Sample Category Title

Pound Breaks Above 1.30 Line on Carney Comments

GBP has posted gains for a third straight day as the pound has moved higher on Thursday. In North American trade, GBP/USD is up 0.47%, trading at 1.2980. Earlier in the day, the pound punched above the 1.30 line, which had held in resistance since May 25. On the release front, British Net Lending to Individuals jumped to GBP 5.3 billion, well above the forecast of GBP 4.0 billion. In the US, Final GDP came in at 1.4%, above the forecast of 1.2%. Unemployment claims rose to 144 thousand, higher than the forecast of 141 thousand. We could see some movement from the pound on Friday, as the UK releases Current Account and Final GDP. The US will publish UoM Consumer Sentiment.

The pound has jumped 1.9% this week, buoyed by comments from BoE Governor Mark Carney at the ECB forum of central bankers. Carney said that the BoE would have to consider removing monetary stimulus, and the markets jumped on his comments as a possible sign that he was not adamantly opposed to rate hikes in the near future. BoE policymakers have waged a public debate about rate policy, with Carney stating last week that he was opposed to hikes, only to be contradicted by MPC member Ande Haldane, who said he had been close to voting in favor of a rate hike at the June rate meeting. The vote at the meeting was 5-3 in favor of maintaining rates, surprising the markets, which had predicted a 7-1 vote to keep rates at current levels. Although there are renewed fears that Brexit will take a toll on the British economy, inflation is running close to 3%, well above the BoE's target of 2 percent. A rate increase would help lower inflation, but Carney, who has voiced concerns about Brexit's negative ramifications since the vote last June, has been solidly against a rate increase.

In the UK, more and more consumers are taking out loans, and that has the Bank of England worried. With wage growth at weak levels and the pound at low levels, the British consumers have seen their purchasing power reduced, with many resorting to unsecured loans. This has led to calls for the BoE to respond with a rate hike in September, in order to curb borrowing levels. Proponent of a rate hike also point to high inflation, which is running at a 3% clip. The BoE cut rates to 0.25% in August 2016, in response to the stunning Brexit vote, which the BoE warned would take a heavy toll on the economy. Those dire warnings are yet to materialize, and Carney faced heavy criticism for is overly-negative forecast. With more BoE policymakers calling for a rate hike, Carney may have to acquiesce and press the rate trigger before the end of the year.

US GDP Lends Dollar a Temporary Lift; Euro’s Strength Unfolds

As the European trading session was coming to a close, the forex market reacted to a string of data releases. The dollar was helped by a positive revision of the first-quarter US GDP, though the gains didn't last long. Upbeat data out of the eurozone helped the euro maintain its positive trend.

The US economy grew at a better pace than initially estimated in the first quarter on the higher consumer spending and a jump in exports. The first quarter GDP growth, quarter-on-quarter, was revised to 1.4% (against the preliminary number of 1.2%). The positive revision lifted the greenback against the yen, though shortly after, the dollar was under pressure, losing all its earlier gains. At 112.58, the pair is still trading at a one-month high.

The upbeat GDP revision offered little support to the dollar index that stayed at a nine-month low around 95.80.

The eurozone business and consumer sentiment is the strongest in a decade based on the European Commission survey that was released today. The economic sentiment index rose to 111.1 in June from 109.2 in May, and above expectations of 109.5. The barometer for Germany, France and the Netherlands rose strongly. The Gfk German Consumer Climate also signaled strong consumer confidence in Germany, as the index rose to 10.6 for July (above the expected and prior month's level of 10.4) and the highest level since 2001. Additionally, preliminary German HICP for June showed rising inflation, up 0.2% year-on-year, above the prior month's 0.2% decline.

The strong HICP data supported the euro against the dollar during the European trading session. However, euro/dollar was under some pressure later in the session on the positive data out of the US. The pair was last trading at 1.1412.

In the absence of data releases, the pound continued building on the earlier gains against the dollar, following the more hawkish tone by the BoE Governor the previous day. Pound/dollar was last trading at 1.2987.

Oil prices continued building on the earlier positive momentum, rising to a two-week high. US government data showed on Wednesday that domestic crude production dropped by 100,000 barrels per day to 9.3 million last week. WTI was last trading at $45.30 a barrel as the European markets were coming to a close. However, there are concerns that this reduction is temporary on Tropical Storm Cindy in the Gulf of Mexico and maintenance in Alaska, implying that the price may be pressured as output rises again.

