Sample Category Title

Trade Idea : EUR/USD – Buy at 1.1280

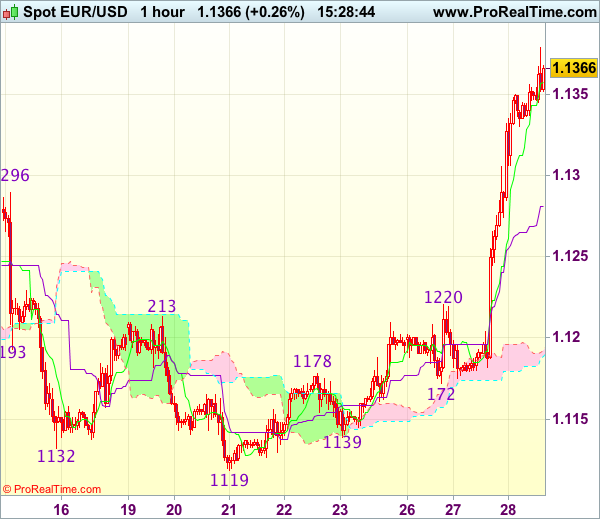

EUR/USD - 1.1375

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1358

Kijun-Sen level : 1.1281

Ichimoku cloud top : 1.1192

Ichimoku cloud bottom : 1.1189

Original strategy :

Buy at 1.1260, Target: 1.1360, Stop: 1.1225

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1280, Target: 1.1395, Stop: 1.1245

Position : -

Target : -

Stop : -

The single currency has continued moving higher after yesterday’s rally above previous resistance at 1.1296, confirming recent upmove has resumed and bullishness for further gain to 1.1400-05 (61.8% projection of 1.0839-1.1296 measuring from 1.1119), then towards 1.1430, however, near term overbought condition should prevent sharp move beyond 1.1450-60 and price should falter below 1.1500, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy euro on pullback as 1.1280-85 should limit downside. Below 1.1245-50 would defer and risk test of previous resistance at 1.1220 but break there is needed to confirm top is formed instead, bring correction towards 1.1180-85 later.

Technical Outlook: EURUSD – Tuesday’s Long Bullish Candle Underpins For Extension Towards 1.1414/28 Targets

The Euro extended gains on Wednesday and hit fresh one year high at 1.1378, following previous day's strong rally which marked the biggest one-day rally in 2017.

The single currency received strong support from the ECB Chief Draghi's speech on Tuesday and accelerated through the target at 1.1300 zone, generating strong bullish signal on close well above broken 1.1300 barrier.

Bulls eye next targets at 1.1414/28 (highs of 09/24 June 2016), with 1.1614 (03 May 2016 peak) coming in short-term focus.

Meanwhile, bulls may take a breather on overbought studies. Initial supports lay at 1.1329 (session low) and 1.1300 zone (former strong barrier).

Ascending converged daily Tenkan-sen/Kijun-sen lines offer next strong support at 1.1245 zone, with 20SMA at 1.1218 expected to contain extended dips.

Res: 1.1378, 1.1400, 1.1414, 1.1428

Sup: 1.1329, 1.1300, 1.1245, 1.1218

Trade Idea : USD/JPY – Buy at 111.80

USD/JPY - 112.25

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.23

Kijun-Sen level : 111.97

Ichimoku cloud top : 111.80

Ichimoku cloud bottom : 111.61

Original strategy :

Buy at 111.60, Target: 112.60, Stop: 111.25

Position : -

Target : -

Stop : -

New strategy :

Buy at 111.80, Target: 112.80, Stop: 111.45

Position : -

Target : -

Stop : -

The greenback has maintained a firm undertone after this week’s rally on active cross-selling in yen, adding credence to our bullishness and signal the rise from 108.82 low is still in progress, hence further gain to 112.75–80 (61.8% projection of 108.82-111.79 measuring from 110.95) would be seen, however, loss of momentum should limit upside and price should falter below 113.00-10 today, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback but at a higher level as 111.80 should limit downside. Below minor support at 111.46 would defer and suggest top is possibly formed, risk weakness to 111.10-15, break there would confirm, then test of support at 110.95 would follow.

Currencies: EUR/USD And EUR/GBP Testing Key Resistance Levels

Sunrise Market Commentary

- Rates: Draghi steps up to the plate

Markets will further digest ECB president Draghi's comments. Can “deflationary replaced by reflationary forces” become the new “whatever it takes”? We recommend a sell-on-upticks strategy in the Bund. On EMU bond markets, it could mark an end to the long-term narrowing trend. - Currencies: EUR/USD and EUR/GBP testing key resistance levels

A combination of hawkish comments from ECB's Draghi and negative (political) headlines from the US propelled EUR/USD for an extensive test of the 1.1300/66 resistance. A break would be significant from a technical point of view. Euro sentiment is strong, but an equity correction remains a wildcard for global FX trading. EUR/GBP is also testing the 2017 top

The Sunrise Headlines

- Wall Street was knocked hard in the wake of a delay to a US healthcare reform vote in Senate, the IMF's US growth forecast downgrade, a tech sell-off (Nasdaq -1.5%) and Fed Yellen's warning of “somewhat rich” asset valuations. Asian stock markets manage to limit losses overnight.

- Energy stocks rose as the broadly weaker tone of the dollar helped oil prices extend their recent rally from multi-month lows. Gold also benefited from a weaker dollar overnight, though still not recovered from the fat-finger sell off.

