Sample Category Title

Trade Idea: USD/CAD – Sell at 1.3170

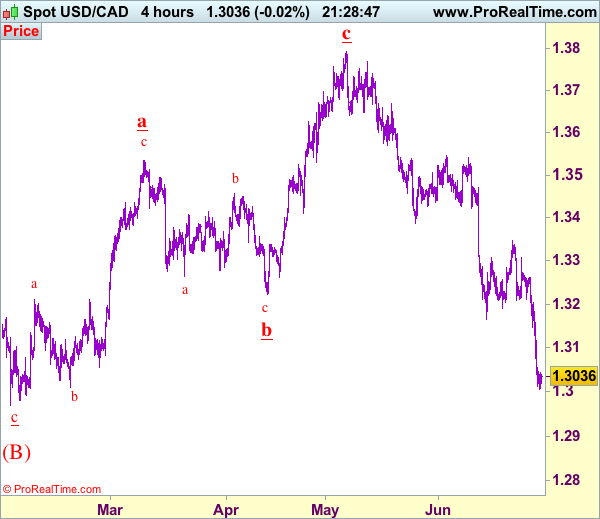

USD/CAD - 1.3038

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term down

Original strategy :

Sell at 1.3170, Target: 1.3020, Stop: 1.3230

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.3150, Target: 1.2980, Stop: 1.3210

Position: -

Target: -

Stop:-

As the greenback has remained under pressure after recent selloff, adding credence to our bearish count that the fall from 1.3794 top (wave c of larger degree wave b top) is still in progress and may extend further weakness to 1.2969, however, near term oversold condition should limit downside to 1.2940 and reckon 1.2900 would hold from here,risk from there has increased for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell the pair again on recovery as 1.3150-60 should limit upside. Above 1.3190-00 would defer and suggest low is formed, bring a stronger rebound to 1.3215-20 and possibly towards 1.3260-65 but only break there would abort and signal a temporary low is formed instead, then test of resistance at 1.3308 would follow.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Trade Idea Update: USD/CHF – Sell at 0.9645

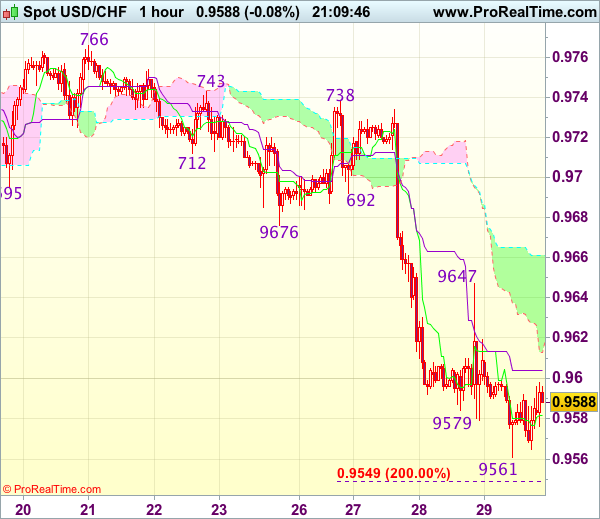

USD/CHF - 0.9589

Original strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

As the greenback has recovered after falling to 0.9561, suggesting minor consolidation would be seen and recovery to 0.9605-10 cannot be ruled out, however, reckon upside would be limited to resistance at 0.9647 and bring another decline, below said support at 0.9579 would signal the decline from 0.9771 top is still in progress and may extend weakness to 0.9545-50 (2 times extension of 0.9771-0.9676 measuring from 0.9738) but reckon downside would be limited to 0.9525-30 (50% projection of 1.10100-0.9613 measuring from 0.9771) and 0.9500 should hold, price should stay above 0.9470 (61.8% projection), bring rebound later.

In view of this, would not chase this fall here and we are looking to sell dollar on recovery as resistance at 0.9647 should limit upside. Only above previous support at 0.9676 (now resistance) would defer and suggest a temporary low is formed, risk test of another previous support at 0.9692.

