Sample Category Title

CAC Gains as Italy Cleans House with Bank Bailouts

The CAC index has started the week with strong gains. In the Monday session, the index has gained 0.94% and is currently trading at 5313.30 points. It's a quiet start to the week, with no eurozone or French numbers on the schedule. ECB President Mario Draghi will speak at the ECB Forum on Central Banking in Portugal.

It was anything but a quiet weekend in Rome, as the Italian government announced that would bail out two ailing banks, Banca Popolare di Vicenza and Veneto Banca. This deal will cost the Italian taxpayer 5.2 billion euros, and the government provided additional guarantees of 12 billion euros. Italy has already agreed to bail out another Italian bank, Monte dei Pashci di Siena, for up to 6.6 billion euros. The Italian government has set aside 20 billion euros to bail out struggling banks, and potentially may have used up the entire amount for these bailouts, depending on how the actual size of the bailouts. European stock markets have reacted positively to the move. On the CAC, bank stocks have posted gains, with Credit Agricole up 1.41% and BNP Paribas gaining 0.62%. These moves remove a major headache for European regulators and should strengthen the fragile Italian banking sector, which has had times been in crisis mode, threatening the stability of the eurozone financial sector.

Global stock markets have lost ground recently, as falling oil prices have weighed on energy sector stocks. Last week, the CAC dropped close to 1 percent. Brent crude has plunged 108% in June, as crude trades around $45 a barrel. As crude prices continue to fall, there are rising concerns of disinflation, and this has soured investor confidence. The US, Japan and much of Europe are struggling with low inflation, and lower levels could hamper economic growth. OPEC members continue to discuss lowering production in an effort to boost prices, but so far, their efforts have been for naught. OPEC is already bound by a production agreement and compliance is over 100%, yet this has failed to prevent the collapse in oil prices. Another headache for major producers is the increase in production from the US, Libya and Nigeria. If crude prices continue to head lower, we could see further drops on global stock markets.

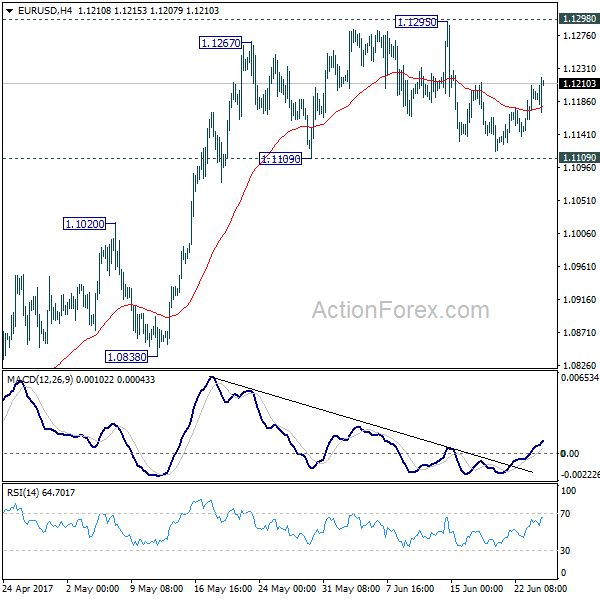

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1156; (P) 1.1182 (R1) 1.1219; More....

The consolidation from 1.1295 is still in progress and intraday bias in EUR/USD remains neutral. With 1.1109 support intact, there is no indication of reversal yet. Decisive break of 1.1298 key resistance will carry larger bullish implication and target 1.1615 resistance next. On the downside, break of 1.1109 support will indicate short term topping and rejection from 1.1298. In such case, intraday bias will be turned to the downside for 1.0838 support.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0941). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