- The Chinese yuan surged for a second day amid speculation of central bank intervention. Meanwhile the euro rose on ECB Draghi's more hawkish tone with EUR/USD now around 1.135 and EUR/JPY just above 127. ECB's Constancio confirmed in an interview that Draghi's speech was in line with policy.

- A new cyberattack similar to WannaCry has reached Asia after spreading from Europe to the US overnight, hitting businesses, port operators and government systems.

- In a CNBC interview, Bank of Canada's Poloz said rate cuts have done their job and stated that excess capacity seems close to being used up. This shows that the BoC is coming closer to changing its monetary policy towards hiking.

- A trio of Fed officials, including Chair Yellen, pointed (although very cautiously) to the potential overvaluation of assets. This could mean that financial stability is gaining some interest in the monetary policy decision mix.

- The eco calendar is thin with only US pending home sales, EMU M3 money supply and a US 7-yr Note auction. Today is also the final day of the ECB forum in Sintra.

Currencies: EUR/USD And EUR/GBP Testing Key Resistance Levels

Draghi propels euro. Yellen fails to help the dollar

The stalemate in USD trading ended yesterday, as ECB's Draghi said the economic improvement could lead to a gradual ECB policy change. The euro jumped higher. Later on, the dollar was sold as the IMF downgraded its US growth forecast and the vote on the US health care bill was delayed. EUR/USD jumped north of 1.13. Fed's Yellen repeated her intention to continue a gradual rate hike path, but it couldn't help the dollar, at least not against the euro. EUR/USD closed the day at 1.1339. USD/JPY behaved differently. The rise in core yields and sharp gains in EUR/JPY pushed USD/JPY beyond the 112.13 resistance even as US equities came under pressure. The pair closed the session at 112.35.

This morning, Asian equities trade with modest losses as the sell-off in the tech sector in the US continues to weigh. At the same time, yields remain under upward pressure, while oil struggles to continue its recent rebound. EUR/USD is holding near the rally highs, currently trading in the 1.1347 area. USD/JPY tries to sustain north of 112, but the momentum eases as correction of tech equities tends to support the yen.

Today, the eco calendar is again thin. There are only second tier eco data in Europe, while in the US, the trade balance and inventory data won't affect USD trading. Investors will ponder the impact of yesterday's comments/events and will also keep a close eye at the final day of the ECB forum in Sintra, with comments from ECB's Draghi, BOJ's Kuroda and former Fed president Bernanke. It's is too early to firmly conclude that the global policy normalisation has started, but tentative signs of such process are multiplying. Even so, investors focus primarily on adapting positions to the ECB change of tone. The euro should remain well supported short-term. Will EUR/USD be able to take out the 1.1366 resistance? The FX reaction to a further equity correction is a less straightforward. For now, USD/JPY and EUR/JPY are supported by higher core yields, but this pattern probably won't continue in case of a more protracted equity correction. In this context we stay cautious on further USD/JPY gains, despite the recent good performance. The euro is currently favoured over the dollar. Short-term there is no reason to row against the euro positive tide. However, we are not convinced on the safe haven characteristics of the euro in case of a protracted global risk-off correction. We continue to keep a close eye at EUR/JPY. A reversal in this cross rate at some point might also cap the topside of EUR/USD.

Technical picture: USD still confined to tight ranges

Early May, EUR/USD failed to break below the 1.0821/1.0778 support (gap). Poor US data and US political upheaval propelled EUR/USD to a test of the 1.1300 area going into the FOMC decision, but the test was rejected. Yesterday, a combination of hawkish ECB comments and negative US headlines pushed EUR/USD for an intensive test of the 1.1300/66 resistance are. The test is ongoing. A sustained break would be significant from a technical point of view and could open the way to the 1.1616/1.1714 LT correction tops A return below 1.12 (STMA) would be a first indication that the euro rally is easing. A drop below 1.1119 would call off the downward alert.

The USD/JPY rally ran into resistance in early May and the pair returned lower in the 108.13/114.37 range. The post-Fed USD rebound pushed the pair beyond a first minor resistance at 110.81. The pair yesterday regained the 112.13 correction top, but the test is ongoing . A break would improve the ST-picture. Even so, were remain cautious on further USD/JPY gains as equity volatility tends to rise

EUR/USD: 1.1300/66 resistance under heavy strain on Draghi comments and negative US headlines

EUR/GBP

EUR/GBP retests 2017 top

Yesterday, the Draghi comments sent EUR/GBP-well north of 0.88, but there were also modest positive spill-over effects on cable. In the financial stability report, the BOE warned on easing credit standards for consumer credit. The bank increased the cyclical capital buffer from June 2018. The measures is a kind of monetary tightening and might make a rate hike (slightly) less probable. Especially EUR/GBP remained well bid after the financial stability report and closed the session at 0.8863. Cable profited from a soft dollar and closed the day at 1.2814.

This morning, the only release of the day, Nationwide UK House prices rose more than expected, but without market impact. So, sterling trading will be driven by global factors (euro strength) and by political/Brexit headlines. The news flow on UK politics remains diffuse, at best and the euro is in good shape. So, there is no reason to row against the EUR/GBP uptrend. A negative risk sentiment, if it would continue, is also more negative for sterling than for the euro.

