Sample Category Title

Euro Zone Businesses Remain Optimistic About Economic Outlook

'The strong jobs growth was also a reflection of ongoing elevated levels of optimism about future growth.' — IHS Markit

Services activity in the 19-country bloc dropped unexpectedly in June, whereas manufacturing activity rose more than expected, a private survey released on Friday showed. IHS Markit reported that its preliminary PMI for the Euro zone's services sector fell to 54.7 points in June, following the preceding month's 56.3 and surpassing expectations for a slight decrease to 56.2. In the meantime, Markit's PMI for the region's manufacturing sector climbed to 57.3 points, up from the prior month's 57.0, while analysts expected a decline to 56.9. The composite PMI, a broad gauge of economic activity across the 19-country bloc's services and manufacturing sectors, dropped to 55.7 in June from May's 56.8 points. Nevertheless, the Index remained well above the 50-point level separating expansion from contraction. Moreover, the survey provided additional evidence that the economy was growing at a moderate, yet stable, pace amid strong optimism over the economic outlook for the region. Apart from that, the respondents pointed to solid employment and new orders growth in the region.

Trade Idea: EUR/JPY – Hold long entered at 123.80

EUR/JPY - 124.88

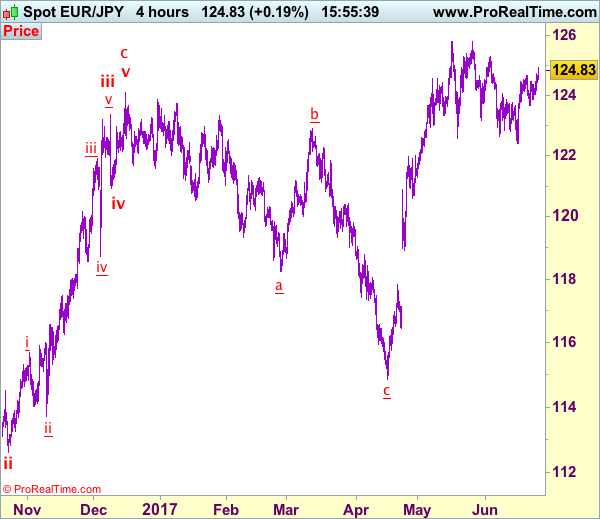

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term up

Original strategy:

Bought art 123.80, Target: 125.30, Stop: 123.60

Position: - Long at 123.80

Target: - 125.30

Stop: - 123.60

New strategy :

Hold long entered at 123.80, Target: 125.30, Stop: 124.00

Position: - Long at 123.80

Target: - 125.30

Stop:- 124.00

As the single currency has surged again after finding renewed buying interest at 123.66 last week and just broke above indicated resistance at 124.65, adding credence to our bullishness for the rise from 122.40 to extend further gain to indicated resistance at 125.31 but break of this level is needed to confirm correction from 125.82 has ended at 122.40, bring subsequent rise towards this recent high which is likely to hold on first testing.

In view of this, we are holding on to our long position entered at 123.80. Only below support at 123.66 would risk weakness to 123.20-25, break there would defer and suggest first leg of rebound from 122.40 has ended instead, risk further weakness to 122.90-00 but price should stay well above said support at 122.40, bring another rebound later.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Trade Idea: AUD/USD – Hold long entered at 0.7595

AUD/USD – 0.7563

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term up

Original strategy :

Bought at 0.7595, Target: 0.7745, Stop: 0.7535

Position: - Long at 0.7595

Target: - 0.7745

Stop: - 0.7535

New strategy :

Hold long entered at 0.7595, Target: 0.7745, Stop: 0.7535

Position: - Long at 0.7595

Target: - 0.7745

Stop:- 0.7535

Aussie did hold above indicated support at 0.7535 and has rebounded, retaining our bullish view and consolidation with upside bias remains for gain to 0.7600, above there would bring test of indicated resistance at 0.7636, break there would confirm recent upmove has resumed and extend the rise from 0.7329 towards previous resistance at 0.7680 but loss of momentum should limit upside to chart resistance at 0.7750 and price should falter below 0.7785-90.