Trade Idea Update: GBP/USD – Buy at 1.2895

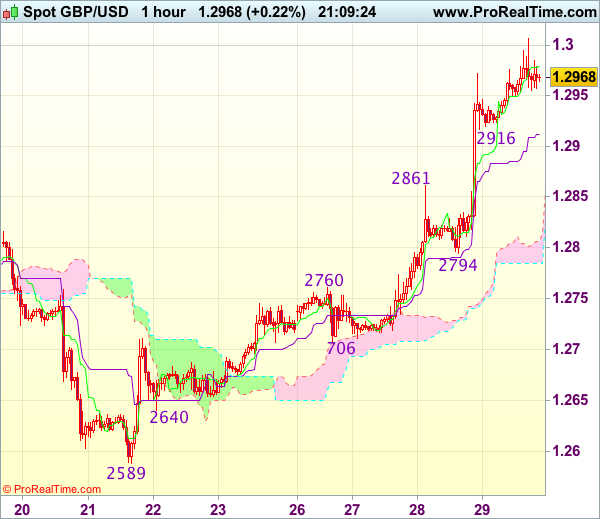

GBP/USD - 1.2976

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2964

Kijun-Sen level : 1.2895

Ichimoku cloud top : 1.2801

Ichimoku cloud bottom : 1.2784

Original strategy :

Buy at 1.2895, Target: 1.2995, Stop: 1.2860

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2895, Target: 1.2995, Stop: 1.2860

Position : -

Target : -

Stop : -

As cable has risen again after brief pullback, suggesting recent upmove is still in progress and may extend further gain to 1.3010-15, however, loss of near term upward momentum should prevent sharp move beyond previous resistance at 1.3048 and reckon 1.3075-80 would hold on first testing, risk from there has increased for a retreat to take place later.

In view of this, we are looking to buy cable again on pullback as 1.2895-00 should limit downside. Below previous resistance at 1.2861 would defer and suggest a temporary top is formed instead, risk weakness to 1.2830-35 but support at 1.2794 should remain intact.

Trade Idea Update: EUR/USD – Buy at 1.1320

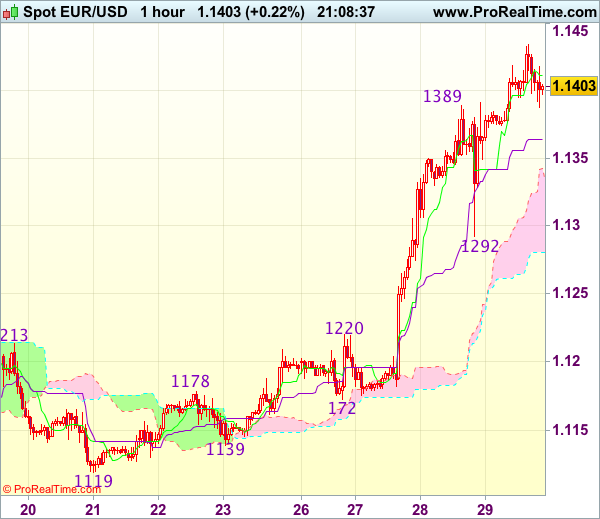

EUR/USD - 1.1408

Original strategy :

Buy at 1.1320, Target: 1.1420, Stop: 1.1285

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1320, Target: 1.1420, Stop: 1.1285

Position : -

Target : -

Stop : -

As the single currency has risen again after finding renewed buying interest at 1.1292,, suggesting recent rise is still in progress and may extend further gain to 1.1455-60 (61.8% projection of 1.1119-1.1389 measuring from 1.1292), then 1.1480, however, overbought condition should prevent sharp move beyond 1.1500, risk from there has increased for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy euro on pullback, below the Kijun-Sen (now at 1.1360) would bring correction to 1.1315-20 but said support at 1.1292 should remain intact, bring another rally later.