From a technical point of view, EUR/GBP is again testing the 0.8854/66 area (2017 top). The BoE debate on a rate hike caused some volatility recently, but wasn't able to support sustained sterling gains against the euro. A break of the 2017 top would open the way to the 0.90 area. A return below the 0.8655 correction low would indicate easing pressure on sterling. Such a break lower will be difficult. A EUR/GBP buy-on-dips approach remains favoured

EUR/GBP: testing key resistance at 0.8854/66

Draghi’s Hawkish Tapering Speech Sends The Euro Higher

ECB President Mario Draghi was speaking in Portugal yesterday where he signaled that from September, the ECB would cut back its bond purchases from the current 60 billion euro to 40 billion euro a month. The talk of tapering sent the euro surging higher on the day, breaking past 1.1300 as a result.

Draghi also signaled that the central bank could adjust its monetary policy tools, currently at sub-zero rates. With the markets putting pressure on the ECB and expecting the hawkish talk, the euro rallied strongly.

Elsewhere, the economic calendar included a late evening speech from Janet Yellen at the British Academy in London. She did not go into much details about the Fed's monetary policy, but Ms. Yellen signaled that major banks were in a much stronger position than before. She also said that it was unlikely for the financial crisis to occur.

Looking ahead, the economic data includes continued speeches from major central bank officials. Thisincludes, ECB's Mario Draghi, BoC President Poloz, Mark Carney and BoJ President Kuroda

EURUSD intraday analysis

EURUSD (1.1350): With the EURUSD posting strong gains and rising above 1.1300, the price action looks bullish from here. Further gains could be seen coming with any pullbacks limited to 1.1300. However, in terms of the fundamentals, there is scope for the common currency to give up its gains especially with this Friday's flash inflation estimates. Therefore, the current gains in EURUSD could be seen as a rally led by market expectations. With a good two months to go, there is scope for the ECB to readjust its forward guidance as well. In the near term, EURUSD remains poised to the upside with initial support seen at 1.1300.

GBPUSD intraday analysis

GBPUSD (1.2826): The British pound extended the gains back to 1.2800 yesterday and slightly closing above this resistance level. Any pullback off this resistance level could see GBPUSD post some declines back to 1.2660 region, where the right shoulder of the inverse head and shoulders pattern could be formed. This would suggest further upside in price. GBPUSD has scope for afurther rally towards 1.3200 at the minimum. The falling median line also shows that price action will need to post a higher low ahead of further gains.

USDJPY intraday analysis

USDJPY (112.10): USDJPY also closed higher on the day surprisingly, despite the weakness in the US dollar. With price lingering near the resistance level of 111.61, there is scope for a pullback in price. Support has now moved up to 111.72 level. This marks the top of the bull flag rally. Yesterday's gains towards 112.44 marked the 127.2% Fibonacci extension level of the bull flag pattern. The next target remains at 113.36 with the pullback to the support at 111.72 likely to limit the declines.

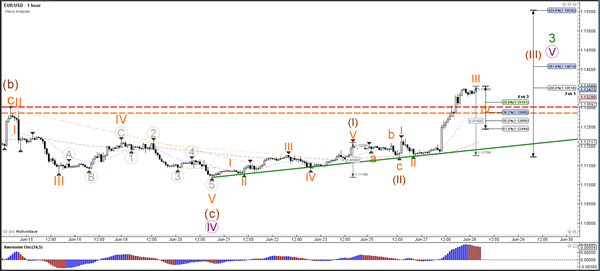

Daily Technical Analysis: EUR/USD Breaks Above Massive 1.13 Resistance And Continues Uptrend

Currency pair EUR/USD

The EUR/USD broke above the critical and important resistance levels at 1.13 (dotted orange and red lines) which invalidated the bearish wave structure. Price also has managed to finally break the sideways range which was indicated by support (blue) and resistance (red/orange). The bullish break makes an uptrend continuation which is reflected in the alternative and new wave structure: price has broken above the 161.8% Fibonacci level which makes a wave C unlikely a wave 3 (blue/green) more likely.

The EUR/USD is showing strong bullish momentum which is most likely a wave 3 (orange). Once the wave 3 is completed, the EUR/USD will most likely build a light retracement within wave 4 (orange) of a larger wave 3 (brown). The wave 4 is invalidated if price manages to break below the 61.8% of wave 4 vs 3.

Currency pair USD/JPY

The USD/JPY is moving higher within a wave 5 (orange) of wave C (brown). A break above the top of the channel (red) could see price move towards the Fibonacci targets of wave C (brown).

The USD/JPY needs to break above the resistance trend lines before a bullish continuation is likely. A break below support could indicate that the waves 5 are completed.

Currency pair GBP/USD

The GBP/USD is building an ABC (grey) zigzag within wave 2 (blue). A wave 2 (blue) becomes unlikely if price manages to break above the 200% Fib and resistance trend line (red).

The GBP/USD bullish momentum is most likely a wave 3 (purple) which means that price could be retracing within a wave 4 (purple). A break below the 61.8% Fib of wave 4 vs 3 and the trend line (blue) invalidates the wave 4.

