 1.2865

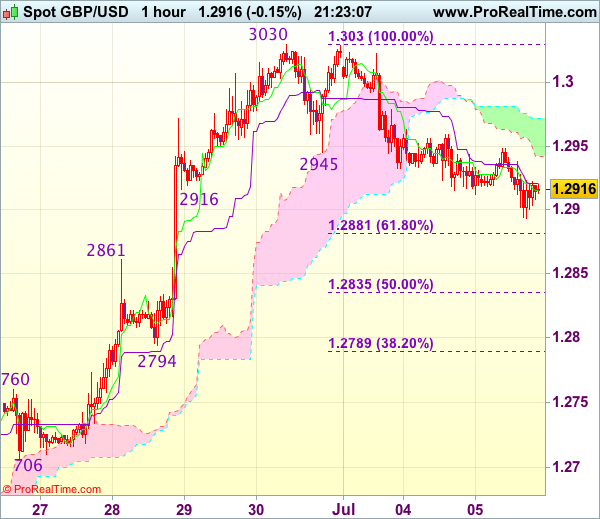

GBP/USD - 1.2905

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2925

Kijun-Sen level : 1.2931

Ichimoku cloud top : 1.2976

Ichimoku cloud bottom : 1.2956

Original strategy :

Buy at 1.2865, Target: 1.3000, Stop: 1.2830

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2865, Target: 1.3000, Stop: 1.2830

Position : -

Target : -

Stop : -

Although the British pound has remained under near term downward pressure and initial downside risk remains for the corrective fall from 1.3030 (last week’s high) to bring retracement of recent upmove to 1.2880-85 (38.2% Fibonacci retracement of 1.2640-1.3030), reckon downside would be limited to 1.2865-70 and bring another upmove later, above 1.2960 would signal low is formed, bring rebound to 1.3000 but break of said resistance at 1.3030 is needed to signal recent upmove has resumed and extend further gain towards recent high 1.3048.

In view of this, we are looking to buy cable again on further corrective fall as previous resistance at 1.2861 should turn into support and contain downside, bring another rise. Below 1.2830-35 (50% Fibonacci retracement of 1.2640-1.3030) would abort and signal top is formed, bring further fall towards support at 1.2794.

Trade Idea Update: EUR/USD – Buy at 1.1290

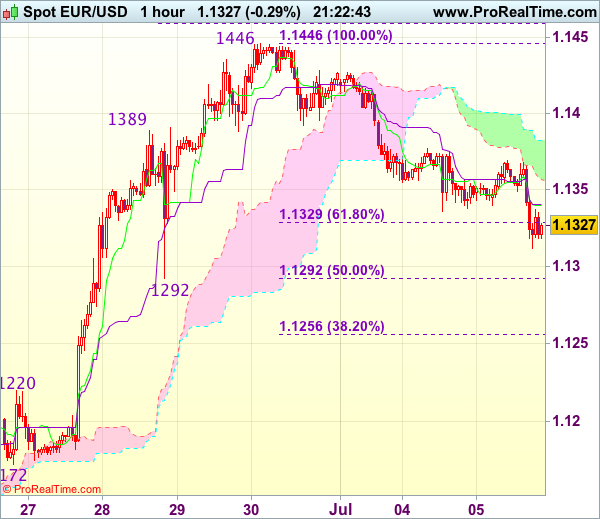

EUR/USD - 1.1321

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1359

Kijun-Sen level : 1.1357

Ichimoku cloud top : 1.1390

Ichimoku cloud bottom : 1.1366

Original strategy :

Buy at 1.1300, Target: 1.1400, Stop: 1.1265

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1290, Target: 1.1390, Stop: 1.1255

Position : -

Target : -

Stop : -

As the single currency has slipped again after brief recovery, suggesting near term downside risk remains for the fall from 1.1446 (last week’s high) to bring retracement of recent upmove, hence weakness to 1.1292 (previous support as well as 50% Fibonacci retracement of 1.1139-1.1446) cannot be ruled out, however, reckon sharp fall below there should not be repeated today and bring rebound later, above 1.1375-80 would signal an intra-day low is formed, bring test of 1.1400-10, break there would suggest the pullback from 1.1446 has ended, then retest of this resistance would follow.

In view of this, we are inclined to buy euro on further corrective fall as 1.1292 (previous support as well as 50% Fibonacci retracement of 1.1139-1.1446) should limit downside, bring rebound. Below 1.1270 would abort and signal a temporary top is formed, bring correction to 1.1250-55 (61.8% Fibonacci retracement) first.

