Sample Category Title

AUD in Tight Range as RBA Stands Pat, Yen Surges Against Dollar

Aussie stays in tight range today after RBA left cash rate unchanged at 1.50% as widely expected. The central bank also maintained a neutral stance and noted that "the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time." Regarding the economy, the statement pointed out that "year-ended GDP growth is expected to have slowed in the March quarter, reflecting the quarter-to-quarter variation in the growth figures." But Governor Philip Lowe is optimistic that "economic growth is still expected to increase gradually over the next couple of years to a little above 3 per cent."

Nonetheless, RBA also pointed out that "indicators of labour market remain mixed". While there was stronger employment growth, the growth in "total hours worked remains weak". Wage growth stays low and is "likely to continue for a while yet". And, as inflation will increase gradually, slow real wages growth will retrain growth in household consumption. RBA also stays alerted with the housing market. And it pointed out that "growth in housing debt has outpaced the slow growth in household income".

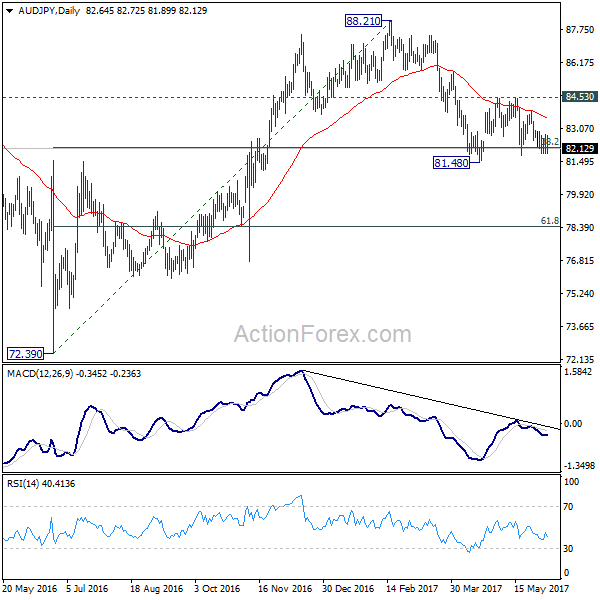

AUD/JPY gyrates in tight range after the release and overall outlook is unchanged. Recovery from 81.48 should have completed after failing to sustain above 55 day EMA. Fall from 88.21 is in expected to resume. Break of 81.48 will pave the way to 38.2% retracement of 72.39 to 88.21 at 78.43. This will be the favored case as long as 84.53 resistance holds.

Yen surges against dollar

Talking about Yen, it resumes recent rally against the greenback with USD/JPY diving through 110 handle. Markets are getting more nervous ahead of former FBI director James Comey's testimony before Senate Intelligence Committee on Thursday. Comey, dismissed by US President Donald Trump, will certainly be asked about the investigation into Russian interference in the presidential election last year. Also, Comey will be asked about Trump's interference in the investigation on former national security advisor Michael Flynn's tie to Russia.

Yesterday, the Intercept published a leaked report by the National Security Agency, detailing how Russian hackers conducted a spear-phishing scheme targeted at the US election infrastructure. And the scheme penetrated the system deeper than previously believed. The report was confirmed by the US government. Also, a private contractor was arrested for leaking the report to media.

Elsewhere...

UK BRC retail sales monitor dropped -0.4% yoy in May. Japan labor cash earnings rose 0.5% yoy in April. Australia current account deficit narrowed to AUD -3.1b in Q1. Looking ahead, Eurozone will release retail sales and Sentix investor confidence in European session. Canada will release Ivey PMI in US session.

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.27; (P) 110.50; (R1) 110.69; More...

USD/JPY's fall from 114.36 resumes by taking out 110.23 support an reaches as low as 109.65 so far. Intraday bias stays on the downside for 108.12 support next. Whole decline from 118.65 is seen as a correction and is still in progress. Break of 108.12 will target 61.8% retracement of 98.97 to 118.65 at 106.48. We'll look for bottoming signal around 106.48. On the upside, above 110.72 minor resistance will turn bias neutral first. But near term outlook will remain bearish as long as 111.70 resistance holds.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y May | -0.40% | -0.50% | 5.60% | |

| 0:00 | JPY | Labor Cash Earnings Y/Y Apr | 0.50% | 0.30% | -0.40% | 0.00% |

| 1:30 | AUD | Current Account Balance (AUD) Q1 | -3.1B | -0.5B | -3.9B | |

| 4:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Jun | 27.4 | 27.4 | ||

| 9:00 | EUR | Eurozone Retail Sales M/M Apr | 0.10% | 0.30% | ||

| 14:00 | CAD | Ivey PMI May | 62 | 62.4 |

Euro-Zone Business Activity Remained Steady In May

For the 24 hours to 23:00 GMT, the EUR declined 0.11% against the USD and closed at 1.1259.

