Sample Category Title

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0907; (P) 1.0942; (R1) 1.0990; More...

Intraday bias in EUR/CHF remains on the upside for 1.0999 resistance first. As noted before, the consolidative pattern from 1.1198 should be completed. Break of 1.0999 will pave the way for a retest on 1.1198 high. On the downside, below 1.0872 minor support will turn bias neutral and bring consolidation. But retreat should be contained by 1.0791 support to bring another rally.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Current strong rebound is raising the chance that it's completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0791 support holds.

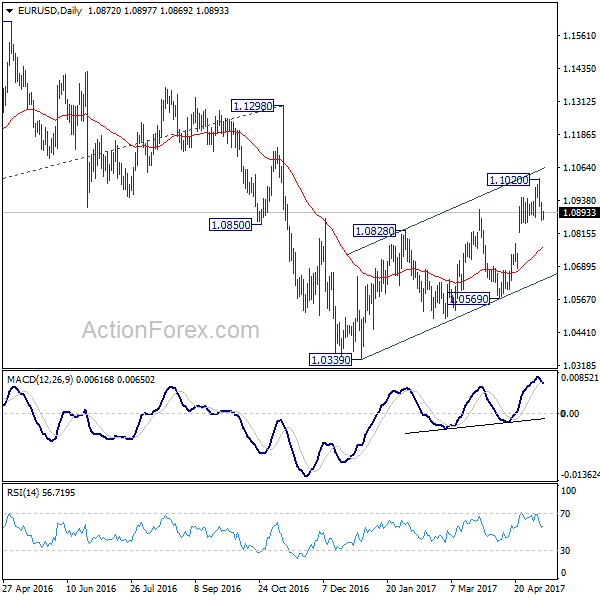

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0846; (P) 1.0890 (R1) 1.0916; More....

The breach of 1.0874 minor support suggests short term topping at 1.1020, on bearish divergence condition in 4 hour MACD. Intraday bias in EUR/USD is turned back to the downside for 55 day EMA (now at 1.0757) first. As noted before, rise from 1.0339 is seen as a corrective move. Break of 55 day EMA will affirm the case that such correction is completed and bring deeper decline to 1.0569 for confirmation. Above 1.1020 will extend such corrective rise instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate long term reversal.

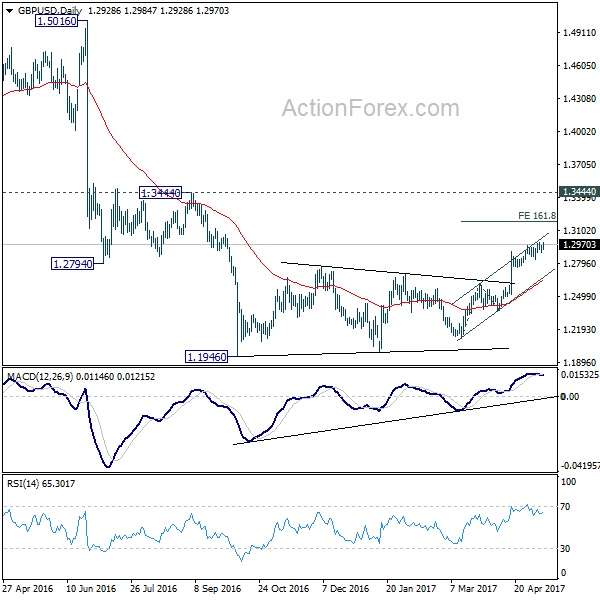

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2904; (P) 1.2932; (R1) 1.2962; More...