Negatively correlated to the greenback, gold has been pressured in late European session as the dollar rose against the yen, but the yellow metal managed to regain some its lost momentum. The commodity was last trading at $1,244.46 an ounce.

Investment Theme – Tale of Two Continents as Dollar Heads for a Chill Summer and Sun May Shine on...

The dollar weakening might further unfold in the coming months amid the latest economic and political concerns. Investors' are increasingly worried that many of the promises President Trump made during his presidential campaign will not be materialized. The greenback has fallen 4% against the yen since the beginning of the year, while the dollar index is down 6%.

The assurances of big tax cuts, massive infrastructure spending and deregulation that President Donald Trump gave during his presidential campaign are being questioned after the Senate Majority Leader, Mitch McConnell, on Tuesday delayed a vote on legislation to repeal the Affordable Care Act. Amid the resistance from Republican senators, there is not enough support to even start the debate on the bill. In fact, the bill has had a patchy path to get to the Senate, as it got a very narrow approval in the House of Representatives at the beginning of May.

This signals a potentially difficult path for the President's remaining plans, most importantly the tax reform one. After the surprising win in the November elections, the greenback and the US equity markets priced in all of Trump's promises. However, considering the current situation, equities and the dollar might be somewhat overvalued and heading for a correction.

Recent data out of the US has been on the soft side and the absence of the proposed fiscal spending stimulus is not helping spur the lost growth momentum. More so, the IMF has recently downgraded the expected US GDP growth for the next couple of years.

There is little to suggest that the US economy is about to hit a turmoil, especially with the tight labour market, though a more tepid growth period might be expected. Some of the data to be released this week, such as the first quarter GDP growth and core PCE for May might signal the latest economic situation. Poor data readings may cause an immediate weakening of the greenback.

Trump's campaign promises also inflated investors' hopes of a faster pace of rate increases by the Fed due to the potential stronger economic growth. However, the expectations that the Fed will raise rates during the September or December meeting have been diminishing. The Fed fund futures imply an 18% probability for the September rate hike and below 50% for the December meeting.

Overall, the possibility of the dollar strengthening further is getting slimmer by the day. While some daily dollar/yen gains might be expected throughout the summer, a big comeback for the pair to maintain an upward momentum above the 113 handle is looking unlikely.

By contrast, the euro's rally following the receding threat of deflation, according to European Central Bank President Mario Draghi, has turned the eurozone currency to one of this year's best performing against the US dollar. Euro/dollar pair broke above the 1.14 handle, with some analysts expecting the pair to go above the 1.16 handle.

The improving economic growth, rising inflation and a reduction in the unemployment rate are supporting the euro in the medium-to-long-term. Additionally, the currency should get a lift if the planned labour reforms by the newly elected French President go through.

By contrast to the US, political risks in the eurozone have largely dissipated. The focus is on the German elections in September, with the latest poll showing that Angela Merkel's conservative party has the highest support since September 2015.

Considering all the above, the strength of the forex market might be on the side of the old continent, as the euro gains against the greenback. Very slow to non-existing movement in the proposed reforms by President Trump could cause the dollar to weaken further during the second half of the year. In the unlikely event of the US tax code getting an overhaul this year, the dollar has an upside potential against the yen.

EUR/USD Rally Slows. USD/JPY Gains on Higher Core Yields

- The positive equity sentiment in Asia failed to translate into sustained gains in Europe. After a limited upturn, equities turned south with losses amounting to well over 1%. American shares also opened slightly lower with especially NASDAQ taking the punches (-0.75%).

- Yields on sovereign bonds rose amid growing expectations that policymakers on both sides of the Atlantic will begin to ease off on stimulus measures more quickly than some market participants had expected

- German inflation unexpectedly accelerated to 0.2% M/M in June while the consensus expected a stabilisation. The Y/Y rise was 1.5% compared to the 1.3% consensus. The key boost came from services inflation which jumped to 1.7% (1.2% in May). The timing of a holiday played also a role. Spanish inflation dropped to a 7-month low of 1.6% Y/Y.

