Sample Category Title

Eco Data 5/8/17

[php_everywhere] [/php_everywhere]

Summary 5/8 – 5/12

Monday, May 8, 2017

[php_everywhere] [/php_everywhere]

Tuesday, May 9, 2017

[php_everywhere] [/php_everywhere]

Wednesday, May 10, 2017

[php_everywhere] [/php_everywhere]

Thursday, May 11, 2017

[php_everywhere] [/php_everywhere]

Friday, May 12, 2017

[php_everywhere] [/php_everywhere].

Weekly Economic and Financial Commentary

U.S. Review

The Economic Narrative Carries into Q2

- The ISM manufacturing index dipped in April but remained firmly in expansionary territory, while its services counterpart rose to a solid 57.8 reading.

- At the conclusion of the FOMC's May meeting, the committee chose not to raise the fed funds rate. Language in the policy statement, however, signaled that the Fed views the Q1 economic slowdown as transitory, potentially teeing up a rate hike in June.

- Employers added 211,000 new jobs in April, topping expectations. Both the U-3 and U-6 unemployment rates fell to cycle-lows, but wage growth was slower than expected.

The Economic Narrative Carries into Q2

Economic data released this week contained some of the first information available for Q2. To kick off the quarter, the ISM manufacturing index showed factory sector activity had cooled a bit in April. The reading of 54.8 was the third consecutive decline and was lower than consensus. At 54.8, however, the index remains firmly in expansion territory and signals a clear improvement relative to the past couple years (top chart). The multi-year high of 57.7 reached in February would be consistent with a much-stronger rate of growth than we have been forecasting, so the return to a more sustainable pace of expansion suggested in this report for April is consistent with our forecast.

On Wednesday, the ISM's service sector counterpart topped expectations, rebounding to 57.8. The new orders index climbed 4.3 points to post its current cycle-high of 63.2. Demand was boosted by better global economic conditions, as new export orders jumped 3 points to 65.5, just a half point below the alltime high for the series. Taken together, the underlying trend for these two indicators suggest that the slowdown in economic growth in Q1 was transitory and a rebound in Q2 is in the offing.

Labor productivity data were also released this week. Over the long-run, economic growth is driven by two factors: the growth in the labor force, and the growth in the productive capacity of these workers. As illustrated in the middle chart, labor productivity growth has been persistently slow in recent years. The data for Q1-2017 largely reinforced this narrative. Nonfarm productivity declined at a 0.6 percent annualized rate in Q1. The year-overyear pace remained steady at 1.1 percent. Amid slow productivity growth and an aging population, achieving sustainable economic growth faster than 2-2.5 percent a year will be challenging.

Against this backdrop, the Fed refrained from raising the fed funds rate at its May meeting. Similar to our view, the Fed's policy statement reinforced the belief that the slowdown in economic growth in Q1 was transitory. In addition, the Fed tweaked its view on inflation, choosing to focus on the recent 12-month change in various inflation measures rather than the performance over recent quarters, as was done following the March meeting. Both the headline and core PCE deflators ticked down on a year-ago basis in March, but at 1.8 percent and 1.6 percent respectively, inflation remains close to the two percent target. The bottom line is the Fed still sees economic activity, the labor market and inflation on course with its expectations, which positions the Fed to raise the fed funds rate in June.

Finally, the employment report this morning showed 211,000 new jobs were added in April. Job gains were generally broadbased, and both the U-3 and U-6 unemployment rates fell to new cycle-lows. Furthermore, despite a slight decline in the total labor force participation rate, the participation rate for prime-age workers actually rose in April, keeping a broader upward trend intact (bottom chart). However, wage growth disappointed relative to consensus. On balance, today's report is supportive of a June rate hike, but the tepid acceleration in wages will likely reinforce the Fed's cautious approach to tightening policy.

U.S. Outlook

Import Prices • Wednesday

Lower prices for imported energy weighed on headline import prices in March, which declined 0.2 percent from February. March was the first decline in four months as the recovery in oil prices slowed. Excluding petroleum, import prices rose 0.2 percent on the month amid strengthening in the business sector, with rebounds in industrial supplies and capital goods driving the nonfuel import price recovery. Revisions to earlier data revealed some easing in the rate of goods deflation in the CPI may be in the offing. Exporters continue to benefit from improved global demand and a more stable dollar allowing further export price increases. Export prices increased in March at the strongest year-over-year pace since 2012. We expect headline import prices declined again in April on continued softness in petroleum prices.

Previous: -0.2% Wells Fargo: -0.1% Consensus: 0.2%

CPI • Friday

Gasoline prices played a large role in March's 0.3 percent decline in the headline CPI. That said, the core CPI also unexpectedly declined in March as consumers paid less for wireless telephone services on the month. Shelter and medical inflation also eased in March, which usually provide a greater lift to core services prices. Core goods declined 0.3 percent on softer apparel and transportation prices. The decline in apparel prices looked to be payback from early outsized gains, but softness in transportation goods prices is unlikely to abate, particularly as the glut of used vehicles coming off lease this year weighs on vehicle prices.

We expect both the core and headline CPI to rise 0.2 percent in April as much of the softness in March could be attributed to oneoff factors, such as the drag from the unusually large decline in wireless services on core services inflation.