In view of this, we are holding on to our long position entered at 0.7595. Below 0.7535 would defer and suggest top is possibly formed, bring correction to 0.7515-20, break there would provide confirmation, then correction to 0.7490-95 and possibly towards support at 0.7457 would be seen later.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

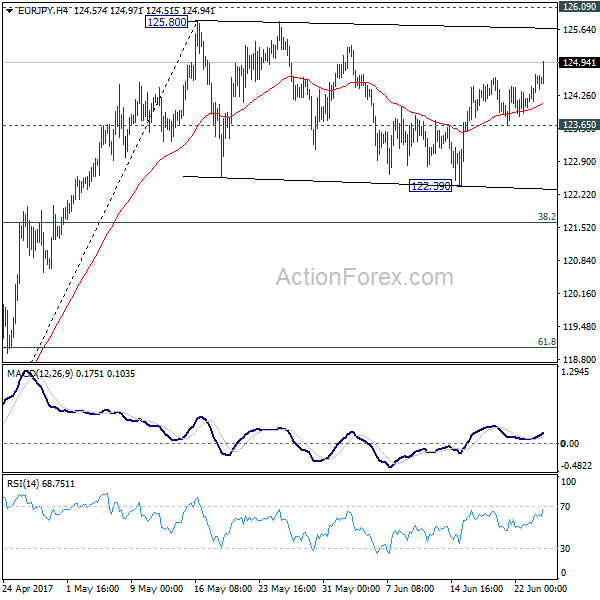

EUR/JPY Daily Outlook

Daily Pivots: (S1) 124.14; (P) 124.42; (R1) 124.83; More...

EUR/JPY rises notably today but it's staying below 125.80 resistance so far. Intraday bias stays neutral first as the consolidation from 125.80 might extend. Below 123.65 minor support will bring another falling leg towards 122.39. In that case, downside should be contained by 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rebound and then rise resumption. On the upside, decisive break of 125.80/126.09 resistance zone will extend the whole rise from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89.

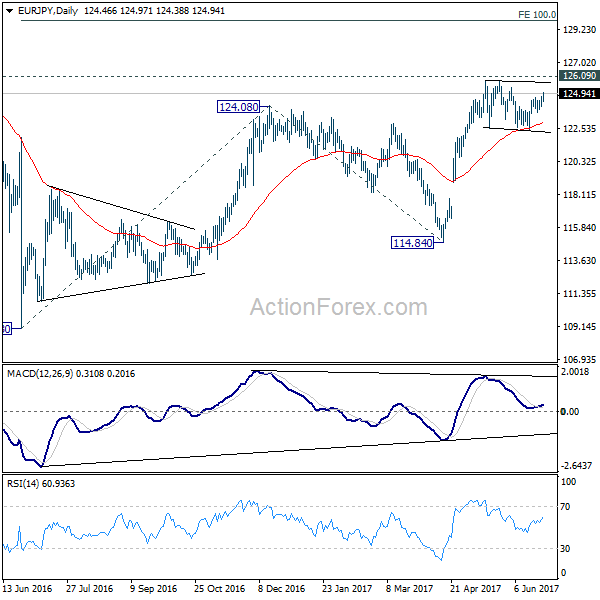

In the bigger picture, focus is staying on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

Yen Broadly Lower as Markets Sentiments Improved, BIS Urges “Great Unwinding”

Yen weakness broadly today as market sentiments improved. Major European indices open higher with FTSE and DAX up 0.5% at the time of writing while CAC is up 0.8%. The development is helped by recovery in oil prices as WTI is trading back above 43 after dipping to as low as 42.05 last week. Swiss Franc also follow Yen and trades mildly lower. Strength is seen in Sterling and commodity currencies but upside is limited so far. Gold, on the other hand, suffered steep selling to as low as 1236.5 earlier today and is back at 1244.

BoJ opinions: Crucial to maintain stimulus

According to summary of opinions of June BoJ meeting, policy members believed there is need to clear up communications to cool talk of stimulus exit. One member noted that "the price stability target cannot be achieved easily within a short time-frame." And, "it is crucial to maintain accommodative financial conditions and keep the economy expanding as long as possible". Another member noted that "it's necessary to continue with the current easy policy persistently and wait for a steady increase in demand and further falls in unemployment rate to lead to higher wages, prices and inflation expectations". Another member also said that "the timing of an exit cannot be foreseen as achievement of the price target is still considerably distant".