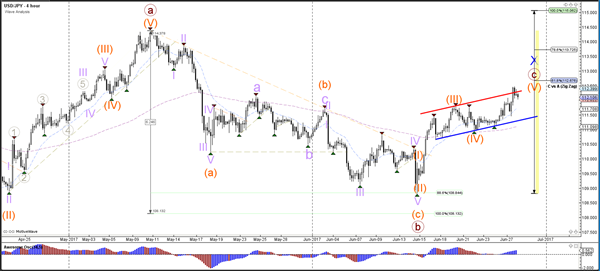

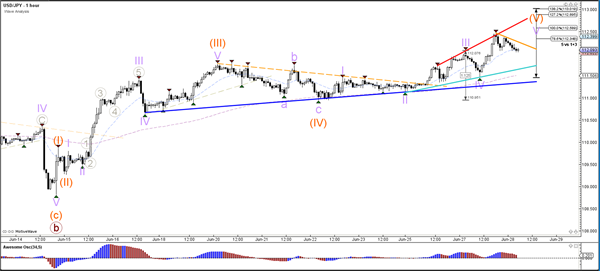

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

We typically search for lower-timeframe confirmation between the M15 and H1 timeframes, since most of our higher-timeframe areas begin with the H4. Stops are usually placed 1-3 pips beyond confirming structures.

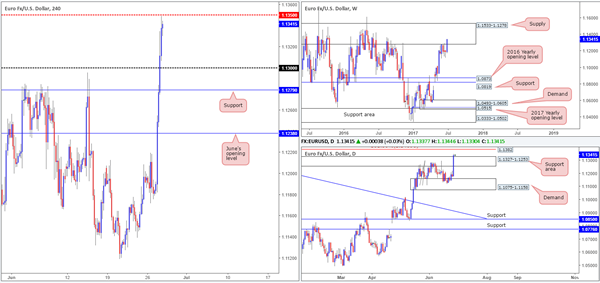

EUR/USD

In response to ECB President Mario Draghi's comments yesterday, the EUR shifted northbound and swallowed June's opening level at 1.1238. The dollar continued to sink throughout both the London and US sessions, despite US consumer confidence coming in higher than expected. The day ended with the single currency topping just ahead of the H4 mid-level resistance at 1.1350.

Over on the daily chart, the recent bout of buying also saw price trade through a resistance area coming in at 1.1327-1.1253, consequently opening up the path north to a daily Quasimodo resistance level seen at 1.1382. Weekly action on the other hand remains trading within the walls of a major weekly supply at 1.1533-1.1278.

Our suggestions: Quite simply, the main interest today is the daily Quasimodo resistance at 1.1382. Not only is the level fresh, it's also positioned within the weekly supply mentioned above and is located just below a daily AB=CD 161.8% ext. at 1.1409 and the psychological band 1.14. Given this, a short from 1.1382, with stops placed above 1.1409, is certainly an option today.

Data points to consider: ECB President Mario Draghi speaks at 2.30pm. US Pending home sales at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.1382 (stop loss: 1.1415).

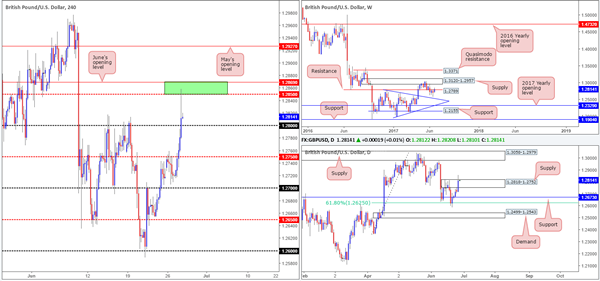

GBP/USD

In a similar fashion to the EUR/USD the GBP/USD also went on the offensive yesterday. Chomping its way through the H4 mid-level resistance at 1.2750 and 1.28 handle, the unit ended the day crossing swords with 1.2869/1.2850 (June's opening level/mid-level resistance – green area).

Daily supply at 1.2818-1.2752, thanks to yesterday's advance, suffered a rather aggressive whipsaw. A truckload of stop-loss orders have likely been triggered here, possibly clearing the path north up to daily supply drawn from 1.3058-1.2979. However, to prove genuine consumption here, we would require a daily close to take shape beyond this area.

Our suggestions: Entering long from the 1.28 handle today is not something we'd recommend, as it's difficult to know if the current daily supply is truly consumed. A H4 decisive close below 1.28 may signal buyer weakness, but is not a move we would consider trying to sell. Therefore, our desk will remain on the sidelines for the time being and reassess price action going into tomorrow's open.

Data points to consider: BoE Gov. Carney speaks at 2.30pm. US Pending home sales at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

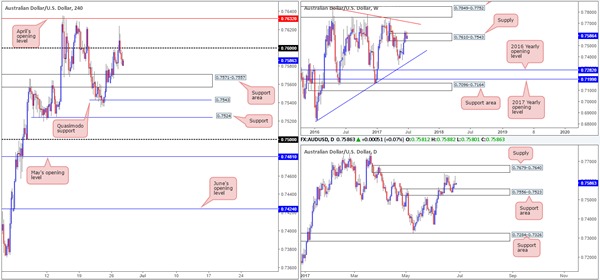

AUD/USD

Failing to sustain gains beyond the 0.76 handle, the commodity currency concluded yesterday's trade relatively unchanged. Consequent to this, a bearish daily selling wick took shape and could potentially send the unit south to retest the daily support area drawn from 0.7556-0.7523. Weekly price, as you can see, remains consolidating within the walls of supply coming in at 0.7610-0.7543.