- The EC measure for euro-area economic confidence jumped to the highest level in a decade. The index of business and consumer sentiment rose to 111.1 in June from 109.2 in May and compared to a consensus of 109.5. Gauges for Germany, France and the Netherlands rose strongly while Spain was up slightly and Italy remained unchanged.

- UK consumer credit continued to grow strongly in May, underlining why BoE officials took action this week to protect banks against a debt bubble. Net consumer credit rose by £1.7 bn, above the £1.5bn in April and consensus of £1.4bn. New mortgage approvals and the amount of housing lending were also higher than expected.

- The US economy grew at a swifter pace in the Q1 than first thought, according to a third GDP-reading of 1.4% annualised qoq. Although this reading is still down from the 2.1% in the Q4 of 2016, it is a step up from the first estimate of 0.7%, and the second of 1.2%. The correction came thanks to the upward revised personal consumption.

- German chancellor Merkel threw down the gauntlet to US president Trump and pledged to fight at next week's G20 summit in Hamburg for free trade, international cooperation and the Paris climate change accord. She also stuck to her recent approach of downplaying the importance of Brexit for the rest of the EU.

- US Initial jobless claims inched up 2k to 244k last week, which followed a slight upward revision to the previous week of 242k (initially reported as 241k). The increase was larger than the consensus expectation of 240k. Despite the rise, the level of jobless claims is still very low.

Rates

The genie is out of the bottle: Yields extend up-leg

Core bonds can't find their composure after several central banks amongst others the ECB and BoE suggested in recent days that the era of the unlimited liquidity providing is running to an end. The repositioning in various markets on this CB expectation isn't finished and overwhelms the traditional strong run of bonds at quarter end. The Bund opened weak and resumed its descent in the afternoon. Technically, the Bund took out an uptrendline at 162.86 and the 50% retracement from 158/89 to 165.93, which attracted technically-oriented seller. Major support comes closer at 161.68 (neckline double top). European equities weakened hand in hand with the Bund and the rise of EUR/USD. The typical inverse relationship between weakness in European equities and strength in Bunds is clearly a thing of the past. The causation might be going from the Bund (and euro) to equities, at least for now. An additional factor that weighted on bonds was an upward surprise in German inflation, which should be reflected in a higher EMU inflation figure tomorrow. It gives the ECB more incentive to be leaning towards starting tapering in a few months' time, especially as the economic confidence, released today, improved sharply further.

In a daily perspective, the German yield curve steepened with yields between 0.8 bps (2-yr) and 6.9 bps (10-yr) higher. The US yield curve steepened with yield changes ranging between +1.2 bps (2-yr) and +4.9 bps (30-yr). Worth watching, the German 10-yr yield rose 20 bps in past three sessions and nears key resistance at 0.50%. On intra-EMU bond markets, yield spreads versus Germany were marginally lower with an outperformance of Greece (13 bps). Higher core yields haven't impacted peripheral bonds yet.

Currencies

EUR/USD rally slows. USD/JPY gains on higher core yields

Today, the impact of Tuesday's Draghi comments on the euro eased even as volatility in (some) other markets remained higher than was the case of late. EUR/USD set a minor new high this morning but returned to the 1.14 area even as EMU data were strong. USD/JPY gained further on higher core yields and ignored a loss of momentum on (European) equity markets. A decline of the yen in a risk-off environment: How far will this trade go?

Overnight, Asian equities went higher in the slipstream of WS. The dollar remained on the defensive. EUR/USD touched a new correction top north of 1.14. USD/JPY still didn't profit from the broad equity rebound. The pair stabilized in the 112.25 area.

European markets initially didn't know which card to play. European equities opened in positive territory, but the gains evaporated almost immediately. The strong euro weighed. EUR/USD gained further ground as the first German regional inflation data came stronger than expected. EUR/USD set a minor new correction top in the 1.1435 area. Interest rate differentials were an insignificant factor (2 year spreads US/Germany were little changed, 10-y spreads narrowed, but only slightly). Finally, the post-Draghi rally ran into resistance. The EC confidence data were also very strong, but caused no further euro gains. Some modest profit taking kicked in.

Remarkably, after a rather poor performance of late, USD/JPY trended further north despite a poor equity performance in Europe. Wider LT US/Japan spreads outweighed the risk-off sentiment. It has been quite some time since we last saw this kind of 'interest rate driven' yen weakness.