Trade Idea Update: USD/JPY – Buy at 112.85

USD/JPY - 113.57

Original strategy :

Buy at 112.85, Target: 113.85, Stop: 112.50

Position : -

Target : -

Stop : -

New strategy :

Buy at 112.85, Target: 113.85, Stop: 112.50

Position : -

Target : -

Stop : -

As the greenback has continued trading with a firm undertone, adding credence to our view that recent upmove has resumed and bullishness remains for further gain to 113.75-85 but loss of momentum should prevent sharp move beyond 114.00, risk from there is seen for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback but one should exit on next rise. Below 112.60 would suggest top is possibly formed, bring weakness to 112.35-40 but break there is needed to confirm, bring correction to 111.90-95 and later towards 111.73 support.

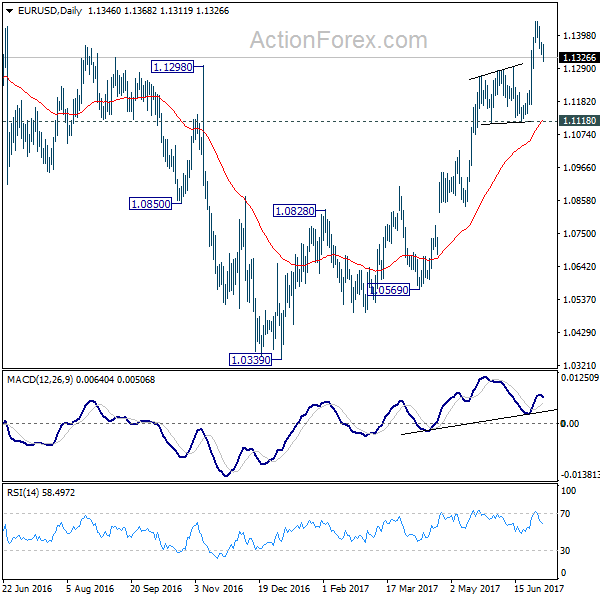

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1327; (P) 1.1352 (R1) 1.1368; More.....

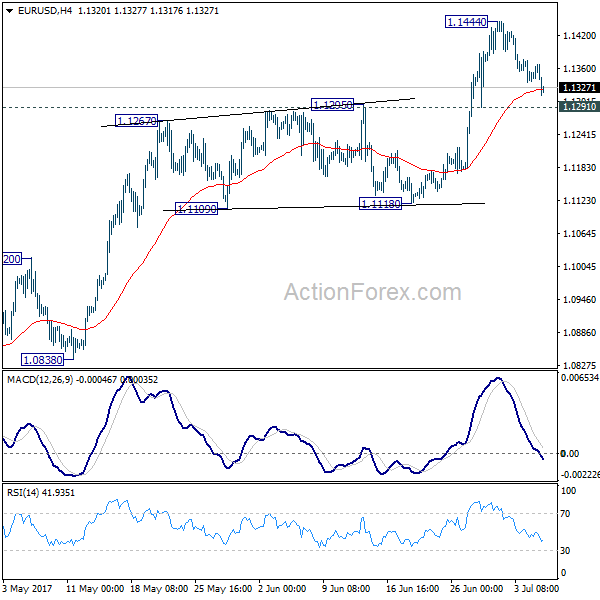

EUR/USD's pull back from 1.1444 extends lower today. But still, it's seen as a corrective move and the pair is staying above 1.1291 support. Intraday bias remains neutral first. Break of 1.1444 will extend the rally from 1.0339 low to 1.1615 resistance next. Meanwhile, break of 1.1291 will turn focus back to 1.1118 support.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1776). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2900; (P) 1.2929; (R1) 1.2946; More...