Previous: -0.3% Wells Fargo: 0.2% Consensus: 0.3%

Retail Sales • Friday

We expect retail sales bounced back in April after a disappointing start to the year. Retail sales declined 0.2 percent in March after falling 0.3 percent in February. The declines were largely due to the auto sector, as retail sales ex auto were flat both months. Sales were also likely affected by unusual weather patterns affecting the timing of purchases at home and garden stores. Gasoline stations and food and drinking places also saw sales decline in March.

Control group sales, used to calculate GDP, were volatile in recent months, and we know from the first look at Q1 GDP that personal consumption did indeed soften in the first three months of the year. That said, underlying fundamentals support our call for a rebound in coming month due to the strong job market and income gains. However, we doubt the auto sector will be as supportive as in recent years as sales likely hit its peak in 2016.

Previous: -0.2% Wells Fargo: 0.5% Consensus: 0.6%

Global Review

Mixed Data on the Global Economy

- We received mixed data from the global economy in April with the Caixin China manufacturing PMI coming in at a lower level than expected, 50.3, versus expectations of 51.3 and lower than the previous month.

- Meanwhile, Eurozone GDP expanded at a 0.5 percent clip, not annualized (which represents a 1.8 percent annualized rate), in the first quarter of the year and in line with consensus expectations. On a year-earlier basis, real GDP was up 1.7 percent.

- The Brazilian industrial production index for March also disappointed when it stumbled 1.8 percent versus February, seasonally adjusted.

Mixed Data on the Global Economy.

We received mixed data from the global economy in April with the Caixin China manufacturing PMI coming in at a lower level than expected, 50.3, versus expectations of 51.3 and lower than the previous month. The lower reading was disappointing at the start of the second quarter. Furthermore, the services PMI was also lower than the March reading, down to 51.5 versus 52.2 in March. That is, this first reading from the manufacturing and service sectors from the second largest economy in the world does not bode well for overall economic growth. Having said this, both indices remained in expansion territory even though the manufacturing index was very close to the 50 demarcation line.

Meanwhile, the Eurozone expanded at a 0.5 percent clip, not annualized (which represents a 1.8 percent annualized rate), in the first quarter of the year and in line with consensus expectations. On a year-earlier basis real GDP was up 1.7 percent. Thus, growth in the Eurozone agreed with expectations and has remained relatively stable recently, which is good for overall global economic growth but not a growth rate that could set off stronger economic growth across the global economy.

At the same time, markets were celebrating the fact that all the political pundits gave Emmanuel Macron an edge over Marine LePen during the first and only French presidential debate ahead of this weekend second round presidential elections. Thus, today, markets are betting that Mr. Macron will be elected president of France and the European Union will probably breathe a sigh of relief as Mr. Macron supports France's continuity in the European Union and in the euro area. Furthermore, if Mr. Macron wins, the country will prevent an extreme rightist party from taking over the presidency in the second largest country in the Eurozone.

Meanwhile, in this hemisphere, the Brazilian industrial production index for March disappointed when it stumbled 1.8 percent versus February, seasonally adjusted. On the positive side, industrial production still managed to increase 1.1 percent versus a year earlier and non-seasonally adjusted. However, this year-over-year comparison is not a very good gauge of the conditions of the sector because it is comparing a full month of industrial production this year with March of last year, which was shorter because of Easter week. At the same time, manufacturing production was also very weak, down 1.7 percent versus February and up only 0.2 percent compared to March of last year.

In Mexico, gross fixed investment in February disappointed once again, coming in lower by 0.8 percent after falling 1.8 percent in January, both seasonally adjusted. On a year-over-year comparison, gross fixed investment in Mexico dropped 3.1 percent, the largest decline since June of last year. Thus, if the better than expected flash result for first quarter GDP is confirmed later this month it will mean that other components of GDP must have been very strong and/or that gross fixed investment recovered strongly in March to close the quarter.

Global Outlook

Canada Housing Starts • Monday

Canadian housing starts raced ahead of market expectations of a 215,000-unit increase in March and instead jumped over 18 percent over the month to a 253,200-unit pace. March's starts marked the highest level since September 2007, with much of the increase coming from multifamily homes and condominiums in urban areas, which rose 30.2 percent to a 160,989-unit pace. Single-family homes, on the other hand, rose by a more moderate 3.1 percent to a 74,685-unit pace. Housing has been a main driver in Canada's economy over the past several years due to historically low interest rates and larger metros, such as Toronto and Ottawa, seeing their housing markets heat up. That said, consensus is expecting some payback from March's surge, and looks for starts to have come back down to a more modest 220,000-unit pace in April.

Previous: 253,200 Consensus: 220,000

U.K. Bank of England Rate • Thursday

Economic growth in the U.K. downshifted in Q1, weighed down by softening in the service sector which suggests that consumer spending started the year on a weaker note. In addition, CPI inflation has started to pick up, helped by the rebound in energy prices, and core CPI has moved higher as well. The jump in prices has started to eroded real income growth and reduced growth in consumer spending, which we expect to remain a headwind for the U.K. economy.

At the Bank of England's meeting next week, we look for the Monetary Policy Committee (MPC) to keep its bank rate unchanged at 0.25 percent and remain on hold through 2017 due to the slowing growth and rising inflationary pressures the economy is facing. Although shifting inflation dynamics could cause some of the MPC members to sanction a rate hike sooner rather than later, the current accommodative stance will likely remain in place.