Fed Williams wants to continue with gradual tightening

In US, San Francisco Fed President John Williams emphasized that gradual tightening is needed to keep the economy healthy. And he warned that "if we delay too long, the economy will eventually overheat, causing inflation or some other problem." He said that "gradually raising interest rates to bring monetary policy back to normal helps us keep the economy growing at a rate that can be sustained for a longer time." He noted that "the very strong labor market actually carries with it the risk of the economy exceeding its safe speed limit and overheating, which could eventually undermine the stainability of the expansion.:" He also tried to talk down the slowdown in inflation and said it's "transitory".

BIS urges policy makers to accelerate the "great unwinding"

The Bank of International Settlement said that even though there are still risks to the global economy due to high debt levels and low productivity growth, policy makers have to accelerate the "great unwinding" of quantitative easing program and low interest rates. The bank's head of research Hyun Song Shin said that "if we leave it too late, it is going to be much more difficult to accomplish that unwinding. Even if there are some short-term bumps in the road it would be much more advisable to stay the course and begin that process of normalization."

Meanwhile, BIS also named some risks for the global economy. It warned that "attention shifted away from monetary policy, and political events took center stage." Other than that, "a significant rise in inflation could choke the expansion by forcing central banks to tighten policy more than expected. Bedsides, "a withdrawal into trade protectionism could spark financial strains and make higher inflation more likely. Also, "policy normalization presents unprecedented challenges, given the current high debt levels and unusual uncertainty". Finally, "banks' continued reliance on short-term U.S. dollar funding remains a pressure point," and "questions remain about the resilience of funding under more stressed conditions."

On the data front

Japan corporate service price index rose 0.7% yoy in May. German Ifo business roe to 115.1 in June versus expectation of 114.5. Expectations rose to 106.8 versus consensus of 106.4. Current assessment also improved to 124.1 versus expectation of 123.2. US will release durable goods orders. Looking ahead, economic data is the main focus this week. In particular, US will release consumer confidence and personal income and spending. Eurozone will release CPI flash. Japan will also release consumer inflation. Meanwhile, China will release PMIs. Here are some highlights:

- Tuesday: BoE financial stability report; US S&P Case-Shiller house price, consumer confidence

- Wednesday: Swiss UBS consumption indicator; Eurozone M3 money supply; US trade balance, whole sale inventories, pending home sales

- Thursday: Japan retail sales; German Gfk consumer confidence, CPI; Eurozone confidence indicators; UK Q1 GDP final, jobless claims

- Friday: UK Gfk consumer confidence; Japan CPI, household spending, unemployment, industrial production; China PMIs; German retail sales, unemployment; Eurozone CPI flash; UK Q1 GDP final; Canada GDP, IPPI and RMPI; US personal income and spending, Chicago PMI

EUR/JPY Daily Outlook

Daily Pivots: (S1) 124.14; (P) 124.42; (R1) 124.83; More...

EUR/JPY rises notably today but it's staying below 125.80 resistance so far. Intraday bias stays neutral first as the consolidation from 125.80 might extend. Below 123.65 minor support will bring another falling leg towards 122.39. In that case, downside should be contained by 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rebound and then rise resumption. On the upside, decisive break of 125.80/126.09 resistance zone will extend the whole rise from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89.

In the bigger picture, focus is staying on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Summary of Opinions at June 15-16 Meeting | ||||

| 23:50 | JPY | Corporate Service Price Y/Y May | 0.70% | 0.70% | 0.70% | 0.80% |

| 8:00 | EUR | German IFO - Business Climate Jun | 115.1 | 114.5 | 114.6 | |

| 8:00 | EUR | German IFO - Expectations Jun | 106.8 | 106.4 | 106.5 | |

| 8:00 | EUR | German IFO - Current Assessment Jun | 124.1 | 123.2 | 123.2 | |

| 8:30 | GBP | BBA Mortgage Approvals May | 40.3K | 40.8K | ||

| 12:30 | USD | Durable Goods Orders May P | -0.60% | -0.80% | ||

| 12:30 | USD | Durables Ex Transportation May P | 0.40% | -0.50% |

GBPJPY Advances For Fourth Consecutive Day, Exceeds 142.00 Handle

GBPJPY continued advancing today after closing higher for three days in a row. Today's movement has led the pair to record a near one-week high of 142.22.

The RSI is close to the 50 neutral level but it has risen considerably in recent days in order to reach its current level at 51. The indicator's movement, which is also upward sloping at the moment, is hinting to a bullish momentum in place for the pair. The stochastics are painting a similar picture. Specifically, the %K line has steeply risen in recent days and is in bullish territory. Moreover, it has crossed above the slow %D line.

