Sample Category Title

EURUSD: Bearish, Declines Further

EURUSD: With the pair extending its downside pressure on Tuesday, further weakness is likely in the days ahead. Resistance comes in at 1.0900 level with a cut through here opening the door for more upside towards the 1.0950 level. Further up, resistance lies at the 1.1000 level where a break will expose the 1.1050 level. Conversely, support lies at the 1.0800 level where a violation will aim at the 1.0750 level. A break of here will aim at the 1.0700 level. Its daily RSI is bearish and pointing lower suggesting further weakness. All in all, EURUSD faces further bear threats.

Pick Your Poison: What is the Market Focusing On?

Wednesday May 10: Five things the markets are talking about

There are a number of moving parts that are currently keeping capital markets on their toes - China, ECB, Fed, N. Korea, Trump and OPEC.

Investors have been extra focused on China after a selloff erased at least -$500B from the value of stocks and bonds since mid-April, amid policy makers' moves to crack down on leverage. Data overnight showed that prices slowed more than expected (see below).

When is the ECB going to start rate normalization? They have to get their timing correct. Today's ECB unemployment figures support the case for ongoing stimulus. A broader measure of regional unemployment shows that around +15% of eurozone workers are "unemployed or underemployed," which suggests wages and inflation are unlikely to pick up for some time. A June Fed hike is almost fully priced in.

North Korea says it's going ahead with its sixth nuclear test, who is pulling the strings?

President Trump fires FBI Director Comey, citing his handling of the investigation into Hillary Clinton's email server - what's the impact on the FBI probe into possible ties between the Trump campaign and Russia?

OPEC still does not have a consensus to maintain last November's production cuts into H2, 2017. But, is it coming soon?

1. Global bourses see mixed results

Overnight, Asian stocks resumed a rally as Hong Kong shares jumped to a two-year high, while European shares are mixed and U.S futures see red as President Trump fired FBI Director James Comey.

In Hong Kong, the Hang Seng rose +0.5%, to its highest level since July 2015. The Hang Seng China Enterprises Index jumped +0.9%, rallying for a third consecutive day, while the Shanghai Composite Index retreated -0.9% to its lowest level since October.

In Japan, the broader Topix index increased +0.2% and the Nikkei 225 rose +0.3%. Gains were limited by yen's rally overnight on tentative 'risk aversion' trading (¥113.83).

In South Korea, the Kospi slid -1% after surging +2.3% on Monday, the most since September 2015.

In Europe, indices are trading mixed this morning with notable weakness in the Swiss SMI and out-performance in the FTSE on energy prices. Corporate earnings look set to dominate the Eurostoxx 600.

U.S stocks are set to open in the red (-0.2%).

Indices: Stoxx50 -0.3% at 3640, FTSE +0.1% at 7347, DAX -0.1% at 12742, CAC-40 -0.2% at 5388, IBEX-35 -0.6% at 10985, FTSE MIB -0.4% at 21398, SMI -0.8% at 9047, S&P 500 Futures -0.2%

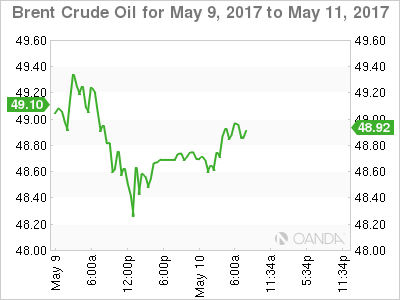

2. Crude oil prices find support on potential cut extension, gold higher

Ahead of the U.S open, oil prices are on the rise on rumoured reports that Saudi Arabia would cut supplies to the region. Prices are also supported by a larger than expected fall in yesterday's API crude inventories last week, down -5.8m barrels compared with market expectations for a -1.8m barrels decline.

Brent futures are up +19c, or +0.4%, at +$48.92 a barrel - they fell -1.2% yesterday. U.S West Texas Intermediate (WTI) crude is up +23c, or +0.5%, at +$46.11 a barrel.

Note: WTI also fell -1.2% Tuesday, and the closing price for both contracts was the second lowest since Nov. 29, the day before OPEC agreed to cut production during H1, 2017.