The US eco data (claims and final GDP) brought no big news. Equity sentiment deteriorated further. However, there was no straight forward impact on the dollar. EUR/USD hovers in the 1.14 area. USD/JPY (112.9 0) is holding (very) strong despite a tentative risk-off sentiment.

No post Carney follow-through gains for sterling

Yesterday, EUR/GBP trading was spooked by sharp euro swings in the wake of the Draghi comment and by BoE Carney preparing the market for a potential rate hike. Today, the EUR/GBP cross rate was an area of perfect calm. The pair was locked in a very narrow range close to the 0.88 pivot. The UK lending data (consumer credit and housing) were stronger than expected, but they were ignored. Cable tested the 1.30 area around noon. However, no sustained break occurred because the decline of the dollar eased as US traders joined the fray. GBP/USD trades currently in the 1.2970 area.

USDJPY Bullish, Threatens Further Upside Pressure

USDJPY: The pair continues to press higher as it saw price extension during Thursday trading today. On the downside, support comes in at the 112.00 level where a break if seen will aim at the 111.50 level. A cut through here will turn focus to the 111.00 level and possibly lower towards the 110.50 level. Its daily RSI is bullish and pointing higher suggesting further u[side pressure. On the upside, resistance resides at the 113.00 level. Further out, we envisage a possible move towards the 113.50 level. Further out, resistance resides at the 114.00 level with a turn above here aiming at the 114.50 level. On the whole, USDJPY looks to strengthen further in the days ahead.

CAC Dips, Euro Jumps on Draghi Aftermath

The CAC index has posted losses in the Thursday session. Currently, the index is down 0.68% and is trading at 5220.80. On the release front, there are no eurozone or French indicators on the schedule. In the US, Preliminary GDP is expected to gain 1.2%. On Friday, the Eurozone publishes CPI Flash Estimate and France will release Consumer Spending and Preliminary CPI.

Mario Draghi was on center stage at this week's ECB forum in Portugal, but he probably was not counting on a sharp euro rally just after delivering his prepared speech. Draghi presented an optimistic view of the euro-area, acknowledging that economic indicators continued to point to a broadening recovery in the eurozone. Draghi noted that the recovery was broad, but pointed to inflation as the barrier to tightening policy. Draghi defended the bank's loose accommodative policy, saying that it had pushed inflation higher, but stimulus was needed until inflation becomes "durable and self-sustaining". Draghi's comments did not appear to be a major change from previous statements, as the ECB has said time and time again that the bank has no plans to remove stimulus until inflation levels in the eurozone are closer to the ECB's target of 2 percent. However, the markets clearly think otherwise, as Draghi's comments have raised speculation that the ECB is planning to tighten policy. After the euro jumped, the ECB beat a hasty retreat, as sources said that the markets had "misinterpreted" Draghi's remarks. This impeded the euro's rally, but only briefly. The ECB has consistently said that it would not reduce stimulus until inflation moves closer to the ECB's target of 2%, but the message the markets appear to have heard is that the long war on inflation has been won, so it's only a matter of time before the ECB wraps up its monetary stimulus. If investors remain convinced that the ECB's easy money policy is on its way out, European stock markets could lose ground.

The presidential and parliamentary elections in France have turned French politics upside down, as the old left-right divide has been erased, at least for now. Then new president, Emmanuel Macron, is a relative newcomer to French politics, and his En Marche party, which has a majority in parliament, is little more than a year old. Macron appears determined to bring major changes to France, and his message has clearly struck a note with French voters. The sense of renewed optimism was underscored by the latest INSEE consumer confidence report, which jumped to 108 points in the June report, up from 103 in May. This marked the highest level since 2007. Although consumers are in a good mood, this optimism has so far not translated into stronger consumer spending, but nevertheless is another sign that the French economy is improving. INSEE has revised upwards its estimate for France's GDP for the first quarter to 0.5%, up from 0.4% earlier in June.

Will the US GDP report miss expectations? The economy is expected to grow 1.2%, but there are worrying signs that Final GDP might miss this target. Recent US economic data has been softer than expected, notably construction and manufacturing reports. US durable goods releases were weak in May. Core Durable Goods broke a streak of two straight declines, but the weak gain of 0.1% missed expectations. Durable Goods declined 1.1%, its sharpest decline since June 2016. The slowdown in orders of business equipment could weigh on second quarter growth. Last week, it was the turn of construction numbers to disappoint, as Housing Starts and Building Permits both missed expectations. Consumer spending has also been softer than expected, and if Final GDP falls short of the modest estimate of 1.2%, investor sentiment could sour and send the stock markets lower.