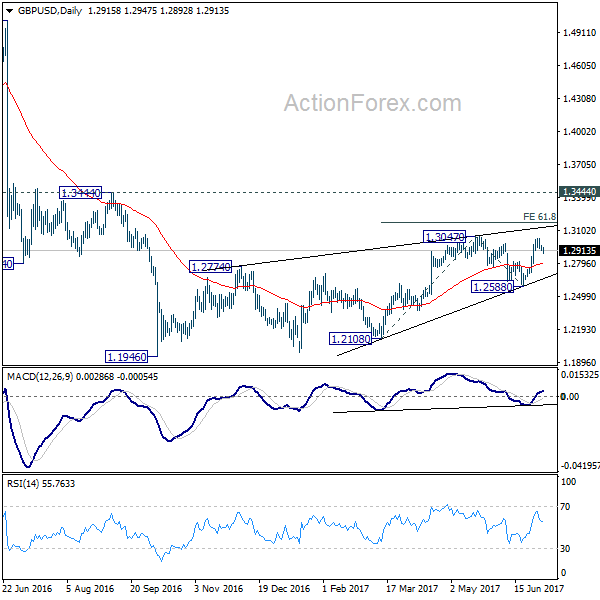

No change in GBP/USD's outlook as price actions from 1.3029 are seen as a corrective pattern. Intraday bias remains neutral first. While deeper retreat cannot be ruled out, downside should be contained above 1.2849 support to bring rise resumption. Break of 1.3029 should then send GBP/USD through 1.3047 to 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 next.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is now in favor, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

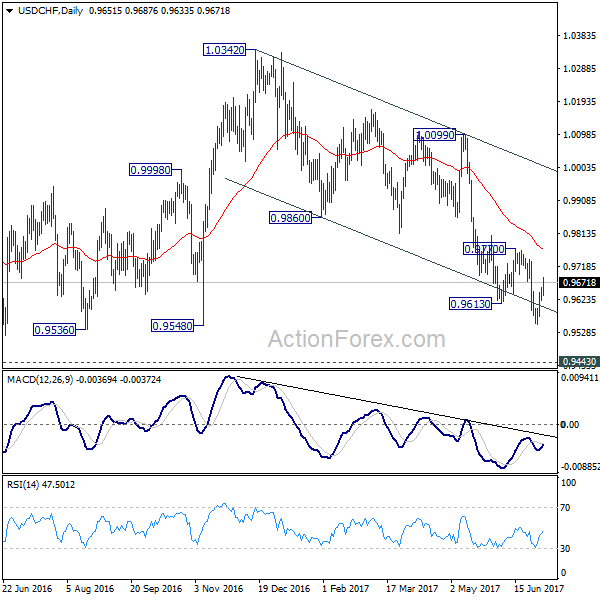

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9630; (P) 0.9644; (R1) 0.9668; More......

USD/CHF's recovery from 0.9551 extends today but it's staying well below 0.9770 resistance. Price actions from 0.9551 are viewed as a corrective pattern and intraday bias remains neutral. Outlook will stay bearish as long as 0.9777 resistance holds. Below 0.9620 minor support will turn bias back to the downside first. Further break of 0.9551 will extend the decline from 1.0342 to 0.94443 key support level. At this point, we'd expect strong support from there to bring rebound. Meanwhile, break of 0.9777 will now indicate short term reversal, on bullish convergence condition in 4 hour MACD.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

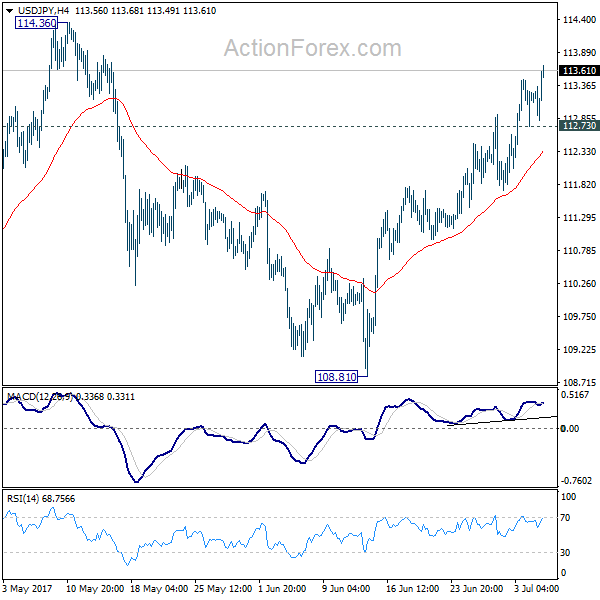

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.85; (P) 113.14; (R1) 113.57; More...

USD/JPY's rally continues today and hits as high as 113.58 so far. Intraday bias remains on the upside for 114.36 resistance next. Decisive break there will confirm our bullish view that corrective pull back from 118.65 has completed at 108.12. In that case, further rally would be seen to retest 118.65 next. On the downside, below 112.73 minor support will turn intraday bias and bring consolidation before staging another rally.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

Dollar Rebound Extends as Markets Await FOMC Minutes

Dollar's rebound extends today as markets are awaiting FOMC minutes. The key to watch is any hint on the next move of Fed. That is, whether Fed will hike rates in September and start shrinking the balance in December, or reverse. Or, Fed would indeed do nothing in September. Currently, fed fund futures are pricing in less than 20% chance of a September hike. Also, odds for federal fund rates to hit 1.25-1.50% and above in December is less than 60%. Technically, the greenback is staying near term bullish against Yen. But Dollar is holding below near term resistance against Euro, Sterling, Aussie and Canadian, and stays bearish.

