Sample Category Title

Technical Outlook: USDJPY – Bulls May Extend Towards 113.00, Broken Daily Cloud Supports

The pair remains firm following strong rally in past two days that eventually broke above daily cloud and generated another strong bullish signal on Tuesday's close above 112.24 (Fibo 61.8% of 114.36/108.80 descend. Consolidation below Tuesday's fresh nearly six-weeks high at 112.46 is so far holding above 112.00 handle, keeping intact more significant daily cloud (currently spanned between 111.82/65 and reinforced by 100SMA) which should ideally contain dips ahead of fresh push higher, as bulls eye target at 113.05 (Fibo 76.4% of 114.36/108.80).

Res: 112.24, 112.46, 113.05, 113.35

Sup: 112.00, 111.82, 111.65, 111.46

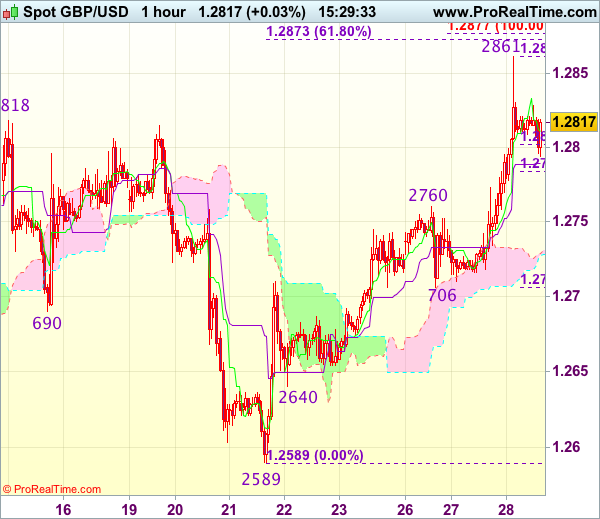

Technical Outlook: GBPUSD – Bulls Look For Renewed Attack At Daily Cloud Top

Cable is consolidating around 1.2800 handle in early Wednesday's trading after strong rally on Tuesday, dragged by rallying Euro and weaker dollar, hit target at 1.2861, provided by top of thick daily cloud.

However, near-term sentiment has improved and sidelined persisting Brexit concerns that open way for further advance.

Close above cracked pivotal barriers at 1.2828/37 (Fibo 61.8% of 1.2977/1.2588 downleg / 55SMA) is needed to confirm bullish stance for renewed attack and break above daily cloud.

Extended consolidation between 20SMA (1.2785) and 55SMA (1.2837) could be expected, with stronger dips expected to find support above 10SMA (1.2732).

Return below Tuesday's low at 1.2715 would be seen as strong bearish signal.

Res: 1.2837, 1.2861, 1.2885, 1.2920

Sup: 1.2785, 1.2756, 1.2732, 1.2715

Trade Idea: GBP/JPY – Buy at 142.60

GBP/JPY - 143.35

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term down

Original strategy:

Buy at 141.30, Target: 143.30, Stop: 140.70

Position: -

Target: -

Stop: -

New strategy :

Buy at 142.60, Target: 144.50, Stop: 142.00

Position: -

Target: -

Stop:-

As sterling has retreated after surging to 144.20 yesterday, suggesting minor consolidation below this level would be seen and pullback to 143.00 is likely, however, reckon previous resistance at 142.50 would turn into support and limit downside and bring another rise later, above said resistance at 144.20 would extend the erratic rise from 138.70 low to 144.90-00 and possibly towards resistance at 145.45 later.

In view of this, would not chase this rise here and we are looking to buy sterling on subsequent pullback as previous resistance at 142.50 should limit downside and bring another rise. Below 142.00 support would defer and suggest top is formed instead, risk weakness towards another previous support at 141.35 first.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

Elliott Wave Analysis: EURUSD Making A Strong Bullish Statement

Because of yesterday's sharp and strong price activity we changed our primary look and are now looking at a bullish impulse being made, with price specifically trading in blue wave 5. Ideally blue wave 5 will unfold a five wave development within itself, before slowing down for a correction.