Despite diminishing upside momentum as seen in 4 hour MACD, with 1.2830 minor support intact, further rally is still expected in GBP/USD. Current rise could target 161.8% projection of 1.2108 to 1.2614 from 1.2365 at 1.3184. At this point, price actions from 1.1946 are still interpreted as a correction pattern. Therefore, we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2830 support will indicate short term topping. In such case, intraday bias will be turned back to the downside for 1.2614 support.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

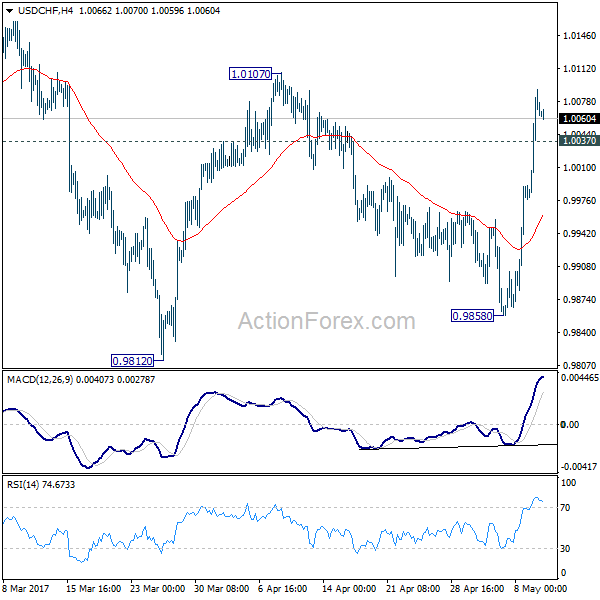

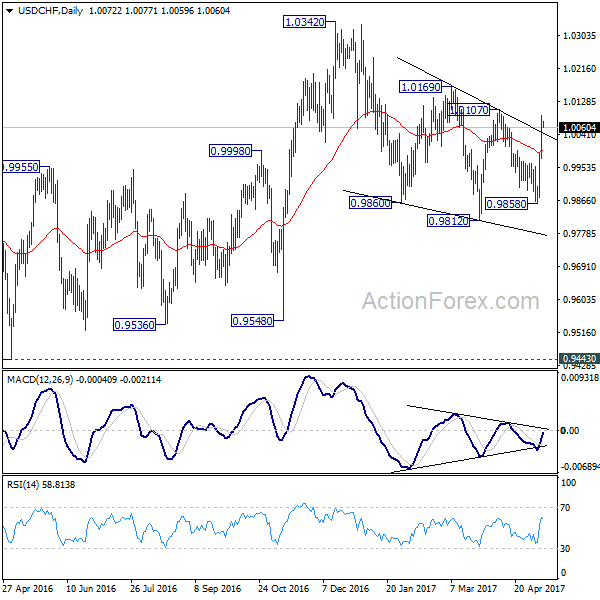

USD/CHF Daily Outlook

Daily Pivots: (S1) 1.0000; (P) 1.0045; (R1) 1.0118; More.....

Intraday bias in USD/CHF remains on the upside for 1.0107 resistance. Current development revived the case that correction from 1.0342 is already completed at 0.9812. Break of 1.0107 will bring a retest on 1.0342 high. On the downside, below 1.0037 minor support will turn bias neutral and bring consolidation first before staging another rise.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

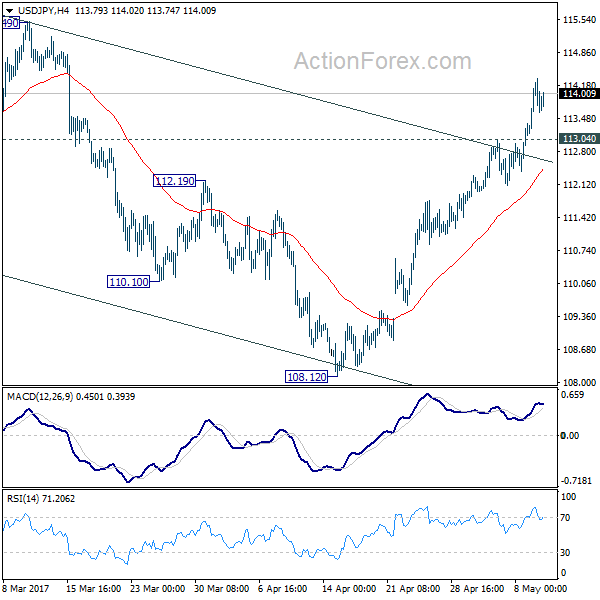

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.30; (P) 113.82; (R1) 114.50; More...

