Sample Category Title

EUR/GBP Elliott Wave Analysis

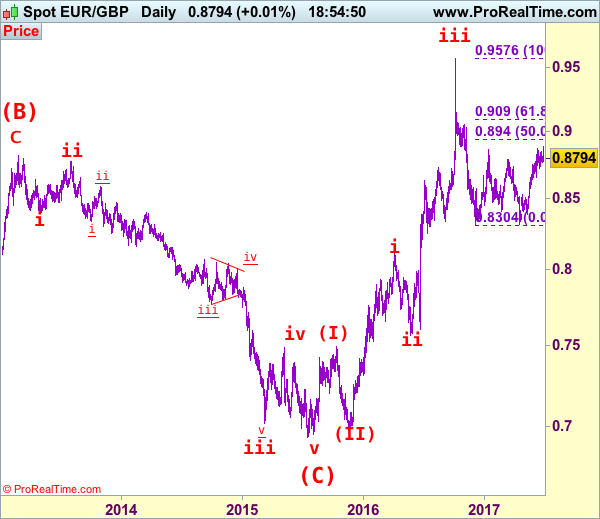

EUR/GBP – 0.8787

EUR/GBP – The major (A)(B)(C)-(X)-(A)(B)(C) correction from 0.9805 is unfolding and 2nd (A) has possibly ended at 0.6936.

Although the single currency edged higher to 0.8882 yesterday, lack of follow through buying and the subsequent retreat suggest consolidation below this level would be seen and initial downside risk is for pullback to support at 0.8719, however, still reckon downside would be limited and support at 0.8652 should hold, bring another rise later. Above said resistance at 0.8882 would signal the erratic rise from 0.8304 low is still in progress and may extend gain to 0.8940-50 (50% Fibonacci retracement of 0.9576-0.8304) but loss of upward momentum should prevent sharp move beyond 0.9000 psychological level and price should falter below 0.9090-00 (61.8% Fibonacci retracement) and bring retreat later.

Our latest preferred count is that the wave V of a 5-wave series from 0.5682 ended at 0.9805 earlier and major from there has possibly ended at 0.8067 as A-B-C-X-A-B-C. We are keeping our view that the entire correction from 0.9805 has possibly ended at 0.7756 and as labeled as the attached daily chart and impulsive move from 0.9084 has ended at 0.7756 as a 5-waver which marked either the (C) wave or the A leg of (C), a daily close above resistance at 0.8831 would suggest (C) leg has ended and headway towards 0.9084.

On the downside, whilst initial pullback to 0.8735-40 cannot be rule out, reckon 0.8680-90 would limit downside and bring another rise later. A daily close below support at 0.8652 would suggest top is possibly formed and risk weakness towards 0.8600-05 but reckon downside would be limited to 0.8550 and previous support at 0.8524 should hold from here, bring rebound later.

Recommendation: Buy at 0.8680 for 0.8880 with stop below 0.8580

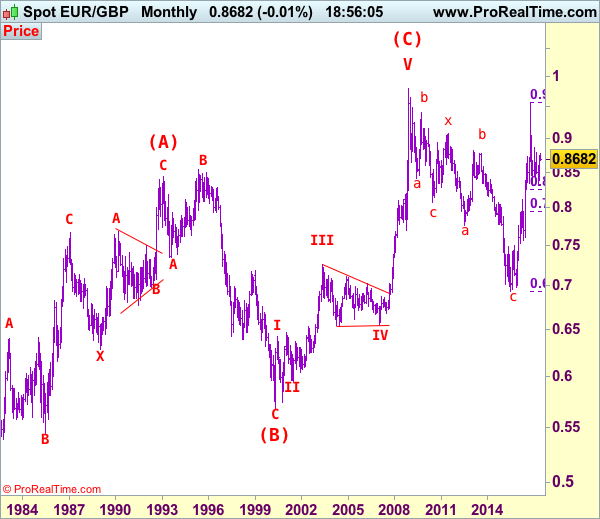

Euro's long term uptrend started in Feb 1981 at 0.5039 and is unfolding as a (A)-(B)-(C) move with (A): 0.8433 (Feb 1993), (B): 0.5682 (May 2000) and impulsive wave (C) should have ended at 0.9805 with wave III ended at 0.7254 (May 2003), triangle wave IV at 0.6536 (23 Jan 2007) and wave V as well as wave (C) has ended at 0.9805.