"Triple-whammy" of disappointing UK PMIs

In UK, Services PMI dropped to 53.4 in June, down from 53.8, and missed expectation of 53.5. Markit chief business economist Chris Williamson noted that "a slowing in services sector growth completes a triple-whammy of disappointing PMI survey readings." And while "the three PMI surveys are running at levels that are historically consistent with GDP growing by around 0.4% in the second quarter, it's clear that the economy heads into the third quarter losing momentum." And he also said that it would be "surprise" to see BoE policy makers vote for a rate hike. And, "the current PMI reading would be more consistent with the Bank of England cutting interest rates rather than hiking." Also from UK, BRC shop price index dropped -0.3% yoy in June.

Nonetheless, markets still believed that BoE is closer than ever to have the first rate hike in the long time. The last time BoE raised interest rate was on July 5, 2007. Yes, that's exactly 10 years ago. Back then, BoE raised the bank rate by 25bps to 5.75%, on 6-3 vote. Recent comments from BoE Governor Market Carney and chief economist Andy Haldane suggest that the central bank will discuss stimulus exit in the coming months. Other BoE hawks are maintaining their stance in recent speeches. MPC member Michael Saunders, who voted for a hike last month, said today that "households should prepare for interest rates to go higher at some point." Another hawk Ian McCafferty said in a newspaper interview that on the balance of monetary policy, "there is a need for change". And a rate hike would be "justified" and "the prudent thing to do at this stage".

Eurozone PMI - Not the start of a slowdown

Eurozone services PMI was finalized at 55.4 in June, revised up from 54.7. Germany services PMI was finalized at 54.0, revised up from 53.7. France services PMI was also revised up to 56.9, from 55.3. However, Italy services PMI dropped to 53.6 in June. Overall, Eurozone PMI composite dropped to 56.3, down from 56.8. Markit noted that "the dip in the PMI in June certainly doesn't look like the start of a slowdown." And, "growth of new orders accelerated very slightly to reach the second highest in just over six years, and companies are struggling to satisfy this increase in demand."

ECB Governing Council member Benoit Coeure said today that "the Governing Council has not been discussing changes in our monetary policy that may come in the future." And recent market reaction to the hawkish comments from ECB President Mario Draghi was, according to Coeure, not very significant in the big picture. ECB chief economist Peter Praet said yesterday that ""underlying price pressures continue to be subdued." Praet called for patience regarding stimulus exit as "inflation convergence needs more time to show through convincingly in the data".

BoJ may lower inflation forecast this month

Reuters reported, quoting unnamed source, that BoJ will likely low inflation forecast for the current fiscal year ending March, 2018, in the upcoming meeting on July 19-20. And the inflation forecast for the next fiscal year might also be revised down. The sources noted that the economy was in good shape and BoJ might further upgrade the assessment. However, time is still needed for the positive effects to pus up prices. Nonetheless, the downward revision in inflation projections would possibly be minor, just reflecting recent softness in energy prices. At the April meeting, BoJ projected core inflation to hit 1.4% in the current fiscal year, and 1.7% in the next.

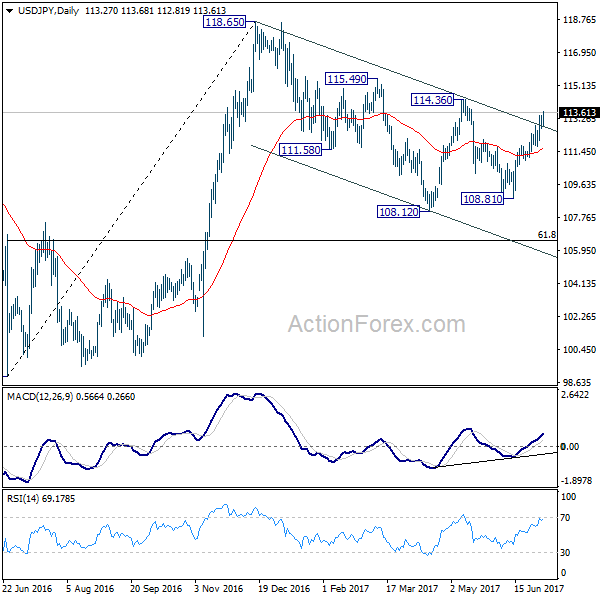

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.85; (P) 113.14; (R1) 113.57; More...