Intraday bias in USD/JPY remains on the upside for 115.49 resistance next. Outlook remains unchanged that correction from 118.65 has completed with three waves down to 108.12. Break of 115.49 will resume larger rally from 98.97 to 125.85 high. On the downside, below 113.04 minor support will turn bias neutral and bring consolidations before staging another rally.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Daily Technical Analysis: EUR/USD Breaks RW And Builds First Bearish Wave

Currency pair EUR/USD

The EUR/USD broke the support trend line (dotted blue) of the rising wedge (RW) reversal chart pattern (red/blue). The bearish breakout could be part of a larger reversal, which is reflected in the 1-2 wave count (brown). The alternative scenario would be a bearish retracement within a larger uptrend continuation, which at the moment would require a break above the top.

The EUR/USD wave 4 (blue) respected the shallow Fibonacci level of 23.6% before breaking support (dotted blue) and price has reached the 61.8% Fibonacci target of wave 5 (blue). Price could either retrace as part of wave 2 on 4 hour chart or break the bottom and continue with 5 (blue).

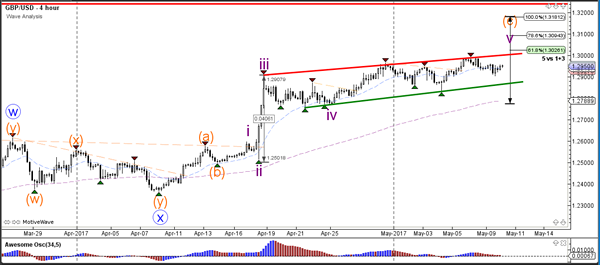

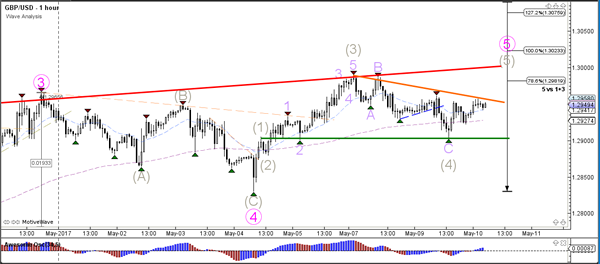

Currency pair GBP/USD

The GBP/USD is moving higher in an uptrend channel which is indicated by the support (green) and resistance (red) trend lines. A bullish break could see price move towards the Fibonacci targets of wave 5 (purple) whereas a bearish break could start a reversal.

The GBP/USD tested the previous top (green) of wave 1 (grey) but did not break and therefore the wave 4 (grey) could still be valid. A break above resistance (orange) could see a bullish break for wave 5 (grey).

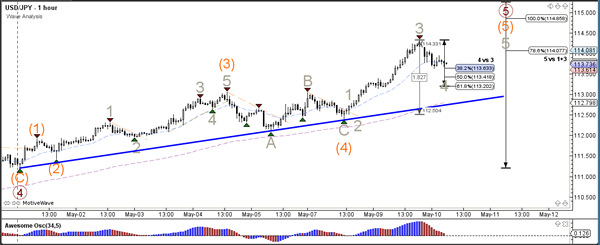

Currency pair USD/JPY

The USD/JPY is building an uptrend channel which is indicated by the support (blue) and resistance (red) trend lines and moving towards the Fib targets of wave 5 (brown).

The USD/JPY is extending the bullish 5th wave (brown/orange) with another 5 waves (grey). The wave 4 (grey) is invalidated if price breaks below the 61.8% Fibonacci level.