We are keeping an alternate count that only wave III ended at 0.9805 and the correction from there is the wave IV and may extend weakness to 0.7700, however, it is necessary to see a daily close above resistance at 0.9143 would change this to be the preferred count.

AUDJPY Bullish At 3-Month High

AUDJPY picked up from where it left yesterday, adding to its gains to record a three-month high of 86.44. The pair currently looks set for its fifth straight day of gains.

The RSI is well into bullish territory and maintains a steep positive slope. It is noteworthy though, that at 73 it has exceeded its overbought threshold (at 70). This might be an indication that the recent uptrend is overextended.

The area around 86.50 has been a heavily congested one in previous months and could provide resistance. Further up, the 87.00 handle might act as a psychological barrier, while a break above would shift focus to the four-month high of 87.48 from March 16.

On the downside, the 61.8% Fibonacci retracement at 85.60 (February 16 – April 19 downleg) could offer support. Should this be violated, the 85.00 mark and 50.0% Fibonacci at 84.81 might form another support area.

In the bigger picture, the recent uptrend leading the price comfortably above the 50- and 200-day moving averages (MAs) has reinforced the bullish outlook which was in danger of turning neutral. Also notice that both MAs are currently upward sloping.

Summing up, both the short- and medium-term outlooks are bullish at the moment.

DAX Edges Lower, German CPI Looms

The DAX index has reversed directions in the Thursday session, dropping 0.36%. Currently, the DAX is at 12,607.50. On the release front, German GfK Consumer Climate improved to 10.6, beating the estimate of 10.4. Later in the day, Germany releases Preliminary CPI, with an estimate of a flat 0.0%. In the US, today's key event is Final GDP, which is expected to gain, 1.2%. As well, unemployment claims are expected to remain at 241 thousand. On Friday, Germany releases Retail Sales and the eurozone publishes CPI Flash Estimate. The US will publish UoM Consumer Sentiment.

Mario Draghi was likely unprepared for the sharp reaction on the currency markets to his remarks at the ECB forum in Portugal. EUR/USD has rallied this week, climbing 1.9% on Draghi's hawkish comments. Draghi presented an optimistic view of the euro-area, saying that the recovery was broad and shrugged off weak inflation levels. Draghi said that the ECB's stimulus program was needed for now, but would be gradually withdrawn once inflation moved higher. Draghi's comments did not appear to be a major change from previous statements, as the ECB has said time and time again that the bank has no plans to remove stimulus until inflation levels in the eurozone are closer to the ECB's target of 2 percent. However, the markets clearly think otherwise, as Draghi's comments have raised speculation that the ECB is planning to tighten policy. After the euro jumped, the ECB beat a hasty retreat, as sources said that the markets had “misinterpreted” Draghi's remarks. This impeded the euro's rally, but only briefly. The ECB has consistently said that it would not reduce stimulus until inflation moves closer to the ECB's target of 2%, but the message the markets appear to have heard is that the long war on inflation has been won, so it's only a matter of time before the ECB wraps up its monetary stimulus. If investors remain convinced that the ECB's easy money policy is on its way out, European stock markets could lose ground.

The German economy continues to perform well, as the labor market is strong, exports are up and consumer demand is solid. Still, Germany has not been immune to low inflation levels, which have hampered economies in Europe, Japan and North America (the UK is one notable exception). German CPI, the primary gauge of consumer inflation, has not posted a gain since March, and the estimate for the June report stands at a flat 0.0%. The strong economy and the ECB's loose monetary policy, inflation remains stubbornly low. One key factor in this is falling oil prices, which have also pushed energy stocks lower, and this has weighed on the DAX as well. Some analysts have projected that the ECB will not raise interest rates before 2019, as the eurozone economy is simply not strong enough to withstand higher interest rates in the near future.