There are reports this morning that State-owned Saudi Aramco will reduce oil supplies to Asian customers by about -7m barrels in June, as part of OPEC's agreement to reduce production.

Capping price gains is higher crude output from the U.S, particularly shale producers.

Note: U.S crude production is expected to rise by more than previously expected in 2017 to +9.31m bpd from +8.87m bpd in 2016.

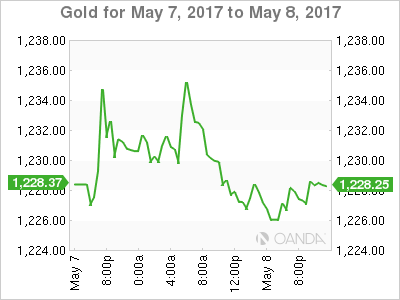

Gold (+0.2% at +$1,223.30 an ounce) has edged off the previous day's two-month low this morning as U.S President Trump's abrupt firing of FBI chief James Comey hit equities, but expectations of further Fed rate hike is likely to limit gains by the metal.

3. Global yields little changed, focus on Central Banks

With Euro go-political risk abating somewhat since the weekend, dealers and investors are returning to fundamentals and central bank monetary policy for guidance.

The markets main focus is on the Fed and the ECB. The current odds for a Fed hike next month are +83%, however, for Draghi, the question is not about rate hikes, but about reducing stimulus.

Central banks may be best placed to understand other central banks, and if so, the ECB is not expected to be winding down its stimulus programs anytime soon. According to today's minutes from its April policy meeting, Sweden's Riksbank expects the "ECB to continue to pursue a very expansionary monetary policy in the foreseeable future." And it's for this reason why the Riksbank is prepared to extend its own bond-buying program to the end of 2017.

Yields on eurozone government bonds are declining slightly in early Wednesday trading, but a major drop seems unlikely due to supply of new debt this week. Not only are sovereigns, including Germany, in the market to place new debt, but so to are agencies. German 10-year Bunds yields have fallen -1 bps to +0.43%.

Elsewhere, the yield on 10-year Treasury notes fell -1 bps to +2.39%, while Australian 10-year yields dropped -3 bps to +2.66%.

Note: The Bank of England (BoE) publishes its interest-rate decision and quarterly Inflation Report Thursday.

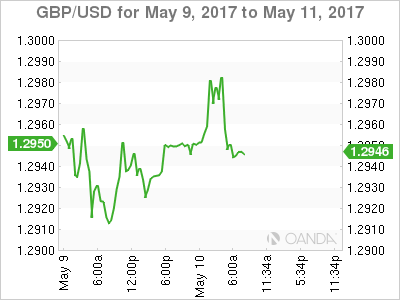

4. Sterling hovers atop key resistance, a break could trigger more gains

Ahead of the U.S open, the pound trades up +0.37% at £1.2983 outright, hovering just below the psychological £1.30 handle, a level not traded in eight-months.

Of late, sterling has been benefitting as "weaker short-positions" are been forced to close out. Ahead of the BoE rate announcement and inflation quarterly report tomorrow, do not be surprised to see more positions unwind ahead of time.

Any hints from Governor Carney that they are considering raising rates would be sterling positive. More market stop-loss orders could be executed when £1.3000 is finally breached with momentum.

Elsewhere, the FX markets saw little volatility in the session. A slightly softer USD was attributed to President Trump's firing of his FBI director, the yen (¥113.83) found some support, while the EUR continues to hover just under the psychological €1.09 area (€1.0873).

5. China CPI rises to 3-month highs while PPI growth slows

China inflation data has also propped up sentiment, with Consumer Price Index rising to three-month highs and beat market expectations on a month-over-month (+0.1% vs. -0.3% prior) and year-over-year basis (+1.2% vs. +1.1%e).

Note: The main driver of the pick-up was an increase food price inflation, which rose from -4.4% y/y to -3.5% on the back of pick-ups in fruit and vegetable price inflation. Non-food inflation also edged up from 2.3% y/y to 2.4%, but this was largely due to a seasonal increase in tourism cost inflation.

