Sample Category Title

Technical Outlook: GBPUSD – Morning Doji Star Reversal Pattern Produces Fresh Strength

Fresh strength emerged after yesterday's downside rejection at 1.2900 and failure to clearly break below daily Tenkan-sen/10SMA supports at 1.2908/14. Morning Doji Star reversal pattern is forming on daily chart, as today's rally regained Monday's multi-month high at 1.2987 and is pressuring psychological 1.3000 barrier. Overall bullish structure remains intact after shallow Mon/Tue correction was contained by initial supports and sees scope for further upside. However, overbought slow stochastic on both daily and weekly charts requires caution, as falling thick weekly cloud weighs (cloud base lies at 1.3088). Repeated failure at 1.3000 barrier would signal extended consolidation, as the pair is eyeing tomorrow's BoE monetary policy decision for stronger signals. Alternatively, break below 10SMA/daily Tenkan-sen would weaken near-term structure and risk stronger correction.

Res: 1.3000, 1.3050, 1.3088, 1.3146

Sup: 1.2939, 1.2914, 1.2908, 1.2862

BoE Expected To Keep Rates Steady

ECB Governor Draghi will make a speech in the Dutch Parliament at 12:00 BST today. It will be Draghi's first speech after the French election so traders should be aware of any comments on the Eurozone's economic outlook or hints of a possible gradual removal of QE.

Thursday May 11th is a crucial day for GBP traders with the release of a series of UK economic data at 09:30 BST. Followed by the the Bank of England's (BoE) interest rate decision and monetary policy minutes at 12:00 BST and the NIESR GDP estimate (Feb to April) at 13:00 BST.

Recent UK economic data has been soft, lowering market expectations for a rate hike. The general election will be held on June 8 and, with the Brexit procedure ongoing, the BoE is unlikely to take any actions at least before the election result; therefore, they are likely to keep policies steady until the Brexit negotiation deal has a clear outline.

UK inflation saw an upswing following the Brexit vote, reaching the central bank's 2% target, due to the weakening of GBP since the Brexit referendum. A weak pound is beneficial for exports and inflation, however, as wage growth has slowed down the rising inflation will likely undermine consumer expenditure; one of the major drivers of the economy.

GBP/USD has rallied approximately 3% since Theresa May's announcement of a snap general election on April 18. On Monday May 8 GBP/USD hit a 7-month high of 1.2988, trading just below the significant psychological level at 1.3000, where heavy selling pressure is expected.

The BoE's announcement will likely cause a move to GBP and GBP crosses. With a hawkish comment GBP/USD will likely breach the level at 1.3000. Conversely, with a dovish comment, we will likely see a correction downward.

The French election outcome has lifted markets' risk-on sentiment and resulted in safe heavens retreat, US and European treasury yields rise thereby pushing USD and EUR up against JPY. The dollar index hit a 2-week high of 99.55 on Tuesday.

Bank of Japan (BoJ) Governor Kuroda stated on Tuesday that 'the Japanese and global economy saw a recovery' however, the BoJ will continue its QE programme as inflation is expected to reach above the 2% target in 2018. The statement further weighed on JPY.

The Bank of Japan has been considering a gradual removal the long-standing QE. However, while the economic recovery is still fragile it is likely that it will take an extended period for the BoJ to implement it until it sees solid and stable economic and inflation growth.

On Tuesday USD/JPY hit a high of 114.32, previously reached on March 15. Spot gold hit an 8-week low of 1214.15.

Technical Outlook: EURUSD – Risk Of Further Downside While The Price Is Holding Below 10SMA / Tenkan-Sen

Two consecutive long red daily candles and close below initial 10SMA / daily Tenkan-sen supports turned near-term picture bearish and weigh on the market.

Reversal from fresh multi-month high at 1.1020 dipped to 1.0862 where temporary footstep was found.

The pair is consolidating in early Wednesday trading, with action so far holding below 1.0900 handle and keeping intact upside pivots at 1.0913/38 (10SMA / Tenkan-sen) now reverted to resistances.

Pullback may extend to 1.0848 (Fibo 38.2% of 1.0568/1.1020) and 1.0826 (200SMA) with the latter expected to hold dips and keep overall bullish bias in play.

Golden cross of 20/200SMA's is forming at 1.0826 and underpinning larger uptrend.

Bounce and close above daily Tenkan-sen will be seen as strong bullish signal for renewed attempts above 1.1000.

Conversely, close below 200SMA will be bearish and signal deeper correction.