It's report card day for the US economy, with the release of Final GDP for the first quarter later on Thursday. The economy is expected to grow 1.2%, but there are worrying signs that the GDP might miss this target. Recent US economic data has been softer than expected, notably construction and manufacturing reports. US durable goods releases were weak in May. Core Durable Goods broke a streak of two straight declines, but the weak gain of 0.1% missed expectations. Durable Goods declined 1.1%, its sharpest decline since June 2016. The slowdown in orders of business equipment could weigh on second quarter growth. Last week, it was the turn of construction numbers to disappoint, as Housing Starts and Building Permits both missed expectations. Consumer spending has also been softer than expected, and if Final GDP falls short of the modest estimate of 1.2%, investor sentiment could sour and send the stock markets lower.

Euro Hits 14 Month Highs On Draghi Remarks

The euro has posted gains for a third straight day, as the pair is up 0.32% in the Thursday session. In Germany, GfK Consumer Climate improved to 10.6, beating the estimate of 10.4. Later in the day, Germany releases Preliminary CPI, with an estimate of a flat 0.0%. In the US, Final GDP is expected to gain 1.2%, while unemployment claims are forecast to remain at 241 thousand. On Friday, Germany releases Retail Sales and the eurozone publishes CPI Flash Estimate. The US will publish UoM Consumer Sentiment.

The Draghi rally continues on Thursday, as the euro has punched past the 1.14 level for the first time since June 2016. The euro has jumped 1.9% this week, buoyed by hawkish comments by ECB President Mario Draghi at the ECB forum in Portugal. Draghi presented an optimistic view of the euro-area, saying that the recovery was broad and shrugged off weak inflation levels. Draghi said that the ECB's stimulus program was needed for now, but would be gradually withdrawn once inflation moved higher. Draghi's comments did not appear to be a major change from previous statements, but the markets thought otherwise, as speculation rose that the ECB was planning to tighten policy. After the euro jumped, the ECB beat a hasty retreat, as sources said that the markets had “misinterpreted” Draghi's remarks. This impeded the euro's rally, but only briefly. The ECB has consistently said that it would not reduce stimulus until inflation moves closer to the ECB's target of 2%, but the message the markets appear to have heard is that the long war on inflation has been won, so it's only a matter of time before the ECB wraps up its monetary stimulus. Unless Draghi does more to convince the markets that they have indeed overreacted, the euro rally could continue.

Investors are casting a nervous glance at Thursday, as the US releases Final GDP for the first quarter. The economy is expected to grow 1.2%, but there are worrying signs that the economy might miss this target. Recent economic data has been softer than expected, notably construction and manufacturing reports. US durable goods releases were weak in May. Core Durable Goods broke a streak of two straight declines, but the weak gain of 0.1% missed expectations. Durable Goods declined 1.1%, its sharpest decline since June 2016. The slowdown in orders of business equipment could weigh on second quarter growth. Last week, it was the turn of construction numbers to disappoint, as Housing Starts and Building Permits both missed expectations. Consumer spending has also been softer than expected, and if Final GDP falls short of the modest estimate of 1.2%, the dollar could respond with losses.