Previous: 0.250% Wells Fargo: 0.250% Consensus: 0.250%

Mexican Industrial Production • Friday

Mexican industrial production (IP) increased 0.1 percent on a monthly basis in February as mining output weighed on overall growth. Construction activity rebounded over the month, rising 0.9 percent and rose an even stronger 3.0 percent year over year. Meanwhile, the mining sector has declined even further, falling 13.7 percent on a year-ago basis. Conversely, growth in the manufacturing industry remained relatively stable at 1.1 percent. Mexico's preliminary Q1 GDP, which printed earlier this week, showed that the secondary sector (includes industrial production) contracted 1.3 percent on a year-ago basis.

Other data on the docket next week include consumer price inflation, which has been running hot lately, rising to 5.4 percent year over year. Markets look for it to rise to 5.8 percent in April.

Previous: -1.7%

Point of View

Interest Rate Watch

Looking Past the First Quarter

The Federal Reserve went out of its way to downplay the slowdown in first quarter real GDP growth, stressing that the rate of growth has slowed rather than economic activity had slowed. Their policy bias remains toward gradually nudging interest rates higher and the financial markets are currently assigning a better than 90 percent probability that the Fed hikes the federal funds rate by a quarter point at the June 13-14 FOMC meeting.

The policy statement from the May meeting contained few surprises. The explanation of current economic conditions essentially stressed that the labor market is continuing to improve solidly and that business investment had firmed. The statement did note that household spending had increased "only modestly' but went on to say that the underlying fundamentals supporting consumer spending remained solid. The bottom line is that Fed will continue to tighten as long as employment conditions remain strong.

The April employment numbers were right in line with the Fed's expectations. Not only did nonfarm employment bounce back, as was expected, but the unemployment rate also fell to 4.4 percent. Job gains were fairly broad based and aggregate hours worked rose by a solid 0.5 percent, suggesting that real GDP will also bounce back in the second quarter.

The drop in the unemployment rate to 4.4 percent may set off concerns that the Fed will accelerate efforts to normalize interest rates. Right now, such a move would be premature. While the unemployment rate has surprised to the downside, wage and salary gains show very little sign of strengthening.

One possible explanation for the lack of wage growth is that the labor force participation rate for prime-working age persons is still well below its historic norms. This may be changing. There has been a notable acceleration in hiring in full-time positions and slowing in part-time jobs. This shift has coincided with an increase in household formations and home ownership. The Fed may not want to stomp this out just as it is getting started.

Credit Market Insights

Mortgage Credit & Rates Hold Steady

Mortgage credit availability was relatively unchanged in April, according to recently released data from the Mortgage Bankers Association's Mortgage Credit Availability Index (MCAI). After rising to a fresh cyclehigh in March, the MCAI fell a slight 0.2 percent to 183 in April. A decrease in the MCAI indicates that lending standards are tightening, while an increase signals they are loosening. Despite the modest dip, the indicator of mortgage credit access remains on an upward trend and has generally risen since hitting a bottom in 2011. That said, on a historical basis, mortgages are still relatively difficult to obtain. While stricter lending conditions have diminished default rates, the mortgage market's tight credit box has proved to be a headwind to the current cycle's housing recovery.

Meanwhile, mortgage rates—another measure pertaining to borrowers' ability to purchase a home—held fairly steady this week. According to Freddie Mac, the 30-year conventional fixed mortgage rate edged down a slight 0.1 percentage point to 4.02 percent during the week ending May 4. The 30-year mortgage rate has been trendless near 4 percent for the past four weeks. Against the backdrop of anticipated Fed tightening, we expect a modestly higher interest rate environment in the near-term. That said, we expect housing demand to trump the modest increase in interest rates, and look for home sales to continue to trend higher over the course of the year.

Topic of the Week

Shutdown Showdown Ends Quietly

Legislators agreed this week to a budget deal that funds the government through the end of fiscal year (FY) 2017, which ends Sept. 30. The agreement is largely devoid of the more controversial policy proposals that had the potential to derail the bill. Deep cuts to nondefense discretionary spending were avoided, and no funds were appropriated for a border wall. Defense spending received a $15 billion boost, although this was a smaller increase than what the White House had requested.

However, with the current fiscal year already more than halfway complete, policymakers will need to revisit this issue in the near future. In just five months, policymakers will once again need a plan to fund the government for FY 2018. Furthermore, the debt ceiling has the potential to add another wrinkle to the next round of negotiations. The spending bill agreed to this week does not increase the debt ceiling, which was reestablished on March 15. For the time being, this is not a major problem as the Treasury has the capacity to take "extraordinary measures" to remain solvent through the fall. A better understanding of how long the Treasury can operate under these circumstances will become clearer as spring tax collection data become available. The timeline suggests that this fall policymakers will face the dual challenge of passing a budget and raising the debt ceiling, a challenging lift during a period when legislators hope to be in the middle of a tax code rewrite.

In addition, legislators also revived their efforts to repeal elements of the Affordable Care Act (ACA). The passage of the ACA repeal bill is a significant accomplishment for Republicans, but it is important to remember that this is just one bar among several more that must be hurdled. The bill now heads to the Senate, where its fate is far from clear and Republicans hold just a two seat majority. If the Senate manages to successfully craft its own version, a conference committee between the two chambers would then have to hash out the differences. The more time spent on an ACA repeal bill, the less legislative calendar time will be free to tackle tax reform.