On macro front, the final composite PMI in the Euro-zone remained unchanged at a level of 56.8 in May, in line with the flash estimate and analysts' expectations, supported by strong growth of new business. On the other hand, the Euro-zone's PMI services PMI inched lower to 56.3 in May from 56.4 reported in the previous month, but was slightly above the preliminary estimate of 56.2.

Meanwhile, Germany's composite PMI unexpectedly rose to 57.4 in May from 56.7 in April and was up from the flash estimate of 57.3. Additionally, the nation's services activity remained stable in May from last month, with the final PMI reading coming in at 55.4. Markets were expecting the index to fall to level of 55.2. The preliminary figures had also recorded a drop to 55.2.

The US Dollar pared its initial gains against other major currencies, after reports showed that activity in the US service sector slowed more than expected in May and the nation's factory orders fell for the first time in five months in April.

Data showed that the US ISM non-manufacturing PMI dropped to a level of 56.9 in May, snapping its four consecutive months of gains, compared to market expectations of a fall to 57.1. The non-manufacturing PMI had recorded a level of 57.5 in the prior month. Moreover, the final Markit US services PMI reading for May came in at 53.6, up from 53.1 recorded in the previous month but lower than the initial estimate of 54.0.

In other economic news, the final durable goods orders fell more than expected on a monthly basis in April, after it registered a drop of 0.8%, compared to a revised rise of 2.3% in the prior month. The preliminary figures had indicated a fall of 0.7%, while markets were expecting durable goods orders to drop 0.6%.

Meanwhile, the US factory orders declined 0.2% in April, meeting the consensus estimate, from a revised rise of 1.0% in March.

In the Asian session, at GMT0300, the pair is trading at 1.1273, with the EUR trading 0.12% higher from yesterday's close.

The pair is expected to find support at 1.1245, and a fall through could take it to the next support level of 1.1217. The pair is expected to find its first resistance at 1.1290, and a rise through could take it to the next resistance level of 1.1307.

Moving ahead, investors will focus on the Euro-zone Sentix investor confidence for June along with retail sales data for April, both due to release today. Also, JOLTS job openings data for April in the US, scheduled to release later in the day, will be closely watched by traders.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

UK’s Services Sector Growth Slowed In May

For the 24 hours to 23:00 GMT, the GBP rose 0.29% against the USD and closed at 1.2906.

Macroeconomic data showed that growth in UK's dominant service sector slowed more than expected in May as political uncertainty ahead of this week's general election and rising consumer prices weighed on the sentiment. The nation's services PMI fell to a three-month low of 53.8 in May from 55.8 reported last month. Investors had expected the index to fall to a level of 55.0.

Meanwhile, the latest opinion poll showed that the Conservative Party would win only 305 seats in the House of Commons, above Labour's 268 but well short of the 326 seats required for a majority.

Overnight data indicated that UK BRC like-for-like retail sales dropped by 0.4% YoY in May, from a rise of 5.6% reported last month, suggesting that the British consumers are feeling the strain from rising inflation and cutting their spending on discretionary items.

In the Asian session, at GMT0300, the pair is trading at 1.2919, with the GBP trading 0.10% higher from yesterday's close.

The pair is expected to find support at 1.2872, and a fall through could take it to the next support level of 1.2826. The pair is expected to find its first resistance at 1.2953, and a rise through could take it to the next resistance level of 1.2988.

Amid no economic release in the UK today, market participants will look forward to global macroeconomic events for further direction in the Pound.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Extends Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.09% against the JPY and closed at 110.45.

Overnight data showed that Japan's labour cash earnings rose 0.5% on an annual basis in April, higher than market expectations for a 0.3% gain. In the previous month, labour cash earnings had registered a revised unchanged reading.

In the Asian session, at GMT0300, the pair is trading at 109.82, with the USD trading 0.57% lower from yesterday's close.

The pair is expected to find support at 109.46, and a fall through could take it to the next support level of 109.09. The pair is expected to find its first resistance at 110.46, and a rise through could take it to the next resistance level of 111.09.

Going forward, Japan's GDP growth data for the first quarter along with preliminary estimates of leading as well as coincident indices, both for April, slated to release tomorrow, would garner a lot of attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Reverses Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.11% against the CHF and closed at 0.9649.

In the Asian session, at GMT0300, the pair is trading at 0.9631, with the USD trading 0.19% lower from yesterday’s close.