Similar to Tuesday's report, between 0.76 and the H4 support area at 0.7571-0.7557 (located just above the aforementioned daily support area), we have thirty pips of room to play with. While this is enough to profit if one is able to pin down a tight stop loss, it is not something we will be looking into.

Beyond 0.76 we see April's opening level at 0.7632, a line that happens to be positioned eight pips below the underside of a daily supply area at 0.7679-0.7640. Below the current H4 support area, there's not much room for price to stretch its legs. Close by is a H4 Quasimodo support at 0.7543, followed by H4 support at 0.7524. As is evident from the H4 timeframe, the unit remains restricted as far as structure is concerned.

Our suggestions: On account of the above, neither a long nor short seems attractive at this time. With that being the case, our team, once again, intends to watch today's action from the safety of the bench and will look to reassess price action going into tomorrow's open.

Data points to consider: US Pending home sales at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

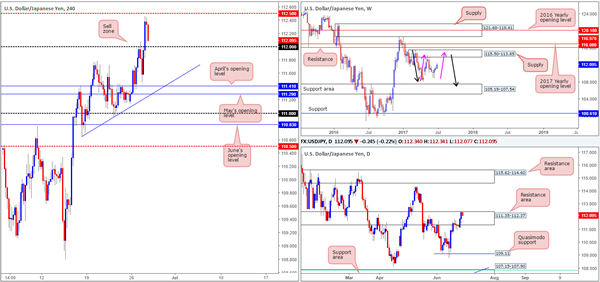

USD/JPY

For those who read Tuesday's report you may recall that our desk underscored the 112 handle as a particularly interesting level to short from. This was due to 112 merging with a left shoulder i.e. a H4 Quasimodo pattern at 112.05, and also being sited within a daily resistance area at 111.35-112.37 as well as converging closely with a H4 AB=CD 127.2% ext. at 112.09 taken from the low 110.64. As you can see, price responded beautifully to 112 and dropped to a low of 111.46, before reversing into the London open. Well done to any of our readers who managed to jump aboard here.

With weekly price showing room to advance up to supply pegged at 115.50-113.85, in the shape of a weekly AB=CD correction (see pink arrows), and daily flow teasing the upper edge of the said daily resistance area, selling is not something we are keen on.

Our suggestions: Although we are not keen sellers right now, buying from the 112 neighborhood without any H4 confluence present is also not a trade we could be confident in unfortunately. As such, our team is reluctant to commit to this market today.

Data points to consider: BoJ Gov. Kuroda speaks at 2.30pm. US Pending home sales at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

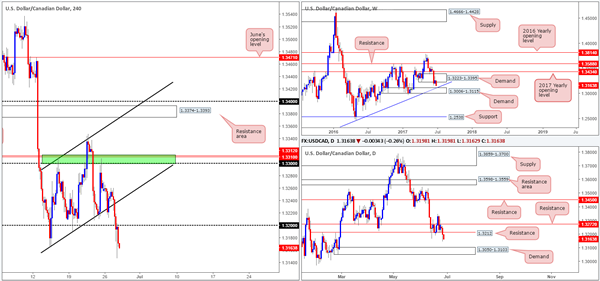

USD/CAD

As anticipated, the H4 ascending channel formation (1.3165/1.3308) gave way during yesterday's sessions. This was something we mentioned in past reports, and the reason we believed this to be the case was not only did we have daily resistance at 1.3272 in play, but let's also not forget that the current weekly demand was also hanging on by a thin thread.

In seeing that H4 price breached the 1.32 handle, our desk is predominantly bearish right now. The reason for this, other than the recent break of 1.32, is simply due to daily support at 1.3212 also being engulfed. Technically speaking, this has possibly cleared the path south down to a daily demand area coming in at 1.3050-1.3103, which happens to be positioned within the walls of a weekly demand at 1.3006-1.3115/weekly trendline support extended from the high 1.1278 (the next downside target on the weekly timeframe).

Our suggestions: We mentioned in yesterday's report that should 1.32 be consumed and retested as resistance, we would consider shorting this market and targeting the top edge of the weekly demand at 1.3115. Well, given the recent bearish rejection seen from the underside of 1.32, we have decided to sell at market from 1.3171, with a stop positioned at 1.3205 (34pips). Now, the distance to the take-profit is 56 pips, so there's at least one and a half times the risk to be had here.

Data points to consider: US Pending home sales at 3pm, followed closely by Crude oil inventories at 3.30pm. BoC Gov. Poloz speaks at 2.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (Stop loss: N/A).

- Sells: 1.3171 ([live] stop loss: 1.3205).

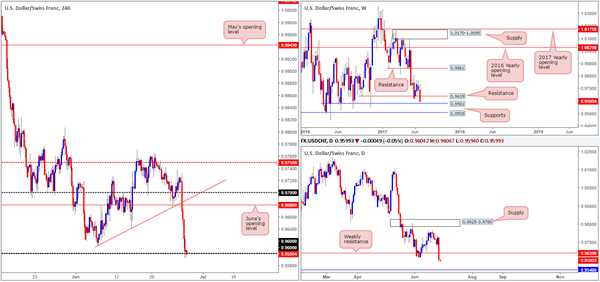

USD/CHF

Beginning with the weekly timeframe this morning, we can clearly see that price is now trading within shouting distance of a weekly support level coming in at 0.9581. Looking down to the daily timeframe on the other hand, support does not come into view until we reach 0.9546.