The Weekly Bottom Line

HIGHLIGHTS OF THE WEEK

United States

- The past week was action packed with economic data and events in Washington. Data largely supported the view that the U.S. economy will bounce back from its winter weakness.

- The job market sprang back into action in April, enabling investors to heave a sigh of relief that the fundamentals remain in place for a Q2 rebound. The Fed expressed its confidence in the economy in its statement accompanying its stand pat rate decision.

- Still, weak auto sales and a recent loss in inflation momentum suggest the U.S. economy is not entirely out of the woods. The Fed will be watching the data closely in the coming weeks before the case for a June hike is cemented.

Canada

- An 8% drop in crude oil prices led the S&P/TSX to a 6-week low and took the loonie below 73 US cents for the first time in over a year.

- The Canadian economy added just 3k jobs in April. The unemployment rate fell to 6.5% as 45k people left the workforce. Wage growth slowed to a record low of just 0.5% y/y.

- Auto sales slipped 1.6% y/y in April, but this follows a record breaking quarter. Sales remain quite elevated relative to historical norms.

- Exports bounced back in March, helping to narrow Canada's trade deficit. However, net trade will still be a drag on growth during the first quarter.

UNITED STATES - ECONOMY SHOWING SIGNS OF SPRING THAW

From Washington to Wall street, there was no shortage of news for investors to digest this week. Data largely supported the view that the U.S. economy is bouncing back from its winter weakness. Markets have one eye turned on policy shifts in Washington too, where the GOP took baby steps towards repealing and replacing Obamacare (ACA). The revised American Health Care Act (AHCA) passed the House by a very narrow margin, but faces a bigger challenge in the Senate.

Investors heaved a sigh of relief on Friday as the job market bounced back in April, bearing out the Fed's confidence in the economy expressed in Wednesday's rate announcement. Payrolls advanced 211k jobs in April and the unemployment rate fell to 4.4% - the lowest level since 2007. Broader measures of labor market slack also declined, with the broadest U6 measure (including discouraged workers and involuntary part-timers) falling to 8.6%, just 0.2 percentage points off its pre-recession level (Chart 1). Average hourly earnings rose 0.3%, as expected in April. That left wages up 2.5% over a year ago, not yet flashing red, but is still sufficient to provide real gains in purchasing power (Chart 2). This should flow through to consumer spending in the months ahead, providing the impetus for stronger economic growth.

As expected, the Fed kept interest rates unchanged on Wednesday and issued a largely status quo statement. It pointed to continued improvement in the labor market, while seeing through disappointing economic growth in the first quarter. The weakness in inflation in March was noted, but one-month's result is unlikely to sway the Fed. As Yellen has continually emphasized, the Fed's path is data dependent. So, members will be watching the data closely over the next few weeks as indicators for the second quarter are released. If the numbers confirm that a second quarter rebound is underway, and that the slowdown in inflation has not become more entrenched, we would expect the Fed to take rates higher in June.

So far this year, measures of sentiment have been more ebullient than the "hard" economic data. Not surprisingly, the ISM Manufacturing index did lose of bit of its postelection optimism in April. We have raised concerns that markets might have been a bit overconfident that Washington could easily implement highly stimulative fiscal policy. While this week, the House finally passed a bill to repeal and replace the ACA, this is only the first step in an ongoing process. Passage in the Senate where the Republican majority is even slimmer, will prove much more difficult.

Passing healthcare reform into law is arguably a necessary pre-condition to making further changes to the tax code. This is because the savings achieved leave room to cut taxes without expanding the deficit. The Congressional Budget Office has not yet scored the new bill, but the previous bill reduced the deficit by over $330 billion over the next decade. This is only about one-tenth of what is necessary to pay for Trump's proposed tax cuts, but it might allow for some reduction in the corporate tax rate. In any case, there is a long road ahead on forging consensus on both the AHCA and eventually tax reform, leaving the potential for further sentiment disappointments in the months ahead.

CANADA - PLUNGING OIL PRICES WEIGH ON FINANCIAL MARKETS

It was a rough week for Canadian financial markets, as the S&P/TSX index and the Canadian dollar were pulled down by an 8% plunge in crude oil prices to US$45 per barrel. The equity market hit a 6-week low, while the loonie fell below 73 US cents for the first time in over a year.

Oil prices have now fallen by 15% in just three weeks, reaching the lowest level seen since November 2016 - right before OPEC members agreed on production cuts. The drop stemmed from concerns surrounding the global supply glut, as efforts by OPEC and a group of non-OPEC countries to scale back production have yet to put a meaningful dent in global stocks. Meanwhile, production elsewhere - particularly in the U.S. - has been on the rise. Indeed, U.S. oil production continues to expand, now sitting at 9.3 million barrels per day - a level not seen August 2015. OPEC will meet on May 25th to determine whether production quotas will be extended past June. Indications from the cartel suggest that they will, however, it appears as though markets are starting to think that bigger cuts will be necessary to bring the market back into balance. Volatility in oil prices is likely to continue as the meeting approaches, moving in response to rhetoric coming from OPEC and U.S. production and inventory data.