The near three-week high of 142.52 form June 20 could act as a barrier to up movements in price. Further up, a resistance area might be formed by the current level of the 50-day moving average (MA) and the 38.2% Fibonacci retracement level of the April 17 to May 10 upleg, ranging from 143.04 and 143.31.

On the downside, the 50% Fibonacci at 141.82, which was exceeded today as the price was moving higher, could instead act as an intra-day support level. Below this level, the 141.00 handle could serve as psychological support, while further down, the 61.8% Fibonacci mark at 140.35 could provide additional support.

Turning to the medium-term picture, it is currently neutral with the price ranging since the start of the year and currently being in between the 50- and 200-day MAs.

To sum up, the short-term bias looks bullish and the medium-term is neutral.

Euro Holds Despite Italian Banking Bailout News, Dollar Remains Weak On Hike Odds

It was a relatively quiet start to the week for forex markets, as many Asian countries were closed because of the end of Ramadan.

The euro mostly held onto the gains it made before the weekend despite the news that the Italian government was going to rescue two of the country's regional lenders at the tune of 17 billion euros. Italian banking woes were seen as contained for now, given the positive political developments and the relative strength of the Eurozone economy.

In other news, San Francisco Fed President John Williams reiterated the Fed's mantra that monetary policy should continue to gradually tighten so as to prevent inflation from rising too fast. Although there have been some soft readings on inflation lately, the Fed's target of 2% should be met by next year, according to Williams. However, the seemingly hawkish talk failed to provide a boost to the US dollar as market participants remain skeptical about the chances of another Fed rate hike this year. Futures markets are currently putting the odds of such a rate hike at less than 50%.

Euro/dollar was trading around 1.12 during late Asian trading, while dollar/yen was at 111.48. The pound was doing relatively well as it traded around 1.2750 versus the dollar, as the chances of the DUP supporting a Tory government appeared improved during the weekend.

The US dollar could get a lift this week if the US senate manages to pass a Healthcare bill that would revoke the Affordable Care Act, which in turn would facilitate tax cuts by the Trump administration. This could help revitalize the so-called ‘Trump rally' in the dollar, as the greenback has given back all the gains it made following the election of Donald Trump as President in November of 2016.

In commodities, front-month US oil futures were stronger at $43.60 a barrel, while gold was slightly softer at $1255 an ounce.

Looking ahead, the German Ifo business sentiment survey for June will be released, while later in the day May durable goods orders will come out of the United States. After the European close, a speech by ECB president Mario Draghi will also be closely watched.

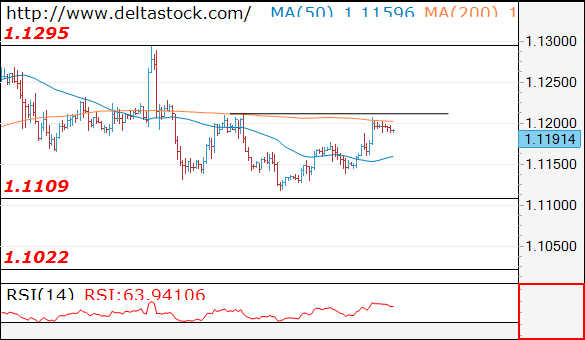

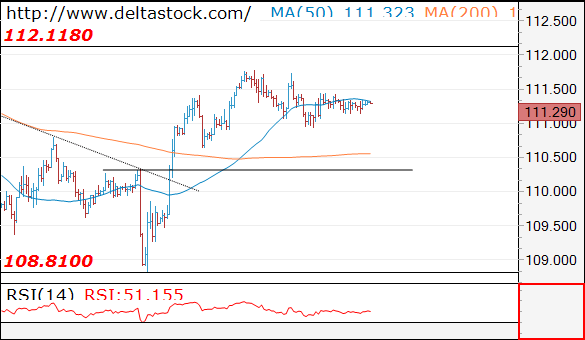

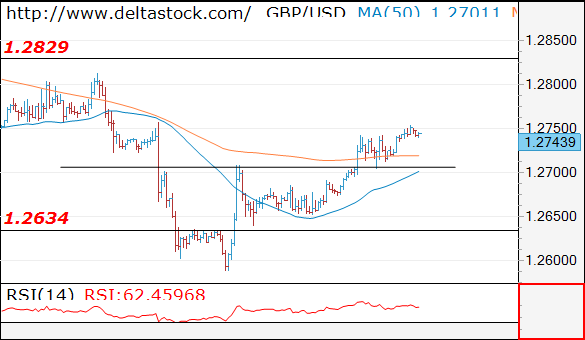

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1191

The intraday bias is positive above 1.1180 minor support, with a risk of a break through 1.1210 resistance, towards 1.1250 area. The latter should cap the upside, for another downswing to 1.1020 zone.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1210 | 1.1360 | 1.1180 | 1.1020 |