USD/CAD Elliott Wave Analysis

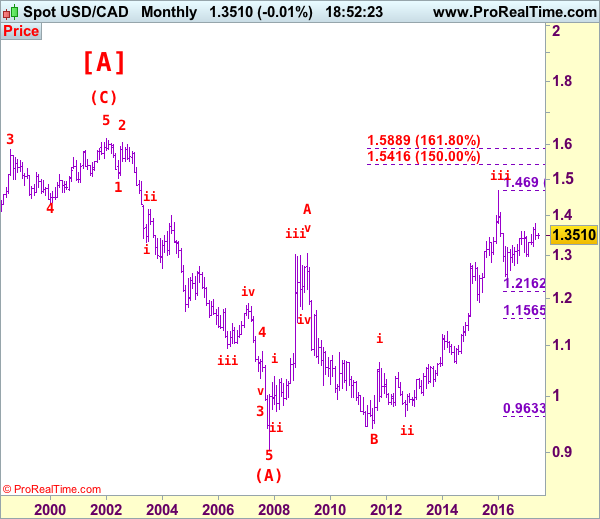

USD/CAD – 1.3012

USD/CAD – Wave v ended at 0.9407 and a-b-c correction may extend gain to 1.4700

The greenback met renewed selling interest at 1.3348 and has dropped sharply since, adding credence to our bearish view that the decline from 1.3794 top is still in progress and bearishness remains for test of previous support at 1.2969, however, a sustained breach below there is needed to retain downside bias and suggest the rebound from 1.2461 has ended at 1.3794 (tentatively wave b top), hence further weakness to 1.2900 and later 1.2850-55 would be seen but near term oversold condition should prevent sharp fall below previous support at 1.2763, risk from there has increased for a rebound later.

We are keeping our view that the wave b from 1.0657 (a leg top) has possibly ended at 0.9633 with (a): 0.9800, wave (b): 1.0447 and wave c at 0.9633, the subsequent rise from there is now treated as wave c exceeded indicated upside target at 1.3770-80 and 1.4000 and wave (3) has possibly ended at 1.4690 and wave (4) correction has commenced for retracement back to 1.2832 support, then 1.2410-20.

On the daily chart, our latest preferred count remains that the A of (B) rally from 0.9059 low (7 Nov 2007) unfolded into an impulsive wave with i: 0.9059-1.0380, ii ended at 0.9819, iii at 1.3019 followed by triangle wave iv at 1.2026 , then wave v formed a top at 1.3066 and also ended the wave A. The wave B is unfolding as an double three a-b-c-x-a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c at 1.0784, followed by wave x at 1.1725, another set of a-b-c unfolded with 2nd a at 0.9931, 2nd b at 1.0674. the 2nd c has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3900 had been met and gain to 1.4700 would follow.

On the upside, whilst initial recovery to 1.3090 cannot be ruled out, reckon upside would be limited to previous support at 1.3165 (now resistance) and bring another decline later. Above 1.3260-65 would defer and risk a stronger rebound to 1.3300 but said resistance at 1.3348 would remain intact, bring another decline later.

Recommendation: Sell at 1.3150 for 1.2950 with stop above 1.3250.

Longer term - The selloff from 1.6194 (21 Jan 2002) to 0.9059 (07 Nov 2007) is viewed as (A) wave which is a 5-waver as labeled on the monthly chart as below, the subsequently rally is labeled as (B) with impulsive A leg of (B) ended at 1.3066, wave B of (B) is unfolding which has either ended at 0.9407 or would extend one more fall but downside should be limited to 0.9200 and 0.9000 should hold.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD continued its bullish momentum yesterday topped at 1.1390 and hit 1.1419 earlier today in Asian session. The bias remains bullish in nearest term testing 1.1425. A clear break above that area could trigger further bullish pressure testing 1.1500 region before targeting 1.1615 area. Immediate support is seen around 1.1350. A clear break below that area could lead price to neutral zone in nearest term testing 1.1300 – 1.1285 region but overall I remain bullish and any downside pullback should be seen as a good opportunity to buy.

GBPUSD

The GBPUSD continued its bullish momentum yesterday topped at 1.2971. The bias remains bullish in nearest term testing 1.3050. Immediate support is seen around 1.2915. A clear break below that area could lead price to neutral zone in nearest term but as long as stay above 1.2815 price is still in a bullish phase and any downside pullback should be seen as a good opportunity to buy. On the upside, a clear break and daily close above 1.3050 would activate my bullish mode.