EURUSD, 4H

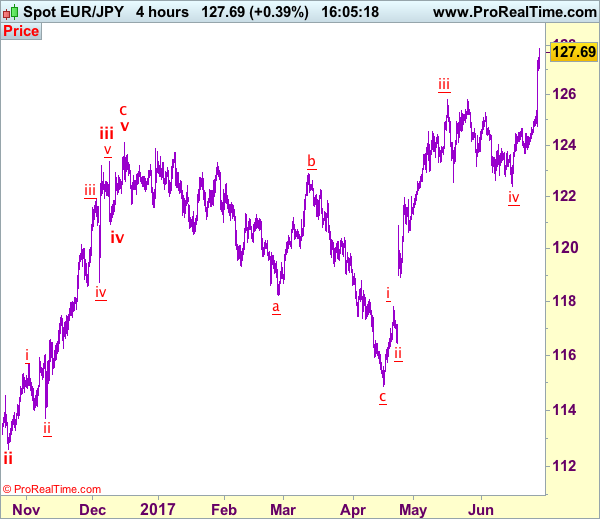

Trade Idea: EUR/JPY – Buy at 126.00

EUR/JPY - 127.17

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term up

Original strategy:

Buy at 125.00, Target: 127.00, Stop: 124.40

Position: -

Target: -

Stop: -

New strategy :

Buy at 126.00, Target: 128.00, Stop: 125.40

Position: -

Target: -

Stop:-

Yesterday’s rally after breaking above previous resistance at 125.82 adds credence to our bullish count for a resumption of recent upmove and upside bias remains for medium term rise to extend further gain to 128.00-10, however, near term overbought condition should prevent sharp move beyond 128.50-60 and reckon 129.00-10 would hold from here, risk from there has increased for a retreat later.

In view of this, we are looking to reinstate long on pullback as said resistance resistance at 125.82 should turn into support and limit downside, bring another upmove. Below 125.40-50 would defer and risk weakness to 124.65-75 but break there is needed to signal top is formed instead, bring correction of recent upmove to 124.00-10, however, support at 123.66 should remain intact.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Trade Idea: AUD/USD – Hold long entered at 0.7595

AUD/USD – 0.7590

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term up

Original strategy :

Bought at 0.7595, Target: 0.7745, Stop: 0.7555

Position: - Long at 0.7595

Target: - 0.7745

Stop: - 0.7555

New strategy :

Hold long entered at 0.7595, Target: 0.7745, Stop: 0.7555

Position: - Long at 0.7595

Target: - 0.7745

Stop:- 0.7555

As aussie has retreated after faltering below resistance at 0.7625, suggesting further consolidation would be seen, however, as long as minor support at 0.7558 holds, mild upside bias remains for another rebound, above said resistance at 0.7625 would bring a retest of indicated resistance at 0.7636, break there would confirm recent upmove has resumed and extend the rise from 0.7329 towards previous resistance at 0.7680 but loss of momentum should limit upside to chart resistance at 0.7750 and price should falter below 0.7785-90.

In view of this, we are holding on to our long position entered at 0.7595. Only below said support at 0.7535 would defer and suggest top is possibly formed, bring correction to 0.7515-20, break there would provide confirmation, then correction to 0.7490-95 and possibly towards support at 0.7457 would be seen later.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

Trade Idea : USD/CHF – Sell at 0.9660

USD/CHF - 0.9595

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9596

Kijun-Sen level : 0.9659

Ichimoku cloud top : 0.9718

Ichimoku cloud bottom : 0.9707

Original strategy :

Sell at 0.9680, Target: 0.9580, Stop: 0.9715

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9660, Target: 0.9550, Stop: 0.9695

Position : -

Target : -

Stop : -

The greenback has remained under pressure after yesterday’s selloff below previous chart support at 0.9613, adding credence to our bearish view that the decline from 0.9771 top is still in progress and downside bias remains for further weakness towards 0.9550, however, reckon downside would be limited to 0.9525-30 (50% projection of 1.10100-0.9613 measuring from 0.9771) and 0.9500 should hold, price should stay above 0.9470 (61.8% projection), bring rebound later.

In view of this, would not chase this fall here and we are looking to sell dollar on recovery as previous support at 0.9676 should turn into resistance and limit dollar’s upside, bring another decline. Above another previous support at 0.9692 would defer and risk a stronger rebound to 0.9715-20 but only break of resistance at 0.9738-43 would signal low is formed.