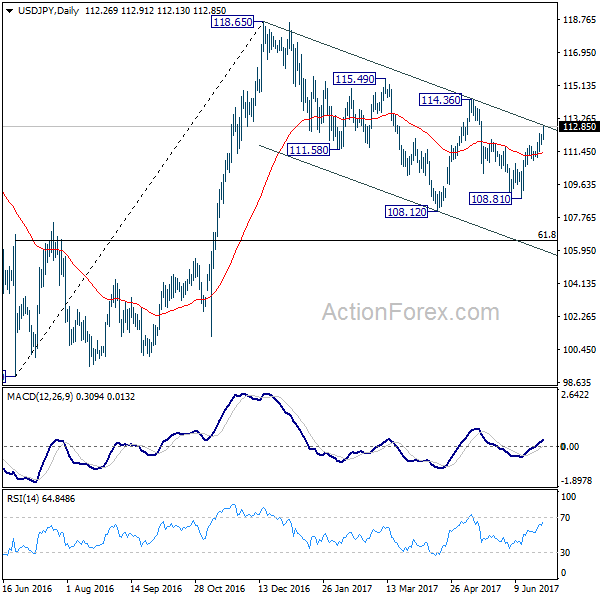

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.96; (P) 112.18; (R1) 112.55; More...

USD/JPY rises to as high as 112.91 in early US session and touching near term channel resistance. Intraday bias stays on the upside. Sustained break of the channel will argue that whole pull back from 118.65 has completed at 108.12 already. In such case, further rise should be seen to 114.36 resistance for confirmation. On the downside, below 111.82 minor support will turn bias neutral first. If that happens, we'll assess the near term outlook alter.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Trade Idea Update: USD/JPY – Buy at 112.40

USD/JPY - 112.87

Original strategy :

Buy at 111.90, Target: 112.90, Stop: 111.55

Position : -

Target : -

Stop : -

New strategy :

Buy at 112.40, Target: 113.40, Stop: 112.05

Position : -

Target : -

Stop : -

The greenback has continued trading with a firm undertone after this week’s rally on active cross-selling in yen, adding credence to our bullishness and signal the rise from 108.82 low is still in progress, hence further gain to 113.00 would be seen, however, near term overbought condition should prevent sharp move beyond 113.40 and price should falter below 113.75-80, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback as 112.40 should limit downside. Below 112.10-15 would suggest an intra-day top is formed, bring correction towards 111.83 support.

Dollar Stabilizes Mildly But Stays Bearish, Yen Selloff Continues

While yen's free fall continues in early US session, Dollar stabilizes mildly. Economic data from US are supportive. Initial jobless claims rose 2k to 244k in the week ended June 24. That's the 121 straight week of sub-300k reading. Four week moving average dropped 2.75k to 242.25k. Continuing claims rose 6k to 1.948m in the week ended June 17. It stayed below 2m mark for 11 straight week. Q1 GDP growth was revised up to 1.4% annualized, from 1.2% annualized. GDP price index was revised down to 1.9%, from 2.2%. Overall, there is no sign in bottoming in the greenback yet and it's still vulnerable to further selloff against Euro, Sterling, Franc, Canadian and Australian. For the week so far, Sterling is the strongest, followed by Euro and then Canadian.

BoE Haldane: Need to look seriously at raising rate

In UK, BoE chief economist Andy Haldane said today that the central bank needs to "look serious at the possibility of raising interest rates to keep the lid of those cost of living increases". He noted that "for now we are happy with where the rates are", but "we need to be vigilant for what happens next". BoE's monthly report on money and credit showed that unsecured consumer credit rose by 10.3% yoy in May, five times as fast as earnings growth. The GBP 1.7b growth in May alone was faster than the average of GBP 1.5b average in the past six months. That is seen by economists as another reason for BoE to raise interest rates, to curb consumer lending. Released from UK, mortgage approvals was unchanged at 65k in May.

ECB expected to announce tapering in September or October

ECB's current EUR 60b per month asset purchase program will end by the end of the year. Markets are now expecting the central bank to announce tapering in September, by latest October. Some expect the tapering to last for a year till December 2018. Meanwhile, opinions on the timing of ECB's first rate hike various. According to a Reuters survey, 90% of currency traders expected a hike in the first quarter of 2018. But some expect that to happen in early 2019.