USDJPY

The USDJPY was indecisive yesterday. Price attempted to push lower, bottomed at 111.83 but whipsawed to the upside and closed higher at 112.32. There are no changes in my technical outlook. The bias remains bullish in nearest term testing 113.00 region. Immediate support is seen around 111.78/45 area. A clear break back below that area could lead price to neutral zone in nearest term but as long as stay above 110.65 price is still in a bullish phase. On the upside, a clear break and daily close above 113.00 would expose 114.30 region.

USDCHF

The USDCHF attempted to push higher yesterday topped at 0.9647 but closed lower at 0.9597. The bias remains bearish in nearest term testing 0.9550 – 0.9500 area. However, from a daily chart perspective as you can see on my daily chart below, 0.9550 – 0.9450 region is a major support area, which is a good place to buy. Immediate resistance is seen around 0.9647 (yesterday’s high). A clear break above that area would interrupt the bearish phase testing 0.9765 region.

GOLD Ready To Bounce Back, SILVER Bullish Consolidation With Medium-Term Bearish Move, CRUDE OIL Continued Bullish Consolidation.

GOLD Ready to bounce back.

RBNZ's medium-term momentum is positive. Hourly support is located at 1236 (26/06/2017 low). Stronger support is given at 1214 (09/05/2017 low). Expected to show renewed bullish pressures.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Bullish consolidation with medium-term bearish move.

Silver's selling pressures are strong despite ongoing bullish consolidation. Closest support is given at 16.29 (26/06/2017 low). Strong support is given at 16.06 (09/05/2017 low). Key resistance is given at a distance at 17.75 (06/06/2017 high). The road seems wide open for further decline.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009)

CRUDE OIL Continued bullish consolidation.

Crude oil is now consolidating higher since the commodity hit 11-month low. Support is given at 42.05 (21/06/2017 low). Expected to show renewed weakness.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

ECB Sources Drag EUR Lower, But Can’t Hold It Down

The euro pulled back briefly yesterday, after media reports familiar with ECB sources suggested that markets misinterpreted ECB President Draghi's comments on Tuesday. Investors had interpreted Draghi's remarks as being on the hawkish side, but these reports said the speech was intended to be balanced.

Our own view is that the ECB appears to be uncomfortable with the elevated speculation regarding an eventual QE-exit, as a rapidly appreciating euro and rising euro area bond yields could weigh on inflation and make the Bank's job of bringing it back to target even harder. Overall, we still believe that the Bank is likely to continue shifting towards a more upbeat tone and that the euro's broader outlook remains positive. The market appears to share our view, considering that even though the euro tumbled on these reports, the currency quickly recovered all its losses to trade even higher in the following hours.

EUR/JPY has been in a rally mode the last few days, especially following the break above the long-term downside resistance line taken from the peak of the 7th of June 2015. We believe that following that break, the medium-term outlook of the pair has turned positive and that the move above 127.80 (S1) may have opened the way for the psychological zone of 130.00 (R1). Nevertheless, given that the rally appears overextended, we would stay careful that a corrective setback may be on the cards before the bulls decide to take charge again.

Carney boosts sterling; Queen's Speech in focus

The BoE Governor shifted to a somewhat hawkish tone yesterday, hinting that he could support a rate hike in the upcoming policy meetings. Carney said that the removal of monetary stimulus is likely to become necessary as the trade-off facing the MPC continues to lessen. He added that a hike may depend mainly on whether weaker consumption growth is offset by stronger business investment, and on whether wages begin to firm.

The result was a surge in the pound as these remarks may have caught investors by surprise, considering that just last week, Carney was perceived as dovish when he said “now is not the time to raise rates”. The question now is: Will the BoE actually hike? We think that much will depend on wage growth, which has been lackluster so far. Unless it picks up notably, any policy tightening seems unlikely, in our view. Having said that, the number of MPC members willing to support a hike appears to be increasing. McCafferty and Saunders already voted for a hike in June, while Haldane and now Carney both hint they could support one in coming months as well.