The pair is expected to find support at 0.9619, and a fall through could take it to the next support level of 0.9606. The pair is expected to find its first resistance at 0.9654, and a rise through could take it to the next resistance level of 0.9676.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canadian Dollar Trading Higher Ahead Of PMI Data

For the 24 hours to 23:00 GMT, the USD declined 0.14% against the CAD and closed at 1.3477.

In the Asian session, at GMT0300, the pair is trading at 1.3467, with the USD trading 0.07% lower from yesterday’s close.

The pair is expected to find support at 1.3450, and a fall through could take it to the next support level of 1.3434. The pair is expected to find its first resistance at 1.3492, and a rise through could take it to the next resistance level of 1.3518.

Trading trends in the pair today are expected to be determined by the release of Canada’s Ivey PMI data for May, due later in the day.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Daily Technical Analysis: GBP/USD Bullish Break Runs Into Resistance Ahead Of UK Elections

Currency pair GBP/USD

The GBP/USD broke above the resistance trend line (dotted red) which invalidated yesterday's bearish wave count and could make a bullish variant more likely although both support and resistance levels remain nearby. The UK will hold general parliamentary elections on Thursday 8 June 2017.

The GBP/USD broke out above the smaller resistance line (dotted yellow) and is now challenging the resistance top (red).

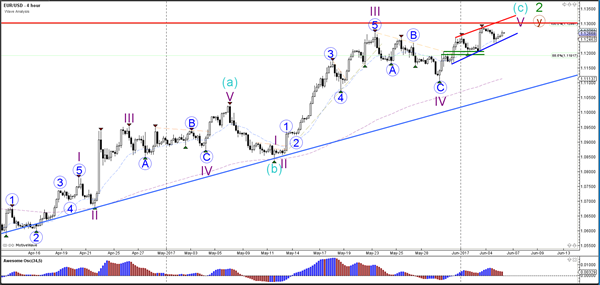

Currency pair EUR/USD

The EUR/USD is moving higher in a bullish trend channel indicated by the support (blue) and resistance (red) trend lines. The new higher high is challenging the 100% Fib level at 1.13 of wave 2 (green), which is a break or bounce zone.

The EUR/USD is trying to break above the resistance trend line (dotted orange) but it has a major resistance zone (red) at 1.13 just above it. It remains to be seen whether price will break or bounce at 1.13.

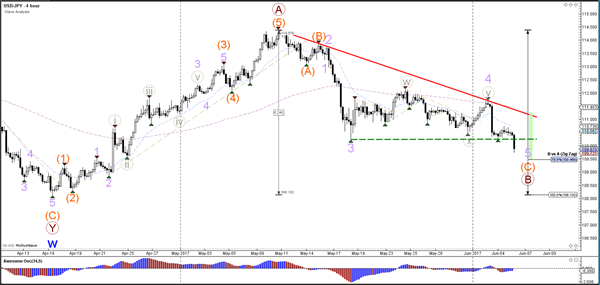

Currency pair USD/JPY

The USD/JPY broke below the support trend line (dotted green) and is challenging the Fibonacci levels of wave B (brown).

The USD/JPY indeed completed a wave 4 (grey) as indicated earlier this week and is building one more lower low via a wave 5.

Minor Risk Aversion As Traders Eye Events On Thursday

- Traders slightly risk averse as Gold and yen push on and equities make small losses;

- Conservative lead under considerable threat in latest Survation poll;

- GBP holding up despite poll moves which may be a concern;

- Eurozone and US data eyed today.

European equity markets are expected to open a little lower on Tuesday, in-keeping with the moderate risk aversion that we've seen overnight and as traders look ahead to a number of major events on Thursday.

It's quite normal to see this kind of behaviour when the latter part of the week is as busy as it is. We're seeing a little bit of risk aversion in the markets today with European futures tracking similarly small losses across the US and Asia, Gold making modest gains to trade at six week highs and the yen making further advances.

But we have a big week or so ahead of us with the UK heading to the polls and the ECB announcing its latest monetary policy decision on Thursday and the Federal Reserve doing the same next Wednesday. Once these events pass, we may have a little more clarity and therefore see a little less caution in the markets.

The UK election remains the standout event for most, with the outcome being so important for Brexit negotiations over the next couple of years. The Conservative lead over Labour has collapsed, if the polls are to be believed, and it seems that the only thing that Theresa May currently has on her side now is time, with Labour still having a lot to do and only two days in which to achieve it. As it is, a working majority is now in doubt with another poll released overnight from Survation showing the lead at only a single point.