| 1.1295 | 1.1610 | 1.1110 | 1.0838 |

USD/JPY

Current level - 111.29

The consolidation pattern is still underway, with a risk of a dip to 110.30 before advancing beyond 111.80, towards 113.00 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.80 | 112.10 | 110.30 | 109.08 |

| 112.10 | 114.30 | 110.30 | 108.12 |

GBP/USD

Current level - 1.2743

The outlook is positive above 1.2700 support zone, for a rise towards 1.2825 major hurdle.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2825 | 1.2970 | 1.2700 | 1.2480 |

| 1.2825 | 1.3050 | 1.2634 | 1.2480 |

Market Update – Asian Session: FX Majors Quiet Ahead Of US Durable Goods Report

Asia Mid-Session Market Update: Takata enters bankruptcy; FX majors quiet ahead of US durable goods report

Friday US Session Highlights

(US) JUN PRELIMINARY MARKIT MANUFACTURING PMI: 52.1 V 53.0E

(US) MAY NEW HOME SALES: 610K V 590KE; Median price: $345.8K v $310.2K prior

Major indices in New York are mixed, firming up after some early downward momentum. A weaker than expected Markit manufacturing PMI reading sent the Dollar to a session low against the Yen, but markets were buoyed by a beat in US new home sales data just minutes later. USD/CAD spiked after Canada May CPI came in lower than anticipated, which is seen as muting BOC rate hike expectations. The energy complex has been lifted by crude prices bouncing off their lows, and healthcare names have retreated from yesterday's highs as attention remains on Washington's ACA repeal efforts.

Politics

(US) Sen Collins (R-ME) awaiting Congressional Budget Office review of Senate healthcare legislation proposal before deciding on whether she will support the bill - US press

(DE) Germany Social Democratic chancellery candidate Martin Schulz rejects a grand coalition lead by Angela Merkel’s CDU/CSU; Calls for Chancellor Merkel to go further in spurring "erratic" US Pres Trump - press

(JP) Japan PM Abe cabinet approval rating falls another 9pts to 39% - Yomiuri

(JP) Ahead of July 2nd metropolitan assembly election in Tokyo, ruling LDP party trails Gov Yuriko Koike's new political group "Tokyoites first" by 26.7% to 25.9% margin - Nikkei

Key economic data:

none seen

Asia Session Notable Observations

Takata finally succumbs to bankruptcy in New York and Japan filings; Trading suspended.

BoJ summary of opinions from last meeting reiterates concerns over slow progress in wage and price inflation while praising improved Consumption sentiment. Recall the last BOJ decision raises Consumption assessment while maintaining policy settings unchanged.

Approval rating for Japan PM Abe continues to crater amid unfolding political scandals.

PBoC sets Yuan firmer for the first time in 5 days; FX majors in very narrow ranges.

Speakers and Press

China

(CN) China’s National Development and Reform Commission (NDRC) has asked all coal miners to curb thermal coal prices at CNY570/t

(CN) China Premier Li calls for more investment in industries such as artificial intelligence, quantum science, gene editing, new materials and new energy - Chinese press

Korea

(KR) Bank of Korea (BOK) regional growth report: Economy is expected to see gradual improvement this year thanks to manufacturing and services

(KR) South Korea President Moon said to be under pressure to drop protectionism

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.1%, Hang Seng +0.4%, Shanghai +0.6%, ASX200 +0.1%, Kospi +0.4%

Equity Futures: S&P500 +0.1%; Nasdaq +0.1%, Dax +0.1%, FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1190-1.1200; JPY 111.15-111.35; AUD 0.7560-0.7585; NZD 0.7270-0.7290; GBP 1.2730-1.2755

Aug Gold flat at 1,256/oz; Aug Crude Oil +1.3% at $43.55/brl; Sept Copper -0.1% at $2.63/lb