Turning to UK politics, the focus today may be on the Queen's Speech vote. Importantly, the Tory-DUP deal is now finalized. Thus, the 10 DUP MPs are expected to vote for the Speech, which implies Theresa May is likely to keep her job as PM. If all goes as planned and Parliament approves the Speech, political uncertainty in the UK could dissipate further, and market focus is likely to turn to headlines surrounding the Brexit negotiations. In this scenario, GBP could gain, but given that this is widely anticipated, any positive reaction may be modest. On the other hand, should lawmakers reject the Speech, GBP could tumble on the increased uncertainty over who will be the next PM, as well as the probable delay of the crucial EU-UK talks. Looking a few days ahead though, the prospect of a Labour government or another election could result in a stronger pound overall, as the likelihood of a hard Brexit will probably diminish.

GBP/USD skyrocketed on Wednesday following Carney's rhetoric to emerge above the key resistance (now turned into support) territory of 1.2850 (S2). Subsequently, it broke above the crossroad of the 1.2910 (S1) barrier and the downside resistance line taken from the peak of the 18th of May. In our view, this keeps the door open for further advances and a positive vote on the Queen Speech today may be the trigger for something like that. A clear break above 1.2975 (R1) is possible to open the way for our next resistance hurdle of 1.3015 (R2). In the unlikely scenario of the Speech being rejected, the pair may tumble back below 1.2910 (S1) and perhaps challenge the 1.2850 (S2) territory as a support this time.

As for today's economic data:

In Germany, the preliminary CPI rate for June is expected to have ticked down. Such a decline could hurt the euro somewhat, but we would like to stress that Germany reports only a headline, not a core, inflation rate. Thus, a small slide in this rate could be owed mainly to movements in the prices of volatile items, and may not necessarily be descriptive of underlying inflationary pressures in Eurozone's economic powerhouse.

From the US, we get the final estimate of GDP for Q1, but considering that Q2 is almost over, we think that these data are likely to be viewed as outdated and thus any reaction in USD may be limited.

EUR/JPY

Support: 127.80 (S1), 126.45 (S2), 125.70 (S3)

Resistance: 130.00 (R1), 132.10 (R2), 134.65 (R3)

GBP/USD

Support: 1.2910 (S1), 1.2850 (S2), .1.2795 (S3)

Resistance: 1.2975 (R1), 1.3015 (R2), 1.3050 (R3)

Daily Technical Analysis: USD/JPY Zig-Zag Uptrend But Watch For D H4 Resistance

The USD/JPY has been moving in a zig-zag pattern that indicates uptrend but at this point its close to ATR top/D H4 resistance. We can also see a bearish divergence so we might expect some pullback. The POC zone is 112.00-15 (38.2, D L4, EMA89, ATR pivot). If the price gets there we might see a bounce towards D H5 112.90. However if the price gets to ATR top/ D H5 we might see a rejection towards 112.20-00 again. So watch for both zones in terms of trading as the price might reject from both POC and D H5/ ATR top confluence.

Technical Outlook: WTI Hits Two-Week High As Recovery Extends Into Sixth Straight Day

WTI oil price hit two-week high at $45.22 on Thursday, after extension of Wednesday's strong rally cracked important barrier at $45.04 zone (Fibo 61.8% of $46.69/$42.04/falling 20SMA/19 June high). Oil price extends recovery rally from $42.04 low into a sixth day, after unexpected build in US crude inventories was offset by bigger than expected fall in gasoline inventories and report of the biggest weekly decline in domestic oil production since July 2016. Positive sentiment that has been established may drive the price higher on sustained break of $45.00 pivot. Fresh bullish extension would look for $45.59/84 (Fibo 76.4% of $46.69/$42.04/Fibo 38.2% of $51.98/$42.04) and may extend towards key short-term barrier at $46.69 (12 June lower top). Corrective dips should find support at $44.30 (4-hr cloud top), while stronger pullback is expected to hold above 10SMA (currently at $43.77) to keep near-term bullish structure intact).

Res: 45.22, 45.59, 45.84, 46.46

Sup: 44.74, 44.30, 44.00, 43.77