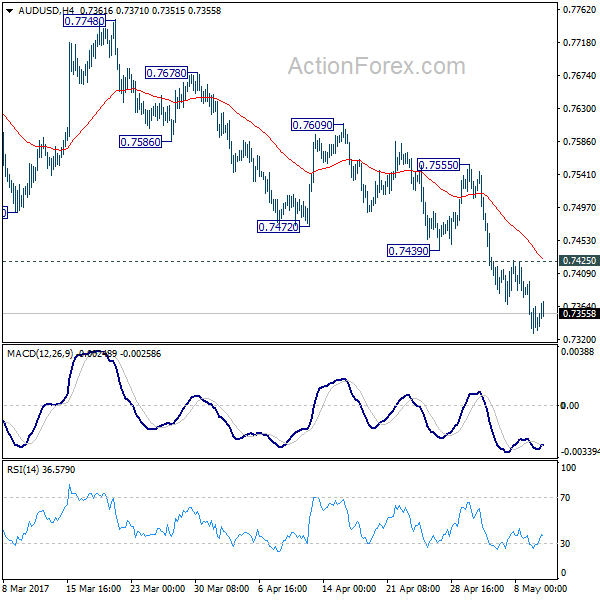

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7315; (P) 0.7357; (R1) 0.7384; More...

Intraday bias in AUD/USD remains on the downside for the moment. Current fall from 0.7748 is expected to target a test on 0.7144/7158 support zone. We'll be cautious on bottoming there as there is no clear sign of larger down trend resumption yet. On the upside, above 0.7425 minor resistance will turn bias neutral and bring consolidations first.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8115) and above.

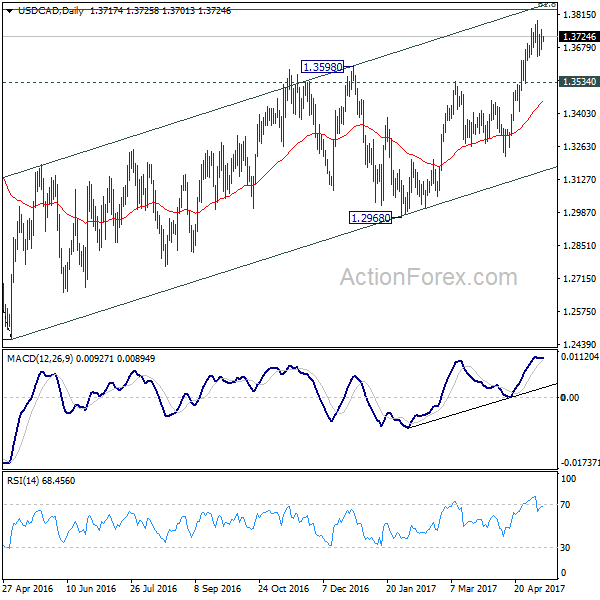

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3674; (P) 1.3714; (R1) 1.3757; More....

Intraday bias in USD/CAD remains neutral as it's staying in consolidation below 1.3793 temporary top. Rise from 1.2460 is seen as a corrective pattern. Hence, in case of another rally, we'll be cautious on topping at around 1.3838 fibonacci level. Meanwhile, consider bearish divergence condition in 4 hour MACD, break of 1.3534 support will argue that rise from 1.2968 is already completed. In such case, intraday bias will be turned back to the downside for 1.3222 support.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and would end at around 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should indicate the start of the third leg while further break of 1.2968 should confirm. Nonetheless, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