Sentiment indicators in Eurozone generally improved. Business climate rose to 1.15, up from 0.9, beat expectation of 0.93. Economic confidence rose to 111.1, up from 109.2, beat expectation of 109.5. Industrial confidence rose to 4.5, up from 2.8, beat expectation of 2.8. Services confidence rose to 13.4, up from 13.0, beat expectation of 13.4. Consumer confidence was finalized at -1.3. Released from Germany, CPI rose 0.2% mom, 1.6% yoy in June, up from prior -0.2% mom and 1.5% yoy, beat expectation of 0.0% mom, 1.4% yoy. Gfk consumer confidence rose to 10.6, above consensus of 10.4.

BoJ Harada: Too early to do anything

BoJ board member Yutaka Harada said today that a weaker yen will stimulate the economy and accelerate inflation. Meanwhile, if the 2% inflation target comes into sight, BoJ might reduce or even top ETF purchases. However, for the moment, it's still too early to do anything as inflation is far off the target. On the other hand, Harada believes the current stimulus is "already sufficiently bold" and he's confident that inflation will gradually approach 2%. Released from Japan, retail sales rose 2.0% yoy in May,

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.96; (P) 112.18; (R1) 112.55; More...

USD/JPY rises to as high as 112.91 in early US session and touching near term channel resistance. Intraday bias stays on the upside. Sustained break of the channel will argue that whole pull back from 118.65 has completed at 108.12 already. In such case, further rise should be seen to 114.36 resistance for confirmation. On the downside, below 111.82 minor support will turn bias neutral first. If that happens, we'll assess the near term outlook alter.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y May | 2.00% | 2.80% | 3.20% | |

| 01:00 | NZD | ANZ Business Confidence Jun | 24.8 | 14.9 | ||

| 06:00 | EUR | German GfK Consumer Confidence Jul | 10.6 | 10.4 | 10.4 | |

| 08:30 | GBP | Mortgage Approvals May | 65K | 64K | 65K | |

| 09:00 | EUR | Eurozone Business Climate Indicator Jun | 1.15 | 0.93 | 0.9 | |

| 09:00 | EUR | Eurozone Economic Confidence Jun | 111.1 | 109.5 | 109.2 | |

| 09:00 | EUR | Eurozone Industrial Confidence Jun | 4.5 | 2.8 | 2.8 | |

| 09:00 | EUR | Eurozone Services Confidence Jun | 13.4 | 12.8 | 13 | |

| 09:00 | EUR | Eurozone Consumer Confidence Jun F | -1.3 | -1.3 | -1.3 | |

| 12:00 | EUR | German CPI M/M Jun P | 0.20% | 0.00% | -0.20% | |

| 12:00 | EUR | German CPI Y/Y Jun P | 1.60% | 1.40% | 1.50% | |

| 12:30 | USD | GDP (Annualized) Q1 T | 1.40% | 1.20% | 1.20% | |

| 12:30 | USD | GDP Price Index Q1 T | 1.90% | 2.20% | 2.20% | |

| 12:30 | USD | Initial Jobless Claims (JUN 24) | 244K | 240K | 241K | 242K |

| 14:30 | USD | Natural Gas Storage | 61B |

Spot Gold Returned Below Daily Cloud

Spot Gold returned below daily cloud after the third continuous strong rejection at $1253 resistance zone.

Three daily candles with long upper wicks weigh on near-term structure, after rallies repeatedly failed to close above cracked 100SMA ($1249).

Near-term bias shifts lower on fresh bearish acceleration that pressures support at $1241 (lows of 27/21 June) and may extend lower for retest of key near-term support at $1236 (26 June low / 200SMA).

Newly created 10/100SMA bear-cross maintains fresh bearish pressure, with today's close below daily cloud to confirm negative stance.

Cloud is spanned between $1246/49 and now acts as resistance, guarding upside rejection levels and upper pivots at $1253/54.

Alternative scenario requires close above daily cloud and regain of $1253/54 barriers to re-open key barrier at $1258 (Fibo 38.2% of $1296//$1236 descend / 55SMA / double upside rejection).

Res: 1246; 1249; 1254; 1258

Sup: 1243; 1241; 1236; 1230

EUR And GBP Extend Gains On Tightening Expectation

Thursday may not be dominated by appearances from prominent central bankers like the previous two were but we're continuing to see markets focus on what's been said, with the euro and sterling both pushing higher again.