Res: 1.0913, 1.0938, 1.0950, 1.0998

Sup: 1.0862, 1.0848, 1.0826, 1.0794

AUDUSD Looking Quite Bearish, More Weakness May Follow

AUDUSD made a sharp fall last week, which we now see as a trigger and an indication for a wave three in progress. As such we can say, that a running flat correction was completed in the previous wave 2, at the 0.7558 level. A running flat correction is like a normal flat, the only difference is that wave C) of a running flat does not breach the end of wave A), as in our case. That said, we now expect pair to stay bearish in sessions ahead, and ideally unfold a five wave movement within the current bigger wave three that can be underway down to 0.7250 or even 0.7130.

AUDUSD, 4H

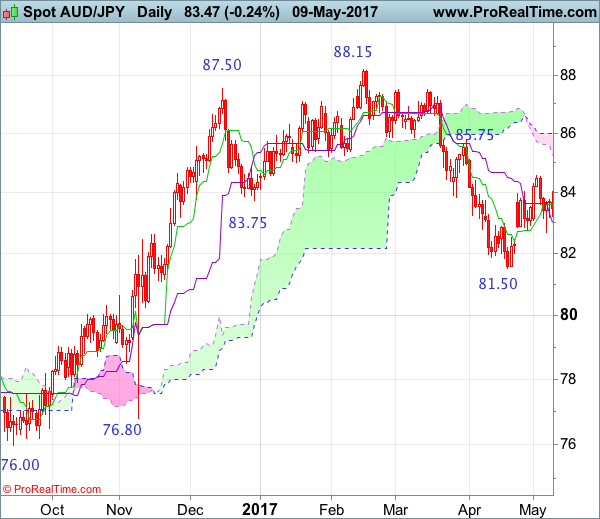

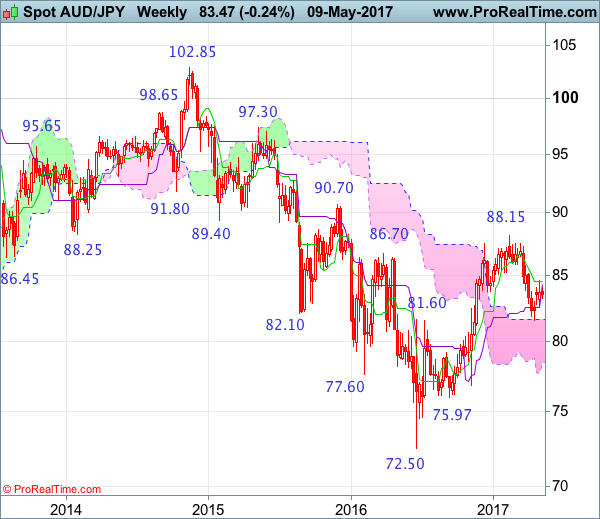

AUD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 13 Mar 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Bearish engulfing pattern

• Time of formation: 16 Feb 2017

• Trend bias: Near term down

Although the Australian dollar rebounded last week to as high as 84.55, the subsequent retreat has retained our bearishness and as long as this level holds, consolidation with mild downside bias remains for another decline, below 82.65-70 would bring weakness to 82.00 but a daily close below there is needed to signal the rebound from 81.49 low has ended, bring retest of this level later. A drop below this level would extend recent decline from 88.15 top to support at 81.10-15, however, near term oversold condition should limit downside and reckon 80.00 psychological support would hold from here, bring rebound later.

On the upside, whilst marginal recovery from here cannot be ruled out, as long as said resistance at 84.55 holds, prospect of another decline to aforesaid downside targets remains. Only a break above said resistance at 84.55 would abort and suggest low is formed instead, risk a stronger rebound to 85.00-10 but said resistance at 85.75 should remain intact, bring another decline later.

Recommendation: Hold short entered at 83.65 for 81.65 with stop above 84.65.

On the weekly chart, although aussie found support at 82.70 and rebounded, still reckon the Tenkan-Sen (now at 84.50) would limit upside and bring another decline, below 83.00 would bring test of said support at 82.70 but break of 82.00 is needed to signal the rebound from 81.49 has ended, bring retest of this level later. A drop below this level would extend the fall from 88.15 top to support at 81.10-15, a weekly close below there would retain bearishness and suggest the rise from 72.50 has ended, then further fall to 80.50 and possibly psychological support at 80.00 would follow.

On the upside, expect recovery to be limited to the Tenkan-Sen (now at 84.50) and bring another decline. A weekly close above resistance at 84.55 would suggest low is formed instead, bring a stronger rebound to 85.00, then towards resistance at 85.75 but only break there would abort and signal low is formed instead, bring further subsequent gain to 86.00 and then 86.50-60, however, price should falter below resistance at 87.50.