China's Producer Price Index (+6.4% vs. +6.7%e) was positive for the eight consecutive month, but the rate of increase was smallest in four-months as the recent free-fall in metal prices is also reflected in the results.

Note: The driver was a drop in industrial commodity prices, with factory gate prices declining most among steel and oil producers.

GBP-AUD Likely to See Some Volatility in the Next Few Days

- Surpise Sterling success and a slip in Australian Dollar - interesting times ahead?

- GBP-AUD likely to see some volatility in the next few days

- Australia unlikely to make further interest rate cuts

Theresa May calling the snap election helped boost the Pound and with the Conservative Party ahead by 22 points in the polls, that's certainly supporting Sterling. The uncertainty of a general election will usually weaken a currency, but the unanimous nature of the polls suggesting a sizeable Tory majority and the repercussions for a stronger hand in the Brexit negotiations have benefitted the Pound. This week we have "Super Thursday" – so called because a large number of economic indicators for the UK are released on the same day:

- We'll hear from the Bank of England (BoE), who will vote on interest rates; in the last meeting, one member of the Monetary Policy Committee (MPC) voted for an interest rate hike, which boosted the Pound. If there's a change to the voting, and we more in favour of an interest rate increase, that will add strength to the Pound. On the other hand, if 9-0 committee members vote in favour of no change of interest rates, then expect the Pound to drop a little.

- The quarterly inflation report will also be released; this will be market moving and may well see the BoE downgrade growth forecasts for the UK for 2017 (currently forecast at 2.0%), which would weaken the Pound.

- Also featuring on "Super Thursday" will be UK manufacturing and industrial production data and trade balance figures. The forecasts are good, so that may counterbalance any Sterling weakness.

GBP-AUD likely to see some volatility in the next few days

With all this key economic data and potential for market movement, it may be worth converting a portion of GBP into AUD beforehand, just in case GBP falls back and signals a short term top on GBP-AUD.

Technically, GBP-AUD had been trading in the 1.5920 to 1.7170 range since October 2016, and so when the breakout happened last April, it was a decisive break. Currently, the Sterling-Australian Dollar exchange rate is heading up towards the next level of resistance at 1.7800 but this week's slew of UK data may see the Pound stumble. On the daily and weekly charts, this currency pair is looking a bit overstretched, so it is possible that this rally could be exhausted. With this in mind, consider reducing your risk and/or trading a portion of your funds.

Australia unlikely to make further interest rate cuts

Over in Australia, the Reserve Bank of Australia (RBA) has left interest rates on hold at 1.5% in recent months and their policy statement remains neutral – it's unlikely that they'll cut interest rates any further. We anticipate that the next move could be higher but that may be sometime in 2018. What has triggered the fall in the Australian Dollar over the last two months is the drop in commodity prices, particularly iron ore – Australia's largest export – and copper, which has meant the Australian Dollar is one of the worst performers of the year, thus far. Building approvals and retail sales data both came in below expectations, which added to the downward pressure on the AUD; but with the GBP-AUD currency pair looking overstretched and with traders focusing on the UK's Super Thursday, the currency pair will likely tread water over the next couple of days.

Guidance for exchanging GBP-AUD

Hedging your bets is always a sensible strategy, particularly when there are warning signs that GBP-AUD may be topping out. You can take advantage of the current exchange rates by converting a portion of your funds on either a spot contract or fixing the rate for a later delivery on a forward contract with the view to converting more if and when GBP-AUD breaks through the next level of resistance at 1.7800.

GBP/USD Bulls Retreat Ahead Of BoE Statement

Thursday May 11th is a crucial day for GBP traders with the release of a series of UK economic data at 09:30 BST. Followed by the Bank of England's (BoE) interest rate decision and monetary policy minutes at 12:00 BST and the NIESR GDP estimate (Feb to April) at 13:00 BST.

Recent UK economic data has been soft, lowering market expectations for a rate hike. The general election will be held on June 8 and, with the Brexit procedure ongoing, the BoE is unlikely to take any actions at least before the election result; therefore, they are likely to keep policies steady until the Brexit negotiation deal has a clear outline.