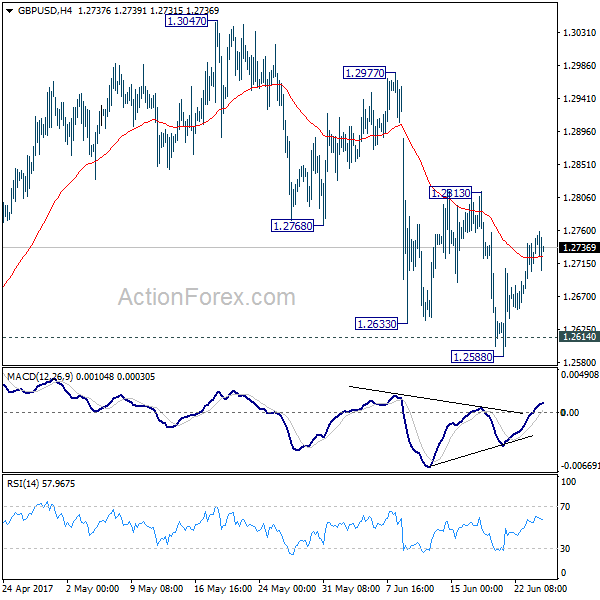

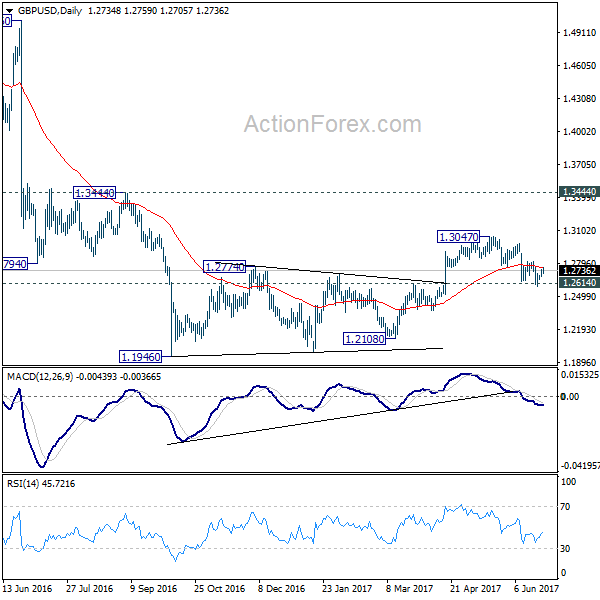

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2680; (P) 1.2711; (R1) 1.2748; More...

Intraday bias in GBP/USD remains neutral for the moment. With 1.2813 resistance intact, deeper decline is expected. Sustained break of 1.2614 resistance turned support will confirm our bearish view that consolidation pattern from 1.1946 has completed. In that case, deeper fall should be seen back to retest 1.1946 low. However, break of 1.2813 resistance will dampen our view and turn bias back to the upside for 1.3047 and above.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. Price actions from 1.1946 medium term low are seen as a consolidation pattern, which could have completed at 1.3047 after hitting 55 week EMA. Break of 1.1946 low will target 61.8% projection of 1.5016 to 1.1946 from 1.3047 at 1.1150 next. In case the consolidation from 1.1946 extends, outlook will stay remain bearish as long as 1.3444 resistance holds.

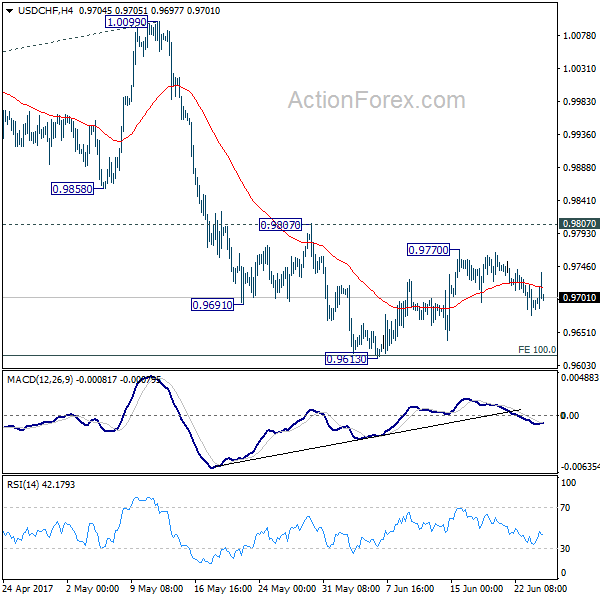

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9671; (P) 0.9696; (R1) 0.9717; More.....