Trade Idea : GBP/USD – Buy at 1.2780

GBP/USD - 1.2825

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2811

Kijun-Sen level : 1.2790

Ichimoku cloud top : 1.2729

Ichimoku cloud bottom : 1.2728

Original strategy :

Buy at 1.2710, Target: 1.2810, Stop: 1.2675

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2780, Target: 1.2880, Stop: 1.2745

Position : -

Target : -

Stop : -

As cable has retreated after rising to 1.2861 in part due to cross-trading against euro, suggesting consolidation below this level would be seen and pullback to 1.2780-85 (50% Fibonacci retracement of 1.2706-1.2861) cannot be ruled out, however, reckon downside would be limited to 1.2760-65 (previous resistance and 61.8% Fibonacci retracement) and bring another rise later, above said resistance at 1.2861 would extend the erratic rise from 1.2589 low 1.2875-80 (100% projection of 1.2589-1.2760 measuring from 1.2706), then towards 1.2915-20 (1.236 times projection) but price should falter well below 1.2978-83 (previous resistance and 1.618 times projection).

In view of this, would not chase this move here and would be prudent to buy cable on pullback as 1.2780-85 should limit downside. Below previous resistance at 1.2760 would defer and signal top is formed instead, bring correction to 1.2730 but support at 1.2706 should hold from here.

EURGBP Bullish In The Short-And Medium-Term, Price Hits 7½-Month High

EURGBP has been in an uptrend over the last couple of months. Today's gain has led the pair to record a fresh seven-and-a-half-month high of 0.8879. In yesterday's trading the pair finished the day 0.7% higher.

Looking at the Ichimoku analysis, the positive alignment when the Tenkan-sen line (red) crossed above the Kijun-sen (blue) in mid-May, is still in place. Moreover, the Tenkan-sen is currently steeply upward sloping, indicating that the positive short-term momentum remains intact. Adding to this conviction is the RSI indicator, which is well into bullish territory at 65 and maintains a positive slope.

The 0.89 handle, a potential psychological level, could act as a barrier to up movements in price. Further up, the near eight-month high of 0.8937 (excluding the November 9 spike), might offer additional resistance.

On the downside, the current level of the Tenkan-sen, which currently coincides with another potential psychological point, namely the 0.88 mark, could provide support. Below this point, the focus would shift to the Kijun-sen at 0.8741 as another support level.

As regards the medium-term outlook, the pair was ranging sideways for a significant part of the year. However, the uptrend in recent weeks, combined with the fact that the price is currently comfortably above both the 50- and 200-day moving averages, are painting a bullish picture.

To sum up, the short-term outlook is bullish. The same holds for the medium-term.

Yellen & Draghi Speak: Markets Listen

Central Banks are the key drivers of the markets this week as traders focused on comments made from two major central bankers; ECB Chief Draghi and Fed Chair Yellen.

Draghi commented that 'he sees room for paring back stimulus' this optimistic comment weighed on government bonds whereas Yellen suggested 'that the US economy can withstand higher interest rates and that asset valuations were rich'. The markets are now looking for additional economic strategy indications from various influential policy makers that are attending a conference in Portugal that ends today.

Volatility in US equities rose the highest in six weeks as investors digested recent economic data and central bank verbiage. The IMF have suggested a less rosy outlook for the US economy dismissing the Trump administrations tax cut pledge and an increase in infrastructure spending. Additionally, traders concerns continue with Oil moving into a Bear Market, the continued sell off of Technology stocks and the cyber attack that originated in the Ukraine and spread to several Major cities late yesterday.

USD remained under pressure slipping 0.2%% against JPY to trade currently at 112.31 near the day's high of 112.394.

EURUSD was higher, up 0.2%, currently trading at 1.1362. This after reaching a 10-month high earlier in the trading session of 1.13711.

GBPUSD also benefitted from USD weakness trading up to 1.28274 overnight before retracing back to currently trade at 1.2810.

USDCAD rose by nearly 0.5% to currently trade at 1.3138 following comments made by Bank of Canada Governor Poloz that interest rate cuts 'have done their job and that levels are now extraordinarily low'.

WTI & Brent have both risen nearly 1% overnight to currently trade at $44.22pb and $46.90pb respectively.

Gold gained another 0.4% against USD for the second consecutive day to trade currently at $1252.

Traders will now be looking ahead to several Central Bankers speeches today – all scheduled for 16:30 BST: BoE Governor Carney, BoJ Governor Karuda, ECB President Draghi & BoC Governor Poloz. At 17:30 BST sees the release of the EIA Crude Oil Stocks Change which is always impactful on Oil prices.