The pound has not been too shaken by the polls in recent days though, having shown a certain vulnerability to them prior to that. Despite the lead closing and May's majority looking under threat, the pound has continued to grind higher against the dollar and remain just below 1.30, and has held its own against both the euro and the yen. Whether this reflects a lack of faith in the polls or just those that point to a much tighter race isn't clear but there doesn't appear to be much election risk being priced in which in itself concerns me given what's happened previously.

As far as today is concerned, it's looking a little quiet on the releases front, with eurozone Sentix investor confidence and retail sales the only notable data this morning. We'll also get JOLTS job openings from the US later this afternoon but aside from this, focus will likely remain on events later in the week.

What’s On The Cards For The Kiwi Dollar Moving Forward?

Key Points:

- We could be approaching a near-term peak for the NZD.

- The technical bias is suggesting that a reversal is warranted.

- Losses likely to be capped at the 0.7053 handle.

The Kiwi Dollar may need to moderate slightlyin the coming days as a number of technical signals are beginning to cast doubt on hopes of extending gains significantly in the near-term. Nevertheless, we may not have reached our reversal point just yet which could mean that we still have a small degree of ground left to be claimed – especially if the impending GDT Price Index comes in above targets.

Firstly, if we look at the daily chart, it is becoming apparent that the pair is beginning to encounter some rather stiff resistance which could, eventually, result in a reversal for the NZD. In particular, the presence of a historical point of inflection and the upside of the regression channel are working against the bulls – likely meaning gains will be capped by the 0.7163 handle. However, we obviously haven't quite hit this price just yet which could mean we don't see a correction begin for a couple of sessions.

Regardless, any further gains will bring the NZD into conflict with the 0.7163 handle which could spell the end of the recent uptrend. Subsequently, the pair should move into retreat, at least until the stochastics and RSI have moved out of overbought territory. However, this would almost definitely invert the Parabolic SAR reading to bullish which could see a sizable tranche of losses begin. Despite this, our current bias is that the Kiwi Dollar sinks to the 0.7053 handle and no further, largely due to the 100 day EMA providing dynamic support around this price.

As for the fundamental side of things, the release of the GDT Price Index this week should work in concert with the technical forecast. On the one hand, if we see a yet another increase in the figure, upsides will be present but not too aggressive as a positive outcome has largely been priced in. On the other hand, if a negative print is seen, it will simply kick start the downtrend that has been described above. This being said, don't expect to see the pair go into free fall as the index is still at its highest point since mid-2014.

Ultimately, despite some residual buying pressure, the outlook for the NZD is rather bearish. As mentioned, the presence of that resistance level around the 0.7163 handle could prove to be a near-term high for the pair and a downtrend could begin once it has been tested properly. Nevertheless, not all is doom and gloom as there is a decent chance that losses are capped at 0.7053 which leaves the pair in possession of most of the gains made over the past month.

Elliott Wave View: EURJPY Bounce Expected

Short Term EURJPY Elliott Wave view suggests the rally from 4/16 low is unfolding as a double three Elliott Wave structure. Up from 4/16 (114.8) low, Intermediate wave (W) ended at 125.81 and Intermediate wave (X) is proposed complete at 122.53. A break above 125.81 however is still needed to add conviction that the next leg higher has started.

From 122.53 low, the rally is also unfolding as a double three Elliott Wave structure. Minute wave ((w)) ended at 125.8 and Minute wave ((x)) ended is proposed complete at 123.11. Rally from there is unfolding as a double three where Minutte wave (w) ended at 125.31 and Minutte wave (x) pullback has reached 100% in 3 swing from 6/2 high. Thus while pair stays above 123.11, and more importantly above 122.53, expect pair to extend higher or at least bounce in 3 waves. If pair breaks below 123.11, then pair is likely doing a double correction from 5/16 peak. This suggests pair can open extension lower to 121.6 – 122.25 area in case of a double correction. From this area, buyers should appear again for an extension higher or at least a 3 waves bounce.

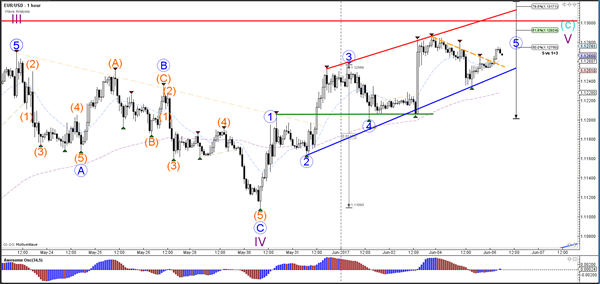

EURJPY 1 Hour Elliott Wave Chart