On the economic front, data out this week was mixed. The Canadian economy added just 3k jobs in April, all part-time, and wage growth slowed to 0.5% y/y - half of its first-quarter pace and the slowest pace on record. While a disappointing report, it does follow several months of strong job creation.

Auto sales were down 1.6% versus year-ago levels, but the drop comes on the heels of a record-breaking first quarter and is contending with last year's stellar performance when sales topped 200,000 units for the first time in a single month. Needless to say, even with a slight pullback in April, auto sales remain quite elevated. That said, given the remarkable strength seen in recent years, it would not be surprising to see auto sales lose some steam in the coming months.

International trade data showed a bounce back in export volumes in March, while imports edged down slightly. This won't be enough to prevent net trade from weighing on economic growth during the first quarter - thanks to rebounding imports - but it does provide a solid hand off for Q2. Moreover, momentum in exports should continue going forward, as the Canadian dollar remains under pressure and economic activity in the U.S. is set to pick up after a slow start to the year.

This will help underpin the rotation in Canadian growth drivers away from stretched consumers and housing, toward a more balanced growth path. In a report released this week, we noted that stabilization in non-residential investment and a modest improvement in other business investment, combined with a better net trade performance should offset expected declines in housing activity over the remainder of this year, keeping the economy advancing at a decent clip of just under 2%. The Bank of Canada will be looking for such signs of a more sustainable growth path before moving off the sidelines.

Week Ahead Dollar Softer Despite Strong US Jobs Report

US retail sales and inflation next up for the USD

The US dollar did not have a strong finish for the week despite employment rising by more than expected with a 211,000 jobs gain in April. The unemployment rate fell to 4.4 percent (the lowest since 2007) but wage growth remains tepid with a 0.3 percent monthly gain. Economists are confident that the reduction in the labor market slack will ultimately result in higher wages. The lack of inflationary pressures in the jobs report will not be enough to derail the June interest rate hike by the Fed.

The US Bureau of Labor Statistics will release the consumer price index (CPI) on Friday, May 12 at 8:30 am EDT. The inflation gauge is expected to expand by 0.2 percent after last month's contraction. The metric preferred by U.S. Federal Reserve officials is the core CPI with a 0.2 percent gain forecast excludes food and energy products. US retail sales will be published by the Census Bureau and big gains are anticipated as warmer weather is expected to have boosted consumption. Last month core retail sales was flat, while the headline figure contracted by 0.2 percent. In April there is a 0.5 percent gain for core and 0.6 percent for retail sales forecasted.

The central banks of New Zealand and England will issue rate statements next week. The Reserve Bank of New Zealand (RBNZ) will deliver its rate statement on Wednesday, May 10 at 5:00 pm EDT and the Bank of England (BoE) will kick off its super Thursday on May 11 at 7:00 am. The two central banks are expected to hold but the market will look to their press conferences to more insights on their monetary policy plans. Italy will host the upcoming G7 Finance Ministers and Central Bank Govenors meeting in Bari from May 11 to 13. While Syria was the main talking point during the meeting between foreign ministers the Finance summit will likely touch on trade with the Brexit process is under way and concerns rising about NAFTA renegotiation between the US and Canada.

The EUR/USD gained 0.777 percent during the week. The single currency is trading at 1.0987 after a period that was high on political risk with the French presidential elections entering their final stretch. The televised debate between the two candidates was an entertaining affair but failed to change the odds by much. Emmanuel Macron is still favoured to win with a 62 percent of the vote going his way according to the polls. The lessons from the Brexit and Donald Trump results are still fresh in the minds of investors. Trust in pollsters is still low, regardless of the good results in the Dutch election.

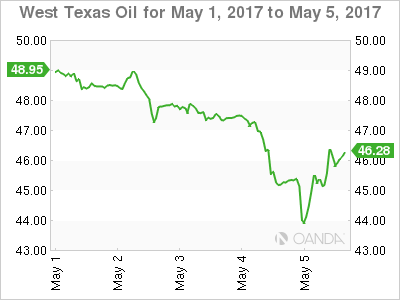

Oil managed to advance 1.081 percent on Friday, but is still down 6.299 percent on a weekly basis. The West Texas Intermediate is trading at $45.83 after starting eh week near $50. The lack of demand for crude and distillates has created a glut of supply despite the efforts of the Organization of the Petroleum Exporting Countries (OPEC). The organization has worked toward reaching a new agreement to extend the production cut deal that stabilized prices, but with US producers increasing activity it is questionable that even that could boost prices as the all important demand remains weak.

Gold continues to slide downward on Friday. The yellow metal is down 0.105 percent on the final day of the trading week. It is trading at $1,227.84. The precious metal lost 3.09 in the last five days as political risk was downgraded after the French presidential debate solidified the lead of Emmanuel Macron ahead of Sunday's vote. The appetite for safety has been reduced putting pressure on gold.