Australian Retail Sales Register Another Drop In March

'The fall (in retail sales) confirms our sense that the pace of household consumption recorded late last year was facilitated by a sharp drop in the savings rate, and was unsustainable.' - Tom Kennedy, JP Morgan

Australian retail sales dropped for the second straight month in March, official data revealed on Tuesday. According to the Australian Bureau of Statistics, sales were down 0.1% on a seasonally adjusted basis in March, following the downwardly revised drop of 0.2% registered in the preceding month and falling short of analysts' expectations for a 0.3% increase. However, in trend terms, Australian turnover soared 2.5% in March compared with the same month a year ago. The rise was backed by an uptick in food retailing, which rose 0.1% in March, but the gain was still offset by a slowdown in household goods retailing and sales of clothing, footwear and personal accessory, with both industries registering a 0.3% dip in the observed period. In the meantime, sales at department stores, cafes, restaurants and takeaway food services were relatively flat, coming in with a 0% change in March. In regional terms, sales plummeted 0.4% in Queensland, 0.1% in West Australia and Tasmania and 0.3% in the Northern Territory, setting off moderate gains observed in other areas.

Canadian Building Permits Drop For Second Straight Month

'Housing demand appears to have been curbed in recent months due to the deterioration in housing affordability caused by a sustained period of rapid house price growth during 2014-16.' - Martin Ellis, Halifax

The value of dwelling permits issued by Canadian municipalities slid for the second straight month, government data revealed on Tuesday. The report released by Statistics Canada showed building permits in Canada dropped 5.8% to a total of $7.0B over the month of March, following the downwardly revised 2.8% plunge registered in February and falling well behind the 4.2% gain eyed by most of the economists. The fall was mainly driven by weaker building intentions for multi-family apartment buildings in nine regions of the country, with British Columbia and Ontario registering the biggest drops. In the meantime, single-family dwelling construction intentions surged 3% to $2.7B in the reported period, putting Ontario and Alberta atop of the four provinces that booked gains. In the non-residential sector, the value of building permits inched 0.5% down to settle at $2.4B in March, with lower commercial building intentions being the main contributor to the decline. Still, the latter was almost completely offset by a 9.1% jump in the institutional component, led by Quebec and Ontario.

US Job Openings Climb To 5.74M In March

'With a 17-year high share of small businesses reporting jobs are hard to fill, an acceleration in quits would bode well for a pick-up in wage growth later this year.' - Sarah House, Wells Fargo

The number of job openings in the US rose in March, according to the JOLTS monthly report. Data from the US Bureau of Labour Statistics released on Tuesday showed that the US job openings increased to 5.74M over the course of March, following the previous month's downwardly revised figure of 5.68M. Meanwhile, analysts anticipated a slight decrease to 5.67M. Job openings grew across business and professional services as well as in local and state government education, while they declined in education services. The number of hires over the reported month was changed insignificantly, coming in at 5.3M with an increase in social assistance and healthcare services, though a modest decrease was registered in logging and mining. Moreover, data showed that total separations, including layoffs, quits and discharges, were little changed at 5.1M in March. The total number of separated employees diminished for government and was slightly changed for the private sector. Separately, the US employment data reported earlier this month suggested that the job market is likely to continue being strong.