GBP/USD has rallied approximately 3% since Theresa May's announcement of a snap general election on April 18. On Monday May 8 GBP/USD hit a 7-month high of 1.2988, trading just below the significant psychological level at 1.3000.

This morning, during early European session, GBP/USD retraced around 50 points, as it was nearing the level at 1.3000, where there is heavy selling pressure.

The BoE's announcement will likely cause a move to GBP and GBP crosses. With a hawkish comment GBP/USD will likely test the level at 1.3000 again. Conversely, with a dovish comment, we will likely see a correction downward.

On the 4-hourly chart, the 10 SMA has crossed over the 20 SMA, suggesting the bullish momentum has been waning.

The daily Stochastic Oscillator reading is around 70, suggesting a pullback.

The resistance level is at 1.2960, followed by 1.2985 and 1.3000.

The support line is at 1.2935, followed by 1.2920 and 1.2900.

GOLD Consolidating Below $1230, SILVER Weakening Towards $16.00, CRUDE OIL Consolidating Around $46.

GOLD Consolidating below $1230.

Gold continues its decline after the yellow metal has faded near the hourly resistance at 1295 (18/04/2017 high). Hourly support is now located at 1195 (10/03/2017 low). The road is wide-open for further decline.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Weakening towards $16.00.

Silver's bearish pressures are still lively. Strong support is given at 15.63 (20/12/2017 low). Closest support is given at 16.20 (04/05/2017 low). Key resistance is given at a distance at 19.00 (09/11/2017 high). Expected to see continued bearish pressures until at least $16.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Consolidating around $46.

Crude oil is bouncing back on short-squeeze move. The commodity has bounced from a level below $44. Strong support is given at 42.20 (14/11/2017 low). Expected to see renewed bearish pressures.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

EUR/JPY Trading Well Above 200-DMA, EUR/GBP Continued Weakness, EUR/CHF Fading Below 1.1000.

EUR/JPY Trading well above 200-DMA

EUR/JPY's buying pressures are there. Hourly resistance at 124.10 (15/12/2016 low) has been broken. Major support is given at 114.90 (18/04/2017low). Expected to see further renewed buying pressures towards 125.00.

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Continued weakness.

EUR/GBP is trading lower. The technical structure remains negative as long as the resistance at 0.8530 (25/04/2017 low) holds. Expected to show continued weakness until support given at 0.8304 (05/12/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

EUR/CHF Fading below 1.1000.

EUR/CHF's volatility is getting stronger. Resistance given at has been broken 1.0898 (08/12/2017 high). Despite the sharp increase and the recent bullish breakout which is very likely psychological, we believe that the medium-term pattern suggests us to see at some point renewed bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low).

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

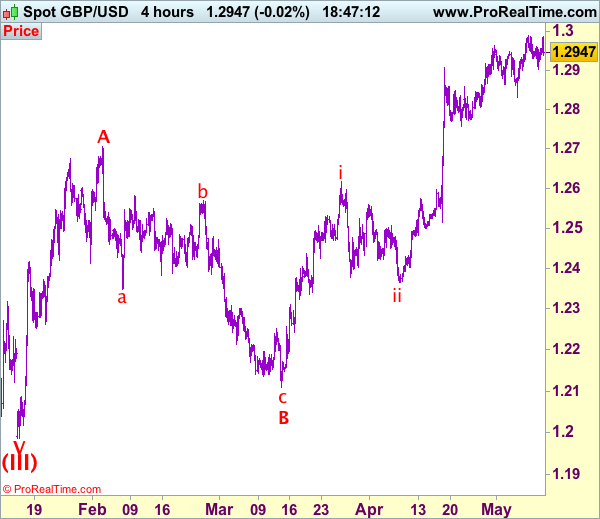

Trade Idea: GBP/USD – Hold short entered at 1.2955

GBP/USD – 1.2941

Recent wave: Wave V of larger degree wave (III) has ended at 1.1986 and major correction has commenced from there for gain to 1.3000 and 1.3140-50

Trend: Near term up

Original strategy :

Sold at 1.2955, Target: 1.2775, Stop: 1.3015

Position: - Short at 1.2955

Target: - 1.2775

Stop: - 1.3015

New strategy :