Intraday bias in USD/CHF remains neutral at this point as consolidation from 0.9613 is still in progress. While another recovery cannot be ruled out, as long as 0.9807 resistance holds, further fall is expected. Break of 0.9613 will resume the decline from 1.0342 and target 0.9548 support and below. We'd start to look for bottoming signal again as it approaches 0.9443 key support level. On the upside, firm break of 0.9807 will indicate near term reversal and turn outlook bullish for 1.0099 resistance next.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

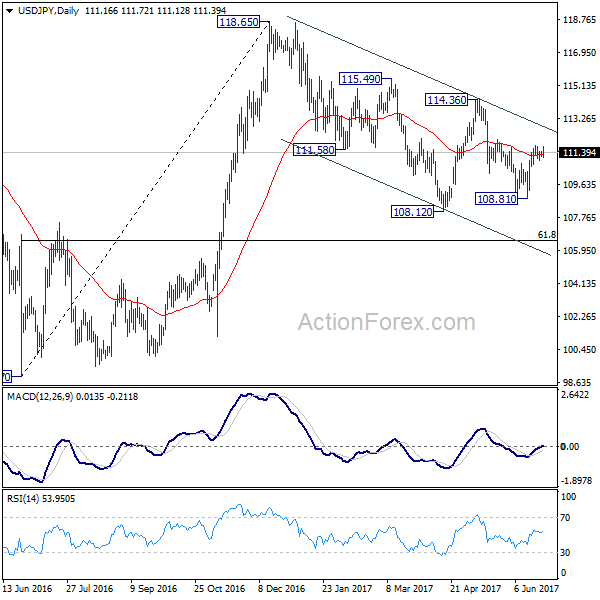

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.12; (P) 111.28; (R1) 111.40; More...

USD/JPY fails to take out 111.78 temporary top and stays in range. Intraday bias remains neutral for the moment. Further rise is favor with 110.63 minor support intact. Above 111.78 will target channel resistance (now at 112.82). Sustained break there will suggest that whole pull back from 118.65 has completed at 108.12 already. In such case, further rise should be seen to 114.36 resistance for confirmation. However, break of 110.63 will turn bias back to the downside for 108.81 instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

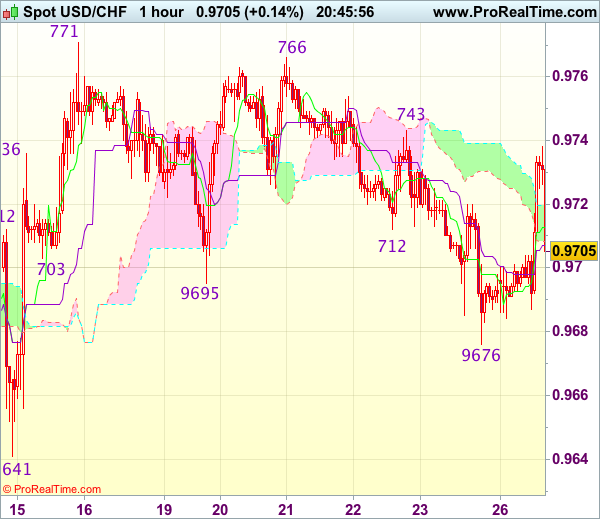

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 0.9703

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite intra-day brief rise to 0.9738, lack of follow through buying and current retreat suggest downside risk remains and test of support at 0.9676 (Friday’s low) cannot be ruled out, break there would signal the erratic fall from 0.9771 top is still in progress for retracement of recent rise, hence further weakness to 0.9660 would be seen, however, as broad outlook remains consolidative, still reckon downside would be limited to 0.9641 support, risk from there is seen for another rise to take place later.

On the upside, expect recovery to be limited to resistance at 0.9720 and price should falter below resistance at 0.9743, bring another decline later. Only a firm break above resistance at 0.9743 would revive bullishness and signal low is formed, bring test of 0.9766-71 resistance first. Once this resistance is penetrated, this would confirm recent rise from 0.9613 low has resumed for test of resistance at 0.9808, then towards another previous resistance at 0.9825.

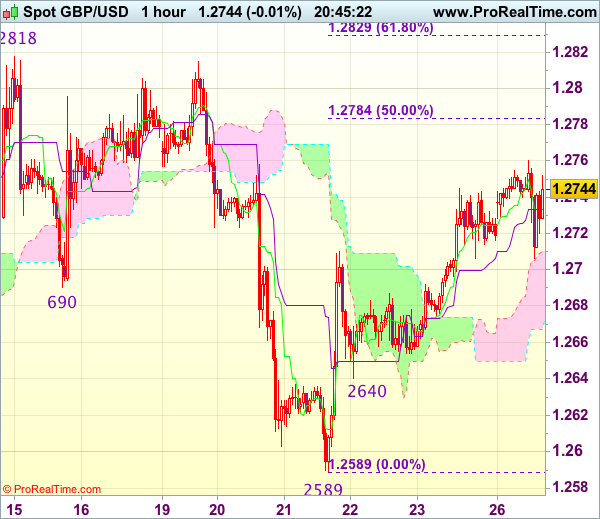

Trade Idea Update: GBP/USD – Stand aside

GBP/USD - 1.2737

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As cable has continued moving higher after last week’s strong rebound from 1.2589, suggesting near term upside risk remains for this move to bring retracement of recent decline to 1.2780-85 (50% Fibonacci retracement of 1.2978-1.2589), however, reckon upside would be limited to 1.2800 and price should falter below resistance at 1.2818, bring another selloff later.