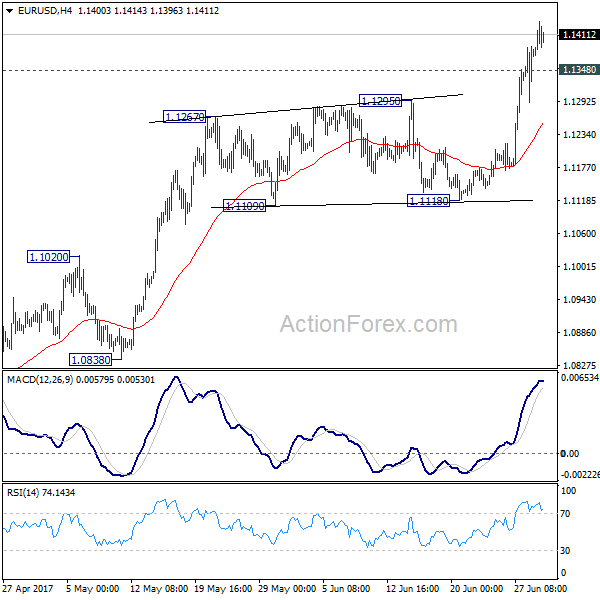

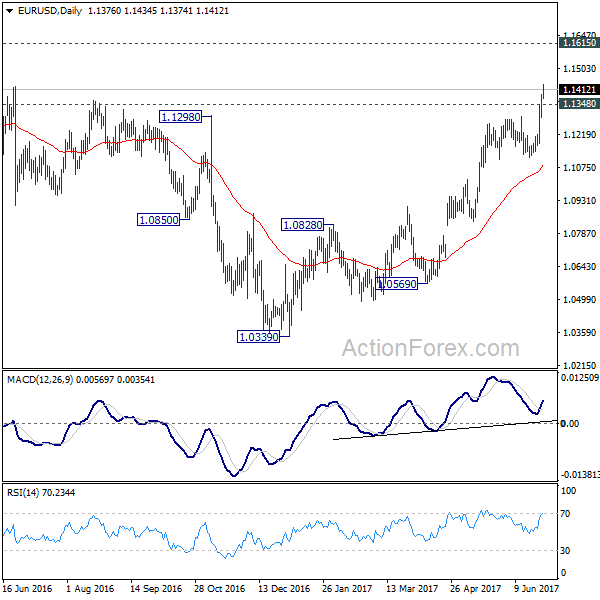

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1315; (P) 1.1352 (R1) 1.1414; More.....

Intraday bias in EUR/USD remains on the upside for the moment. Current rally from 1.0339 should target 1.1615 medium term resistance next. On the downside, below 1.1348 minor support will turn intraday bias neutral and bring retreat. But downside should be contained above 1.1118 support and bring rise resumption.

In the bigger picture, the break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition is seen in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1776). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