Market events to watch this week:

Monday, May 8

- 9:30pm AUD Retail Sales m/m

Tuesday, May 9

- 5:30am AUD Annual Budget Release

Wednesday, May 10

- 10:30am USD Crude Oil Inventories

- 5:00pm NZD Official Cash Rate

- 5:00pm NZD RBNZ Rate Statement

- 6:00pm NZD RBNZ Press Conference

- 9:10pm NZD RBNZ Gov Wheeler Speaks

Thursday, May 11

- 4:30am GBP Manufacturing Production m/m

- 7:00am GBP BOE Inflation Report

- 7:00am GBP MPC Official Bank Rate Votes

- 7:00am GBP Monetary Policy Summary

- 7:00am GBP Official Bank Rate

- 8:30am USD PPI m/m

- 8:30am USD Unemployment Claims

Friday, May 12

- All day G7 Meetings

- 8:30am USD CPI m/m

- 8:30am USD Core Retail Sales m/m

- 8:30am USD Retail Sales m/m

- 10:00am USD Prelim UoM Consumer Sentiment

- Saturday, May 13

- All day G7 Meetings

*All times EDT

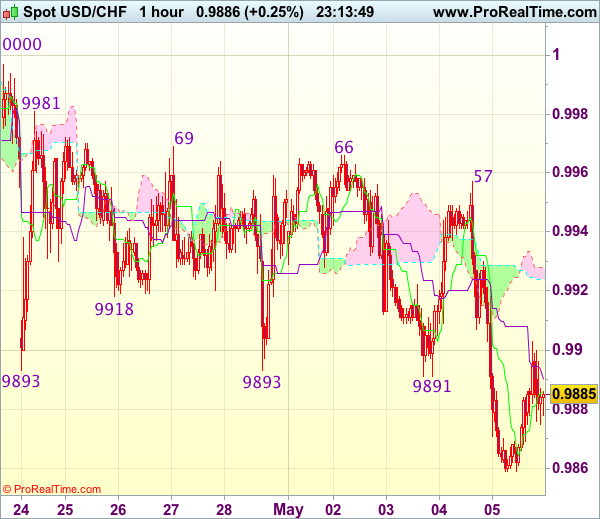

Trade Idea Wrap-up: USD/CHF – Stand aside

USD/CHF - 0.9873

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9886

Kijun-Sen level : 0.9890

Ichimoku cloud top : 0.9928

Ichimoku cloud bottom : 0.9924

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Yesterday’s selloff after meeting renewed selling interest at 0.9957 together with the breach of support at 0.9891-93 confirm recent decline from 1.0108 top has resumed and bearishness remains for further weakness to support at 0.9831 and possibly towards 0.9800, however, near term oversold condition should prevent sharp fall below 0.9770, risk from there is seen for a rebound later.

In view of this, would not chase this fall here and would be prudent to stand aside in the meantime. Above 0.9905-10 would bring recovery to 0.9925-30 but price should falter well below said resistance at 0.9957, bring another decline later. Only break of 0.9966-69 resistance would signal low is formed instead, bring subsequent bounce to 1.0000-08 later.

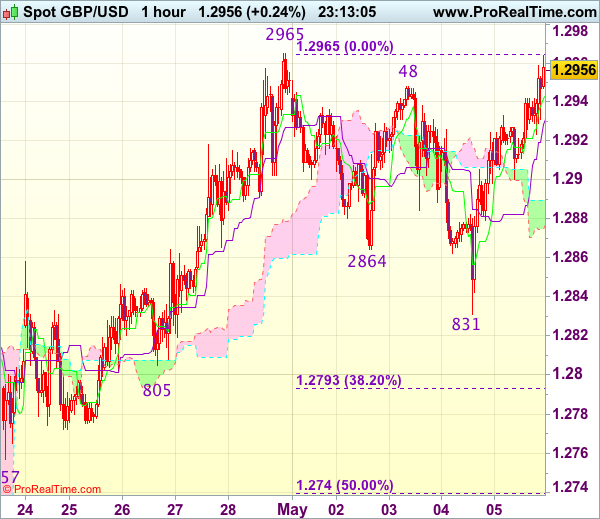

Trade Idea Wrap-up: GBP/USD – Buy at 1.2885

GBP/USD - 1.2959

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2944

Kijun-Sen level : 1.2931

Ichimoku cloud top : 1.2890

Ichimoku cloud bottom : 1.2877

Original strategy :

Buy at 1.2885, Target: 1.2985, Stop: 1.2850

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2885, Target: 1.2985, Stop: 1.2850

Position : -

Target : -

Stop : -

As cable has staged a strong rebound after finding support at 1.2831 yesterday, signaling the pullback from 1.2965 has ended at 1.2831 and retest of 1.2965 is likely, once this level is penetrated, this would confirm recent upmove has resumed and extend further gain to 1.2990-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance), then towards 1.3040-50 which is likely to hold from here.

In view of this, would not chase this rise here and would be prudent to buy cable on pullback as 1.2880-85 should limit downside and bring another rise later. Only break of said support at 1.0831 would abort and signal a temporary top has been formed, bring retracement of recent upmove to 1.2790-95 (38.2% Fibonacci retracement of 1.2515-1.2965) but support at 1.2740-50 (50% Fibonacci retracement) should hold.