In view of this, would not chase this move here and would be prudent to stand aside for now. Below 1.2705-10 would suggest an intra-day top is formed, bring weakness towards 1.2675-80 but break of latter level is needed to signal the rebound from 1.2589 has ended, bring retest of this level later.

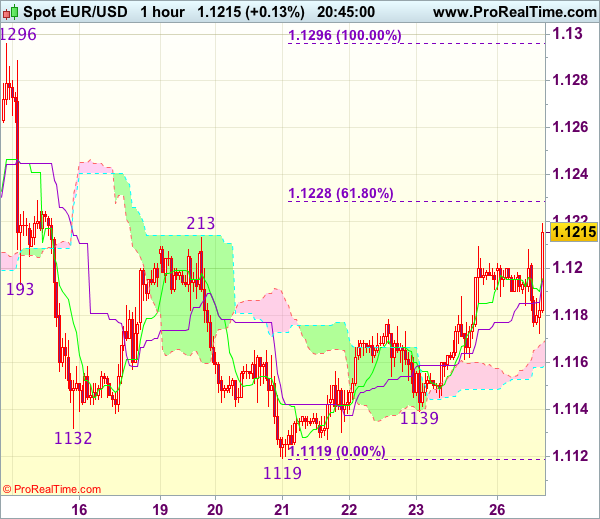

Trade Idea Update: EUR/USD – Stand aside

EUR/USD - 1.1216

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The single currency has risen again after brief pullback to 1.1172, retaining our view that near term upside risk remains for the rebound from 1.1119 (last week’s low) to extend gain to 1.1228-30 (61.8% Fibonacci retracement of 1.1296-1.1119), however, reckon upside would e limited to 1.1260-70 and price should falter well below resistance at 1.1296, bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below said intra-day support at 1.1172 would bring weakness towards 1.1139 support but break there is needed to revive bearishness and signal top is formed, bring retest of 1.1119.

Dollar Lower after Durables, Sterling Highs as Prime Minister May Struck a Deal With DUP

Dollar trades broadly lower today after weaker than expected economic data. Hawkish comments from Fed officials provide little support to the greenback. On the other hand, Canadian Dollar jumps as oil prices rebound. Sterling follows and is lifted broadly by political news in UK. Euro is supported by sentiments data which saw German Ifo hits record high. The greenback is only performing better than Japanese Yen and Swiss Franc. Released from US, durable goods orders dropped -1.1% in May versus expectation of -0.6%. Ex-transport orders rose 0.1% versus expectation of 0.4%.

Fed Dudley and Williams sound hawkish

New York Fed President William Dudley emphasized that "monetary policymakers need to take the evolution of financial conditions into consideration." And, "when financial conditions ease, as has been the case recently, this can provide additional impetus for the decision to continue to remove monetary policy accommodation." San Francisco Fed President John Williams emphasized that gradual tightening is needed to keep the economy healthy. Recent slowdown in inflation was seen by him as due to one-off factors. And he maintained his stance that a total of three hikes this year is still appropriate. His estimate of neutral policy rate is a little below 3.00%, comparing to the current 1.00-1.25%.

UK PM May struck a deal with DUP finally

Sterling is lifted by news that Prime Minister Theresa May has finally struck a deal with Northern Ireland's Democratic Unionist Party to secure a government majority. Under the agreement, DUP's 10 lawmakers will back May's over the Queen's Speech, national security and Brexit legislation. In return, May pledged extra GBP 1b in investment over the new two years, in addition to the GBP 0.5b committed. May said in a statement that "I welcome this agreement which will enable us to work together in the interest of the whole United Kingdom, give us the certainty we require as we embark on our departure from the European Union, and help us build a stronger and fairer society at home".