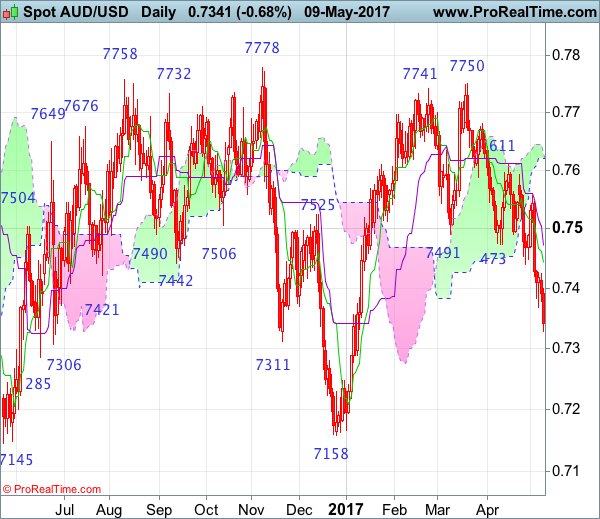

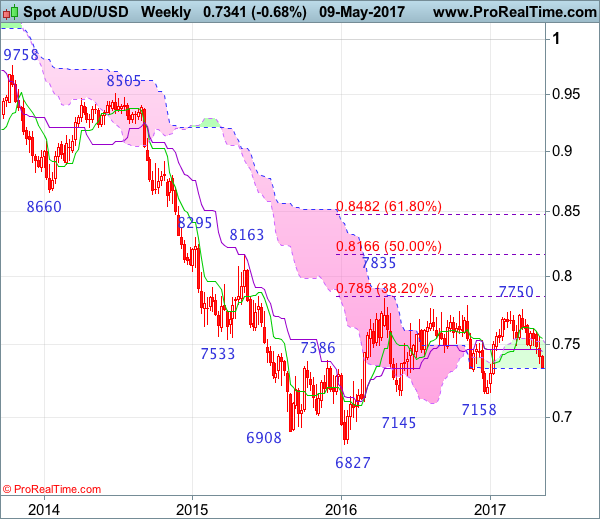

AUD/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting doji

• Time of formation: 20 Feb 2017

• Trend bias: Sideways

Daily

• Last Candlesticks pattern: Bearish engulfing pattern

• Time of formation: 21 Mar 2017

• Trend bias: Near term down

As aussie has dropped again after brief, adding credence to our bearish view (our short position entered at 0.7590 met target at 0.7390 with 200 points profit) and downside bias remains for the decline from 0.7750 to bring at least a strong retracement of the rise from 0.7158, hence further weakness to 0.7300-10 and possibly 0.7250-60 is underway, however, near term oversold condition should prevent sharp fall below 0.7200-10 and price should stay well above support at 0.7158.

On the upside, whilst initial recovery to 0.7400 cannot be ruled out, reckon the Tenkan-Sen (now at 0.7443) would limit upside and bring another decline later. A daily close above 0.7490-00 would defer and risk a stronger rebound towards resistance at 0.7556 but break there is needed to signal a temporary low is formed instead, bring a stronger rebound to 0.7590-95 but price should falter below resistance at 0.7611 and bring another decline later.

Recommendation: Target met and sell aussie again at 0.7440 for 0.7240 with stop above 0.7540.

On the weekly chart, last week’s selloff adds credence to our view that the rebound from 0.7158 has ended at 0.7750, bearishness remains for the fall from there to extend further decline to 0.7290-00 and possibly towards 0.7230, however, reckon downside would be limited to 0.7200 and price should stay well above previous support at 0.7158, risk from there is seen for a rebound to take place later.

On the upside, although initial recovery to 0.7420-30 cannot be ruled out, reckon the Kijun-Sen (now at 0.7454) would limit upside and bring another decline later. Only above last weeks high at 0.7556 would abort and signal low is formed instead, risk a stronger rebound to 0.7590-95 but break of resistance at 0.7611 is needed to add credence to this view, bring further gain towards resistance at 0.7680 but a sustained breach above this level is needed to signal the retreat from 0.7750 has ended, bring another bounce towards this level.

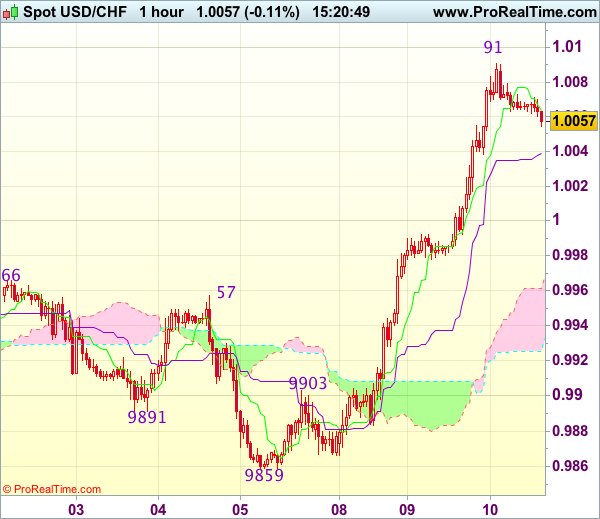

Trade Idea : USD/CHF – Buy at 1.0005

USD/CHF - 1.0066

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0064

Kijun-Sen level : 1.0039

Ichimoku cloud top : 0.9961

Ichimoku cloud bottom : 0.9926

Original strategy :

Buy at 0.9980, Target: 1.0080, Stop: 0.9945

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0005, Target: 1.0105, Stop: 0.9970

Position : -

Target : -

Stop : -

Although dollar has eased after rising to 1.0091 and consolidation below this level would be seen, reckon pullback would be limited to the Kijun-Sen (now at 1.0039) and renewed buying interest should emerge around 1.0000-05, bring another rise, above said resistance would add credence to our view that early upmove has resumed for retest of 1.0108 resistance, break there would confirm and encourage for headway to 1.0130 and then 1.0150-55.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback as 1.0000-05 should limit downside. Only below previous resistance at 0.9957 would defer and suggest top is possibly formed, bring test of 0.9920-25 but break of previous resistance at 0.9903 is needed to add credence to this view, bring further fall to 0.9880-85.