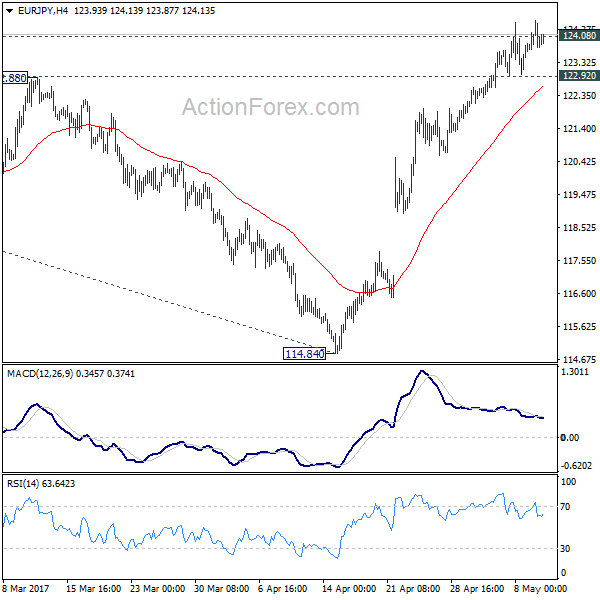

EUR/JPY Daily Outlook

Daily Pivots: (S1) 123.55; (P) 124.04; (R1) 124.45; More...

No change in EUR/JPY's outlook despite diminishing upside moment as seen in 4 hour MACD. Further rally is expected with 122.92 minor support intact. Firm break of 124.08 resistance will confirm resumption of whole rise from 109.20. In that case, EUR/JPY would target 126.09 resistance first. Break there will pave the way to 100% projection of 109.03 to 124.08 from 114.84 at 129.89. On the downside, below 122.92 minor support will turn bias to the downside and bring pull back.

In the bigger picture, focus is back on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

Chinese PPI And CPI Inflation Figures Have Been Released This Morning

Market movers today

With a thin global calendar, focus is on Scandinavia inflation with the release of the Danish and Norwegian figures for April. The Danish figure should be unchanged but the Norwegian print is more interesting after weak inflation in recent months has prompted markets to shift the spot light from oil and growth to inflation. We estimate core inflation climbed to 1.9% y/y, well below Norges Bank's projections in its last monetary policy report (2.1%) but this could still allay some of the fears that inflation will fall far enough to trigger further rate cuts.

In Sweden, the Riksbank minutes from the last monetary policy meeting will be released. The minutes will be followed closely as they cover the meeting when the Riksbank surprisingly decided to extend the QE programme. The Swedish Prospera inflation expectations are also due for release today.

ECB president Draghi is scheduled to speak in the Dutch parliament in the afternoon and focus will be on whether the latest jump in core inflation as well as Macron winning the French presidency have changed the ECB's monetary policy stance. In our view, the elimination of the Frexit risk has paved the way for a more hawkish communication at the next ECB meeting in June, but regarding the inflation out look, we expect the ECB to await more information in judging whether the latest rise is due to the timing of Easter or higher underlying price pressure.

Selected market news

Former French prime minister, Manuel Val ls, has reported he wants to run under president-elect Macron's new political movement i n th e upcoming parliamen tary election. Macron aims to put candidates up in all 577 constituencies and the candidates are expected to be announced on Thursday. the election out come will be decisive for how much of Macron's policy proposals he can actually implement and the risk remains that Macron's parliamentary majority will be unstable and fragmented, see Research France: Clouds lift over Europe after Macron wins presidency, 8 May.

Chinese PPI and CPI inflation figures have been released this morning and confirm our view that some of the engines fuelling reflation are losing steam. PPI inflation fell sharply to 6.4% y/y in April from 7.6% in March and below consensus expectations at 6.7%. Hence, it seems PPI inflation peaked at the beginning of the year when it was quite high due to the big increases in commodity prices in 2016. The peak in commodity price inflation was one of the reasons we believed the reflation theme was fading, see Research: Global reflation set to lose steam, 3 April.

US President Trump has fired FBI director James Comey at a time when the agency was investigating Russia's i nterference in l ast year's election, see Bloomberg. Democrats alleged it was an effort to cut short the Russia probe and demanded a special prosecutor to carry the process forward.