German Ifo hits record high

German Ifo business climate rose to 115.1 in June, up from 114.6 and beat expectation of 114.5. That's also the highest level on record since 1991 and the fifth straight monthly increase. Expectations rose to 106.8 versus consensus of 106.4. Current assessment also improved to 124.1 versus expectation of 123.2. Ifo President Clemens Fuest said in the release that "sentiment among German businesses is jubilant," and the economy is "performing very strongly." He added that "companies were significantly more satisfied with their current business situation this month" and they also expect business to improve. Looking closer to the detail, "demand and order books have both progressed very well. Production plans remain focused on expansion."

BoJ opinions: Crucial to maintain stimulus

According to summary of opinions of June BoJ meeting, policy members believed there is need to clear up communications to cool talk of stimulus exit. One member noted that "the price stability target cannot be achieved easily within a short time-frame." And, "it is crucial to maintain accommodative financial conditions and keep the economy expanding as long as possible". Another member noted that "it's necessary to continue with the current easy policy persistently and wait for a steady increase in demand and further falls in unemployment rate to lead to higher wages, prices and inflation expectations". Another member also said that "the timing of an exit cannot be foreseen as achievement of the price target is still considerably distant".

BIS urges policy makers to accelerate the "great unwinding"

The Bank of International Settlement said that even though there are still risks to the global economy due to high debt levels and low productivity growth, policy makers have to accelerate the "great unwinding" of quantitative easing program and low interest rates. The bank's head of research Hyun Song Shin said that "if we leave it too late, it is going to be much more difficult to accomplish that unwinding. Even if there are some short-term bumps in the road it would be much more advisable to stay the course and begin that process of normalization."

Meanwhile, BIS also named some risks for the global economy. It warned that "attention shifted away from monetary policy, and political events took center stage." Other than that, "a significant rise in inflation could choke the expansion by forcing central banks to tighten policy more than expected. Bedsides, "a withdrawal into trade protectionism could spark financial strains and make higher inflation more likely. Also, "policy normalization presents unprecedented challenges, given the current high debt levels and unusual uncertainty". Finally, "banks' continued reliance on short-term U.S. dollar funding remains a pressure point," and "questions remain about the resilience of funding under more stressed conditions."

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.12; (P) 111.28; (R1) 111.40; More...

USD/JPY fails to take out 111.78 temporary top and stays in range. Intraday bias remains neutral for the moment. Further rise is favor with 110.63 minor support intact. Above 111.78 will target channel resistance (now at 112.82). Sustained break there will suggest that whole pull back from 118.65 has completed at 108.12 already. In such case, further rise should be seen to 114.36 resistance for confirmation. However, break of 110.63 will turn bias back to the downside for 108.81 instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Summary of Opinions at June 15-16 Meeting | ||||

| 23:50 | JPY | Corporate Service Price Y/Y May | 0.70% | 0.70% | 0.70% | 0.80% |

| 08:00 | EUR | German IFO - Business Climate Jun | 115.1 | 114.5 | 114.6 | |

| 08:00 | EUR | German IFO - Expectations Jun | 106.8 | 106.4 | 106.5 | |

| 08:00 | EUR | German IFO - Current Assessment Jun | 124.1 | 123.2 | 123.2 | |

| 08:30 | GBP | BBA Mortgage Approvals May | 40.3K | 40.3K | 40.8K | 40.7K |

| 12:30 | USD | Durable Goods Orders May P | -1.10% | -0.60% | -0.80% | |

| 12:30 | USD | Durables Ex Transportation May P | 0.10% | 0.40% | -0.50% |

Trade Idea Update: USD/JPY – Buy at 110.65

USD/JPY - 111.40

Original strategy :

Buy at 110.65, Target: 111.65, Stop: 110.30

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.65, Target: 111.65, Stop: 110.30

Position : -

Target : -

Stop : -

Although the greenback rebounded after finding support at 110.95 last week and gain towards resistance at 111.79 (last week’s high) cannot be ruled out, break there is needed to signal recent upmove has resumed and extend headway to 111.90-95 (50% projection of 108.82-111.42-110.65), however, upside should be limited to resistance at 112.13 and 112.25 (61.8% Fibonacci retracement of 114.37-108.82 and 61.8% projection) should hold. If said resistance at 111.79 continues to hold, then further consolidation would take place and another retreat to 110.95 cannot be ruled out, however, previous support at 110.65 would limit downside and bring another rise later.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback as 110.65 support should limit downside. Below 110.30-35 (50% Fibonacci retracement of 108.82-111.79 and previous resistance turned support) would abort and signal a temporary top has been formed instead, risk weakness towards 109.95-00 (61.8% Fibonacci retracement).