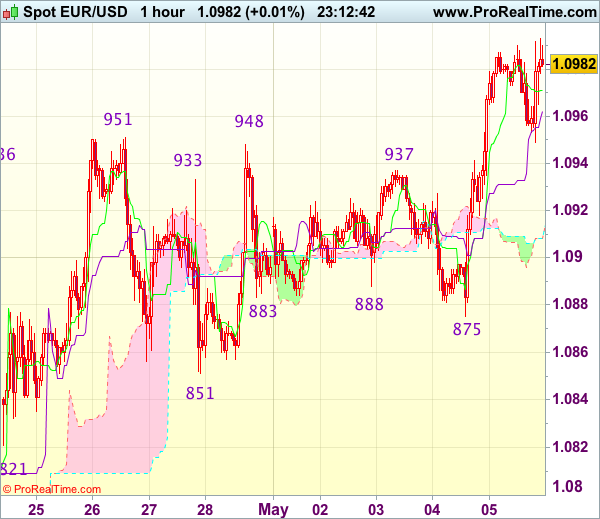

Trade Idea Wrap-up: EUR/USD – Buy at 1.0920

EUR/USD - 1.0990

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0971

Kijun-Sen level : 1.0962

Ichimoku cloud top : 1.0908

Ichimoku cloud bottom : 1.0908

Original strategy :

Buy at 1.0920, Target: 1.1020, Stop: 1.0885

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0920, Target: 1.1020, Stop: 1.0885

Position : -

Target : -

Stop : -

Euro finally broke above indicated resistance at 1.0951 (last week’s high), confirming our view that recent upmove from 1.0340 low has resumed and bullishness remains for this move to extend further gain to 1.1000, then towards 1.1025 (50% projection of 1.0602-1.0951 measuring from 1.0851) but reckon upside would be limited to 1.0050-60, risk from there is seen for a retreat later.

In view of this, would not chase this move here and would be prudent to buy euro on subsequent pullback as 1.0915-20 should limit downside. Only below support at 1.0875 (yesterday’s low) would abort and signal top is formed instead, bring correction to support at 1.0851 but price should stay above 1.0821 support, bring another rise later.

AUD In The Doldrums As Commodities Slide

- Long EM Asia - Peter Rosenstreich

- AUD In The Doldrums As Commodities Slide - Arnaud Masset

- Markets Are Very Confident About A Fed Rate Hike In June - Yann Quelenn

- Weed

Economics - Long EM Asia

Asia emerging markets asset have been benefiting from continual improvement of risk appetite and solid external and domestic fundamental data. Last week marginal correct was due to uncertainty around the French elections, weaknesses in commodity prices as China further tightening financial conditions. In addition the specter of seasonal selling in May weigh on investors mind. However, we suspect these issues are transitional and should fade in investors' minds as conditions stabilize favorably. EM Asia should return to positive performance especially against the JPY which is challenged to hold investors' attention as US interest rate rise.

KRW has borne the brunt of much external noise selling. Rising tension with North Korea, political scandal, fear of restrict trade policy, worries that relative growth rates would decline sent KRW lower. On 9th May South Korea is scheduled to holds its Presidential elections. Since there is no transition between governments, this will lower the current period of political uncertainty. The polls indicate that Moon Jae-in would bring the liberal party back into power after 10 years. A smooth political process will help regain confidence and support KRW moving forward.

Indonesia GDP growth improved marginally in 1Q 2017 rising to 5.01% y/y from 4.9% in 4Q, yet the read was slightly weaker than expected (5.1%). Despite solid export performance and government consumption growth remains sluggish. However, Bank of Indonesia provided some hawkish commentary, the outlook for tighter monetary policy seem unlikely. We anticipate the BI will continue to focus on supporting growth, capping inflations and managing IDR volatility.

While we don't expected any proactive hikes, as growth remains suboptimal (yet sudden pickup could easily trigger a reexamination of this view), the threat of higher interest rate should provide IDR with additional fundamentals support.

Finally, in the Philippines headline inflations rise 3.4% in April (in-line with Bangko Sentrals current 2017 forecasts). Food inflations remained elevated at 4-2% from 4.0% in March. We remain focused on the potential upside in inflations especially form government promoted tax reforms. With growth and inflation trending positively we could see the BSP starting increase rates before EM Asia hiking cycle really kicks off. A strong reason to position yourself long PHP.

Economics - AUD In The Doldrums As Commodities Slide

The Australian dollar has been, by far, the worst performer last week among the G10 complex. The Aussie collapsed to 0.7368 against the greenback, the lowest level since January 11th. The free-fall of the Aussie is due to the combination of several factors ranging from disappointing economic data, central bank announcement to falling commodity prices.

Last Tuesday, the Reserve Bank of Australia held unchanged the official cash rate target at record low 1.50%. The decision was broadly anticipated by market participants. Therefore they focused on the tone of the statement as they tried to get some hint about the institution's next move. The tone was slightly more positive than a month ago as Governor Lowe highlighted the positive trend in employment growth. However, the central bank reiterated its cautious stance as core inflation is still running low and has shown little sign of improvement recently: core gauge printed at 1.5% y/y versus 1.3% in the previous quarter, while headline inflation reached 2.1% y/y compared to 1.5% in the previous quarter. All in all, the RBA wants to avoid as much as possible to appear hawkish - mostly to prevent a sharp appreciation of the Aussie - even though it cannot turn a blind eye to the recent improvements, even minor ones

Secondly, the broad debasement of commodity prices - mostly crude oil and iron ore prices - weighted on exporters such as Australia. This move has to be seen within the context of tightening financial conditions in China amid a tougher bond market regulation. In China, the price of iron ore fell 14% over the last five days, amid concerns over weak demand. Iron ore futures for delivery in September on the Dalian Commodity Exchange ended the week at CNY 461.5 a metric ton.