Over on the H4 timeframe, however, the 0.96 handle is currently seeing some action, following yesterday's rather one-sided move south. With the bulls failing to print anything of note from 0.96 as of yet, this could lead to a break of this level. Be that as it may, trying to short this move could end in tears since let's remember that only 20 pips below sits weekly support at 0.9581, and 35 pips below that is daily support at 0.9546.

Our suggestions: With stop-loss orders below 0.96 just begging to be filled, along with breakout sellers' orders (this will likely provide liquidity for the big boys to buy), we believe a long trade from between 0.9546/0.9581 is high probability today. To be on the safe side, we would only consider a buy from here in the event that a H4 bullish engulfing candle takes shape. This will, for us, confirm buyer intent.

Data points to consider: US Pending home sales at 3pm GMT+1.

Levels to watch/live orders:

- Buys: 0.9546/0.9581 ([waiting for a reasonably sized H4 bull candle to form – preferably a full-bodied candle – following the retest is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

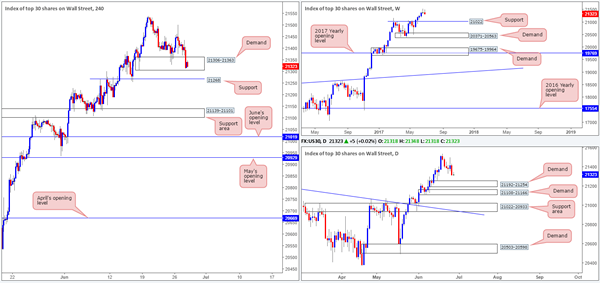

DOW 30

The H4 demand at 21306-21363 is now seen under pressure, following yesterday's selloff. For those who follow our analysis on a regular basis, you may recall that our desk is currently long from 21164. 50% of that position was quickly liquidated at 21234, with the remaining 50% left in the market to run since we intend on trailing this trend long term. Therefore, recent price action is particularly concerning for us considering that we have a stop-loss order located just beneath this zone!

Should the current H4 demand base be taken out, it is likely that the unit will challenge H4 support pegged at 21268, which happens to be located just above daily demand fixed at 21192-21254. For that reason, looking to sell the breakout beneath the said H4 demand is not something we would recommend.

Our suggestions: At the time of writing, there is not much else to hang our hat on. Of course, we would like to see the aforementioned H4 demand stabilize price, but judging H4 price action right now, it's likely to punch lower today.

If that's the case, why not then look for longs from the 21268 neighborhood? Personally, entering into a buy position just beneath a broken demand base, which could act as a resistance area, is too much of a risk in this situation.

Data points to consider: US Pending home sales at 3pm GMT+1.

Levels to watch/live orders:

- Buys: 21164 ([live] stop loss: 21298).

- Sells: Flat (stop loss: N/A).

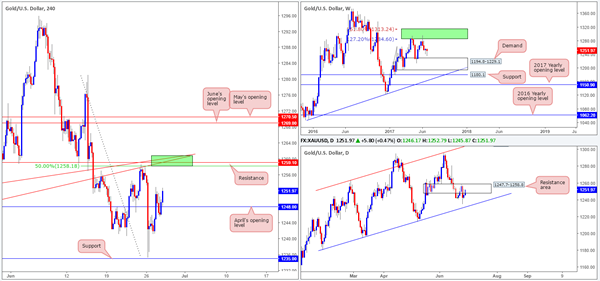

GOLD

Looking at this market from the top this morning shows that weekly price is on course to print yet another buying tail, just ahead of weekly demand coming in at 1194.8-1229.1. What's also interesting is that daily action is seen retesting a resistance area at 1247.7-1258.8.

Jumping across to the H4 timeframe, we can see that the bulls have found a temporary home above April's opening level at 1248.0. Continual buying here could see the H4 candles connect with the green H4 area which we deem to be a sell zone. The reasons as to why are as follows:

H4 resistance at 1259.1.

Two H4 trendline resistances taken from lows of 1245.9/1252.9.

H4 50.0% retracement value at 1258.1 taken from the high 1281.1.

Located within the upper limits of a daily resistance area at 1247.7-1258.8.

Our suggestions: H4 price is likely to test the above noted green H4 sell zone today. However, with little weekly connection seen around this area, there's a chance that a fakeout could take shape. Therefore, we will only consider a sell from here valid if, and only if, a H4 bearish candle forms, preferably a full-bodied candle.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1259.1 region ([waiting for a reasonably sized H4 bear candle – preferably a full-bodied candle – to form before pulling the trigger is advised] stop loss: ideally beyond the candle's wick).