USD/JPY's rally continues today and hits as high as 113.58 so far. Intraday bias remains on the upside for 114.36 resistance next. Decisive break there will confirm our bullish view that corrective pull back from 118.65 has completed at 108.12. In that case, further rally would be seen to retest 118.65 next. On the downside, below 112.73 minor support will turn intraday bias and bring consolidation before staging another rally.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Jun | -0.30% | -0.40% | ||

| 1:45 | CNY | Caixin PMI Services Jun | 51.6 | 52.9 | 52.8 | |

| 7:45 | EUR | Italy Services PMI Jun | 53.6 | 54.6 | 55.1 | |

| 7:50 | EUR | France Services PMI Jun F | 56.9 | 55.3 | 55.3 | |

| 7:55 | EUR | Germany Services PMI Jun F | 54 | 53.7 | 53.7 | |

| 8:00 | EUR | Eurozone Services PMI Jun F | 55.4 | 54.7 | 54.7 | |

| 8:30 | GBP | Services PMI Jun | 53.4 | 53.5 | 53.8 | |

| 9:00 | EUR | Eurozone Retail Sales M/M May | 0.40% | 0.30% | 0.10% | |

| 14:00 | USD | Factory Orders May | -0.50% | -0.20% | ||

| 18:00 | USD | FOMC Meeting Minutes |

FOMC Minutes, Sterling and WTI in Focus

Wednesday's main risk event and potential market shaker will be the release of June's FOMC meeting minutes, which investors may closely scrutinize for clues on rate hike timings in the second half of 2017. With the Federal Reserve speakers repeatedly sending hawkish signals, the pending Fed minutes could follow a similar school of thought, potentially supporting the Greenback. Markets will also be paying very close attention to see if the minutes suggest that the recent fall in inflation is 'transitory' with suggestions of higher rates still on the cards, unless the US economy decelerates.

Investors will also be seeking insight over how and when the central bank plans to reduce its $4.5 trillion balance sheet, as the precise timing still remains a riddle. While the US Dollar could find support if Fed hawks make an appearance this afternoon, the upside may face headwinds as market participants maintain a cautious approach ahead of Friday's NFP data.

From a technical standpoint, the Dollar Index remains pressured on the daily timeframe. The first relevant resistance level can be located around 96.50 with bears eyeing 97.00 as a secondary level to attack.

Sterling pressured from all directions

It's quite thought provoking how today marks exactly ten years since the Bank of England raised UK interest rates. The last time the BoE's monetary policy committee raised rates by 25 basis points to 5.75% was on 05 July 2007. Since then, the financial crisis which followed compelled the central bank to cut interest rates to 0.5% over the following two years. Rates were cut once again to 0.25% in August 2016, in an effort to shield against the impacts of Brexit.

As the second half of 2017 gets underway, the negative impacts of Brexit can be reflected in the British Pound and domestic economic data. Uncertainty over Brexit has exposed the Sterling to heavy losses and this continues to fuel inflation. With rising inflation outpacing wage growth, consumers are feeling the pinch and as such, has raised questions over the sustainability of the UK's consumer driven economic momentum. Political risk at home has also added to the messy mix while uncertainty over the Brexit talks continues to encourage sellers to attack the Sterling at any given opportunity.

There have been discussions over the Bank of England raising UK interest rates in the coming months, with BoE governor, Mark Carney's hawkish remarks last week almost subliminally positioning markets for a surprise. While raising rates may control inflation, it could impact business confidence and even pressure consumers further. It will be interesting to see if the BoE surprises by raising UK interest rates in August and how the markets react.

From a technical standpoint, the GBPUSD is a risk of depreciating lower if bears can break below 1.2850.

Commodity Spotlight - WTI

WTI Crude was exposed to heavy losses on Wednesday after reports of Russia opposing any further supply cuts attracted a school of sellers to attack. It is becoming clear that the fundamental reason why oil prices have remained depressed for a prolonged period lies in the high global inventories. With the increasing output from Nigeria and Libya threatening to obstruct the efforts made by the rest of the group to rebalance the markets, oil could be in store for further pain moving forward. Price action currently suggests that the unyielding dynamic of the markets have disappointed investors who were initially optimistic about OPEC's output cuts providing a solution. WTI Crude could be vulnerable to further downside if bears break below $46.