An apparent acceptance by the heads of the UK and European central banks that tighter monetary policy may be appropriate in the not too distant future is once again supporting the currencies this morning, with the euro having hit fresh 13-month highs against the dollar and the pound rising above 1.30 briefly, also against the greenback.

It's clear that both Mario Draghi and Mark Carney aren't entirely behind the idea that monetary policy should be tightened any time soon but comments in recent days appear to suggest they're reluctantly accepting the growing consensus within their central banks and preparing markets for a potential move. I still believe that a further reduction in bond buying from the ECB is much more likely than a rate hike from the Bank of England this year but given how markets were positioned on the latter only a couple of weeks ago, the market response is probably appropriate.

While the euro now looks likely to add to its gains in the coming weeks - with 1.16 being the next key technical level once 1.1425-1.1450 is overcome – the new found bullishness in the pound will be tested, with 1.30 against the dollar representing a big psychological test. We did briefly breach this level in the middle of May but the move failed to generate any real momentum and fell back towards 1.26 in the following weeks. There does appear to be more momentum with the move on this occasion which could aid the push but the pair did fail at the first time of asking this morning.

The absence of central bankers today will put more focus back on the data today, with the final revision of US first quarter GDP being released, alongside jobless claims. With investors already doubting whether the Fed will raise rates again this year, it will be interesting to see how they respond should we get a downward revision in the first quarter figure.

Are Hawks Really Back In Town?

The global currency markets were volatile and painfully unpredictable during Wednesday's trading session, with power pairs causing havoc as central bank heavyweights defied market expectations by sounding rather hawkish. Euro bulls rampaged while Sterling received a new lease of life followingspeculation that Europe and Britain's central banks areplanning to end an era of easy money. While the foreign exchange markets remained chaotic, the prospect of central banks scaling back monetary policiessupported risk sentiment. Asian shares marched higher during Thursday's trading session following Wall Street's impressive rebound as participants rediscovered their confidence over the global economy.

Sterling/Dollar clips 1.3000

Sterling staged a market-shaking rebound on Wednesday, with the upside invading Thursday's trading session after Bank of England Governor Mark Carney dished out a hawkish surprise. Bullish investors were swift in gobbling up Carney's hawkish remarks that 'some removal of stimulus is likely to become necessary' to send the GBPUSD towards 1.3000. While Sterling is likely to edge higher in the short term as investors overlook Brexit-related uncertainty and daydream over the possibility of higher rates, I still believe the upside remains limited.

It should be kept in mind that it was only last week that Carney stated that 'now was not yet the time' to raise interest rates. While raising interest rates may put a lid on inflation, it has the ability to negatively impact the fragile UK economy while also denting business confidence and pressuring consumers. Will the Bank of England raise interest rates while the UK economy is battling ongoing Brexit woes? Time will tell

EURUSD hits yearly high

I find it quite interesting how at the start of 2017 it was all about the EURUSD parity dream as political uncertainty in Europe and a Trump-fueled Dollar rally left the currency vulnerable to heavy losses. Six months later, the absence of political risk in Europe, a Dollar that lacks attitude and QE tapering speculations have sent the EURUSD to a yearly high at 1.1435. Although ECB sources attempted to quell the heated taper expectations on Wednesday, price action currently suggests that investors remain optimistic over the ECB scaling back monetary policy in the future. From a technical standpoint, the EURUSD is heavily bullish on the daily charts. The breakout above 1.1400 could encourage a further incline higher towards 1.1500.

Dollar sulks in the background

The Dollar tumbled to a new year-low on Thursday after a delayed healthcare bill vote heavily weighed on the prospects for tax cuts and infrastructure spending. With the IMF’s growth downgrade for the US economy shattering any surviving remnants of the Trump rally, the Dollar remains exposed to further downside losses. Although Fed policymakers remain optimistic over the health of the US economy the IMF and investors think otherwise and such can be reflected in the bearish price action of the Dollar Index. Who would have thought that after eight months the Dollar would relinquish its Trump rally gains and then some?

Participants may direct some of their attention towards the pending Final US GDP for Q1which could make or break the Dollar further this afternoon.From a technical standpoint, the Greenback is heavily pressured on the daily charts and the breakdown below 96.00 should encourage a decline towards 94.00.