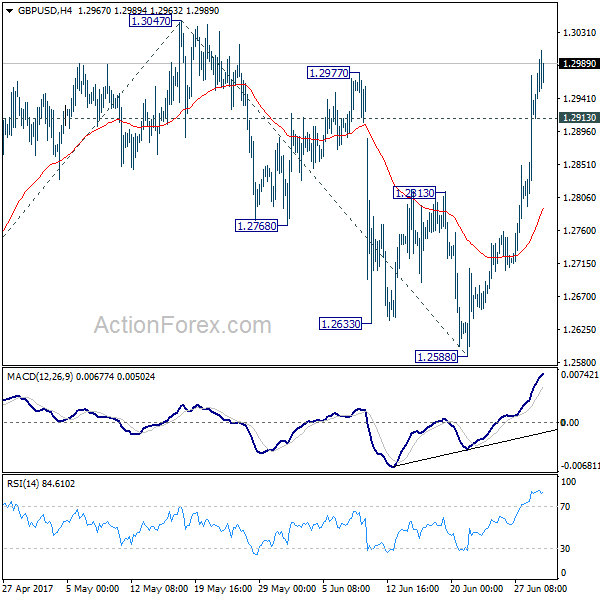

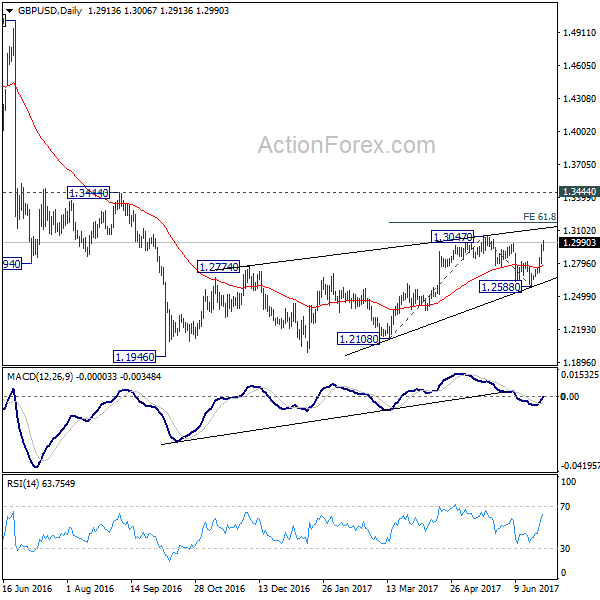

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2821; (P) 1.2896; (R1) 1.2998; More...

Intraday bias in GBP/USD remains on the upside for 1.3047 as rise from 1.2588 continues. Break of 1.3047 will target 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168. On the downside, below 1.2913 minor support will turn bias neutral and bring retreat, before staging rally resumption.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. Pull back from 1.3047 has completed after failing to sustain below 1.2614 resistance turned support. It argues that the corrective pattern from 1.1946 is still in progress for another high above 1.3047. But still, outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes.

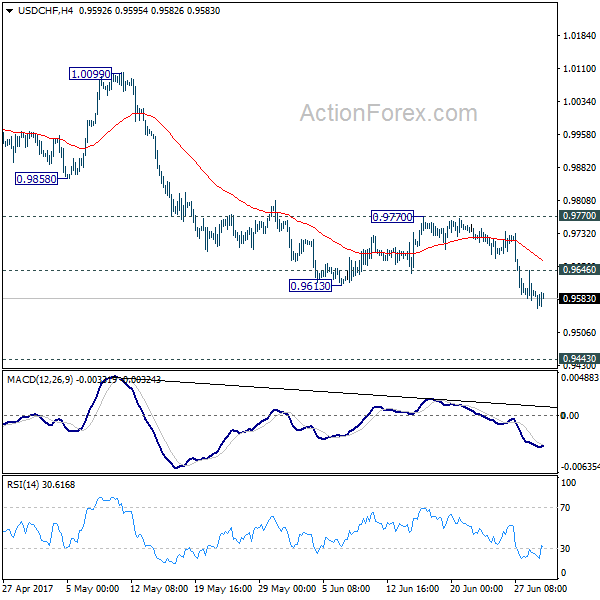

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9568; (P) 0.9607; (R1) 0.9637; More.....

Intraday bias in USD/CHF remains on the downside as fall from 1.0342 continues. Deeper decline would be seen to 0.9548 support and below. We'd start to look for bottoming signal again as it approaches 0.9443 key support level. On the upside, above 0.9646 minor resistance will turn bias neutral and bring recovery. But still, break of 0.9770 resistance is ended to indicate short term bottoming. Otherwise, outlook will remain bearish.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

Trade Idea: EUR/GBP – Stand aside

EUR/GBP - 0.8791

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

Original strategy :

Exit long entered at 0.8800,

Position : -

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the single currency rose to as high as 0.8882 yesterday, lack of follow through buying and the subsequent sharp retreat suggest a temporary top is possibly formed there and few days of consolidation would be seen with mild downside bias for a test of 0.8763 support, break there would add credence to this view, bring retracement of recent upmove to 0.8730-35, however, still reckon downside would be limited to 0.8719 support.

In view of this, would be prudent to stand aside for now and look to turn short on recovery as 0.8840-50 should limit upside. Above 0.8882 would revive bullishness and extend recent upmove from 0.8304 low to 0.8900-10, having said that, as broad outlook remains consolidative, reckon current c leg of larger degree wave b should be limited to 0.8950 and price should falter well below 0.9000 psychological level.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.