Market Update – Asian Session: China Beige Book And CASS Think Tank See Robust Q2 Growth

US Session Highlights

(US) APR S&P / CASE-SHILLER 20-CITY M/M: 0.28% V 0.50%E; Y/Y: 5.67% V 5.90%E; HOUSE PRICE INDEX (HPI): 197.19 V 195.38 PRIOR

(US) JUN RICHMOND FED MANUFACTURING INDEX: 7 V 5E

(US) JUNE DALLAS FED MANUFACTURING ACTIVITY: 15.0 V 16.0E; new orders 6 v 0 prior

(US) JUN CONSUMER CONFIDENCE: 118.9 V 116.0E

(US) FDA to take new steps to improve prescription drug competition; to expedite review of generic drug applications

(CN) Trump administration reportedly mulling tougher stance on China trade which could include steel tariffs - press

(US) Fed's Harker (hawk, voter) still supports one more rate hike this year; inflation weakness likely temporary

(US) Sen Cornyn (R-TX): Senate will vote on healthcare bill this week; expects to have support to get it done

Stocks fell across the board today, with technology showing the largest losses, as the Nasdaq dropped 1.6%. The S&P was not far behind; it had its lowest close in 6 weeks. Investors have begun to take note of the downward movement, as the VIX increased 10% to 11.06, its highest close in 2 weeks. Financials rose 0.5% on the day, the only sector posting gains.

US markets on close: Dow -0.5%, S&P500 -0.8%, Nasdaq -1.6%

Best Sector in S&P500: Financials

Worst Sector in S&P500: Technology

Biggest gainers: SIG +4.6%; DRI +2.9%; CHK +2.8%

Biggest losers: ARNC -9.0%; STX -6.8%; NFLX -4.1%

At the close: VIX 11.1 (+1.2pts); Treasuries: 2-yr 1.37% (+1bps), 10-yr 2.20% (+6bps), 30-yr 2.74% (+4bps)

Politics

(US) President Trump: I just finished a great meeting with the Republican Senators concerning HealthCare. They really want to get it right, unlike OCare! - tweet

(VE) Venezuela President Maduro: Supreme Court building in Caracas suffered a "terror attack" by police helicopter - press

(JP) Japan chief cabinet secretary Suga: Defense Min Inada will continue to perform his duties; Remarks were reported to PM Abe, have no impact on timing of cabinet reshuffle - press

Key economic data

none seen

Asia Session Observations

Sentiment has turned more cautious as investors sold both Equities and Treasuries in US session, while the Vix jumped above 11. Euro spiked up over 1 big figure overnight on much less dovish comments from ECB President Draghi. USD/JPY is pulling back to 112 handle after rising above 112.40, while Nikkei225 has reversed its opening gains.

Takata briefly resumed trading, plunging over 40%; Toshiba is also struggling to close its chip unit sale on resistance from WDC.

Speakers and Press

China

(CN) PBoC adviser: Anticipates no further tightening of monetary policy in H2 - Chinese press

(CN) Bank of China (BOC) economists see China 2017 GDP around 6.8% - press

(CN) China Beige Book International (CBB) Q2 survey: Economy continues to improve

(CN) China Academy of Social Sciences (CASS): Q2 GDP estimated at 6.8% v 6.9% in Q1; 2017 GDP seen around 6.7% v around 6.5% official target - Chinese press

Japan

(JP) Japan PM Abe reportedly considering abandoning plans to balance the budget by FY20 in exchange for looser debt-to-GDP ratio target - press

(JP) Japan top banks sold off their JGB holdings to lowest level on record - Nikkei

Australia / New Zealand

(AU) Former RBA board member Edwards: RBA may raise interest rates as many as 8 times in 2018-19 - AFR

(NZ) According to latest RBNZ data, property investors borrowing in May fell to NZ$1.5B from NZ$2.5B y/y

(NZ) RBNZ Gov Wheeler: Outlook for growth remains positive - statement of intent outlining priorities

Korea

(CN) China National Petroleum Corporation (CNPC) suspends fuel sales to North Korea over concerns that it won’t get paid

Asian Equity Indices/Futures (00:00ET)

Nikkei -0.3%, Hang Seng -0.4%, Shanghai Composite +0.1%, ASX200 +0.3%, Kospi -0.2%

Equity Futures: S&P500 -0.1%; Nasdaq -0.3%, Dax flat, FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1330-1.1355; JPY 112.05-112.35; AUD 0.7580-0.7615; NZD 0.7260-0.7285

Aug Gold +0.5% at 1,253/oz; Aug Crude Oil -0.2% at $44.14/brl; Sept Copper +0.2% at $2.66/lb

(US) Weekly API Oil Inventories: Crude: +0.9M v -2.7M prior

(CN) PBOC SETS YUAN MID POINT AT 6.8053 V 6.8292 PRIOR; strongest Yuan fix since June 19th

(CN) PBoC: To skip today's open market operation (OMO); 4th consecutive skip

(CN) China MOF sells 3-yr bonds at 3.4349% v 3.42%e; bid-to-cover 2.73x

(AU) Australia sells A$800M in 2027 bonds; avg yield 2.4791%; bid-to-cover 3.5x

Asia equities notable movers

Australia

Sirtex Medical (SRX) +14.9%; To cut staff by 15%; to write off A$90M in R&D, performing within FY17 guidance

Nine Entertainment (NEC) +6.1%; Raises FY17 Reported EBITDA to A$200-210M; Sees FY17 reduction in the licensing fees that it has to pay, equal to ~A$33M (guided A$158-187M on May 2nd)

AusNet Services (AST) +2.5%; Raised at Credit Suisse

Japan

FujiFilm (4901) -1.1%; Files to delay financial results to July 31st

Toshiba (6502) -1.2%; CEO: Western Digital is unfairly obstructing the chip unit sale; Looking to resolve dispute at an early stage

Hong Kong

Yanzhou Coal (1171) +2.6%; Raised at HSBC

Kenford Group holdings (464) -7.1%; Reports FY17 (HK$) Net loss 22.2M v 22.5M y/y; Rev 495.4M v 522.9M y/y

Italy Will Be The First Euro Country To Release HICP Inflation For June

Market movers today

Data on euro area credit and M3 growth are due out today. While we estimate M3 continued to show around 5% yearly growth, we believe loan growth continued its upward trend. In particular, adjusted loans to NFCs increased from 1.9% in February to 2.4% in April. We estimate this increased further in May, as credit demand continued to increase.