Hold short entered at 1.2955, Target: 1.2775, Stop: 1.3000

Position: - Short at 1.2955

Target: - 1.2775

Stop:- 1.3000

Although cable rebounded after finding support at 1.2903 yesterday, as long as indicated resistance at 1.2991-00 holds, further consolidation would be seen with mild downside bias for another test of 1.2900-03 support, break there would suggest a temporary top is possibly formed, bring weakness to 1.2831 support, however, a break below this level is needed to add credence to this view, bring retracement of recent rise to 1.2770-75 but previous support at 1.2757 should hold from here. We are keeping our view that the wave c as well as larger degree wave B has ended at 1.2109, hence impulsive wave C has commenced from there with wave i of C ended at 1.2616, follow by a correction to 1.2365 (end of wave ii) and wave iii rally is unfolding.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

On the upside, expect recovery to be limited to 1.2980 and bring another retreat later. Above said resistance at 1.2995 would extend recent upmove to 1.3040-50 but overbought condition should limit upside to 1.3075-80 and price should falter below 1.3100.

USD/CHF Trading Mixed Around Parity, USD/CAD Pushing Slightly Higher, AUD/USD On The Road Toward Key Support 0.7145.

USD/CHF Trading mixed around parity.

USD/CHF is trading mixed. The technical structure has invalidated the short-term negative momentum. Hourly resistance is given at 1.0107 (10/04/2017 high).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Pushing slightly higher.

USD/CAD has declined after failing to reach 1.3800 before bouncing back. Hourly support can be found at 1.3411 (24/04/2017 high) then 1.3353 (20/01/2017 high). Expected to show renewed bullish pressures as long as the pair remains above 1.3530 (27/04/2017 low).

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD On the road toward key support 0.7145.

AUD/USD is trading below 0.7500. As long as prices remain below the resistance at 0.7608 (17/04/2017 high), the short-term technical structure is negative. Key resistance stands at 0.7681 (30/03/2017 high). Expected to show further weakness.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Short-Term Weakness, GBP/USD Pushing Higher Towards 1.3000, USD/JPY Bullish!!

EUR/USD Short-term weakness.

EUR/USD is trading lower. Hourly support is given at 1.0852 (27/04/2017 low) then 1.0682 (21/04/2017 base). Stronger support can be found at 1.0494 (22/02/2017 low). Expected to show another leg higher towards 1.10.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Pushing higher towards 1.3000.

GBP/USD is trading mixed. The pair is trading around former hourly resistance given at 1.2966 (30/04/2017 high). Hourly support can be found at 1.2757 (21/04/2017 low). An unlikely break of this support would indicate further weakness. Expected to push higher.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Bullish!!

USD/JPY is pushing higher since the pair broke resistance given at 112.20 (31/03/2017 high). Hourly support can be found at 110.88 (26/04/2017 low). Stronger support is located at 108.13 (17/04/2017 low). Other key supports lie at a distant 106.04 (11/11/2016 low). Expected to show continued bullish pressures.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

Trade Idea: GBP/JPY – Buy at 145.75

GBP/JPY - 147.25

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term up

Original strategy:

Buy at 146.20, Target: 148.20, Stop: 145.60

Position: -

Target: -

Stop: -

New strategy :

Buy at 145.75, Target: 148.75, Stop: 145.15

Position: -

Target: -

Stop:-

As sterling has eased after rising to 148.10, suggesting consolidation below this level would be seen and pullback to 146.50-60 cannot be ruled out, however, reckon downside would be limited to 145.70-75 and bring another upmove later, above said resistance at 148.10 would extend recent upmove from 135.60 to previous chart resistance at 148.45, then towards 148.90-00 but near term overbought condition should prevent sharp move beyond 149.50, bring retreat later.

In view of this, would not chase this rise here and would be prudent to buy sterling on subsequent pullback as 145.65-70 should limit downside, bring another rise later. Below said support at 145.15-20 would defer and suggest a temporary top is possibly formed, bring correction to 144.80-85 but only break there would provide confirmation, bring correction to 144.50 first.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.