(US) Weekly Baker Hughes US Rig Count: 941 v 933 w/w (+0.8%) (23rd straight weekly rise)

SPDR Gold Trust ETF daily holdings fall 3.0 tonnes to 851.0 tonnes

(CN) PBOC SETS YUAN MID POINT AT 6.8220 V 6.8238 PRIOR; first firmer Yuan fix in 5 sessions

(CN) PBoC: To skip today's open market operation (OMO); 2nd straight skip; Drains CNY50B

(KR) South Korea Finance Ministry sells 20-yr treasury bonds; avg yield 2.190%

Asia equities/Notables/movers

Hong Kong

epring Group (1884) +5.7%; Reports FY17 (HK$) Net 22.2M v 29.7M y/y; Rev 390.6M v 382.8M y/y

ICBC (1398) +0.6%; Responds to media reports that it had been ordered to assess credit risks, saying checks of loans to companies that made overseas acquisitions is routine

International Entertainment Corporation (1009) -2.5%; Reports FY17 (HK$) Net 66.1M v 45.2M y/y; Rev 290.7M v 330.9M y/y

Upbest Group (335) -8.0%; Reports FY17 (HK$) Net 225.9M v 518.2M y/y; Rev 317.5M v 443.4M y/y

Australia

Metcash (MTS) +3.4%; Reports FY17 adj Net A$194.8M v A$186Me; EBIT A$296.7M v A$287Me; Rev A$14.13B v A$14.1Be

Rio Tinto (RIO) +0.9%; Confirms receipt of revised proposal from Glencore plc to acquire Rio Tinto's wholly-owned Australian subsidiary; Yancoal considering matching Glencore bid for Coal & Allied - AFR

Japan

Kirin (2503) +0.5%; Looking to sell its dairy business, have received some interest in parts of the business, but the company is aiming to sell the entire operation - AFR

Honda (7267) flat; Takata decision has limited impact on FY17 earnings; no decision reached over inflator recall responsibilities; Nissan (7201) +0.1%; set aside appropriate reserve related to Takata recall

ECB’s Draghi To Speak Today

Over the weekend, ECB Governing Council member and Bundesbank president Jens Weidmann told a German newspaper Welt am Sonntag that the time might be nearing for the European Central Bank to begin discussions on ending its stimulus program. Mr. Weidmann, is one of the staunch opponents of the ECB's QE program and his comments over the weekend were therefore not surprising.

Looking ahead the economic data today includes a speech by ECB president Mario Draghi while in the U., the durable goods orders will be released.Headline durable goods ordersare expected to fall, while core durable goods orders are expected to post a modest recovery, rising 0.4% according to economists polled.

EURUSD intraday analysis

EURUSD (1.1193): The EUR/USD is seen trading within Friday's range today with price action seen well supported above 1.1129. After testing 1.1200 resistance on Friday, we could expect to see some downside bias in the EURUSD prevailing. On the 4-hour chart, following the upside breakout from the triangle pattern and with theprice at resistance, EURUSD could be seen range bound between 1.1200 and 1.1171 levels. A breakout below 1.1171 will signal a continuation to the downside with 1.1129 support coming into focus. Below 1.1129 further declines could be seen coming. Alternately, above 1.1200, EURUSD could potentially target the upside towards 1.1300.

GBPUSD intraday analysis

GBPUSD (1.2744): The British pound is seen pushing higher this morning after Friday closed above 1.2688. Further upside could see GBP/USD attempt another go at the resistance level of 1.2800 which was briefly tested just a a week ago. The current rally to 1.2800 could, therefore, be a short term recovery before the bias opens to the downside. With the test of 1.2800, GBPUSD could be potentially forming a head and shoulders pattern. Therefore, watch for a higher low after the resistance at 1.2800 is tested. On the 4-hour chart, any near-term decline could be seen held near the support level at 1.2688.

USDJPY intraday analysis

USDJPY (111.32): USDJPY which has been struggling to break the resistance level at 111.61 is likely to see a near term pullback in price. However, price action is attempting to retest this resistance level once again. This comes following the bullish breakout from the descending wedge pattern on the daily chart. On the 4-hour chart, we notice the bull flag pattern which signals continuation. Resistance at 111.72 - 111.61 will be key, and a breakout above this level is required for USDJPY to extend gains to a minimum of 113.360.