ECB president Mario Draghi is due to participate in a Policy Panel at 15:30 CET at the ECB Forum on central banking in Portugal. The Fed's Williams is due to speak at 9:30 CET but the speech will be a reprise of the speech held yesterday.

Italy will be the first euro country to release HICP inflation for June. Consensus estimates a decline to 1.4% y/y from 1.6% y/y in May. Tomorrow, Germany and Spain are due to release inflation data, followed by the flash estimate for the euro area on Friday.

Data on the US trade balance and pending home sales are due for release.

Selected market news

Yesterday, EUR crosses soared and the German 10-year government benchmark bond sold off. The yield climbed some 5bp initially, following some hawkish comments from ECB President Mario Draghi. In a speech in Portugal, Draghi said, ‘as the economy continues to recover, a constant policy stance will become more accommodative and the central bank can accompany the recovery by adjusting parameters of its policy instrument – not in order to tighten the policy stance, but to keep it broadly unchanged' . Additionally, he said that ‘all the signs now point to a strengthening and broadening recovery in the euro area – deflationary forces have been replaced by reflationary ones'. Despite the hawkish comments, Draghi concluded that ‘a considerable degree of monetary accommodation is still needed for inflation dynamics to become durable and self-sustaining' (for more see Bloomberg, 27 June 2017). As the ECB, in our view, is currently too optimistic on wages and core inflation, we stick to our view that it will extend its QE purchases and continue its monthly purchases at EUR40bn per month in H1 18.

In the UK, the Bank of England (BoE) is set to ‘reduce' some of its stimuli by raising the countercyclical capital buffer to 0.5% and plans to increase the level to 1% in November 2018. According to the BoE's Financial Stability Report , each 0.5pp increase will swell the bank's cushion of common equity Tier 1 by GBP 5.7bn .

In the US, the Senate Republicans postponed a vote on the healthcare bill yesterday after resistance from members of their own party. According to conservative Republicans, the Senate bill does not do enough to erase Obamacare, whereas moderate Republicans are worried that millions of people will lose their insurance. The House of Representatives has passed its own version of the healthcare bill last month .

Yesterday in London, Fed Chair Janet Yellen reiterated that the Fed's balance sheet is set to be shrunk ‘gradually and predictably' and that the Fed intends to raise interest rates only gradually

European Open Briefing: The Euro Rallied After Hawkish Comments From ECB President Draghi

Global Markets:

- Asian stock markets: Nikkei down 0.35 %, Shanghai Composite gained 0.05 %, Hang Seng fell 0.30 %, ASX 200 rose 0.40 %

- Commodities: Gold at $1253 (+0.50 %), Silver at $16.80 (+1.25 %), WTI Oil at $44.15 (-0.25 %), Brent Oil at $46.90 (+0.05 %)

- Rates: US 10-year yield at 2.20, UK 10-year yield at 1.09, German 10-year yield at 0.37

News & Data

- PBoC Sets CNY/USD Mid-Point Fix At 6.8053 Vs Prev 6.8292 and Last Close 6.8145

- RBNZ: Outlook for Econ Growth Positive, But Considerable Uncertainties

- Financial System Sound, Key Domestic Risk Is Housing Market

- Fed's Yellen: We Believe Appropriate to Raise Rates Gradually

- Fed's Yellen: Even Though Jobless Rate Low, Below Level Colleagues See as Sustainable, Inflation Has Continued to Run Below Our Objectives

- Asia stocks pressured as Wall St. hit by healthcare vote delay – RTRS

Markets Update:

The Euro rallied after hawkish comments from ECB President Draghi. EUR/USD reached a high of 1.1355 in Asia. While it looks a bit overbought in the short-term, the pair is likely to find good support around 1.1300. Overall, further gains seem likely, with 1.1450 now the next notable resistance level.

GBP/USD recovered as well, although it has not been able to gather the same momentum as EUR/USD. The pair reached a high of 1.2825 in Asia. The break above 1.2810 resistance suggests GBP/USD could test 1.2970 soon. However, the topside is likely to be capped ahead of 1.30 amid on-going political uncertainty in the UK.

USD/JPY traded 112.05-35 overnight. The tech outlook remains positive, but broad USD weakness could weigh on the pair as well. Key support is seen at 111.50, while resistance lies ahead of 113.

USD/CAD broke below a key support level overnight, and it is likely that it will move towards 1.30 in the coming days. While falling oil prices would usually be bearish for the Canadian Dollar, it didn't have much of an impact in the last few trading weeks.

The main event today will be US crude oil inventories data. If the increase in inventory is larger than expected, WTI is likely to test 42.00 soon.

Upcoming Events:

- 07:45 BST – French Consumer Confidence

- 10:00 BST – Italian CPI

- 15:00 BST – US Pending Home Sales

- 15:30 BST – US Crude Oil Inventories