Finally, the market is heavily positioned on the bullish side as net noncommercial positioning, reported by the CFTC, stands at around 39% of total open interest (as of April 25th). An unwinding of those long positions - which already started - may accelerated the Aussie's debasement. AUD/USD has already broke all of its short-term supports as the market is trying to determine a bottom in the currency pair. The next key support can be found at 0.7145 (low from May 24th last year).

Title - Markets Are Confident About A Fed Rate Hike In June

The FOMC meeting was clearly the key FX event last Wednesday. The market got it right and priced in a no-rate hike. Markets already feel more confident for a rate increase at the next meeting in June. Markets' estimates are around 100% at the moment. When looking carefully at the Fed meeting statement, we can notice that the US central bank is worried about the slowing in growth but believe it is going to be transitory.

If we assess more closely the data of the US economy, the jobs report were, in average, much better. Last Friday's NFP printed above the consensus (211k vs 190k). It is nonetheless important to notice that March figure has been revised down to 79k from 98k. Other recent data were lacklustre (GDP and personal consumption in particular). The inflation target of 2% was beaten in February before falling again below this level. In March, industrial production also saw its biggest decline for the last two years.

We remain suspicious on Fed rate path tightening for this year as we believe that the state the US economy is overestimated. A few elements allow us to say so. For example, the number of bankruptcies in the US in 2017 is already higher than all bankruptcies in 2016. On top of that, the second-hand car market is collapsing as the losses on auto credit subprime have reached their highest level. Last but not least, 60% of Americans - according to a CNN poll - do not have a $500 emergency fund.

Out of this is why we maintain our bullish position on the EURUSD, despite political uncertainties in Europe. This should continue in our view as the Trump's spending plans, tax reforms are going to cost a lot and the Federal government current interest payments have never been so high. Above 508 billion dollars for the first quarter of the year.

Themes Trading - Weed

Marijuana

Yes, we all know the jokes, but marijuana is big business in North America. US comedian Jimmy Kimmel stated that Colorado's new state slogan is "Come for the legal marijuana, stay because you forgot to leave."

The North American market for weed is estimated to have grown to $53 billion in 2016. This includes legal recreational use, medical markets and the illegal trade. The legal North American marijuana market generated 2016 revenues of $6.9 billion, 34% higher than the 2015 total, largely as a result of explosive growth in adult consumer sales. There are currently 26 states plus the District of Columbia with laws broadly legalizing marijuana in some form (8 with legalization for recreational use), together with other states preparing to introduce legislation permitting marijuana use.

As of now, under federal law cannabis remains a controlled substance and illegal. For the time being, companies whose business is marijuana must obtain individual state licenses to operate and sell. This makes the evolution from small to medium-sized company and then national brand, which is critical for public listing, a challenge. However, there is a growing group of small cap stocks that have led the charge in this booming industry. To build a comprehensive, diversified portfolio, we have added cannabis producers and growers as well as biotechnology companies that have high profit potential (no pun intended) thanks to the legalization of marijuana. Please note that many of these stocks are high-risk and should be traded with caution due to illiquidity, low stock prices and a history of sharp reactions to news.

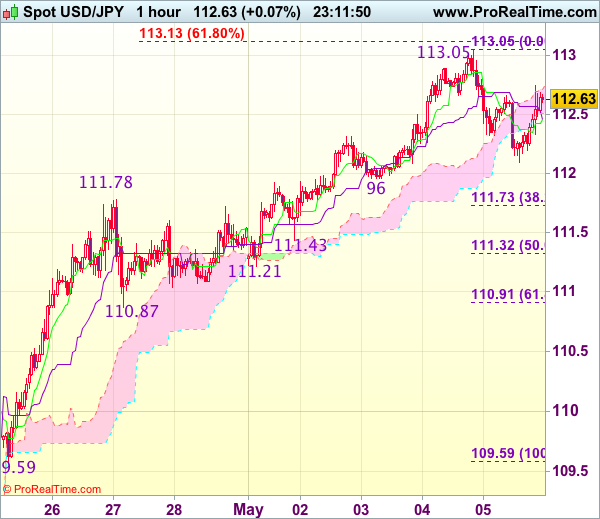

Trade Idea Wrap-up: USD/JPY – Stand aside

USD/JPY - 112.68

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.46

Kijun-Sen level : 112.46

Ichimoku cloud top : 112.71

Ichimoku cloud bottom : 112.51

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback has rebounded after finding support at 112.09 and gain towards 112.90-00 cannot be ruled out, break of yesterday’s high at 113.05 is needed to confirm recent upmove has resumed and extend gain to 113.10-15 (61.8% projection of 108.13-111.78 measuring from 110.87) but reckon upside would be limited to previous resistance at 113.54 and price should falter well below 113.90-00.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 112.09 support would bring test of 111.96 but break of this level is needed to signal a temporary top has been formed at 113.05, bring correction to 111.73-78 (38.2% Fibonacci retracement of 109.59-113.05 and previous resistance), however, reckon 111.21-32 (previous support and 50% Fibonacci retracement) would contain weakness.